|

|

市場調査レポート

商品コード

1385082

テレラジオロジーソフトウェアの世界市場規模、シェア、産業動向分析レポート:展開別、タイプ別、地域別展望と予測、2023年~2030年Global Teleradiology Software Market Size, Share & Industry Trends Analysis Report By Deployment (Web-based, Cloud-based, and On-premise), By Type, By Regional Outlook and Forecast, 2023 - 2030 |

||||||

|

|

|||||||

|

|||||||

| テレラジオロジーソフトウェアの世界市場規模、シェア、産業動向分析レポート:展開別、タイプ別、地域別展望と予測、2023年~2030年 |

|

出版日: 2023年10月31日

発行: KBV Research

ページ情報: 英文 186 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

テレラジオロジーソフトウェアの市場規模は2030年までに35億米ドルに達し、予測期間中にCAGR 10.2%の市場成長率で上昇すると予測されています。

対面診察の必要性を減らし、患者やヘルスケア従事者の感染の危険性を低減するため、遠隔画像診断ソフトウェアによって放射線科医が遠隔地から医療画像を評価できるようになっています。遠隔医療はパンデミックの間に急速に普及し、遠隔画像診断ソフトウェアは遠隔医療プラットフォームに統合され、包括的なバーチャルヘルスケア相談を提供するようになっています。これにより、COVID-19とは無関係のものも含め、さまざまな病状に苦しむ患者の遠隔診断やモニタリングが可能になっています。テレラジオロジーはヘルスケア施設が資源配分を最適化するのに役立っています。放射線科サービスをテレラジオロジー・プロバイダーに委託または共有することで、病院はCOVID-19ケアの重要な需要に対応するために院内スタッフを割り当てることができます。テレラジオロジーは、肺炎などのCOVID-19関連合併症の遠隔モニタリングや早期発見を容易にすることで、予防措置の一翼を担っています。

しかし、進化する規制状況と償還政策は、テレラジオロジー・プロバイダーにとって課題となりうる。複雑なヘルスケア償還制度を利用し、変化する規制に適応するには、継続的な努力が必要です。ヘルスケア償還方針は頻繁に変更される可能性があり、遠隔画像診断サービスの財政的な実行可能性に影響を与えます。プロバイダーは進化する償還規制に適応するため、財務計画に不確実性が生じます。テレラジオロジー診療報酬は標準化されておらず、異なる支払者(例えば、公的保険者、民間保険者)が異なる方針と要件を持つことがあります。このような統一性の欠如は、請求と償還のプロセスを複雑にしています。償還と規制の課題は、市場における大きな障害となっています。

タイプ別展望

タイプ別では、放射線情報システム(RIS)、画像アーカイブ・通信システム(PACs)、ベンダーニュートラルアーカイブ(VNA)に分類されます。2022年には、画像アーカイブ・通信システム(PACs)分野が市場で最も高い収益シェアを占めました。PACsは、ヘルスケアプロバイダーが多数の医療画像を電子的に保存・管理することを可能にします。遠隔画像診断では、放射線科医やヘルスケア専門家が患者の画像にリモートでアクセスでき、物理的な場所に関係なくタイムリーで正確な診断を提供できます。PACSはテレラジオロジー・ソフトウェアとシームレスに統合され、統一された画像解釈と報告プラットフォームを作り出します。この統合により、手作業によるデータ入力、重複作業、エラーのリスクが軽減され、最終的に遠隔画像診断医のワークフローが合理化されます。

展開の展望

展開に基づき、市場はウェブベース、クラウドベース、オンプレミスに分類されます。クラウドベースのセグメントは、2022年の市場でかなりの収益シェアを獲得しました。クラウドベースの遠隔画像診断ソフトウェアは、インターネット接続さえあればどこからでも医療画像や患者データにリモートアクセスできます。放射線科医やヘルスケア専門家は、さまざまな場所から画像を解釈し、レポートを作成することができ、アクセシビリティと柔軟性が向上します。複数の放射線科医やヘルスケア専門家が、地理的な場所に関係なく、同時に画像を確認し、複雑な症例について協力することができます。この遠隔コラボレーションにより、診断サービスの質が向上します。クラウドベースの遠隔画像診断ソフトウェアは多くの場合スケーラブルであり、ヘルスケア施設は需要に応じて容量を調整することができます。この柔軟性により、医療施設は検査数や症例数の変動に対応することができます。

地域別展望

地域別に見ると、市場は北米、欧州、アジア太平洋、ラテンアメリカ・中東・アフリカで分析されます。2022年には、北米地域が最も高い収益シェアを獲得して市場をリードしました。対象人口の新興国市場開拓、がんや骨障害などの慢性疾患の発生率、重要な市場プレーヤー、整備された医療ITインフラが、市場拡大に寄与する主な要素です。この地域の市場開拓に影響を与える主な要因は、有利な政府の取り組み、技術の進歩、高いヘルスケア費用です。

目次

第1章 市場範囲と調査手法

- 市場の定義

- 目的

- 市場範囲

- セグメンテーション

- 調査手法

第2章 市場の概要

- 主なハイライト

第3章 市場概要

- イントロダクション

- 概要

- 市場構成とシナリオ

- 概要

- 市場に影響を与える主な要因

- 市場促進要因

- 市場抑制要因

- ポーターファイブフォース分析

第4章 世界のテレラジオロジーソフトウェア市場:展開別

- 世界のウェブベース市場:地域別

- 世界のクラウドベース市場:地域別

- 世界のオンプレミス市場:地域別

第5章 世界の市場:タイプ別

- 世界の画像アーカイブ・通信システム(PAC)市場:地域別

- 世界の放射線情報システム(RIS)市場:地域別

- 世界ベンダーニュートラルアーカイブ(VNA)市場:地域別

第6章 世界の市場:地域別

- 北米の市場

- 北米の市場:展開別

- 北米の国別ウェブベース市場

- 北米の国別クラウドベース市場

- 北米の国別オンプレミス市場

- 北米の市場:タイプ別

- 北米の国別画像アーカイブ・通信システム(PAC)市場

- 北米の国別放射線情報システム(RIS)市場

- 北米の国別ベンダーニュートラルアーカイブ(VNA)市場

- 北米の市場:国別

- 米国のテレラジオロジーソフトウェア市場

- カナダのテレラジオロジーソフトウェア市場

- メキシコのテレラジオロジーソフトウェア市場

- その他の北米の市場

- 北米の市場:展開別

- 欧州の市場

- 欧州の市場:展開別

- 欧州の国別ウェブベース市場

- 欧州の国別クラウドベース市場

- 欧州の国別オンプレミス市場

- 欧州の市場:タイプ別

- 欧州の国別画像アーカイブ・通信システム(PAC)市場

- 欧州の国別放射線情報システム(RIS)市場

- 欧州の国別ベンダーニュートラルアーカイブ(VNA)市場

- 欧州の市場:国別

- ドイツのテレラジオロジーソフトウェア市場

- 英国のテレラジオロジーソフトウェア市場

- フランスのテレラジオロジーソフトウェア市場

- ロシアのテレラジオロジーソフトウェア市場

- スペインのテレラジオロジーソフトウェア市場

- イタリアのテレラジオロジーソフトウェア市場

- その他の欧州の市場

- 欧州の市場:展開別

- アジア太平洋の市場

- アジア太平洋の市場:展開別

- アジア太平洋の国別ウェブベース市場

- アジア太平洋の国別クラウドベース市場

- アジア太平洋の国別オンプレミス市場

- アジア太平洋の市場:タイプ別

- アジア太平洋の画像アーカイブ・通信システム(PAC)市場:(国別)

