|

|

市場調査レポート

商品コード

1456997

世界の移植市場-2024年から2029年までの予測Global Transplant Market - Forecasts from 2024 to 2029 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 世界の移植市場-2024年から2029年までの予測 |

|

出版日: 2024年03月02日

発行: Knowledge Sourcing Intelligence

ページ情報: 英文 128 Pages

納期: 即日から翌営業日

|

全表示

- 概要

- 目次

移植市場はCAGR 9.35%で成長し、市場規模は2022年の167億900万米ドルから2029年には312億3,800万米ドルに達すると予想されています。

移植とは、組織標本または完全な臓器を、元の場所から別の場所に移植または移転するプロセスを指します。移植された臓器や組織は、元の場所に比べて新しい、より健康的な環境で栄養を与えられ、成長します。移植プロセスは、現在の医療医療セグメントで広く採用されているプロセスです。移植プロセスは、腎臓、心臓、肝臓などの組織や臓器の場合に広く用いられています。医療セグメントで開発された移植技術は、医療セグメントに新たな発展と革新をもたらしました。慢性疾患の患者数の増加と手術件数の増加が、世界の移植市場の成長を牽引しています。人々の健康意識と意識の高まりも、世界の移植市場の成長を後押ししています。臓器バンクや臓器移植の推進における政府の支援も、世界の移植市場の成長に寄与しています。国際的な医療組織の啓発プログラムも、臓器や組織の提供を促進・奨励しており、世界の移植市場の成長に寄与しています。また、臓器登録率の上昇により、今後数年間は臓器移植の需要が高まると予想されています。臓器移植セグメントで行われている研究開発プロセスは、臓器移植市場における先進的な開発とイノベーションを生み出しています。Abbvie Inc.やArthrex Inc.などの大手企業が臓器移植に投資していることが、世界の移植市場の成長を促進しています。

市場の促進要因:

- 臓器移植需要の増加と慢性疾患患者の増加

臓器移植の需要と人気の高まりが、世界の臓器・組織移植市場の成長を後押ししています。移植法や手術が提供する効率性と移植法の成功率が、世界の移植市場の成長に可能性を与えています。PAHO(汎米保健機構)の報告によると、米国では毎年約100件以上の肺移植手術が行われています。米国保健社会福祉省は、2021年時点で約10万7,000人が全米の移植待機リストに載っているとしています。臓器移植と臓器登録の増加率が、世界の移植市場の市場規模を引き上げています。慢性疾患の罹患率の上昇も、世界の移植市場の成長を促進する主要要因の1つです。ALA(米国肺協会)のデータによると、2018年には約900万人の成人が慢性気管支炎を患い、肺移植や手術に至っています。ALAはまた、米国では毎年約20万人の肺がんが新たに報告されているとしています。一部の慢性疾患の効果的な治療法として臓器・組織移植の需要が高まっていることが、世界の移植市場の成長を促進しています。

- 政府の取り組みと支援

政府やその他の組織が提供する高レベルの支援は、世界の移植市場の成長を促進する主要要因の1つです。政府の取り組みや政策が世界の移植市場の成長を後押ししています。また、政府と非公開会社が協力して開発した臓器・組織バンクも世界の移植市場の成長を促進しています。臓器移植市場に対する企業の高額投資が、世界の移植セグメントの市場開拓とイノベーションを促進しています。また、大手企業が導入した新しい3D技術や先進機能の開発が、世界の移植市場の成長を促進しています。公共キャンペーン、教育プログラム、立法措置などの政府の取り組みは、臓器提供の意識を高め、ドナー臓器の利用可能性を高めることができます。また、臓器移植に関する規制の枠組みを確立・施行し、研究開発のための資金を割り当て、安全で効果的な移植処置を保証するために移植センターを含む医療インフラを強化します。

北米地域が市場を独占すると予想される

地域別では、北米地域が世界の移植市場で大幅な成長を示すと予想されています。整備されたインフラと大手企業の存在が北米地域の市場成長に寄与しています。慢性疾患の存在と増加率も世界の移植市場の成長を後押ししています。北米が世界の移植市場を独占すると予想されるのは、その先進的な医療インフラ、調査と技術革新、慢性疾患の高い発生率、確立された臓器調達と移植ネットワーク、規制環境、ドナー臓器の入手可能性、経済的要因、移植センター、医療機関、製薬企業間の協力関係によるものです。この地域の先進医療施設は、臓器移植手術の成功を支えています。末期腎不全、肝不全、心不全などの慢性疾患の罹患率の高さが、移植手術の需要を後押ししています。United Network for Organ Sharingのような組織による監督を含む規制環境は、移植市場に影響を与えています。この地域の臓器提供や移植に対する意識向上への取り組みは、ドナー臓器の入手可能性を高めることに貢献しています。

