|

|

市場調査レポート

商品コード

1800288

ネオジム磁石市場-2025年から2030年までの予測Neodymium Magnet Market - Forecasts fom 2025 to 2030 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| ネオジム磁石市場-2025年から2030年までの予測 |

|

出版日: 2025年08月18日

発行: Knowledge Sourcing Intelligence

ページ情報: 英文 148 Pages

納期: 即日から翌営業日

|

全表示

- 概要

- 目次

ネオジム磁石市場は、2025年の30億2,000万米ドルから2030年には37億6,700万米ドルへ、CAGR 4.52%で成長すると予測されます。

ネオジム磁石市場は、コンシューマーエレクトロニクス、自動車、再生可能エネルギーセグメントでの需要増加に牽引され、力強い成長を遂げています。ネオジム-鉄-ボロン(NdFeB)磁石は、その卓越した強度とコンパクトなサイズで知られ、高性能アプリケーションに不可欠です。同市場は、技術の進歩、電気自動車(EV)の普及拡大、再生可能エネルギーの世界の推進によって後押しされており、特に中国を中心とするアジア太平洋がレアアース生産で優位を占めています。

市場促進要因

再生可能エネルギーの拡大

再生可能エネルギーの導入、特に風力発電の急増は、ネオジム磁石の需要を大きく牽引しています。風力タービンはネオジム磁石の効率的な発電機に依存しており、世界の持続可能性の目標を支えています。国際エネルギー機関(IEA)は、風力発電が2030年までに7,900TWhに達し、2050年までのネットゼロエミッション(Net Zero Emission)目標に整合すると予測しており、タービン組立品におけるネオジム磁石の必要性をさらに高めています。

自動車産業の需要

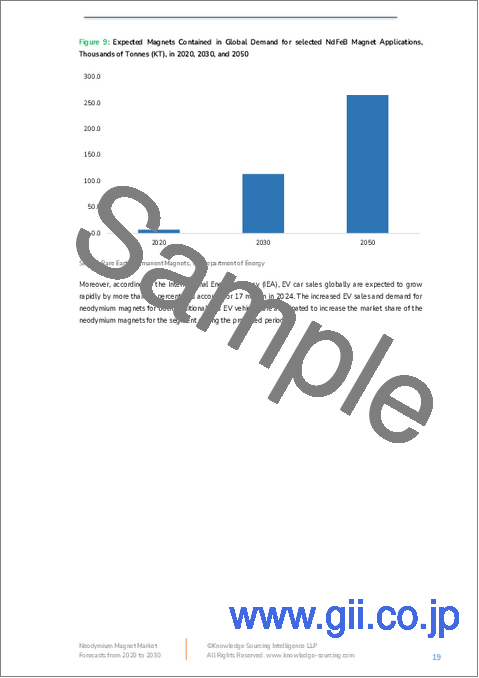

自動車産業、特にEVセグメントは主要な促進要因です。ネオジム磁石は、電気モーター、センサ、衝突予知や自律走行技術などの安全システムに不可欠です。IEAは、バッテリー電気自動車(BEV)やプラグインハイブリッド電気自動車(PHEV)を含む電気自動車の販売台数が2022年に1,000万台を超えると報告しており、市場の力強い成長を反映しています。米国エネルギー省は、2025年までにバッテリーとハイブリッドEVの90~100%にネオジム磁石を使用した同期トラクションモーターが採用され、EV用途のネオジム磁石の世界需要は2030年までに11万4,100トン、2050年までに26万6,000トンに達すると予測しています。

技術の進歩

磁石技術の革新は性能と効率を高め、長期的な市場成長を支えます。ネオジム磁石製造の進歩はエネルギー密度を向上させ、サイズを小型化するため、EVや民生用電子機器製品に最適です。しかし、特にフッ化物ベース溶融塩電解では、ネオジムの熱力学的安定性のために生産にかかるエネルギーコストが高く、エネルギー価格の上昇が市場拡大に影響を与える可能性があるという課題があります。

リサイクルの可能性

ネオジムのリサイクルは、セクタを再構築し、サプライチェーンの脆弱性に対処する戦略として注目を集めています。企業は、最終製品からネオジムを回収するリサイクルプロセスを導入し、一次採掘への依存を減らし、環境懸念を緩和しています。この動向は、特に風力発電センターのような再生可能エネルギープロジェクトからの需要が高まる中、サステイナブル成長を支えています。

地理的展望

中国を中心とするアジア太平洋は、その膨大なレアアース埋蔵量、低い生産コスト、有利な政府施策により、ネオジム磁石市場を独占しています。中国の生産能力は大きく、国内と世界の供給を牽引し、市場の主導権を強めています。北米のと欧州のも、EVの普及と再生可能エネルギーへの取り組みに後押しされて成長しているが、中国の供給優位性という課題に直面しています。

