|

|

市場調査レポート

商品コード

1627803

世界の種子市場:予測(2025年~2030年)Global Seed Market - Forecasts from 2025 to 2030 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 世界の種子市場:予測(2025年~2030年) |

|

出版日: 2024年12月16日

発行: Knowledge Sourcing Intelligence

ページ情報: 英文 142 Pages

納期: 即日から翌営業日

|

全表示

- 概要

- 目次

世界の種子市場はCAGR6.20%で成長し、市場規模は2025年の815億5,700万米ドルから2030年には1,101億9,300万米ドルに達すると予想されています。

種子は胚の段階で植物の栄養素を蓄え、世界人口の増加に伴い、食糧需要は増加の一途をたどっています。遺伝子組み換え種子と従来の種子では、植物になるために必要な水分摂取量やその他の要素が異なりますが、環境への関心の高まりとともに、その需要はプラス成長を遂げると予想されます。

例えば、BASFは2023年2月、ToBRFVに耐性を持つトマトの新品種を発表しました。同社のNunhems(R)ポートフォリオには現在、ToBRFVに耐性を示すトマト種子品種のセレクションが含まれています。同様に2024年3月、Syngenta Vegetable Seedsはインドのハイデラバードに新しいシード・ヘルス・ラボを開設しました。このラボはインド初の種子衛生専門ラボです。このラボは、インドのみならずアジア太平洋地域、さらにはそれ以外の地域の生産者にもサービスを提供します。

世界の種子市場の促進要因

- 園芸栽培の拡大が市場成長を促進する見込み

園芸は、果物、野菜、観賞用植物を含む遺伝子操作作物の栽培を定義しており、ハイブリッド作物品種を開発するための新しい技術オプションを採用する枠組みを提供しています。そのため、主要国はハイブリッド作物生産の成長可能性を最適化することを目指しており、園芸生産を強化するために垂直農業や屋内農業プログラムへの投資が実施されています。

例えば、農業・農民福祉省の2023年から2024年第2次事前予測によると、インドの園芸生産量は3億5,223万トンに達し、果物、芳香・薬用植物、ハニーフラワー、スパイス、プランテーション作物が積極的な拡大を見せています。同様に、欧州地域では、ジャガイモなどの主要な園芸作物の生産を強化するために様々な計画が実施されており、これもまた市場拡大に弾みをつけています。

世界の種子市場の地理的展望

- 予測期間中、北米が市場で大きなシェアを占めると予想されます。

地域的には、世界の種子市場は北米、南米、欧州、中東・アフリカ、アジア太平洋に区分されます。

予測期間中、北米が市場で大きなシェアを占めていますが、これは米国とカナダという主要地域経済における作物生産の強化に起因しています。例えば、米国農務省(USDA)によると、2021年から2022年の小麦生産量は4,480万トンで、2022年から2023年には4,490万トンに増加しました。同様に、2021年の米国のトウモロコシ生産量は150億ブッシェルで、2023年には153億ブッシェルに増加します。

さらに、米国では種子生産が重視されるようになり、様々な研究協力が行われるようになったことも、この地域市場を形成しています。例えば、Syngentaは2023年8月、米国イリノイ州にSyngenta Seeds R&D Innovation Centerとして知られる研究開発用の最新鋭の32,000平方フィートの研究所を開設しました。

本レポートを購入する理由

- 洞察に満ちた分析:主要地域だけでなく新興地域もカバーし、顧客セグメント、政府政策と社会経済要因、消費者選好、産業別、その他のサブセグメントに焦点を当てた詳細な市場考察を得ることができます。

- 競合情勢:世界の主要企業が採用している戦略的作戦を理解し、適切な戦略による市場浸透の可能性を理解することができます。

- 市場動向と促進要因:ダイナミックな要因と極めて重要な市場動向、そしてそれらが今後の市場展開をどのように形成していくかを探ります。

- 実行可能な提言:ダイナミックな環境の中で新たなビジネスストリームと収益を発掘するための戦略的決断を下すために、洞察を活用します。

- 幅広い利用者に対応:新興企業、研究機関、コンサルタント、中小企業、大企業にとって有益で費用対効果に優れています。

どのような用途で利用されていますか?