主要発展

- 2022年10月-ZEISS Medical Technologyは、新世代の電気手術用バイポーラ鉗子MTLawtonのFDA認可を取得しました。この鉗子は特殊な銅ベース合金製で、組織の癒着や凝固を抑え、効率的な準備を可能にします。また、延長されたシャフトは、術野の視覚的制限を軽減し、外科医が電気外科手術の際に、より効率的に手術を行えるようにします。

- 2022年3月-Biocompositesは、医療技術の世界的リーダーであるZimmer Biometと提携し、米国整形外科市場でGenex Bone Graft Substituteを販売します。この二相性複合材料は、骨伝導性足場の強度と体内での持続性のバランスをとるように設計されており、最適な骨アーキテクチャーの再構築を可能にします。この新しい契約には、米国市場向けの新しいクローズドミキシングシステムが含まれており、準備時間の短縮と作業時間の延長を実現しています。Genexはまた、より包括的な送達オプションを提供し、外科医が好みの手技に従ってビーズを注入、成形、調製できるようにします。

目次

第1章 イントロダクション

- 市場概要

- 市場の定義

- 調査範囲

- 市場セグメンテーション

- 通貨

- 前提条件

- 基準年と予測年のタイムライン

- 関係者にとっての主要メリット

第2章 調査手法

- 調査デザイン

- 調査プロセス

第3章 エグゼクティブサマリー

- 主要調査結果

- アナリストビュー

第4章 市場力学

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 業界バリューチェーン分析

- アナリストビュー

第5章 世界の移植市場:タイプ別

- イントロダクション

- 組織移植

- 臓器移植

第6章 世界の移植市場:最終用途別

- イントロダクション

- 病院

- 移植センター

- その他

第7章 世界の移植市場:地域別

- イントロダクション

- 北米

- 南米

- 欧州

- 中東・アフリカ

- アジア太平洋

第8章 競合環境と分析

- 主要企業と戦略分析

- 市場シェア分析

- 合併、買収、合意とコラボレーション

- 競合ダッシュボード

第9章 企業プロファイル

- Abbvie Inc.

- Arthrex Inc.

- Medtronic PLC

- Teva Pharmaceuticals

- Zimmer Biomet

- Strykers

- Novartis AG

- Veloxis Pharmaceuticals

- 21st Century Medicin

- BiolifeSolutions Inc

The transplant market is expected to grow at a CAGR of 9.35%, reaching a market size of US$31.238 billion in 2029 from US$16.709 billion in 2022.

Transplantation is the process of a tissue specimen or a complete organ being transplanted or transferred to another place from its original site. The transplanted organ or tissue will have nourishment and develop in the new, healthier environment compared to the original site. The transplant process is a process that is widely employed in the current medical and healthcare field. The transplantation process is widely used in the case of tissues and organs such as kidneys, hearts, livers, and so on. The transplantation techniques developed in the medical field have given way to new developments and innovations in the medical field. The increasing number of cases of chronic diseases and the rising number of surgeries are driving the market growth of the global transplant market. The rising health awareness and consciousness of people are also driving the market growth of the global transplant market. The support of the government in promoting organ banks and organ transplantation is also contributing to the market growth of the global transplant market. International healthcare organizations' awareness programs are also promoting and encouraging people to donate organs and tissues, which contributes to the global transplant market's growth. The rising rate of organ registration is also expected to increase the demand for organ transplants in the upcoming years. The research and development process taking place in the organ transplant field is resulting in advanced developments and innovations in the organ transplant market. The investment of major players like Abbvie Inc. and Arthrex Inc. in organ transplantation is fuelling the growth of the global transplant market.