- アジア太平洋の国別放射線情報システム(RIS)市場

- アジア太平洋の国別ベンダーニュートラルアーカイブ(VNA)市場

- アジア太平洋の市場:国別

- 中国のテレラジオロジーソフトウェア市場

- 日本のテレラジオロジーソフトウェア市場

- インドのテレラジオロジーソフトウェア市場

- 韓国のテレラジオロジーソフトウェア市場

- シンガポールのテレラジオロジーソフトウェア市場

- マレーシアのテレラジオロジーソフトウェア市場

- その他のアジア太平洋の市場

- アジア太平洋の市場:展開別

- ラテンアメリカ・中東・アフリカの市場

- ラテンアメリカ・中東・アフリカの市場:展開別

- ラテンアメリカ・中東・アフリカの国別ウェブベース市場

- ラテンアメリカ・中東・アフリカの国別クラウドベース市場

- ラテンアメリカ・中東・アフリカの国別オンプレミス市場

- ラテンアメリカ・中東・アフリカの市場:タイプ別

- ラテンアメリカ・中東・アフリカの国別画像アーカイブ・通信システム(PAC)市場

- ラテンアメリカ・中東・アフリカの国別放射線情報システム(RIS)市場

- ラテンアメリカ・中東・アフリカの国別ベンダーニュートラルアーカイブ(VNA)市場

- ラテンアメリカ・中東・アフリカの市場:国別

- ブラジルのテレラジオロジーソフトウェア市場

- アルゼンチンのテレラジオロジーソフトウェア市場

- UAEのテレラジオロジーソフトウェア市場

- サウジアラビアのテレラジオロジーソフトウェア市場

- 南アフリカのテレラジオロジーソフトウェア市場

- ナイジェリアテレラジオロジーソフトウェア市場

- その他のラテンアメリカ・中東・アフリカの市場

- ラテンアメリカ・中東・アフリカの市場:展開別

第7章 企業プロファイル

- Carestream Health, Inc(Onex Corporation)

- Teleradiology Solutions, Inc

- Comarch SA

- RamSoft, Inc

- Koninklijke Philips NV

- Morton & Partners Radiologists

- Everrtech Software Private Limited

- Pediatrix Medical Group, Inc

- Siemens AG

- Radical Imaging LLC

第8章 テレラジオロジーソフトウェア市場の勝利の必須条件

LIST OF TABLES

- TABLE 1 Global Teleradiology Software Market, 2019 - 2022, USD Million

- TABLE 2 Global Teleradiology Software Market, 2023 - 2030, USD Million

- TABLE 3 Global Teleradiology Software Market, by Deployment, 2019 - 2022, USD Million

- TABLE 4 Global Teleradiology Software Market, by Deployment, 2023 - 2030, USD Million

- TABLE 5 Global Web-based Market, by Region, 2019 - 2022, USD Million

- TABLE 6 Global Web-based Market, by Region, 2023 - 2030, USD Million

- TABLE 7 Global Cloud-based Market, by Region, 2019 - 2022, USD Million

- TABLE 8 Global Cloud-based Market, by Region, 2023 - 2030, USD Million

- TABLE 9 Global On-premise Market, by Region, 2019 - 2022, USD Million

- TABLE 10 Global On-premise Market, by Region, 2023 - 2030, USD Million

- TABLE 11 Global Teleradiology Software Market, by Type, 2019 - 2022, USD Million

- TABLE 12 Global Teleradiology Software Market, by Type, 2023 - 2030, USD Million

- TABLE 13 Global Picture Archive and Communication System (PACs) Market, by Region, 2019 - 2022, USD Million

- TABLE 14 Global Picture Archive and Communication System (PACs) Market, by Region, 2023 - 2030, USD Million

- TABLE 15 Global Radiology Information System (RIS) Market, by Region, 2019 - 2022, USD Million

- TABLE 16 Global Radiology Information System (RIS) Market, by Region, 2023 - 2030, USD Million

- TABLE 17 Global Vendor Neutral Archive (VNA) Market, by Region, 2019 - 2022, USD Million

- TABLE 18 Global Vendor Neutral Archive (VNA) Market, by Region, 2023 - 2030, USD Million

- TABLE 19 Global Teleradiology Software Market, by Region, 2019 - 2022, USD Million

- TABLE 20 Global Teleradiology Software Market, by Region, 2023 - 2030, USD Million

- TABLE 21 North America Teleradiology Software Market, 2019 - 2022, USD Million

- TABLE 22 North America Teleradiology Software Market, 2023 - 2030, USD Million

- TABLE 23 North America Teleradiology Software Market, by Deployment, 2019 - 2022, USD Million

- TABLE 24 North America Teleradiology Software Market, by Deployment, 2023 - 2030, USD Million

- TABLE 25 North America Web-based Market, by Country, 2019 - 2022, USD Million

- TABLE 26 North America Web-based Market, by Country, 2023 - 2030, USD Million

- TABLE 27 North America Cloud-based Market, by Country, 2019 - 2022, USD Million

- TABLE 28 North America Cloud-based Market, by Country, 2023 - 2030, USD Million

- TABLE 29 North America On-premise Market, by Country, 2019 - 2022, USD Million

- TABLE 30 North America On-premise Market, by Country, 2023 - 2030, USD Million

- TABLE 31 North America Teleradiology Software Market, by Type, 2019 - 2022, USD Million

- TABLE 32 North America Teleradiology Software Market, by Type, 2023 - 2030, USD Million

- TABLE 33 North America Picture Archive and Communication System (PACs) Market, by Country, 2019 - 2022, USD Million

- TABLE 34 North America Picture Archive and Communication System (PACs) Market, by Country, 2023 - 2030, USD Million

- TABLE 35 North America Radiology Information System (RIS) Market, by Country, 2019 - 2022, USD Million

- TABLE 36 North America Radiology Information System (RIS) Market, by Country, 2023 - 2030, USD Million

- TABLE 37 North America Vendor Neutral Archive (VNA) Market, by Country, 2019 - 2022, USD Million

- TABLE 38 North America Vendor Neutral Archive (VNA) Market, by Country, 2023 - 2030, USD Million

- TABLE 39 North America Teleradiology Software Market, by Country, 2019 - 2022, USD Million

- TABLE 40 North America Teleradiology Software Market, by Country, 2023 - 2030, USD Million

