|

|

市場調査レポート

商品コード

1219682

半導体製造装置の世界市場規模、シェア、産業動向分析レポート:次元別、サプライチェーンプロセス別、製品タイプ別、機能別、地域別展望と予測、2022年~2028年Global Semiconductor Production Equipment Market Size, Share & Industry Trends Analysis Report By Dimension, By Supply Chain Process, By Product Type, By Function, By Regional Outlook and Forecast, 2022 - 2028 |

||||||

|

|

|||||||

| 半導体製造装置の世界市場規模、シェア、産業動向分析レポート:次元別、サプライチェーンプロセス別、製品タイプ別、機能別、地域別展望と予測、2022年~2028年 |

|

出版日: 2023年01月31日

発行: KBV Research

ページ情報: 英文 255 Pages

納期: 即納可能

|

- 全表示

- 概要

- 図表

- 目次

半導体製造装置の世界市場規模は、2028年までに1538億米ドルに達し、予測期間中にCAGR9.2%の市場成長率で上昇すると予測されています。

半導体加工は繊細なため、切断、乾燥、洗浄、エッチング、組み立てなどの自動化された工程を正確に監視し、温度や湿度などの作業パラメータを完全に制御する必要があります。このような自動化された工程や、半導体が作られる環境をよりよく管理するためのソリューションが、半導体製造装置です。半導体製造装置は、生産性の向上、生産量と信頼性の向上、生産エラーと設計エラーの減少、プロセスと装置のダウンタイムの減少、職場のセキュリティ強化など、多くの利点を提供します。

COVID-19影響度分析

パンデミックは、半導体製造装置市場にマイナスの影響を与えました。COVID-19が大流行した際、半導体のサプライチェーンにも大きな不足が生じたため、電子産業は悪影響を受けた。COVID-19の封鎖により、半導体分野の多くの部品が生産できなくなり、世界的に半導体の供給不足が発生しました。また、もともと半導体のエンドユーザーは、不況の影響で生産設備の購入を控えていました。その後、いくつかの企業で回復の兆しが見られるようになっています。

市場の成長要因

世界の家電製品の需要拡大

家電製品、医療機器、センサーシステムなどのメーカーによる半導体チップの需要拡大が、半導体ビジネスの成長を後押ししています。携帯電話、ノートパソコン、テレビなどの家電製品を使用する人が増えているため、産業が拡大しています。半導体は、通信、情報技術、機械自動化、電力・太陽光発電など、家電製品に関連する多くの分野で不可欠であるため、生産設備のニーズは高まると予想されます。デジタルコンテンツの増加や接続性の向上、また今後数年間のモビリティの向上により、市場の拡大がさらに促進されるでしょう。

自動車産業における半導体利用の増加

自動車産業は、最近の不況や需要の変動にもかかわらず、半導体ベンダーにとって重要な需要源であるとともに、潜在的な可能性の源泉であり続けています。自律走行車や電気自動車の需要の増加、自動車1台あたりの半導体部品数の増加といった動向は、半導体メーカーにとって重要な動機付けとなります。自動車に搭載されるセンサー、マイクロコントローラー、レーダーチップなどの半導体部品の増加に伴い、半導体製造装置の市場も拡大しています。

市場抑制要因

機械の高コスト化、サプライチェーンの寸断

半導体製造装置市場のサプライチェーンには、多くの参入企業が存在します。しかし、コロナウイルスの大流行により、市場のサプライチェーンに大きな支障をきたしました。半導体製造工場の立地は、整然とした地域であることが求められます。さらに、半導体を作るために供給される装置にキズがあってはならないです。何より、半導体製造装置は高価であり、多額の先行投資を必要とします。機械価格の変動が市場拡大の妨げになることが予想されます。

寸法の見通し

半導体製造装置市場は、2次元、2.5次元、3次元に分類されます。2次元セグメントは、2021年の半導体製造装置市場でかなりの収益シェアを獲得しました。2次元半導体は、再利用性だけでなく、長さを減らすことができ、さらに時間とシステムコストを削減することができます。このため、2次元半導体製造装置市場は急成長しています。

サプライチェーンプロセスの展望

半導体製造装置市場は、サプライチェーンプロセスによってIDM、OSAT、ファウンドリーに分類されます。2021年の半導体製造装置市場では、OSAT分野がかなりの成長率を調達しました。OSAT(Outsourced semiconductor assembly and test)企業は、テストサービスやサードパーティのICパッケージングを提供しています。OSATは、ファウンドリで製造されたシリコン製品を市場に出す前に、テストとパッケージングを行う企業です。

製品タイプ別の展望

半導体製造装置市場は、製品タイプ別に前工程用装置と後工程用装置に分類されます。2021年の半導体製造装置市場では、前工程装置が最大の収益シェアを獲得しました。半導体の製造に使用される製造ツールはすべて前工程装置に含まれます。IoTデバイスやCPU、GPUなどに使用される高効率で高密度なチップの需要が高まっていることが、このセグメントの拡大の一因となっています。

機能別の展望

半導体製造装置市場は、機能別に集積回路とOSDに区分されます。2021年の半導体製造装置市場では、集積回路(IC)分野が最大の売上シェアを占めました。集積回路製造装置(IDM)は、半導体産業における生産および販売プロセスの各段階を監督します。IDMは、コスト削減、製造工場の最適な操業の維持、市場戦略の策定を支援します。このようなIDMのメリットが、同分野の成長要因となっています。