MARKET DRIVERS:

- Rising Demand for Organ Transplants and Increasing Cases of Chronic Diseases

The increasing demand and popularity of organ transplantation are boosting the market growth of the global organ and tissue transplant market. The efficiency offered by transplantation methods or surgeries and the success rate of transplant methods are giving potential to the growth of the global transplant market. According to the reports of PAHO (Pan American Health Organisation), about 100+ lung transplantation surgeries take place in the United States every year. The United States Department of Health and Human Services states that about 107,000 people are on the national transplant waiting list as of 2021. The increased rate of organ transplantation and organ registration is raising the market size of the global transplant market. The rising incidence of chronic diseases is also one of the major factors driving the growth of the global transplant market. According to the data from the ALA (American Lung Association), about 9 million adults suffered from chronic bronchitis in 2018, which led to lung transplantation and surgery. ALA also states that around 200,000 new lung cancers are reported in the U.S. every year. The rising demand for organ and tissue transplantation as an effective treatment for some chronic diseases is driving the market growth of the global transplant market.

- Government Initiatives and Support

The high level of support offered by governments and other organizations is one of the major factors driving the market growth of the global transplant market. Government initiatives and policies are assisting in the growth of the global transplant market. The organ and tissue banks developed by the collaboration of governments and private companies are also fuelling the growth of the global transplant market. The high investment of companies in the organ transplant market is enhancing the development and innovations in the global transplant field. The development of new 3D technologies and advanced features in the field introduced by major companies is also fuelling the growth of the global transplant market. Government initiatives, including public campaigns, education programs, and legislative measures, can increase organ donation awareness and increase donor organ availability. They also establish and enforce regulatory frameworks for organ transplantation, allocate funding for research and development, and enhance healthcare infrastructure, including transplant centers, to ensure safe and effective transplant procedures.

The region of North America is anticipated to dominate the market

Geographically, the North American region is expected to showcase drastic growth in the global transplant market. The well-developed infrastructure and the presence of leading companies are contributing to the market growth in the North American region. The presence and increasing rate of chronic diseases are also propelling the growth of the global transplant market. North America is expected to dominate the global transplant market due to its advanced healthcare infrastructure, research and innovation, high incidence of chronic diseases, well-established organ procurement and transplantation networks, regulatory environment, availability of donor organs, economic factors, and collaborations between transplant centers, healthcare institutions, and pharmaceutical companies. The region's advanced medical facilities support successful implementation of organ transplantation procedures. The high incidence of chronic diseases, such as end-stage renal disease, liver failure, and heart failure, drives the demand for transplant procedures. The regulatory environment, including oversight by organizations like the United Network for Organ Sharing, influences the transplantation market. The region's efforts in promoting organ donation and transplantation awareness contribute to the higher availability of donor organs.

Key Developments:

- October 2022- ZEISS Medical Technology has received FDA clearance for its new MTLawton, a new generation of bipolar forceps for electrosurgery. These forceps, made from a special copper-base alloy, reduce tissue adhesion and coagulation for efficient preparation. The extended shaft also reduces visual restrictions in the surgical field, allowing surgeons to perform more efficiently during electrosurgical procedures. The forceps are expected to reduce tissue adhesion and charring during tissue dissection.

- March 2022- Biocomposites has partnered with global medical technology leader Zimmer Biomet to distribute Genex Bone Graft Substitute in the U.S. orthopedic market. The biphasic composite is designed to balance osteoconductive scaffold strength and persistence in the body, enabling optimal bone architecture remodeling. The new agreement includes a new closed-mixing system for the U.S. market, reducing preparation time and extending working time. Genex also offers a more comprehensive set of delivery options, allowing surgeons to inject, mold, or prepare beads according to their preferred technique.