- TABLE 41 US Teleradiology Software Market, 2019 - 2022, USD Million

- TABLE 42 US Teleradiology Software Market, 2023 - 2030, USD Million

- TABLE 43 US Teleradiology Software Market, by Deployment, 2019 - 2022, USD Million

- TABLE 44 US Teleradiology Software Market, by Deployment, 2023 - 2030, USD Million

- TABLE 45 US Teleradiology Software Market, by Type, 2019 - 2022, USD Million

- TABLE 46 US Teleradiology Software Market, by Type, 2023 - 2030, USD Million

- TABLE 47 Canada Teleradiology Software Market, 2019 - 2022, USD Million

- TABLE 48 Canada Teleradiology Software Market, 2023 - 2030, USD Million

- TABLE 49 Canada Teleradiology Software Market, by Deployment, 2019 - 2022, USD Million

- TABLE 50 Canada Teleradiology Software Market, by Deployment, 2023 - 2030, USD Million

- TABLE 51 Canada Teleradiology Software Market, by Type, 2019 - 2022, USD Million

- TABLE 52 Canada Teleradiology Software Market, by Type, 2023 - 2030, USD Million

- TABLE 53 Mexico Teleradiology Software Market, 2019 - 2022, USD Million

- TABLE 54 Mexico Teleradiology Software Market, 2023 - 2030, USD Million

- TABLE 55 Mexico Teleradiology Software Market, by Deployment, 2019 - 2022, USD Million

- TABLE 56 Mexico Teleradiology Software Market, by Deployment, 2023 - 2030, USD Million

- TABLE 57 Mexico Teleradiology Software Market, by Type, 2019 - 2022, USD Million

- TABLE 58 Mexico Teleradiology Software Market, by Type, 2023 - 2030, USD Million

- TABLE 59 Rest of North America Teleradiology Software Market, 2019 - 2022, USD Million

- TABLE 60 Rest of North America Teleradiology Software Market, 2023 - 2030, USD Million

- TABLE 61 Rest of North America Teleradiology Software Market, by Deployment, 2019 - 2022, USD Million

- TABLE 62 Rest of North America Teleradiology Software Market, by Deployment, 2023 - 2030, USD Million

- TABLE 63 Rest of North America Teleradiology Software Market, by Type, 2019 - 2022, USD Million

- TABLE 64 Rest of North America Teleradiology Software Market, by Type, 2023 - 2030, USD Million

- TABLE 65 Europe Teleradiology Software Market, 2019 - 2022, USD Million

- TABLE 66 Europe Teleradiology Software Market, 2023 - 2030, USD Million

- TABLE 67 Europe Teleradiology Software Market, by Deployment, 2019 - 2022, USD Million

- TABLE 68 Europe Teleradiology Software Market, by Deployment, 2023 - 2030, USD Million

- TABLE 69 Europe Web-based Market, by Country, 2019 - 2022, USD Million

- TABLE 70 Europe Web-based Market, by Country, 2023 - 2030, USD Million

- TABLE 71 Europe Cloud-based Market, by Country, 2019 - 2022, USD Million

- TABLE 72 Europe Cloud-based Market, by Country, 2023 - 2030, USD Million

- TABLE 73 Europe On-premise Market, by Country, 2019 - 2022, USD Million

- TABLE 74 Europe On-premise Market, by Country, 2023 - 2030, USD Million

- TABLE 75 Europe Teleradiology Software Market, by Type, 2019 - 2022, USD Million

- TABLE 76 Europe Teleradiology Software Market, by Type, 2023 - 2030, USD Million

- TABLE 77 Europe Picture Archive and Communication System (PACs) Market, by Country, 2019 - 2022, USD Million

- TABLE 78 Europe Picture Archive and Communication System (PACs) Market, by Country, 2023 - 2030, USD Million

- TABLE 79 Europe Radiology Information System (RIS) Market, by Country, 2019 - 2022, USD Million

- TABLE 80 Europe Radiology Information System (RIS) Market, by Country, 2023 - 2030, USD Million

- TABLE 81 Europe Vendor Neutral Archive (VNA) Market, by Country, 2019 - 2022, USD Million

- TABLE 82 Europe Vendor Neutral Archive (VNA) Market, by Country, 2023 - 2030, USD Million

- TABLE 83 Europe Teleradiology Software Market, by Country, 2019 - 2022, USD Million

- TABLE 84 Europe Teleradiology Software Market, by Country, 2023 - 2030, USD Million

- TABLE 85 Germany Teleradiology Software Market, 2019 - 2022, USD Million

- TABLE 86 Germany Teleradiology Software Market, 2023 - 2030, USD Million

- TABLE 87 Germany Teleradiology Software Market, by Deployment, 2019 - 2022, USD Million

- TABLE 88 Germany Teleradiology Software Market, by Deployment, 2023 - 2030, USD Million

- TABLE 89 Germany Teleradiology Software Market, by Type, 2019 - 2022, USD Million

- TABLE 90 Germany Teleradiology Software Market, by Type, 2023 - 2030, USD Million

- TABLE 91 UK Teleradiology Software Market, 2019 - 2022, USD Million

- TABLE 92 UK Teleradiology Software Market, 2023 - 2030, USD Million

- TABLE 93 UK Teleradiology Software Market, by Deployment, 2019 - 2022, USD Million

- TABLE 94 UK Teleradiology Software Market, by Deployment, 2023 - 2030, USD Million

- TABLE 95 UK Teleradiology Software Market, by Type, 2019 - 2022, USD Million

- TABLE 96 UK Teleradiology Software Market, by Type, 2023 - 2030, USD Million

- TABLE 97 France Teleradiology Software Market, 2019 - 2022, USD Million

- TABLE 98 France Teleradiology Software Market, 2023 - 2030, USD Million

- TABLE 99 France Teleradiology Software Market, by Deployment, 2019 - 2022, USD Million

- TABLE 100 France Teleradiology Software Market, by Deployment, 2023 - 2030, USD Million

- TABLE 101 France Teleradiology Software Market, by Type, 2019 - 2022, USD Million

- TABLE 102 France Teleradiology Software Market, by Type, 2023 - 2030, USD Million

- TABLE 103 Russia Teleradiology Software Market, 2019 - 2022, USD Million

- TABLE 104 Russia Teleradiology Software Market, 2023 - 2030, USD Million

- TABLE 105 Russia Teleradiology Software Market, by Deployment, 2019 - 2022, USD Million

- TABLE 106 Russia Teleradiology Software Market, by Deployment, 2023 - 2030, USD Million

- TABLE 107 Russia Teleradiology Software Market, by Type, 2019 - 2022, USD Million

- TABLE 108 Russia Teleradiology Software Market, by Type, 2023 - 2030, USD Million

- TABLE 109 Spain Teleradiology Software Market, 2019 - 2022, USD Million

- TABLE 110 Spain Teleradiology Software Market, 2023 - 2030, USD Million

- TABLE 111 Spain Teleradiology Software Market, by Deployment, 2019 - 2022, USD Million

- TABLE 112 Spain Teleradiology Software Market, by Deployment, 2023 - 2030, USD Million