業界と市場考察、事業機会評価、製品需要予測、市場参入戦略、地理的拡大、設備投資の決定、規制の枠組みと影響、新製品開拓、競合の影響

調査範囲

- 2022年から2030年までの実績データと予測

- 成長機会、課題、サプライチェーンの展望、規制枠組み、顧客行動、動向分析

- 競合のポジショニング、戦略、市場シェア分析

- 収益の成長と予測各国を含むセグメントおよび地域の分析

- 企業プロファイリング(戦略、製品、財務状況、主な発展など)

世界の種子市場は以下のセグメントに分析されます:

由来別

- 遺伝子組み換え

- 従来型

特性別

- 除草剤耐性

- 殺虫剤耐性

- スタック形質

作物タイプ別

- 果物・野菜

- 油糧種子・豆類

- 穀物・穀類

地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他

- 欧州

- 英国

- ドイツ

- フランス

- その他

- 中東・アフリカ

- サウジアラビア

- UAE

- イスラエル

- その他

- アジア太平洋

- 日本

- 中国

- インド

- オーストラリア

- その他

目次

第1章 イントロダクション

- 市場概要

- 市場の定義

- 調査範囲

- 市場セグメンテーション

- 通貨

- 前提条件

- 基準年と予測年のタイムライン

- ステークホルダーにとっての主なメリット

第2章 調査手法

- 調査デザイン

- 調査プロセス

第3章 エグゼクティブサマリー

- 主な調査結果

- CXOの視点

第4章 市場力学

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 業界バリューチェーン分析

- アナリストビュー

第5章 世界の種子市場:由来別

- イントロダクション

- 遺伝子組み換え

- 従来型

第6章 世界の種子市場:特性別

- イントロダクション

- 除草剤耐性

- 殺虫剤耐性

- スタック特性

第7章 世界の種子市場:作物別

- イントロダクション

- 果物・野菜

- 油糧種子・豆類

- 穀物・穀類

第8章 世界の種子市場:地域別

- イントロダクション

- 北米

- 由来別

- 特性別

- 作物別

- 国別

- 南米

- 由来別

- 特性別

- 作物別

- 国別

- 欧州

- 由来別

- 特性別

- 作物別

- 国別

- 中東・アフリカ

- 由来別

- 特性別

- 作物別

- 国別

- アジア太平洋

- 由来別

- 特性別

- 作物別

- 国別

第9章 競合環境と分析

- 主要企業と戦略分析

- 市場シェア分析

- 合併、買収、合意、コラボレーション

- 競合ダッシュボード

第10章 企業プロファイル

- ADM Monsanto Company

- Dowdupont Inc.

- Groupe Limagrain

- Bayer Ag

- Kws Saat Se

- Chemchina(Sinochem Holdings Corporation Ltd.)

- Land O'lakes, Inc.

- Sakata Seed Corporation(Sakata Group)

- Takii & Co., Ltd.

- Dlf

- Basf Corporation

- Cargill Corporation

- Ball Horticultural Company

- Syngenta

- Limagrain(the Limagrain Cooperative)

- Growmark, Inc.

- CHS Inc.

- United Cooperative

- Beck's Hybrids

- Heartland Co-op

- Hazera Seeds(the Limagrain Group)

- Rijk Zwaan

The global seed market is expected to grow at a CAGR of 6.20%, reaching a market size of US$110.193 billion in 2030 from US$81.557 billion in 2025.

Seeds store the nutrients of a plant during the embryonic stage and with the growing global population, the food demand is on the constant rise thereby bolstering the need for more food production. Genetically engineered or conventional seeds differ on the basis of water intake and other ex-factors required for them to turn into plants, but with the growing environmental concern, their demand is anticipated to positive growth.

Several companies have launched disease-resistant seeds, for example, on February 2023, BASF introduced new tomato seed varieties that are resistant to ToBRFV. Their Nunhems(R) portfolio currently includes a selection of tomato seed varieties that exhibit resistance to ToBRFV. Likewise, In March 2024, Syngenta Vegetable Seeds opened a new Seed Health Lab in Hyderabad, India, showcasing the company's ongoing commitment to enhancing quality control capabilities. This lab is India's first specialized seed health lab. It will cater to growers not only in India but also across the Asia Pacific region and beyond.

Global Seed Market Drivers

- Growing horticulture practices is expected to improve the market growth

Horticulture defines the growing of genetically engineered crops inclusive of fruits, vegetables, and ornamental plants which has provided a framework for the adoption of new technological options for developing hybrid crop varieties. Hence major economies are aiming to optimize the growing potential of hybrid crop production, therefore investments in vertical farming and indoor farming programs are being implemented to bolster horticulture production.