Market Segmentation

By Type

- Tissue Transplant

- Organ Transplant

By End-Use

- Hospitals

- Transplant Centers

- Others

By Geography

- North America

- USA

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Others

- Europe

- Germany

- France

- UK

- Others

- Middle East and Africa

- Saudi Arabia

- UAE

- Others

- Asia Pacific

- China

- India

- Japan

- South Korea

- Taiwan

- Thailand

- Indonesia

- Others

TABLE OF CONTENTS

1. INTRODUCTION

- 1.1. Market Overview

- 1.2. Market Definition

- 1.3. Scope of the Study

- 1.4. Market Segmentation

- 1.5. Currency

- 1.6. Assumptions

- 1.7. Base, and Forecast Years Timeline

- 1.8. Key Benefits to the Stakeholder

2. RESEARCH METHODOLOGY

- 2.1. Research Design

- 2.2. Research Processes

3. EXECUTIVE SUMMARY

- 3.1. Key Findings

- 3.2. Analyst View

4. MARKET DYNAMICS

- 4.1. Market Drivers

- 4.2. Market Restraints

- 4.3. Porter's Five Forces Analysis

- 4.3.1. Bargaining Power of Suppliers

- 4.3.2. Bargaining Power of Buyers

- 4.3.3. Threat of New Entrants

- 4.3.4. Threat of Substitutes

- 4.3.5. Competitive Rivalry in the Industry

- 4.4. Industry Value Chain Analysis

- 4.5. Analyst View

5. GLOBAL TRANSPLANT MARKET, BY TYPE

- 5.1. Introduction

- 5.2. Tissue Transplant

- 5.2.1. Market Opportunities and Trends

- 5.2.2. Growth Prospects

- 5.2.3. Geographic Lucrativeness

- 5.3. Organ Transplant

- 5.3.1. Market Opportunities and Trends

- 5.3.2. Growth Prospects

- 5.3.3. Geographic Lucrativeness

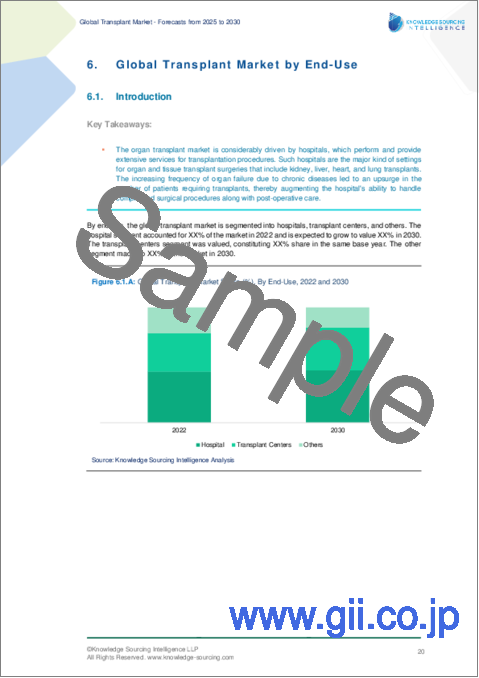

6. GLOBAL TRANSPLANT MARKET, BY END-USE

- 6.1. Introduction

- 6.2. Hospitals

- 6.2.1. Market Opportunities and Trends

- 6.2.2. Growth Prospects

- 6.2.3. Geographic Lucrativeness

- 6.3. Transplant Centers

- 6.3.1. Market Opportunities and Trends

- 6.3.2. Growth Prospects

- 6.3.3. Geographic Lucrativeness

- 6.4. Others

- 6.4.1. Market Opportunities and Trends

- 6.4.2. Growth Prospects

- 6.4.3. Geographic Lucrativeness

7. GLOBAL TRANSPLANT MARKET, BY GEOGRAPHY

- 7.1. Introduction

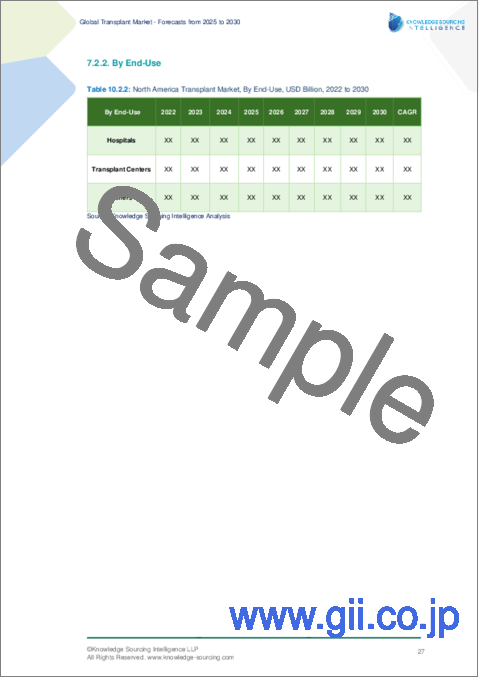

- 7.2. North America

- 7.2.1. By Type

- 7.2.2. By End-Use

- 7.2.3. By Country

- 7.2.3.1. USA

- 7.2.3.1.1. Market Opportunities and Trends

- 7.2.3.1.2. Growth Prospects

- 7.2.3.2. Canada

- 7.2.3.2.1. Market Opportunities and Trends

- 7.2.3.2.2. Growth Prospects

- 7.2.3.3. Mexico

- 7.2.3.3.1. Market Opportunities and Trends

- 7.2.3.3.2. Growth Prospects

- 7.2.3.1. USA

- 7.3. South America

- 7.3.1. By Type

- 7.3.2. By End-Use

- 7.3.3. By Country