- TABLE 113 Spain Teleradiology Software Market, by Type, 2019 - 2022, USD Million

- TABLE 114 Spain Teleradiology Software Market, by Type, 2023 - 2030, USD Million

- TABLE 115 Italy Teleradiology Software Market, 2019 - 2022, USD Million

- TABLE 116 Italy Teleradiology Software Market, 2023 - 2030, USD Million

- TABLE 117 Italy Teleradiology Software Market, by Deployment, 2019 - 2022, USD Million

- TABLE 118 Italy Teleradiology Software Market, by Deployment, 2023 - 2030, USD Million

- TABLE 119 Italy Teleradiology Software Market, by Type, 2019 - 2022, USD Million

- TABLE 120 Italy Teleradiology Software Market, by Type, 2023 - 2030, USD Million

- TABLE 121 Rest of Europe Teleradiology Software Market, 2019 - 2022, USD Million

- TABLE 122 Rest of Europe Teleradiology Software Market, 2023 - 2030, USD Million

- TABLE 123 Rest of Europe Teleradiology Software Market, by Deployment, 2019 - 2022, USD Million

- TABLE 124 Rest of Europe Teleradiology Software Market, by Deployment, 2023 - 2030, USD Million

- TABLE 125 Rest of Europe Teleradiology Software Market, by Type, 2019 - 2022, USD Million

- TABLE 126 Rest of Europe Teleradiology Software Market, by Type, 2023 - 2030, USD Million

- TABLE 127 Asia Pacific Teleradiology Software Market, 2019 - 2022, USD Million

- TABLE 128 Asia Pacific Teleradiology Software Market, 2023 - 2030, USD Million

- TABLE 129 Asia Pacific Teleradiology Software Market, by Deployment, 2019 - 2022, USD Million

- TABLE 130 Asia Pacific Teleradiology Software Market, by Deployment, 2023 - 2030, USD Million

- TABLE 131 Asia Pacific Web-based Market, by Country, 2019 - 2022, USD Million

- TABLE 132 Asia Pacific Web-based Market, by Country, 2023 - 2030, USD Million

- TABLE 133 Asia Pacific Cloud-based Market, by Country, 2019 - 2022, USD Million

- TABLE 134 Asia Pacific Cloud-based Market, by Country, 2023 - 2030, USD Million

- TABLE 135 Asia Pacific On-premise Market, by Country, 2019 - 2022, USD Million

- TABLE 136 Asia Pacific On-premise Market, by Country, 2023 - 2030, USD Million

- TABLE 137 Asia Pacific Teleradiology Software Market, by Type, 2019 - 2022, USD Million

- TABLE 138 Asia Pacific Teleradiology Software Market, by Type, 2023 - 2030, USD Million

- TABLE 139 Asia Pacific Picture Archive and Communication System (PACs) Market, by Country, 2019 - 2022, USD Million

- TABLE 140 Asia Pacific Picture Archive and Communication System (PACs) Market, by Country, 2023 - 2030, USD Million

- TABLE 141 Asia Pacific Radiology Information System (RIS) Market, by Country, 2019 - 2022, USD Million

- TABLE 142 Asia Pacific Radiology Information System (RIS) Market, by Country, 2023 - 2030, USD Million

- TABLE 143 Asia Pacific Vendor Neutral Archive (VNA) Market, by Country, 2019 - 2022, USD Million

- TABLE 144 Asia Pacific Vendor Neutral Archive (VNA) Market, by Country, 2023 - 2030, USD Million

- TABLE 145 Asia Pacific Teleradiology Software Market, by Country, 2019 - 2022, USD Million

- TABLE 146 Asia Pacific Teleradiology Software Market, by Country, 2023 - 2030, USD Million

- TABLE 147 China Teleradiology Software Market, 2019 - 2022, USD Million

- TABLE 148 China Teleradiology Software Market, 2023 - 2030, USD Million

- TABLE 149 China Teleradiology Software Market, by Deployment, 2019 - 2022, USD Million

- TABLE 150 China Teleradiology Software Market, by Deployment, 2023 - 2030, USD Million

- TABLE 151 China Teleradiology Software Market, by Type, 2019 - 2022, USD Million

- TABLE 152 China Teleradiology Software Market, by Type, 2023 - 2030, USD Million

- TABLE 153 Japan Teleradiology Software Market, 2019 - 2022, USD Million

- TABLE 154 Japan Teleradiology Software Market, 2023 - 2030, USD Million

- TABLE 155 Japan Teleradiology Software Market, by Deployment, 2019 - 2022, USD Million

- TABLE 156 Japan Teleradiology Software Market, by Deployment, 2023 - 2030, USD Million

- TABLE 157 Japan Teleradiology Software Market, by Type, 2019 - 2022, USD Million

- TABLE 158 Japan Teleradiology Software Market, by Type, 2023 - 2030, USD Million

- TABLE 159 India Teleradiology Software Market, 2019 - 2022, USD Million

- TABLE 160 India Teleradiology Software Market, 2023 - 2030, USD Million

- TABLE 161 India Teleradiology Software Market, by Deployment, 2019 - 2022, USD Million

- TABLE 162 India Teleradiology Software Market, by Deployment, 2023 - 2030, USD Million

- TABLE 163 India Teleradiology Software Market, by Type, 2019 - 2022, USD Million

- TABLE 164 India Teleradiology Software Market, by Type, 2023 - 2030, USD Million

- TABLE 165 South Korea Teleradiology Software Market, 2019 - 2022, USD Million

- TABLE 166 South Korea Teleradiology Software Market, 2023 - 2030, USD Million

- TABLE 167 South Korea Teleradiology Software Market, by Deployment, 2019 - 2022, USD Million

- TABLE 168 South Korea Teleradiology Software Market, by Deployment, 2023 - 2030, USD Million

- TABLE 169 South Korea Teleradiology Software Market, by Type, 2019 - 2022, USD Million

- TABLE 170 South Korea Teleradiology Software Market, by Type, 2023 - 2030, USD Million

- TABLE 171 Singapore Teleradiology Software Market, 2019 - 2022, USD Million

- TABLE 172 Singapore Teleradiology Software Market, 2023 - 2030, USD Million

- TABLE 173 Singapore Teleradiology Software Market, by Deployment, 2019 - 2022, USD Million

- TABLE 174 Singapore Teleradiology Software Market, by Deployment, 2023 - 2030, USD Million

- TABLE 175 Singapore Teleradiology Software Market, by Type, 2019 - 2022, USD Million

- TABLE 176 Singapore Teleradiology Software Market, by Type, 2023 - 2030, USD Million

- TABLE 177 Malaysia Teleradiology Software Market, 2019 - 2022, USD Million

- TABLE 178 Malaysia Teleradiology Software Market, 2023 - 2030, USD Million

- TABLE 179 Malaysia Teleradiology Software Market, by Deployment, 2019 - 2022, USD Million

- TABLE 180 Malaysia Teleradiology Software Market, by Deployment, 2023 - 2030, USD Million