地域別の概況

半導体製造装置市場を地域別に見ると、北米、欧州、アジア太平洋、LAMEAの4地域で分析されています。アジア太平洋地域は、2021年の半導体製造装置市場で最大の収益シェアを記録しました。この地域は、半導体需要の恩恵を受ける半導体産業が大きく、このセグメントの上昇に寄与しています。このことは、同地域の半導体製造装置市場の予後に好影響を与えています。

市場参入企業がとる主な戦略は、「買収」です。カーディナルマトリックスに記載されている分析によると、Applied Materials, Inc.、ASML Holdings N.V.、Lam Research Corporation、KLA Corporationが半導体製造装置市場の先行者であることがわかります。Carl Zeiss AG、Teradyne, Inc.、Screen Holdingsなどの企業が、半導体製造装置市場における主要なイノベーターとして挙げられます。

目次

第1章 市場の範囲と調査手法

- 市場の定義

- 目的

- 市場規模

- セグメンテーション

- 半導体製造装置の世界市場:ディメンション別

- 半導体製造装置の世界市場:サプライチェーンプロセス別

- 半導体製造装置の世界市場:製品タイププロセス別

- 半導体製造装置の世界市場:機能別

- 半導体製造装置の世界市場:地域別

- 調査手法

第2章 市場概要

- イントロダクション

- 概要説明

- 市場の構成とシナリオ

- 概要説明

- 市場に影響を与える主な要因

- 市場促進要因

- 市場の抑制要因

第3章 競合分析-世界

- KBVカーディナルマトリックス

- 最近の業界全体の戦略的展開

- パートナーシップ、コラボレーション、契約

- 製品上市と製品拡張

- 買収と合併

- 主要成功戦略

- 主要なリーディング戦略:割合の分布(2018-2022年)

第4章 半導体製造装置の世界市場:ディメンション別

- 3-Dimensionの世界市場:地域別

- 2.5-Dimensionの世界地域別市場

- 2-Dimensionの世界市場:地域別

第5章 半導体製造装置の世界市場:サプライチェーンプロセス別

- IDMの世界市場:地域別

- OSATの世界市場:地域別

- その他の地域別世界市場

第6章 半導体製造装置の世界市場:製品タイプ別

- 前工程装置の世界市場:地域別

- 後工程装置の世界市場:地域別

第7章 半導体製造装置の世界市場機能別

- 集積回路の世界市場:地域別

- OSDの世界市場:地域別

第8章 半導体製造装置の世界市場:地域別

- 北米

- 北米の半導体製造装置の国別市場

- 米国

- カナダ

- メキシコ

- その他北米地域

- 北米の半導体製造装置の国別市場

- 欧州

- 欧州半導体製造装置市場:国別

- ドイツ

- 英国

- フランス

- ロシア

- スペイン

- イタリア

- その他欧州

- 欧州半導体製造装置市場:国別

- アジア太平洋地域

- アジア太平洋地域の半導体製造装置市場:国別一覧

- 中国

- 日本

- インド

- 韓国

- シンガポール

- マレーシア

- その他アジア太平洋地域

- アジア太平洋地域の半導体製造装置市場:国別一覧

- LAMEA

- LAMEA半導体製造装置市場:国別

- ブラジル

- アルゼンチン

- UAE

- サウジアラビア

- 南アフリカ共和国

- ナイジェリア

- LAMEAの他の地域

- LAMEA半導体製造装置市場:国別

第9章 企業プロファイル

- KLA Corporation

- Teradyne, Inc.

- ASML Holding N.V

- Applied Materials, Inc.

- SCREEN Holdings Co., Ltd

- Veeco Instruments, Inc.

- Nikon Corporation

- Carl Zeiss AG

- Lam Research Corporation

- Alsil Material

LIST OF TABLES

- TABLE 1 Global Semiconductor Production Equipment Market, 2018 - 2021, USD Million

- TABLE 2 Global Semiconductor Production Equipment Market, 2022 - 2028, USD Million

- TABLE 3 Partnerships, Collaborations and Agreements- Semiconductor Production Equipment Market

- TABLE 4 Product Launches And Product Expansions- Semiconductor Production Equipment Market

- TABLE 5 Acquisition and Mergers- Semiconductor Production Equipment Market

- TABLE 6 Global Semiconductor Production Equipment Market by Dimension, 2018 - 2021, USD Million

- TABLE 7 Global Semiconductor Production Equipment Market by Dimension, 2022 - 2028, USD Million

- TABLE 8 Global 3-Dimension Market by Region, 2018 - 2021, USD Million

- TABLE 9 Global 3-Dimension Market by Region, 2022 - 2028, USD Million

- TABLE 10 Global 2.5-Dimension Market by Region, 2018 - 2021, USD Million

- TABLE 11 Global 2.5-Dimension Market by Region, 2022 - 2028, USD Million

- TABLE 12 Global 2-Dimension Market by Region, 2018 - 2021, USD Million

- TABLE 13 Global 2-Dimension Market by Region, 2022 - 2028, USD Million

- TABLE 14 Global Semiconductor Production Equipment Market by Supply Chain Process, 2018 - 2021, USD Million