課題

市場は、高い生産エネルギーコストや、中国がレアアースの供給を支配していることによる地政学的リスクなどのハードルに直面しています。採掘と加工に関連する環境への懸念も、サステイナブルプラクティスと規制遵守を必要とします。

結論

ネオジム磁石市場は、EVの普及、再生可能エネルギーの拡大、技術の進歩に牽引され、大きな成長が見込まれています。アジア太平洋、特に中国の優位性は、世界のサプライチェーンにおける重要な役割を強調しています。リサイクルと技術革新が持続可能性の機会を提供する一方で、エネルギーコストとサプライチェーンのリスクに対処することは、2030年以降も持続的に市場を拡大する上で極めて重要です。

本レポートの主要利点

- 洞察分析:顧客セグメント、政府施策と社会経済要因、消費者嗜好、産業別、その他のサブセグメントに焦点を当て、主要地域だけでなく新興地域も網羅した詳細な市場考察を得ることができます。

- 競合情勢:世界の主要企業が採用している戦略的策略を理解し、適切な戦略による市場浸透の可能性を理解することができます。

- 市場動向と促進要因:ダイナミック要因と極めて重要な市場動向、それらが今後の開発をどのように形成していくかを探る。

- 行動可能な提言:洞察力を戦略的意思決定に活用し、ダイナミック環境の中で新たなビジネスストリームと収益を発掘します。

- 幅広い利用者に対応:新興企業、研究機関、コンサルタント、中小企業、大企業にとって有益で費用対効果の高いです。

どのような用途で利用されていますか?

産業と市場考察、事業機会評価、製品需要予測、市場参入戦略、地理的拡大、設備投資の決定、規制の枠組みと影響、新製品開拓、競合の影響

調査範囲

- 2020~2024年までの過去データ&2025~2030年までの予測データ

- 成長機会、課題、サプライチェーンの展望、規制の枠組み、動向分析

- 競合のポジショニング、戦略、市場シェア分析

- 収益の成長と予測各国を含むセグメントと地域の分析

- 企業プロファイリング(特に動向)、財務情報、主要開発

目次

第1章 エグゼクティブサマリー

第2章 市場スナップショット

- 市場概要

- 市場の定義

- 調査範囲

- 市場セグメンテーション

第3章 ビジネス情勢

- 市場促進要因

- 市場抑制要因

- 市場機会

- ポーターのファイブフォース分析

- 産業バリューチェーン分析

- 施策と規制

- 戦略的提言

第4章 技術展望

第5章 ネオジム磁石市場:タイプ別

- イントロダクション

- 結合

- 焼結

第6章 ネオジム磁石市場:エンドユーザー別

- イントロダクション

- 自動車

- 民生用電子機器

- ヘルスケア

- エネルギー

- 産業機械

- 航空宇宙と防衛

- 民生用電子機器製品

- その他

第7章 ネオジム磁石市場:地域別

- イントロダクション

- 北米

- タイプ別

- エンドユーザー別

- 国別

- 米国

- カナダ

- メキシコ

- 南米

- タイプ別

- エンドユーザー別

- 国別

- ブラジル

- アルゼンチン

- その他

- 欧州

- タイプ別

- エンドユーザー別

- 国別

- 英国

- ドイツ

- フランス

- スペイン

- その他

- 中東・アフリカ

- タイプ別

- エンドユーザー別

- 国別

- サウジアラビア

- アラブ首長国連邦

- その他

- アジア太平洋

- タイプ別

- エンドユーザー別

- 国別

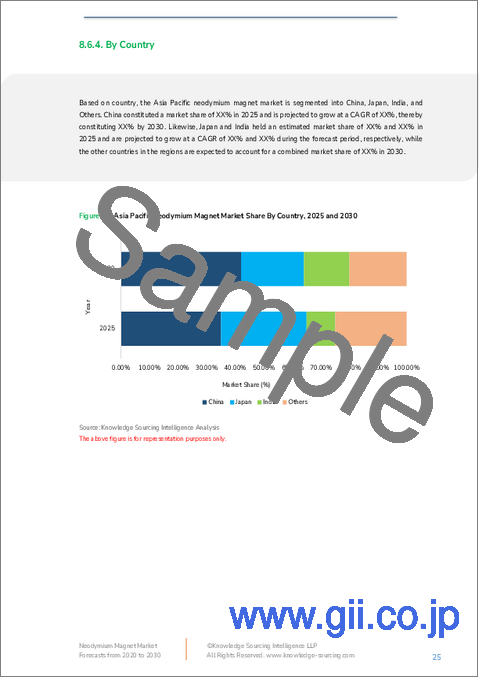

- 中国

- 日本

- インド

- 韓国

- 台湾

- その他

第8章 競合環境と分析

- 主要企業と戦略分析

- 市場シェア分析

- 合併、買収、合意とコラボレーション

- 競合ダッシュボード

第9章 企業プロファイル

- Introduction

- Neodymium

- Cerium

- Lanthanum

- Neodymium Magnet

第10章 付録

- 通貨

- 前提条件

- 基準年と予測年のタイムライン

- 利害関係者にとっての主要メリット

- 調査手法

- 略語

The Neodymium Magnet Market is expected to grow from USD 3.020 billion in 2025 to USD 3.767 billion in 2030, at a CAGR of 4.52%.