- TABLE 181 Malaysia Teleradiology Software Market, by Type, 2019 - 2022, USD Million

- TABLE 182 Malaysia Teleradiology Software Market, by Type, 2023 - 2030, USD Million

- TABLE 183 Rest of Asia Pacific Teleradiology Software Market, 2019 - 2022, USD Million

- TABLE 184 Rest of Asia Pacific Teleradiology Software Market, 2023 - 2030, USD Million

- TABLE 185 Rest of Asia Pacific Teleradiology Software Market, by Deployment, 2019 - 2022, USD Million

- TABLE 186 Rest of Asia Pacific Teleradiology Software Market, by Deployment, 2023 - 2030, USD Million

- TABLE 187 Rest of Asia Pacific Teleradiology Software Market, by Type, 2019 - 2022, USD Million

- TABLE 188 Rest of Asia Pacific Teleradiology Software Market, by Type, 2023 - 2030, USD Million

- TABLE 189 LAMEA Teleradiology Software Market, 2019 - 2022, USD Million

- TABLE 190 LAMEA Teleradiology Software Market, 2023 - 2030, USD Million

- TABLE 191 LAMEA Teleradiology Software Market, by Deployment, 2019 - 2022, USD Million

- TABLE 192 LAMEA Teleradiology Software Market, by Deployment, 2023 - 2030, USD Million

- TABLE 193 LAMEA Web-based Market, by Country, 2019 - 2022, USD Million

- TABLE 194 LAMEA Web-based Market, by Country, 2023 - 2030, USD Million

- TABLE 195 LAMEA Cloud-based Market, by Country, 2019 - 2022, USD Million

- TABLE 196 LAMEA Cloud-based Market, by Country, 2023 - 2030, USD Million

- TABLE 197 LAMEA On-premise Market, by Country, 2019 - 2022, USD Million

- TABLE 198 LAMEA On-premise Market, by Country, 2023 - 2030, USD Million

- TABLE 199 LAMEA Teleradiology Software Market, by Type, 2019 - 2022, USD Million

- TABLE 200 LAMEA Teleradiology Software Market, by Type, 2023 - 2030, USD Million

- TABLE 201 LAMEA Picture Archive and Communication System (PACs) Market, by Country, 2019 - 2022, USD Million

- TABLE 202 LAMEA Picture Archive and Communication System (PACs) Market, by Country, 2023 - 2030, USD Million

- TABLE 203 LAMEA Radiology Information System (RIS) Market, by Country, 2019 - 2022, USD Million

- TABLE 204 LAMEA Radiology Information System (RIS) Market, by Country, 2023 - 2030, USD Million

- TABLE 205 LAMEA Vendor Neutral Archive (VNA) Market, by Country, 2019 - 2022, USD Million

- TABLE 206 LAMEA Vendor Neutral Archive (VNA) Market, by Country, 2023 - 2030, USD Million

- TABLE 207 LAMEA Teleradiology Software Market, by Country, 2019 - 2022, USD Million

- TABLE 208 LAMEA Teleradiology Software Market, by Country, 2023 - 2030, USD Million

- TABLE 209 Brazil Teleradiology Software Market, 2019 - 2022, USD Million

- TABLE 210 Brazil Teleradiology Software Market, 2023 - 2030, USD Million

- TABLE 211 Brazil Teleradiology Software Market, by Deployment, 2019 - 2022, USD Million

- TABLE 212 Brazil Teleradiology Software Market, by Deployment, 2023 - 2030, USD Million

- TABLE 213 Brazil Teleradiology Software Market, by Type, 2019 - 2022, USD Million

- TABLE 214 Brazil Teleradiology Software Market, by Type, 2023 - 2030, USD Million

- TABLE 215 Argentina Teleradiology Software Market, 2019 - 2022, USD Million

- TABLE 216 Argentina Teleradiology Software Market, 2023 - 2030, USD Million

- TABLE 217 Argentina Teleradiology Software Market, by Deployment, 2019 - 2022, USD Million

- TABLE 218 Argentina Teleradiology Software Market, by Deployment, 2023 - 2030, USD Million

- TABLE 219 Argentina Teleradiology Software Market, by Type, 2019 - 2022, USD Million

- TABLE 220 Argentina Teleradiology Software Market, by Type, 2023 - 2030, USD Million

- TABLE 221 UAE Teleradiology Software Market, 2019 - 2022, USD Million

- TABLE 222 UAE Teleradiology Software Market, 2023 - 2030, USD Million

- TABLE 223 UAE Teleradiology Software Market, by Deployment, 2019 - 2022, USD Million

- TABLE 224 UAE Teleradiology Software Market, by Deployment, 2023 - 2030, USD Million

- TABLE 225 UAE Teleradiology Software Market, by Type, 2019 - 2022, USD Million

- TABLE 226 UAE Teleradiology Software Market, by Type, 2023 - 2030, USD Million

- TABLE 227 Saudi Arabia Teleradiology Software Market, 2019 - 2022, USD Million

- TABLE 228 Saudi Arabia Teleradiology Software Market, 2023 - 2030, USD Million

- TABLE 229 Saudi Arabia Teleradiology Software Market, by Deployment, 2019 - 2022, USD Million

- TABLE 230 Saudi Arabia Teleradiology Software Market, by Deployment, 2023 - 2030, USD Million

- TABLE 231 Saudi Arabia Teleradiology Software Market, by Type, 2019 - 2022, USD Million

- TABLE 232 Saudi Arabia Teleradiology Software Market, by Type, 2023 - 2030, USD Million

- TABLE 233 South Africa Teleradiology Software Market, 2019 - 2022, USD Million

- TABLE 234 South Africa Teleradiology Software Market, 2023 - 2030, USD Million

- TABLE 235 South Africa Teleradiology Software Market, by Deployment, 2019 - 2022, USD Million

- TABLE 236 South Africa Teleradiology Software Market, by Deployment, 2023 - 2030, USD Million

- TABLE 237 South Africa Teleradiology Software Market, by Type, 2019 - 2022, USD Million

- TABLE 238 South Africa Teleradiology Software Market, by Type, 2023 - 2030, USD Million

- TABLE 239 Nigeria Teleradiology Software Market, 2019 - 2022, USD Million

- TABLE 240 Nigeria Teleradiology Software Market, 2023 - 2030, USD Million

- TABLE 241 Nigeria Teleradiology Software Market, by Deployment, 2019 - 2022, USD Million

- TABLE 242 Nigeria Teleradiology Software Market, by Deployment, 2023 - 2030, USD Million

- TABLE 243 Nigeria Teleradiology Software Market, by Type, 2019 - 2022, USD Million

- TABLE 244 Nigeria Teleradiology Software Market, by Type, 2023 - 2030, USD Million

- TABLE 245 Rest of LAMEA Teleradiology Software Market, 2019 - 2022, USD Million

- TABLE 246 Rest of LAMEA Teleradiology Software Market, 2023 - 2030, USD Million

- TABLE 247 Rest of LAMEA Teleradiology Software Market, by Deployment, 2019 - 2022, USD Million

- TABLE 248 Rest of LAMEA Teleradiology Software Market, by Deployment, 2023 - 2030, USD Million

- TABLE 249 Rest of LAMEA Teleradiology Software Market, by Type, 2019 - 2022, USD Million

- TABLE 250 Rest of LAMEA Teleradiology Software Market, by Type, 2023 - 2030, USD Million

- TABLE 251 Key Information - Carestream Health, Inc.