- TABLE 15 Global Semiconductor Production Equipment Market by Supply Chain Process, 2022 - 2028, USD Million

- TABLE 16 Global IDM Market by Region, 2018 - 2021, USD Million

- TABLE 17 Global IDM Market by Region, 2022 - 2028, USD Million

- TABLE 18 Global OSAT Market by Region, 2018 - 2021, USD Million

- TABLE 19 Global OSAT Market by Region, 2022 - 2028, USD Million

- TABLE 20 Global Others Market by Region, 2018 - 2021, USD Million

- TABLE 21 Global Others Market by Region, 2022 - 2028, USD Million

- TABLE 22 Global Semiconductor Production Equipment Market by Product Type, 2018 - 2021, USD Million

- TABLE 23 Global Semiconductor Production Equipment Market by Product Type, 2022 - 2028, USD Million

- TABLE 24 Global Front-end Equipment Market by Region, 2018 - 2021, USD Million

- TABLE 25 Global Front-end Equipment Market by Region, 2022 - 2028, USD Million

- TABLE 26 Global Back-end Equipment Market by Region, 2018 - 2021, USD Million

- TABLE 27 Global Back-end Equipment Market by Region, 2022 - 2028, USD Million

- TABLE 28 Global Semiconductor Production Equipment Market by Function, 2018 - 2021, USD Million

- TABLE 29 Global Semiconductor Production Equipment Market by Function, 2022 - 2028, USD Million

- TABLE 30 Global Integrated Circuits Market by Region, 2018 - 2021, USD Million

- TABLE 31 Global Integrated Circuits Market by Region, 2022 - 2028, USD Million

- TABLE 32 Global OSD Market by Region, 2018 - 2021, USD Million

- TABLE 33 Global OSD Market by Region, 2022 - 2028, USD Million

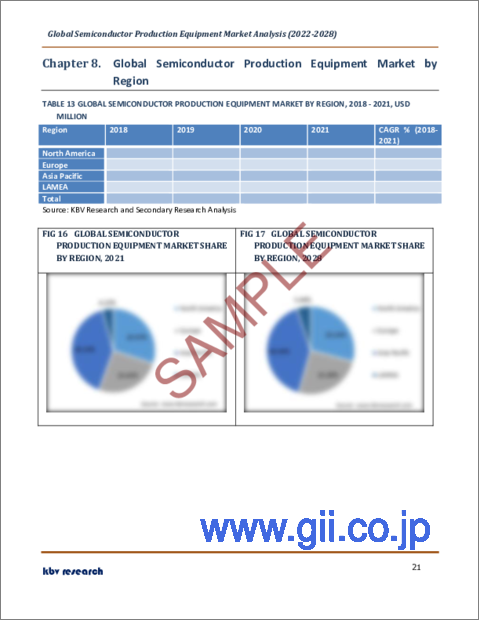

- TABLE 34 Global Semiconductor Production Equipment Market by Region, 2018 - 2021, USD Million

- TABLE 35 Global Semiconductor Production Equipment Market by Region, 2022 - 2028, USD Million

- TABLE 36 North America Semiconductor Production Equipment Market, 2018 - 2021, USD Million

- TABLE 37 North America Semiconductor Production Equipment Market, 2022 - 2028, USD Million

- TABLE 38 North America Semiconductor Production Equipment Market by Dimension, 2018 - 2021, USD Million

- TABLE 39 North America Semiconductor Production Equipment Market by Dimension, 2022 - 2028, USD Million

- TABLE 40 North America 3-Dimension Market by Country, 2018 - 2021, USD Million

- TABLE 41 North America 3-Dimension Market by Country, 2022 - 2028, USD Million

- TABLE 42 North America 2.5-Dimension Market by Country, 2018 - 2021, USD Million

- TABLE 43 North America 2.5-Dimension Market by Country, 2022 - 2028, USD Million

- TABLE 44 North America 2-Dimension Market by Country, 2018 - 2021, USD Million

- TABLE 45 North America 2-Dimension Market by Country, 2022 - 2028, USD Million

- TABLE 46 North America Semiconductor Production Equipment Market by Supply Chain Process, 2018 - 2021, USD Million

- TABLE 47 North America Semiconductor Production Equipment Market by Supply Chain Process, 2022 - 2028, USD Million

- TABLE 48 North America IDM Market by Country, 2018 - 2021, USD Million

- TABLE 49 North America IDM Market by Country, 2022 - 2028, USD Million

- TABLE 50 North America OSAT Market by Country, 2018 - 2021, USD Million

- TABLE 51 North America OSAT Market by Country, 2022 - 2028, USD Million

- TABLE 52 North America Others Market by Country, 2018 - 2021, USD Million

- TABLE 53 North America Others Market by Country, 2022 - 2028, USD Million

- TABLE 54 North America Semiconductor Production Equipment Market by Product Type, 2018 - 2021, USD Million

- TABLE 55 North America Semiconductor Production Equipment Market by Product Type, 2022 - 2028, USD Million

- TABLE 56 North America Front-end Equipment Market by Country, 2018 - 2021, USD Million

- TABLE 57 North America Front-end Equipment Market by Country, 2022 - 2028, USD Million

- TABLE 58 North America Back-end Equipment Market by Country, 2018 - 2021, USD Million