The neodymium magnet market is experiencing robust growth, driven by increasing demand across consumer electronics, automotive, and renewable energy sectors. Neodymium-iron-boron (NdFeB) magnets, known for their exceptional strength and compact size, are critical in high-performance applications. The market is propelled by technological advancements, rising adoption of electric vehicles (EVs), and the global push for renewable energy, with Asia-Pacific, particularly China, leading due to its dominance in rare earth production.

Market Drivers

Renewable Energy Expansion

The surge in renewable energy adoption, particularly wind power, significantly drives demand for neodymium magnets. Wind turbines rely on NdFeB magnets for efficient generators, supporting global sustainability goals. The International Energy Agency (IEA) projects wind electricity generation to reach 7,900 TWh by 2030, aligning with Net Zero Emission targets by 2050, further boosting the need for neodymium magnets in turbine assemblies.

Automotive Sector Demand

The automotive industry, especially the EV segment, is a major growth driver. Neodymium magnets are essential in electric motors, sensors, and safety systems like collision prediction and autonomous driving technologies. The IEA reported that electric car sales, including battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs), exceeded 10 million in 2022, reflecting strong market growth. The U.S. Department of Energy estimates that 90-100% of battery and hybrid EVs will use synchronous traction motors with NdFeB magnets by 2025, with global demand for neodymium magnets in EV applications projected to reach 114.1 thousand tons by 2030 and 266 thousand tons by 2050.

Technological Advancements

Innovations in magnet technology enhance performance and efficiency, supporting long-term market growth. Advances in NdFeB magnet production improve energy density and reduce size, making them ideal for EVs and consumer electronics. However, high energy costs for production, particularly in fluoride-based fused salt electrolysis, pose challenges due to the thermodynamic stability of neodymium, with rising energy prices potentially impacting market expansion.

Recycling Potential

Neodymium recycling is gaining traction as a strategy to restructure the sector and address supply chain vulnerabilities. Businesses are implementing recycling processes to recover neodymium from end-use products, reducing reliance on primary mining and mitigating environmental concerns. This trend supports sustainable growth, particularly as demand rises from renewable energy projects like wind energy centers.

Geographical Outlook

The Asia-Pacific region, led by China, dominates the neodymium magnet market due to its vast rare earth reserves, low production costs, and favorable government policies. China's significant production capacity drives both domestic and global supply, reinforcing its market leadership. North America and Europe are also growing, fueled by EV adoption and renewable energy initiatives, though they face challenges from China's supply dominance.

Challenges

The market faces hurdles such as high production energy costs and geopolitical risks due to China's control over rare earth supplies. Environmental concerns related to mining and processing also necessitate sustainable practices and regulatory compliance.

Conclusion

The neodymium magnet market is poised for significant growth, driven by EV adoption, renewable energy expansion, and technological advancements. Asia-Pacific's dominance, particularly China's, underscores its critical role in the global supply chain. While recycling and innovation offer opportunities for sustainability, addressing energy costs and supply chain risks will be crucial for sustained market expansion through 2030 and beyond.

Key Benefits of this Report:

- Insightful Analysis: Gain detailed market insights covering major as well as emerging geographical regions, focusing on customer segments, government policies and socio-economic factors, consumer preferences, industry verticals, and other sub-segments.

- Competitive Landscape: Understand the strategic maneuvers employed by key players globally to understand possible market penetration with the correct strategy.

- Market Drivers & Future Trends: Explore the dynamic factors and pivotal market trends and how they will shape future market developments.

- Actionable Recommendations: Utilize the insights to exercise strategic decisions to uncover new business streams and revenues in a dynamic environment.

- Caters to a Wide Audience: Beneficial and cost-effective for startups, research institutions, consultants, SMEs, and large enterprises.

What do businesses use our reports for?

Industry and Market Insights, Opportunity Assessment, Product Demand Forecasting, Market Entry Strategy, Geographical Expansion, Capital Investment Decisions, Regulatory Framework & Implications, New Product Development, Competitive Intelligence

Report Coverage:

- Historical data from 2020 to 2024 & forecast data from 2025 to 2030

- Growth Opportunities, Challenges, Supply Chain Outlook, Regulatory Framework, and Trend Analysis

- Competitive Positioning, Strategies, and Market Share Analysis

- Revenue Growth and Forecast Assessment of segments and regions including countries

- Company Profiling (Strategies, Products, Financial Information, and Key Developments among others.