- TABLE 252 Key Information - Teleradiology Solutions, Inc.

- TABLE 253 key Information - Comarch SA

- TABLE 254 Key Information - RamSoft, Inc.

- TABLE 255 Key Information - Koninklijke Philips N.V.

- TABLE 256 Key Information - Morton & Partners Radiologists

- TABLE 257 Key Information - Everrtech Software Private Limited

- TABLE 258 Key Information - Pediatrix Medical Group, Inc.

- TABLE 259 Key Information - Siemens AG

- TABLE 260 Key Information - Radical Imaging LLC.

The Global Teleradiology Software Market size is expected to reach $3.5 billion by 2030, rising at a market growth of 10.2% CAGR during the forecast period.

The need for medical imaging in the Asia Pacific region is driven by a significant unmet medical need brought on by chronic diseases, including cancer and cardiovascular disease. Consequently, the APAC region accounted for $430.9 million revenue in the market in 2022. Additionally, encouraging government initiatives in the region of digital health, the increasing uptake of cutting-edge technology, and the scarcity of radiologists in several nations, including India, all contribute to the growth of this market. Some of the factors impacting the market are rising incidence of chronic diseases, improved access to specialized care, and evolving reimbursement and regulation policies.

The demand for diagnostic imaging services has surged due to the rising incidence of chronic diseases like cancer. Teleradiology provides a means to manage the resulting increase in imaging studies. Chronic diseases often require ongoing monitoring and diagnostic imaging to assess the progression and response to treatment. Conditions like cancer, cardiovascular diseases, and diabetes necessitate frequent medical imaging studies, including X-rays, MRIs, CT scans, and ultrasounds. Teleradiology allows healthcare facilities to access specialized radiologists remotely, ensuring patients receive accurate and timely diagnoses, even if these subspecialists are unavailable on-site. Additionally, Teleradiology allows patients and healthcare facilities in underserved or remote areas to access specialized radiology services. This increases the availability of expert opinions and timely diagnoses. Access to specialized radiologists via teleradiology can lead to quicker and more accurate diagnoses. This is crucial in cases where rapid diagnosis is essential for effective treatment, such as in certain types of cancer. Patients with specific conditions benefit from having access to subspecialists. Teleradiology connects patients with the right experts, even in different locations, ensuring they receive specialized care. Many teleradiology software solutions include teleconsultation features, enabling healthcare providers to consult with radiologists and specialists in real time. This enhances the quality of care and the exchange of medical knowledge. Improved access to specialized care is a significant driver in expanding the market.

To reduce the need for in-person consultations and lower the danger of infection for patients and healthcare personnel, teleradiology software enabled radiologists to evaluate medical pictures from remote places. Telemedicine saw rapid adoption during the pandemic, and teleradiology software was integrated into telehealth platforms to provide comprehensive virtual healthcare consultations. This allowed for the remote diagnosis and monitoring of patients suffering from various medical conditions, including those unrelated to COVID-19. Teleradiology helped healthcare facilities optimize resource allocation. By outsourcing or sharing radiology services with teleradiology providers, hospitals allocate their in-house staff to address the critical demands of COVID-19 care. Teleradiology played a role in preventive measures by facilitating the remote monitoring and early detection of COVID-19-related complications, such as pneumonia.

However, the evolving regulatory landscape and reimbursement policies can pose challenges for teleradiology providers. Navigating the complex healthcare reimbursement system and adapting to changing regulations require ongoing effort. Healthcare reimbursement policies can change frequently, affecting the financial viability of teleradiology services. Providers adapt to evolving reimbursement regulations, which can create uncertainty in financial planning. Teleradiology reimbursement lacks standardization, and different payers (e.g., public, and private insurers) may have different policies and requirements. This lack of uniformity complicates billing and reimbursement processes. Reimbursement and regulation challenges are significant obstacles in the market.

Type Outlook

By type, the market is categorized into radiology information system (RIS), picture archive and communication system (PACs), and vendor neutral archive (VNA). In 2022, the picture archive and communication system (PACs) segment held the highest revenue share in the market. PACs allow healthcare providers to electronically store and manage many medical images. In teleradiology, radiologists and healthcare professionals can access patient images remotely, providing timely and accurate diagnoses regardless of physical location. PACS integrates seamlessly with teleradiology software, creating a unified image interpretation and reporting platform. This integration reduces manual data entry, duplication of efforts, and the risk of errors, ultimately streamlining the workflow of teleradiologists.

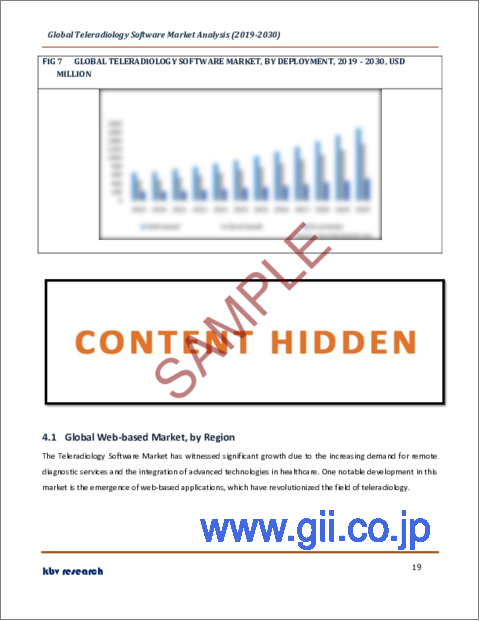

Deployment Outlook

Based on deployment, the market is classified into web-based, cloud-based, and on-premise. The cloud-based segment acquired a substantial revenue share in the market in 2022. Cloud-based teleradiology software allows remote access to medical images and patient data from anywhere with an internet connection. Radiologists and healthcare professionals can interpret images and generate reports from different locations, improving accessibility and flexibility. Multiple radiologists and healthcare professionals can simultaneously review images and collaborate on complex cases, regardless of their geographic locations. This remote collaboration enhances the quality of diagnostic services. Cloud-based teleradiology software is often scalable, allowing healthcare facilities to adjust their capacity based on demand. This flexibility ensures they can accommodate fluctuations in the number of studies and cases.

Regional Outlook

Region-wise, the market is analysed across North America, Europe, Asia Pacific, and LAMEA. In 2022, the North America region led the market by generating the highest revenue share. Increasing the target population, the incidence of chronic diseases such as cancer and bone impairments, significant market players, and a well-developed healthcare IT infrastructure are the primary elements contributing to the expansion. The primary factors influencing regional market development are favorable government efforts, technological advancements, and high healthcare expenses.