- TABLE 59 North America Back-end Equipment Market by Country, 2022 - 2028, USD Million

- TABLE 60 North America Semiconductor Production Equipment Market by Function, 2018 - 2021, USD Million

- TABLE 61 North America Semiconductor Production Equipment Market by Function, 2022 - 2028, USD Million

- TABLE 62 North America Integrated Circuits Market by Country, 2018 - 2021, USD Million

- TABLE 63 North America Integrated Circuits Market by Country, 2022 - 2028, USD Million

- TABLE 64 North America OSD Market by Country, 2018 - 2021, USD Million

- TABLE 65 North America OSD Market by Country, 2022 - 2028, USD Million

- TABLE 66 North America Semiconductor Production Equipment Market by Country, 2018 - 2021, USD Million

- TABLE 67 North America Semiconductor Production Equipment Market by Country, 2022 - 2028, USD Million

- TABLE 68 US Semiconductor Production Equipment Market, 2018 - 2021, USD Million

- TABLE 69 US Semiconductor Production Equipment Market, 2022 - 2028, USD Million

- TABLE 70 US Semiconductor Production Equipment Market by Dimension, 2018 - 2021, USD Million

- TABLE 71 US Semiconductor Production Equipment Market by Dimension, 2022 - 2028, USD Million

- TABLE 72 US Semiconductor Production Equipment Market by Supply Chain Process, 2018 - 2021, USD Million

- TABLE 73 US Semiconductor Production Equipment Market by Supply Chain Process, 2022 - 2028, USD Million

- TABLE 74 US Semiconductor Production Equipment Market by Product Type, 2018 - 2021, USD Million

- TABLE 75 US Semiconductor Production Equipment Market by Product Type, 2022 - 2028, USD Million

- TABLE 76 US Semiconductor Production Equipment Market by Function, 2018 - 2021, USD Million

- TABLE 77 US Semiconductor Production Equipment Market by Function, 2022 - 2028, USD Million

- TABLE 78 Canada Semiconductor Production Equipment Market, 2018 - 2021, USD Million

- TABLE 79 Canada Semiconductor Production Equipment Market, 2022 - 2028, USD Million

- TABLE 80 Canada Semiconductor Production Equipment Market by Dimension, 2018 - 2021, USD Million

- TABLE 81 Canada Semiconductor Production Equipment Market by Dimension, 2022 - 2028, USD Million

- TABLE 82 Canada Semiconductor Production Equipment Market by Supply Chain Process, 2018 - 2021, USD Million

- TABLE 83 Canada Semiconductor Production Equipment Market by Supply Chain Process, 2022 - 2028, USD Million

- TABLE 84 Canada Semiconductor Production Equipment Market by Product Type, 2018 - 2021, USD Million

- TABLE 85 Canada Semiconductor Production Equipment Market by Product Type, 2022 - 2028, USD Million

- TABLE 86 Canada Semiconductor Production Equipment Market by Function, 2018 - 2021, USD Million

- TABLE 87 Canada Semiconductor Production Equipment Market by Function, 2022 - 2028, USD Million

- TABLE 88 Mexico Semiconductor Production Equipment Market, 2018 - 2021, USD Million

- TABLE 89 Mexico Semiconductor Production Equipment Market, 2022 - 2028, USD Million

- TABLE 90 Mexico Semiconductor Production Equipment Market by Dimension, 2018 - 2021, USD Million

- TABLE 91 Mexico Semiconductor Production Equipment Market by Dimension, 2022 - 2028, USD Million

- TABLE 92 Mexico Semiconductor Production Equipment Market by Supply Chain Process, 2018 - 2021, USD Million

- TABLE 93 Mexico Semiconductor Production Equipment Market by Supply Chain Process, 2022 - 2028, USD Million

- TABLE 94 Mexico Semiconductor Production Equipment Market by Product Type, 2018 - 2021, USD Million

- TABLE 95 Mexico Semiconductor Production Equipment Market by Product Type, 2022 - 2028, USD Million

- TABLE 96 Mexico Semiconductor Production Equipment Market by Function, 2018 - 2021, USD Million

- TABLE 97 Mexico Semiconductor Production Equipment Market by Function, 2022 - 2028, USD Million

- TABLE 98 Rest of North America Semiconductor Production Equipment Market, 2018 - 2021, USD Million

- TABLE 99 Rest of North America Semiconductor Production Equipment Market, 2022 - 2028, USD Million

- TABLE 100 Rest of North America Semiconductor Production Equipment Market by Dimension, 2018 - 2021, USD Million

- TABLE 101 Rest of North America Semiconductor Production Equipment Market by Dimension, 2022 - 2028, USD Million

- TABLE 102 Rest of North America Semiconductor Production Equipment Market by Supply Chain Process, 2018 - 2021, USD Million

- TABLE 103 Rest of North America Semiconductor Production Equipment Market by Supply Chain Process, 2022 - 2028, USD Million

- TABLE 104 Rest of North America Semiconductor Production Equipment Market by Product Type, 2018 - 2021, USD Million

- TABLE 105 Rest of North America Semiconductor Production Equipment Market by Product Type, 2022 - 2028, USD Million

- TABLE 106 Rest of North America Semiconductor Production Equipment Market by Function, 2018 - 2021, USD Million