- 7.3.3.1. Brazil

- 7.3.3.1.1. Market Opportunities and Trends

- 7.3.3.1.2. Growth Prospects

- 7.3.3.2. Argentina

- 7.3.3.2.1. Market Opportunities and Trends

- 7.3.3.2.2. Growth Prospects

- 7.3.3.3. Others

- 7.3.3.3.1. Market Opportunities and Trends

- 7.3.3.3.2. Growth Prospects

- 7.3.3.1. Brazil

- 7.4. Europe

- 7.4.1. By Type

- 7.4.2. By End-Use

- 7.4.3. By Country

- 7.4.3.1. Germany

- 7.4.3.1.1. Market Opportunities and Trends

- 7.4.3.1.2. Growth Prospects

- 7.4.3.2. France

- 7.4.3.2.1. Market Opportunities and Trends

- 7.4.3.2.2. Growth Prospects

- 7.4.3.3. UK

- 7.4.3.3.1. Market Opportunities and Trends

- 7.4.3.3.2. Growth Prospects

- 7.4.3.4. Others

- 7.4.3.4.1. Market Opportunities and Trends

- 7.4.3.4.2. Growth Prospects

- 7.4.3.1. Germany

- 7.5. Middle East and Africa

- 7.5.1. By Type

- 7.5.2. By End-Use

- 7.5.3. By Country

- 7.5.3.1. Saudi Arabia

- 7.5.3.1.1. Market Opportunities and Trends

- 7.5.3.1.2. Growth Prospects

- 7.5.3.2. UAE

- 7.5.3.2.1. Market Opportunities and Trends

- 7.5.3.2.2. Growth Prospects

- 7.5.3.3. Others

- 7.5.3.3.1. Market Opportunities and Trends

- 7.5.3.3.2. Growth Prospects

- 7.5.3.1. Saudi Arabia

- 7.6. Asia Pacific

- 7.6.1. By Type

- 7.6.2. By End-Use

- 7.6.3. By Country

- 7.6.3.1. China

- 7.6.3.1.1. Market Opportunities and Trends

- 7.6.3.1.2. Growth Prospects

- 7.6.3.2. India

- 7.6.3.2.1. Market Opportunities and Trends

- 7.6.3.2.2. Growth Prospects

- 7.6.3.3. Japan

- 7.6.3.3.1. Market Opportunities and Trends

- 7.6.3.3.2. Growth Prospects

- 7.6.3.4. South Korea

- 7.6.3.4.1. Market Opportunities and Trends

- 7.6.3.4.2. Growth Prospects

- 7.6.3.5. Taiwan

- 7.6.3.5.1. Market Opportunities and Trends

- 7.6.3.5.2. Growth Prospects

- 7.6.3.6. Thailand

- 7.6.3.6.1. Market Opportunities and Trends

- 7.6.3.6.2. Growth Prospects

- 7.6.3.7. Indonesia

- 7.6.3.7.1. Market Opportunities and Trends

- 7.6.3.7.2. Growth Prospects

- 7.6.3.8. Others

- 7.6.3.8.1. Market Opportunities and Trends

- 7.6.3.8.2. Growth Prospects

- 7.6.3.1. China

8. COMPETITIVE ENVIRONMENT AND ANALYSIS

- 8.1. Major Players and Strategy Analysis

- 8.2. Market Share Analysis

- 8.3. Mergers, Acquisitions, Agreements, and Collaborations

- 8.4. Competitive Dashboard

9. COMPANY PROFILES

- 9.1. Abbvie Inc.

- 9.2. Arthrex Inc.

- 9.3. Medtronic PLC

- 9.4. Teva Pharmaceuticals

- 9.5. Zimmer Biomet

- 9.6. Strykers

- 9.7. Novartis AG

- 9.8. Veloxis Pharmaceuticals

- 9.9. 21st Century Medicin

- 9.10. BiolifeSolutions Inc