The market research report covers the analysis of key stake holders of the market. Key companies profiled in the report include Carestream Health, Inc. (Onex Corporation), Teleradiology Solutions, Inc., Comarch SA, RamSoft, Inc., Koninklijke Philips N.V., Morton and Partners Radiologists, Everrtech Software Private Limited, Pediatrix Medical Group, Inc., Siemens AG, and Radical Imaging LLC.

Scope of the Study

By Deployment

- Web-based

- Cloud-based

- On-premise

By Type

- Picture Archive and Communication System (PACs)

- Radiology Information System (RIS)

- Vendor Neutral Archive (VNA)

By Geography

- North America

- US

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- UK

- France

- Russia

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Singapore

- Malaysia

- Rest of Asia Pacific

- LAMEA

- Brazil

- Argentina

- UAE

- Saudi Arabia

- South Africa

- Nigeria

- Rest of LAMEA

Companies Profiled

- Carestream Health, Inc. (Onex Corporation)

- Teleradiology Solutions, Inc.

- Comarch SA

- RamSoft, Inc.

- Koninklijke Philips N.V.

- Morton and Partners Radiologists

- Everrtech Software Private Limited

- Pediatrix Medical Group, Inc.

- Siemens AG

- Radical Imaging LLC.

Unique Offerings from KBV Research

- Exhaustive coverage

- Highest number of market tables and figures

- Subscription based model available

- Guaranteed best price

- Assured post sales research support with 10% customization free

Table of Contents

Chapter 1. Market Scope & Methodology

- 1.1 Market Definition

- 1.2 Objectives

- 1.3 Market Scope

- 1.4 Segmentation

- 1.4.1 Global Teleradiology Software Market, by Deployment

- 1.4.2 Global Teleradiology Software Market, by Type

- 1.4.3 Global Teleradiology Software Market, by Geography

- 1.5 Methodology for the research

Chapter 2. Market At a Glance

- 2.1 Key Highlights

Chapter 3. Market Overview

- 3.1 Introduction

- 3.1.1 Overview

- 3.1.1.1 Market Composition and Scenario

- 3.1.1 Overview

- 3.2 Key Factors Impacting the Market

- 3.2.1 Market Drivers

- 3.2.2 Market Restraints

- 3.3 Porter Five Forces Analysis

Chapter 4. Global Teleradiology Software Market, by Deployment

- 4.1 Global Web-based Market, by Region

- 4.2 Global Cloud-based Market, by Region

- 4.3 Global On-premise Market, by Region

Chapter 5. Global Teleradiology Software Market, by Type

- 5.1 Global Picture Archive and Communication System (PACs) Market, by Region

- 5.2 Global Radiology Information System (RIS) Market, by Region

- 5.3 Global Vendor Neutral Archive (VNA) Market, by Region

Chapter 6. Global Teleradiology Software Market, by Region

- 6.1 North America Teleradiology Software Market

- 6.1.1 North America Teleradiology Software Market, by Deployment

- 6.1.1.1 North America Web-based Market, by Country

- 6.1.1.2 North America Cloud-based Market, by Country

- 6.1.1.3 North America On-premise Market, by Country

- 6.1.2 North America Teleradiology Software Market, by Type

- 6.1.2.1 North America Picture Archive and Communication System (PACs) Market, by Country

- 6.1.2.2 North America Radiology Information System (RIS) Market, by Country

- 6.1.2.3 North America Vendor Neutral Archive (VNA) Market, by Country

- 6.1.3 North America Teleradiology Software Market, by Country

- 6.1.3.1 US Teleradiology Software Market

- 6.1.3.1.1 US Teleradiology Software Market, by Deployment

- 6.1.3.1.2 US Teleradiology Software Market, by Type

- 6.1.3.2 Canada Teleradiology Software Market

- 6.1.3.2.1 Canada Teleradiology Software Market, by Deployment

- 6.1.3.2.2 Canada Teleradiology Software Market, by Type

- 6.1.3.3 Mexico Teleradiology Software Market

- 6.1.3.3.1 Mexico Teleradiology Software Market, by Deployment

- 6.1.3.3.2 Mexico Teleradiology Software Market, by Type

- 6.1.3.4 Rest of North America Teleradiology Software Market

- 6.1.3.4.1 Rest of North America Teleradiology Software Market, by Deployment

- 6.1.3.4.2 Rest of North America Teleradiology Software Market, by Type

- 6.1.3.1 US Teleradiology Software Market

- 6.1.1 North America Teleradiology Software Market, by Deployment

- 6.2 Europe Teleradiology Software Market

- 6.2.1 Europe Teleradiology Software Market, by Deployment

- 6.2.1.1 Europe Web-based Market, by Country

- 6.2.1.2 Europe Cloud-based Market, by Country

- 6.2.1.3 Europe On-premise Market, by Country

- 6.2.2 Europe Teleradiology Software Market, by Type

- 6.2.2.1 Europe Picture Archive and Communication System (PACs) Market, by Country

- 6.2.2.2 Europe Radiology Information System (RIS) Market, by Country

- 6.2.2.3 Europe Vendor Neutral Archive (VNA) Market, by Country

- 6.2.3 Europe Teleradiology Software Market, by Country

- 6.2.3.1 Germany Teleradiology Software Market

- 6.2.3.1.1 Germany Teleradiology Software Market, by Deployment

- 6.2.3.1.2 Germany Teleradiology Software Market, by Type

- 6.2.3.2 UK Teleradiology Software Market

- 6.2.3.2.1 UK Teleradiology Software Market, by Deployment

- 6.2.3.2.2 UK Teleradiology Software Market, by Type

- 6.2.3.3 France Teleradiology Software Market

- 6.2.3.3.1 France Teleradiology Software Market, by Deployment

- 6.2.3.3.2 France Teleradiology Software Market, by Type

- 6.2.3.4 Russia Teleradiology Software Market

- 6.2.3.4.1 Russia Teleradiology Software Market, by Deployment

- 6.2.3.4.2 Russia Teleradiology Software Market, by Type

- 6.2.3.5 Spain Teleradiology Software Market

- 6.2.3.5.1 Spain Teleradiology Software Market, by Deployment

- 6.2.3.5.2 Spain Teleradiology Software Market, by Type

- 6.2.3.6 Italy Teleradiology Software Market

- 6.2.3.6.1 Italy Teleradiology Software Market, by Deployment

- 6.2.3.6.2 Italy Teleradiology Software Market, by Type

- 6.2.3.7 Rest of Europe Teleradiology Software Market

- 6.2.3.7.1 Rest of Europe Teleradiology Software Market, by Deployment

- 6.2.3.7.2 Rest of Europe Teleradiology Software Market, by Type

- 6.2.3.1 Germany Teleradiology Software Market

- 6.2.1 Europe Teleradiology Software Market, by Deployment

- 6.3 Asia Pacific Teleradiology Software Market

- 6.3.1 Asia Pacific Teleradiology Software Market, by Deployment

- 6.3.1.1 Asia Pacific Web-based Market, by Country

- 6.3.1.2 Asia Pacific Cloud-based Market, by Country

- 6.3.1.3 Asia Pacific On-premise Market, by Country

- 6.3.2 Asia Pacific Teleradiology Software Market, by Type

- 6.3.2.1 Asia Pacific Picture Archive and Communication System (PACs) Market, by Country