- TABLE 107 Rest of North America Semiconductor Production Equipment Market by Function, 2022 - 2028, USD Million

- TABLE 108 Europe Semiconductor Production Equipment Market, 2018 - 2021, USD Million

- TABLE 109 Europe Semiconductor Production Equipment Market, 2022 - 2028, USD Million

- TABLE 110 Europe Semiconductor Production Equipment Market by Dimension, 2018 - 2021, USD Million

- TABLE 111 Europe Semiconductor Production Equipment Market by Dimension, 2022 - 2028, USD Million

- TABLE 112 Europe 3-Dimension Market by Country, 2018 - 2021, USD Million

- TABLE 113 Europe 3-Dimension Market by Country, 2022 - 2028, USD Million

- TABLE 114 Europe 2.5-Dimension Market by Country, 2018 - 2021, USD Million

- TABLE 115 Europe 2.5-Dimension Market by Country, 2022 - 2028, USD Million

- TABLE 116 Europe 2-Dimension Market by Country, 2018 - 2021, USD Million

- TABLE 117 Europe 2-Dimension Market by Country, 2022 - 2028, USD Million

- TABLE 118 Europe Semiconductor Production Equipment Market by Supply Chain Process, 2018 - 2021, USD Million

- TABLE 119 Europe Semiconductor Production Equipment Market by Supply Chain Process, 2022 - 2028, USD Million

- TABLE 120 Europe IDM Market by Country, 2018 - 2021, USD Million

- TABLE 121 Europe IDM Market by Country, 2022 - 2028, USD Million

- TABLE 122 Europe OSAT Market by Country, 2018 - 2021, USD Million

- TABLE 123 Europe OSAT Market by Country, 2022 - 2028, USD Million

- TABLE 124 Europe Others Market by Country, 2018 - 2021, USD Million

- TABLE 125 Europe Others Market by Country, 2022 - 2028, USD Million

- TABLE 126 Europe Semiconductor Production Equipment Market by Product Type, 2018 - 2021, USD Million

- TABLE 127 Europe Semiconductor Production Equipment Market by Product Type, 2022 - 2028, USD Million

- TABLE 128 Europe Front-end Equipment Market by Country, 2018 - 2021, USD Million

- TABLE 129 Europe Front-end Equipment Market by Country, 2022 - 2028, USD Million

- TABLE 130 Europe Back-end Equipment Market by Country, 2018 - 2021, USD Million

- TABLE 131 Europe Back-end Equipment Market by Country, 2022 - 2028, USD Million

- TABLE 132 Europe Semiconductor Production Equipment Market by Function, 2018 - 2021, USD Million

- TABLE 133 Europe Semiconductor Production Equipment Market by Function, 2022 - 2028, USD Million

- TABLE 134 Europe Integrated Circuits Market by Country, 2018 - 2021, USD Million

- TABLE 135 Europe Integrated Circuits Market by Country, 2022 - 2028, USD Million

- TABLE 136 Europe OSD Market by Country, 2018 - 2021, USD Million

- TABLE 137 Europe OSD Market by Country, 2022 - 2028, USD Million

- TABLE 138 Europe Semiconductor Production Equipment Market by Country, 2018 - 2021, USD Million

- TABLE 139 Europe Semiconductor Production Equipment Market by Country, 2022 - 2028, USD Million

- TABLE 140 Germany Semiconductor Production Equipment Market, 2018 - 2021, USD Million

- TABLE 141 Germany Semiconductor Production Equipment Market, 2022 - 2028, USD Million

- TABLE 142 Germany Semiconductor Production Equipment Market by Dimension, 2018 - 2021, USD Million

- TABLE 143 Germany Semiconductor Production Equipment Market by Dimension, 2022 - 2028, USD Million

- TABLE 144 Germany Semiconductor Production Equipment Market by Supply Chain Process, 2018 - 2021, USD Million

- TABLE 145 Germany Semiconductor Production Equipment Market by Supply Chain Process, 2022 - 2028, USD Million

- TABLE 146 Germany Semiconductor Production Equipment Market by Product Type, 2018 - 2021, USD Million

- TABLE 147 Germany Semiconductor Production Equipment Market by Product Type, 2022 - 2028, USD Million

- TABLE 148 Germany Semiconductor Production Equipment Market by Function, 2018 - 2021, USD Million

- TABLE 149 Germany Semiconductor Production Equipment Market by Function, 2022 - 2028, USD Million

- TABLE 150 UK Semiconductor Production Equipment Market, 2018 - 2021, USD Million

- TABLE 151 UK Semiconductor Production Equipment Market, 2022 - 2028, USD Million

- TABLE 152 UK Semiconductor Production Equipment Market by Dimension, 2018 - 2021, USD Million

- TABLE 153 UK Semiconductor Production Equipment Market by Dimension, 2022 - 2028, USD Million

- TABLE 154 UK Semiconductor Production Equipment Market by Supply Chain Process, 2018 - 2021, USD Million

- TABLE 155 UK Semiconductor Production Equipment Market by Supply Chain Process, 2022 - 2028, USD Million

- TABLE 156 UK Semiconductor Production Equipment Market by Product Type, 2018 - 2021, USD Million

- TABLE 157 UK Semiconductor Production Equipment Market by Product Type, 2022 - 2028, USD Million