Segmentation:

By Type

- Bonded

- Sintered

By End-User

- Automotive

- Consumer Electronics

- Healthcare

- Energy

- Industrial Machinery

- Aerospace & Defense

- Home Appliances

- Others

By Geography

- North America

- South America

- Europe

- Middle East and Africa

- Asia Pacific

TABLE OF CONTENTS

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

- 2.1. Market Overview

- 2.2. Market Definition

- 2.3. Scope of the Study

- 2.4. Market Segmentation

3. BUSINESS LANDSCAPE

- 3.1. Market Drivers

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.4. Porter's Five Forces Analysis

- 3.5. Industry Value Chain Analysis

- 3.6. Policies and Regulations

- 3.7. Strategic Recommendations

4. TECHNOLOGICAL OUTLOOK

5. NEODYMIUM MAGNET MARKET BY TYPE

- 5.1. Introduction

- 5.2. Bonded

- 5.3. Sintered

6. NEODYMIUM MAGNET MARKET BY END-USER

- 6.1. Introduction

- 6.2. Automotive

- 6.3. Consumer Electronics

- 6.4. Healthcare

- 6.5. Energy

- 6.6. Industrial Machinery

- 6.7. Aerospace & Defense

- 6.8. Home Appliances

- 6.9. Others

7. NEODYMIUM MAGNET MARKET BY GEOGRAPHY

- 7.1. Introduction

- 7.2. North America

- 7.2.1. By Type

- 7.2.2. By End-User

- 7.2.3. By Country

- 7.2.3.1. USA

- 7.2.3.2. Canada

- 7.2.3.3. Mexico

- 7.3. South America

- 7.3.1. By Type

- 7.3.2. By End-User

- 7.3.3. By Country

- 7.3.3.1. Brazil

- 7.3.3.2. Argentina

- 7.3.3.3. Others

- 7.4. Europe

- 7.4.1. By Type

- 7.4.2. By End-User

- 7.4.3. By Country

- 7.4.3.1. United Kingdom

- 7.4.3.2. Germany

- 7.4.3.3. France

- 7.4.3.4. Spain

- 7.4.3.5. Others

- 7.5. Middle East and Africa

- 7.5.1. By Type

- 7.5.2. By End-User

- 7.5.3. By Country

- 7.5.3.1. Saudi Arabia

- 7.5.3.2. UAE

- 7.5.3.3. Others

- 7.6. Asia Pacific

- 7.6.1. By Type

- 7.6.2. By End-User

- 7.6.3. By Country

- 7.6.3.1. China

- 7.6.3.2. Japan

- 7.6.3.3. India

- 7.6.3.4. South Korea

- 7.6.3.5. Taiwan

- 7.6.3.6. Others

8. COMPETITIVE ENVIRONMENT AND ANALYSIS

- 8.1. Major Players and Strategy Analysis

- 8.2. Market Share Analysis

- 8.3. Mergers, Acquisitions, Agreements, and Collaborations

- 8.4. Competitive Dashboard

9. COMPANY PROFILES

- 9.1. Introduction

- 9.2. Neodymium

- 9.2.1. MP Materials

- 9.2.2. Iluka Resources

- 9.2.3. Phoenix Tailings

- 9.2.4. CVMR Corporation

- 9.2.5. Lynas Rare Earths, Ltd.

- 9.2.6. China Rare Earth Holdings Limited

- 9.3. Cerium

- 9.3.1. Iluka Resources

- 9.3.2. MP Materials

- 9.3.3. CVMR Corporation

- 9.3.4. Lynas Rare Earths, Ltd.

- 9.4. Lanthanum

- 9.4.1. Iluka Resources

- 9.4.2. MP Materials

- 9.4.3. CVMR Corporation

- 9.4.4. Lynas Rare Earths, Ltd.

- 9.5. Neodymium Magnet

- 9.5.1. Adams Magnetic Products

- 9.5.2. Dexter Magnetic Technologies

- 9.5.3. Arnold Magnetic Technologies

- 9.5.4. Vacuumschmelze GmbH & Co. KG

- 9.5.5. TDK Corporation

- 9.5.6. Hitachi Metals, Ltd.

- 9.5.7. Baotou Tianhe Magnetics Technology Co., Ltd.

- 9.5.8. Goudsmit Magnetics

- 9.5.9. Thomas and Skinner Inc.

- 9.5.10. Pacific Metals Co., Ltd.

10. APPENDIX

- 10.1. Currency

- 10.2. Assumptions

- 10.3. Base and Forecast Years Timeline

- 10.4. Key Benefits for the Stakeholders

- 10.5. Research Methodology

- 10.6. Abbreviations