For instance, according to the Department of Agriculture and Farmers Welfare's second advanced estimate for 2023-2024, India's horticulture production reached 352.23 million tons with fruits, aromatic & medicinal plants, honey flowers, spices and plantation crops showing positive expansion. Likewise, the European region undertaking various schemes to bolster the production of major horticulture crops such as potatoes which is also creating a surge in the market expansion.

Global Seed Market Geographical Outlook

- North America is expected to account for a significant share of the market during the forecast period.

Geographically, the global seed market has been segmented into North America, South America, Europe, the Middle East, Africa, and the Asia Pacific.

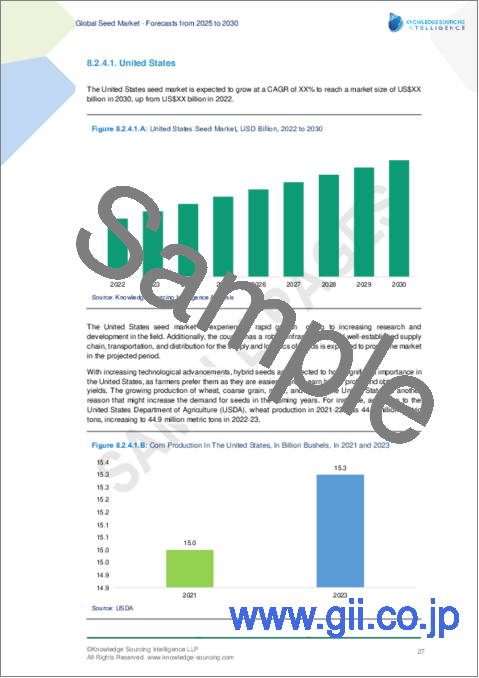

During the forecast period, North America will be holding a considerable share of the market which is attributable to the bolstering of crop production in major regional economies namely the United States and Canada. For instance, according to the United States Department of Agriculture (USDA), wheat production in 2021-22 was 44.8 million metric tons, which increased to 44.9 million metric tons in 2022-23. Likewise, in 2021, corn production in the United States was 15.0 billion bushels, which increased to 15.3 billion bushels in 2023.

Moreover, the growing emphasis on seed production in the United States has led to various research collaborations which are also shaping the regional market. Major companies are extending their product to improve their market presence in North America, for instance, in August 2023, Syngenta launched a new state-of-the-art 32,000 square feet laboratory space for research and development known as Syngenta Seeds R&D Innovation Center, in Illinois, United States

Reasons for buying this report:-

- Insightful Analysis: Gain detailed market insights covering major as well as emerging geographical regions, focusing on customer segments, government policies and socio-economic factors, consumer preferences, industry verticals, other sub- segments.

- Competitive Landscape: Understand the strategic maneuvers employed by key players globally to understand possible market penetration with the correct strategy.

- Market Drivers & Future Trends: Explore the dynamic factors and pivotal market trends and how they will shape up future market developments.

- Actionable Recommendations: Utilize the insights to exercise strategic decision to uncover new business streams and revenues in a dynamic environment.

- Caters to a Wide Audience: Beneficial and cost-effective for startups, research institutions, consultants, SMEs, and large enterprises.

What do businesses use our reports for?

Industry and Market Insights, Opportunity Assessment, Product Demand Forecasting, Market Entry Strategy, Geographical Expansion, Capital Investment Decisions, Regulatory Framework & Implications, New Product Development, Competitive Intelligence

Report Coverage:

- Historical data & forecasts from 2022 to 2030

- Growth Opportunities, Challenges, Supply Chain Outlook, Regulatory Framework, Customer Behaviour, and Trend Analysis

- Competitive Positioning, Strategies, and Market Share Analysis

- Revenue Growth and Forecast Assessment of segments and regions including countries

- Company Profiling (Strategies, Products, Financial Information, and Key Developments among others)

Global Seed Market is analyzed into the following segments:

By Origin

- Genetically Modified

- Conventional

By Trait

- Herbicide-Tolerant

- Insecticide-Resistance

- Stacked Trait

By Crop Type

- Fruits and Vegetables

- Oilseed and Pulses

- Cereals and Grains

By Geography

- North America

- USA

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Others

- Europe

- United Kingdom

- Germany

- France

- Others

- Middle East and Africa

- Saudi Arabia

- UAE

- Israel

- Others

- Asia Pacific

- Japan

- China

- India

- Australia

- Others

TABLE OF CONTENTS

1. INTRODUCTION

- 1.1. Market Overview

- 1.2. Market Definition

- 1.3. Scope of the Study

- 1.4. Market Segmentation

- 1.5. Currency

- 1.6. Assumptions

- 1.7. Base and Forecast Years Timeline

- 1.8. Key Benefits to the Stakeholder

2. RESEARCH METHODOLOGY

- 2.1. Research Design

- 2.2. Research Processes

3. EXECUTIVE SUMMARY

- 3.1. Key Findings

- 3.2. CXO Perspective

4. MARKET DYNAMICS

- 4.1. Market Drivers

- 4.2. Market Restraints

- 4.3. Porter's Five Forces Analysis

- 4.3.1. Bargaining Power of Suppliers

- 4.3.2. Bargaining Power of Buyers

- 4.3.3. Threat of New Entrants

- 4.3.4. Threat of Substitutes

- 4.3.5. Competitive Rivalry in the Industry

- 4.4. Industry Value Chain Analysis

- 4.5. Analyst View

5. GLOBAL SEED MARKET BY ORIGIN

- 5.1. Introduction

- 5.2. Genetically Modified

- 5.3. Conventional

6. GLOBAL SEED MARKET BY TRAIT

- 6.1. Introduction

- 6.2. Herbicide-Tolerant

- 6.3. Insecticide-Resistance

- 6.4. Stacked-Trait

7. GLOBAL SEED MARKET BY CROPS

- 7.1. Introduction

- 7.2. Fruits and Vegetables

- 7.3. Oilseed and Pulses

- 7.4. Cereals and Grains

8. GLOBAL SEED MARKET BY GEOGRAPHY

- 8.1. Introduction

- 8.2. North America

- 8.2.1. By Origin

- 8.2.2. By Trait

- 8.2.3. By Crops

- 8.2.4. By Country

- 8.2.4.1. USA

- 8.2.4.2. Canada

- 8.2.4.3. Mexico

- 8.3. South America

- 8.3.1. By Origin

- 8.3.2. By Trait

- 8.3.3. By Crops

- 8.3.4. By Country

- 8.3.4.1. Brazil

- 8.3.4.2. Argentina

- 8.3.4.3. Others

- 8.4. Europe

- 8.4.1. By Origin

- 8.4.2. By Trait

- 8.4.3. By Crops

- 8.4.4. By Country

- 8.4.4.1. United Kingdom

- 8.4.4.2. Germany

- 8.4.4.3. France

- 8.4.4.4. Others

- 8.5. Middle East and Africa

- 8.5.1. By Origin

- 8.5.2. By Trait

- 8.5.3. By Crops

- 8.5.4. By Country

- 8.5.4.1. Saudi Arabia

- 8.5.4.2. UAE

- 8.5.4.3. Israel

- 8.5.4.4. Others

- 8.6. Asia Pacific

- 8.6.1. By Origin

- 8.6.2. By Trait

- 8.6.3. By Crops

- 8.6.4. By Country

- 8.6.4.1. Japan

- 8.6.4.2. China

- 8.6.4.3. India

- 8.6.4.4. Australia

- 8.6.4.5. Others

9. COMPETITIVE ENVIRONMENT AND ANALYSIS

- 9.1. Major Players and Strategy Analysis

- 9.2. Market Share Analysis

- 9.3. Mergers, Acquisitions, Agreements, and Collaborations

- 9.4. Competitive Dashboard

10. COMPANY PROFILES

- 10.1. ADM Monsanto Company

- 10.2. Dowdupont Inc.

- 10.3. Groupe Limagrain

- 10.4. Bayer Ag

- 10.5. Kws Saat Se

- 10.6. Chemchina( (Sinochem Holdings Corporation Ltd.)

- 10.7. Land O'lakes, Inc.

- 10.8. Sakata Seed Corporation (Sakata Group)

- 10.9. Takii & Co., Ltd.

- 10.10. Dlf

- 10.11. Basf Corporation

- 10.12. Cargill Corporation

- 10.13. Ball Horticultural Company

- 10.14. Syngenta

- 10.15. Limagrain (the Limagrain Cooperative)

- 10.16. Growmark, Inc.

- 10.17. CHS Inc.

- 10.18. United Cooperative

- 10.19. Beck's Hybrids

- 10.20. Heartland Co-op

- 10.21. Hazera Seeds (the Limagrain Group)

- 10.22. Rijk Zwaan