- TABLE 158 UK Semiconductor Production Equipment Market by Function, 2018 - 2021, USD Million

- TABLE 159 UK Semiconductor Production Equipment Market by Function, 2022 - 2028, USD Million

- TABLE 160 France Semiconductor Production Equipment Market, 2018 - 2021, USD Million

- TABLE 161 France Semiconductor Production Equipment Market, 2022 - 2028, USD Million

- TABLE 162 France Semiconductor Production Equipment Market by Dimension, 2018 - 2021, USD Million

- TABLE 163 France Semiconductor Production Equipment Market by Dimension, 2022 - 2028, USD Million

- TABLE 164 France Semiconductor Production Equipment Market by Supply Chain Process, 2018 - 2021, USD Million

- TABLE 165 France Semiconductor Production Equipment Market by Supply Chain Process, 2022 - 2028, USD Million

- TABLE 166 France Semiconductor Production Equipment Market by Product Type, 2018 - 2021, USD Million

- TABLE 167 France Semiconductor Production Equipment Market by Product Type, 2022 - 2028, USD Million

- TABLE 168 France Semiconductor Production Equipment Market by Function, 2018 - 2021, USD Million

- TABLE 169 France Semiconductor Production Equipment Market by Function, 2022 - 2028, USD Million

- TABLE 170 Russia Semiconductor Production Equipment Market, 2018 - 2021, USD Million

- TABLE 171 Russia Semiconductor Production Equipment Market, 2022 - 2028, USD Million

- TABLE 172 Russia Semiconductor Production Equipment Market by Dimension, 2018 - 2021, USD Million

- TABLE 173 Russia Semiconductor Production Equipment Market by Dimension, 2022 - 2028, USD Million

- TABLE 174 Russia Semiconductor Production Equipment Market by Supply Chain Process, 2018 - 2021, USD Million

- TABLE 175 Russia Semiconductor Production Equipment Market by Supply Chain Process, 2022 - 2028, USD Million

- TABLE 176 Russia Semiconductor Production Equipment Market by Product Type, 2018 - 2021, USD Million

- TABLE 177 Russia Semiconductor Production Equipment Market by Product Type, 2022 - 2028, USD Million

- TABLE 178 Russia Semiconductor Production Equipment Market by Function, 2018 - 2021, USD Million

- TABLE 179 Russia Semiconductor Production Equipment Market by Function, 2022 - 2028, USD Million

- TABLE 180 Spain Semiconductor Production Equipment Market, 2018 - 2021, USD Million

- TABLE 181 Spain Semiconductor Production Equipment Market, 2022 - 2028, USD Million

- TABLE 182 Spain Semiconductor Production Equipment Market by Dimension, 2018 - 2021, USD Million

- TABLE 183 Spain Semiconductor Production Equipment Market by Dimension, 2022 - 2028, USD Million

- TABLE 184 Spain Semiconductor Production Equipment Market by Supply Chain Process, 2018 - 2021, USD Million

- TABLE 185 Spain Semiconductor Production Equipment Market by Supply Chain Process, 2022 - 2028, USD Million

- TABLE 186 Spain Semiconductor Production Equipment Market by Product Type, 2018 - 2021, USD Million

- TABLE 187 Spain Semiconductor Production Equipment Market by Product Type, 2022 - 2028, USD Million

- TABLE 188 Spain Semiconductor Production Equipment Market by Function, 2018 - 2021, USD Million

- TABLE 189 Spain Semiconductor Production Equipment Market by Function, 2022 - 2028, USD Million

- TABLE 190 Italy Semiconductor Production Equipment Market, 2018 - 2021, USD Million

- TABLE 191 Italy Semiconductor Production Equipment Market, 2022 - 2028, USD Million

- TABLE 192 Italy Semiconductor Production Equipment Market by Dimension, 2018 - 2021, USD Million

- TABLE 193 Italy Semiconductor Production Equipment Market by Dimension, 2022 - 2028, USD Million

- TABLE 194 Italy Semiconductor Production Equipment Market by Supply Chain Process, 2018 - 2021, USD Million

- TABLE 195 Italy Semiconductor Production Equipment Market by Supply Chain Process, 2022 - 2028, USD Million

- TABLE 196 Italy Semiconductor Production Equipment Market by Product Type, 2018 - 2021, USD Million

- TABLE 197 Italy Semiconductor Production Equipment Market by Product Type, 2022 - 2028, USD Million

- TABLE 198 Italy Semiconductor Production Equipment Market by Function, 2018 - 2021, USD Million

- TABLE 199 Italy Semiconductor Production Equipment Market by Function, 2022 - 2028, USD Million

- TABLE 200 Rest of Europe Semiconductor Production Equipment Market, 2018 - 2021, USD Million

- TABLE 201 Rest of Europe Semiconductor Production Equipment Market, 2022 - 2028, USD Million

- TABLE 202 Rest of Europe Semiconductor Production Equipment Market by Dimension, 2018 - 2021, USD Million

- TABLE 203 Rest of Europe Semiconductor Production Equipment Market by Dimension, 2022 - 2028, USD Million

- TABLE 204 Rest of Europe Semiconductor Production Equipment Market by Supply Chain Process, 2018 - 2021, USD Million

- TABLE 205 Rest of Europe Semiconductor Production Equipment Market by Supply Chain Process, 2022 - 2028, USD Million