- 6.3.2.2 Asia Pacific Radiology Information System (RIS) Market, by Country

- 6.3.2.3 Asia Pacific Vendor Neutral Archive (VNA) Market, by Country

- 6.3.3 Asia Pacific Teleradiology Software Market, by Country

- 6.3.3.1 China Teleradiology Software Market

- 6.3.3.1.1 China Teleradiology Software Market, by Deployment

- 6.3.3.1.2 China Teleradiology Software Market, by Type

- 6.3.3.2 Japan Teleradiology Software Market

- 6.3.3.2.1 Japan Teleradiology Software Market, by Deployment

- 6.3.3.2.2 Japan Teleradiology Software Market, by Type

- 6.3.3.3 India Teleradiology Software Market

- 6.3.3.3.1 India Teleradiology Software Market, by Deployment

- 6.3.3.3.2 India Teleradiology Software Market, by Type

- 6.3.3.4 South Korea Teleradiology Software Market

- 6.3.3.4.1 South Korea Teleradiology Software Market, by Deployment

- 6.3.3.4.2 South Korea Teleradiology Software Market, by Type

- 6.3.3.5 Singapore Teleradiology Software Market

- 6.3.3.5.1 Singapore Teleradiology Software Market, by Deployment

- 6.3.3.5.2 Singapore Teleradiology Software Market, by Type

- 6.3.3.6 Malaysia Teleradiology Software Market

- 6.3.3.6.1 Malaysia Teleradiology Software Market, by Deployment

- 6.3.3.6.2 Malaysia Teleradiology Software Market, by Type

- 6.3.3.7 Rest of Asia Pacific Teleradiology Software Market

- 6.3.3.7.1 Rest of Asia Pacific Teleradiology Software Market, by Deployment

- 6.3.3.7.2 Rest of Asia Pacific Teleradiology Software Market, by Type

- 6.3.3.1 China Teleradiology Software Market

- 6.3.1 Asia Pacific Teleradiology Software Market, by Deployment

- 6.4 LAMEA Teleradiology Software Market

- 6.4.1 LAMEA Teleradiology Software Market, by Deployment

- 6.4.1.1 LAMEA Web-based Market, by Country

- 6.4.1.2 LAMEA Cloud-based Market, by Country

- 6.4.1.3 LAMEA On-premise Market, by Country

- 6.4.2 LAMEA Teleradiology Software Market, by Type

- 6.4.2.1 LAMEA Picture Archive and Communication System (PACs) Market, by Country

- 6.4.2.2 LAMEA Radiology Information System (RIS) Market, by Country

- 6.4.2.3 LAMEA Vendor Neutral Archive (VNA) Market, by Country

- 6.4.3 LAMEA Teleradiology Software Market, by Country

- 6.4.3.1 Brazil Teleradiology Software Market

- 6.4.3.1.1 Brazil Teleradiology Software Market, by Deployment

- 6.4.3.1.2 Brazil Teleradiology Software Market, by Type

- 6.4.3.2 Argentina Teleradiology Software Market

- 6.4.3.2.1 Argentina Teleradiology Software Market, by Deployment

- 6.4.3.2.2 Argentina Teleradiology Software Market, by Type

- 6.4.3.3 UAE Teleradiology Software Market

- 6.4.3.3.1 UAE Teleradiology Software Market, by Deployment

- 6.4.3.3.2 UAE Teleradiology Software Market, by Type

- 6.4.3.4 Saudi Arabia Teleradiology Software Market

- 6.4.3.4.1 Saudi Arabia Teleradiology Software Market, by Deployment

- 6.4.3.4.2 Saudi Arabia Teleradiology Software Market, by Type

- 6.4.3.5 South Africa Teleradiology Software Market

- 6.4.3.5.1 South Africa Teleradiology Software Market, by Deployment

- 6.4.3.5.2 South Africa Teleradiology Software Market, by Type

- 6.4.3.6 Nigeria Teleradiology Software Market

- 6.4.3.6.1 Nigeria Teleradiology Software Market, by Deployment

- 6.4.3.6.2 Nigeria Teleradiology Software Market, by Type

- 6.4.3.7 Rest of LAMEA Teleradiology Software Market

- 6.4.3.7.1 Rest of LAMEA Teleradiology Software Market, by Deployment

- 6.4.3.7.2 Rest of LAMEA Teleradiology Software Market, by Type

- 6.4.3.1 Brazil Teleradiology Software Market

- 6.4.1 LAMEA Teleradiology Software Market, by Deployment

Chapter 7. Company Profiles

- 7.1 Carestream Health, Inc. (Onex Corporation)

- 7.1.1 Company Overview

- 7.1.2 Recent strategies and developments:

- 7.1.2.1 Partnerships, Collaborations, and Agreements:

- 7.1.2.2 Product Launches and Product Expansions:

- 7.1.3 SWOT Analysis

- 7.2 Teleradiology Solutions, Inc.

- 7.2.1 Company Overview

- 7.2.2 SWOT Analysis

- 7.3 Comarch SA

- 7.3.1 Company Overview

- 7.3.2 Financial Analysis

- 7.3.3 Research & Development Expense

- 7.3.4 SWOT Analysis

- 7.4 RamSoft, Inc.

- 7.4.1 Company Overview

- 7.4.2 Recent strategies and developments:

- 7.4.2.1 Product Launches and Product Expansions:

- 7.4.2.2 Acquisition and Mergers:

- 7.4.3 SWOT Analysis

- 7.5 Koninklijke Philips N.V.

- 7.5.1 Company Overview

- 7.5.2 Financial Analysis

- 7.5.3 Segmental and Regional Analysis

- 7.5.4 Research & Development Expense

- 7.5.5 Recent strategies and developments:

- 7.5.5.1 Partnerships, Collaborations, and Agreements:

- 7.5.6 SWOT Analysis

- 7.6 Morton & Partners Radiologists

- 7.6.1 Company Overview

- 7.6.2 SWOT Analysis

- 7.7 Everrtech Software Private Limited

- 7.7.1 Company Overview

- 7.8 Pediatrix Medical Group, Inc.

- 7.8.1 Company Overview

- 7.8.2 Financial Analysis

- 7.8.3 SWOT Analysis

- 7.9 Siemens AG

- 7.9.1 Company Overview

- 7.9.2 Financial Analysis

- 7.9.3 Segmental and Regional Analysis

- 7.9.4 Research & Development Expense

- 7.9.5 Recent strategies and developments:

- 7.9.5.1 Partnerships, Collaborations, and Agreements:

- 7.9.6 SWOT Analysis

- 7.10. Radical Imaging LLC.

- 7.10.1 Company Overview

- 7.10.2 SWOT Analysis