- TABLE 206 Rest of Europe Semiconductor Production Equipment Market by Product Type, 2018 - 2021, USD Million

- TABLE 207 Rest of Europe Semiconductor Production Equipment Market by Product Type, 2022 - 2028, USD Million

- TABLE 208 Rest of Europe Semiconductor Production Equipment Market by Function, 2018 - 2021, USD Million

- TABLE 209 Rest of Europe Semiconductor Production Equipment Market by Function, 2022 - 2028, USD Million

- TABLE 210 Asia Pacific Semiconductor Production Equipment Market, 2018 - 2021, USD Million

- TABLE 211 Asia Pacific Semiconductor Production Equipment Market, 2022 - 2028, USD Million

- TABLE 212 Asia Pacific Semiconductor Production Equipment Market by Dimension, 2018 - 2021, USD Million

- TABLE 213 Asia Pacific Semiconductor Production Equipment Market by Dimension, 2022 - 2028, USD Million

- TABLE 214 Asia Pacific 3-Dimension Market by Country, 2018 - 2021, USD Million

- TABLE 215 Asia Pacific 3-Dimension Market by Country, 2022 - 2028, USD Million

- TABLE 216 Asia Pacific 2.5-Dimension Market by Country, 2018 - 2021, USD Million

- TABLE 217 Asia Pacific 2.5-Dimension Market by Country, 2022 - 2028, USD Million

- TABLE 218 Asia Pacific 2-Dimension Market by Country, 2018 - 2021, USD Million

- TABLE 219 Asia Pacific 2-Dimension Market by Country, 2022 - 2028, USD Million

- TABLE 220 Asia Pacific Semiconductor Production Equipment Market by Supply Chain Process, 2018 - 2021, USD Million

- TABLE 221 Asia Pacific Semiconductor Production Equipment Market by Supply Chain Process, 2022 - 2028, USD Million

- TABLE 222 Asia Pacific IDM Market by Country, 2018 - 2021, USD Million

- TABLE 223 Asia Pacific IDM Market by Country, 2022 - 2028, USD Million

- TABLE 224 Asia Pacific OSAT Market by Country, 2018 - 2021, USD Million

- TABLE 225 Asia Pacific OSAT Market by Country, 2022 - 2028, USD Million

- TABLE 226 Asia Pacific Others Market by Country, 2018 - 2021, USD Million

- TABLE 227 Asia Pacific Others Market by Country, 2022 - 2028, USD Million

- TABLE 228 Asia Pacific Semiconductor Production Equipment Market by Product Type, 2018 - 2021, USD Million

- TABLE 229 Asia Pacific Semiconductor Production Equipment Market by Product Type, 2022 - 2028, USD Million

- TABLE 230 Asia Pacific Front-end Equipment Market by Country, 2018 - 2021, USD Million

- TABLE 231 Asia Pacific Front-end Equipment Market by Country, 2022 - 2028, USD Million

- TABLE 232 Asia Pacific Back-end Equipment Market by Country, 2018 - 2021, USD Million

- TABLE 233 Asia Pacific Back-end Equipment Market by Country, 2022 - 2028, USD Million

- TABLE 234 Asia Pacific Semiconductor Production Equipment Market by Function, 2018 - 2021, USD Million

- TABLE 235 Asia Pacific Semiconductor Production Equipment Market by Function, 2022 - 2028, USD Million

- TABLE 236 Asia Pacific Integrated Circuits Market by Country, 2018 - 2021, USD Million

- TABLE 237 Asia Pacific Integrated Circuits Market by Country, 2022 - 2028, USD Million

- TABLE 238 Asia Pacific OSD Market by Country, 2018 - 2021, USD Million

- TABLE 239 Asia Pacific OSD Market by Country, 2022 - 2028, USD Million

- TABLE 240 Asia Pacific Semiconductor Production Equipment Market by Country, 2018 - 2021, USD Million

- TABLE 241 Asia Pacific Semiconductor Production Equipment Market by Country, 2022 - 2028, USD Million

- TABLE 242 China Semiconductor Production Equipment Market, 2018 - 2021, USD Million

- TABLE 243 China Semiconductor Production Equipment Market, 2022 - 2028, USD Million

- TABLE 244 China Semiconductor Production Equipment Market by Dimension, 2018 - 2021, USD Million

- TABLE 245 China Semiconductor Production Equipment Market by Dimension, 2022 - 2028, USD Million

- TABLE 246 China Semiconductor Production Equipment Market by Supply Chain Process, 2018 - 2021, USD Million

- TABLE 247 China Semiconductor Production Equipment Market by Supply Chain Process, 2022 - 2028, USD Million

- TABLE 248 China Semiconductor Production Equipment Market by Product Type, 2018 - 2021, USD Million

- TABLE 249 China Semiconductor Production Equipment Market by Product Type, 2022 - 2028, USD Million

- TABLE 250 China Semiconductor Production Equipment Market by Function, 2018 - 2021, USD Million

- TABLE 251 China Semiconductor Production Equipment Market by Function, 2022 - 2028, USD Million

- TABLE 252 Japan Semiconductor Production Equipment Market, 2018 - 2021, USD Million

- TABLE 253 Japan Semiconductor Production Equipment Market, 2022 - 2028, USD Million

- TABLE 254 Japan Semiconductor Production Equipment Market by Dimension, 2018 - 2021, USD Million

- TABLE 255 Japan Semiconductor Production Equipment Market by Dimension, 2022 - 2028, USD Million

- TABLE 256 Japan Semiconductor Production Equipment Market by Supply Chain Process, 2018 - 2021, USD Million

- TABLE 257 Japan Semiconductor Production Equipment Market by Supply Chain Process, 2022 - 2028, USD Million

- TABLE 258 Japan Semiconductor Production Equipment Market by Product Type, 2018 - 2021, USD Million

- TABLE 259 Japan Semiconductor Production Equipment Market by Product Type, 2022 - 2028, USD Million

- TABLE 260 Japan Semiconductor Production Equipment Market by Function, 2018 - 2021, USD Million

- TABLE 261 Japan Semiconductor Production Equipment Market by Function, 2022 - 2028, USD Million

- TABLE 262 India Semiconductor Production Equipment Market, 2018 - 2021, USD Million

- TABLE 263 India Semiconductor Production Equipment Market, 2022 - 2028, USD Million

- TABLE 264 India Semiconductor Production Equipment Market by Dimension, 2018 - 2021, USD Million

- TABLE 265 India Semiconductor Production Equipment Market by Dimension, 2022 - 2028, USD Million

- TABLE 266 India Semiconductor Production Equipment Market by Supply Chain Process, 2018 - 2021, USD Million

- TABLE 267 India Semiconductor Production Equipment Market by Supply Chain Process, 2022 - 2028, USD Million

- TABLE 268 India Semiconductor Production Equipment Market by Product Type, 2018 - 2021, USD Million

- TABLE 269 India Semiconductor Production Equipment Market by Product Type, 2022 - 2028, USD Million

- TABLE 270 India Semiconductor Production Equipment Market by Function, 2018 - 2021, USD Million

- TABLE 271 India Semiconductor Production Equipment Market by Function, 2022 - 2028, USD Million

- TABLE 272 South Korea Semiconductor Production Equipment Market, 2018 - 2021, USD Million

- TABLE 273 South Korea Semiconductor Production Equipment Market, 2022 - 2028, USD Million

- TABLE 274 South Korea Semiconductor Production Equipment Market by Dimension, 2018 - 2021, USD Million

- TABLE 275 South Korea Semiconductor Production Equipment Market by Dimension, 2022 - 2028, USD Million

- TABLE 276 South Korea Semiconductor Production Equipment Market by Supply Chain Process, 2018 - 2021, USD Million

- TABLE 277 South Korea Semiconductor Production Equipment Market by Supply Chain Process, 2022 - 2028, USD Million

- TABLE 278 South Korea Semiconductor Production Equipment Market by Product Type, 2018 - 2021, USD Million

- TABLE 279 South Korea Semiconductor Production Equipment Market by Product Type, 2022 - 2028, USD Million

- TABLE 280 South Korea Semiconductor Production Equipment Market by Function, 2018 - 2021, USD Million

- TABLE 281 South Korea Semiconductor Production Equipment Market by Function, 2022 - 2028, USD Million

- TABLE 282 Singapore Semiconductor Production Equipment Market, 2018 - 2021, USD Million

- TABLE 283 Singapore Semiconductor Production Equipment Market, 2022 - 2028, USD Million

- TABLE 284 Singapore Semiconductor Production Equipment Market by Dimension, 2018 - 2021, USD Million

- TABLE 285 Singapore Semiconductor Production Equipment Market by Dimension, 2022 - 2028, USD Million

- TABLE 286 Singapore Semiconductor Production Equipment Market by Supply Chain Process, 2018 - 2021, USD Million

- TABLE 287 Singapore Semiconductor Production Equipment Market by Supply Chain Process, 2022 - 2028, USD Million

- TABLE 288 Singapore Semiconductor Production Equipment Market by Product Type, 2018 - 2021, USD Million

- TABLE 289 Singapore Semiconductor Production Equipment Market by Product Type, 2022 - 2028, USD Million

- TABLE 290 Singapore Semiconductor Production Equipment Market by Function, 2018 - 2021, USD Million

- TABLE 291 Singapore Semiconductor Production Equipment Market by Function, 2022 - 2028, USD Million

- TABLE 292 Malaysia Semiconductor Production Equipment Market, 2018 - 2021, USD Million

- TABLE 293 Malaysia Semiconductor Production Equipment Market, 2022 - 2028, USD Million

- TABLE 294 Malaysia Semiconductor Production Equipment Market by Dimension, 2018 - 2021, USD Million

- TABLE 295 Malaysia Semiconductor Production Equipment Market by Dimension, 2022 - 2028, USD Million

- TABLE 296 Malaysia Semiconductor Production Equipment Market by Supply Chain Process, 2018 - 2021, USD Million

- TABLE 297 Malaysia Semiconductor Production Equipment Market by Supply Chain Process, 2022 - 2028, USD Million

- TABLE 298 Malaysia Semiconductor Production Equipment Market by Product Type, 2018 - 2021, USD Million

- TABLE 299 Malaysia Semiconductor Production Equipment Market by Product Type, 2022 - 2028, USD Million

- TABLE 300 Malaysia Semiconductor Production Equipment Market by Function, 2018 - 2021, USD Million

- TABLE 301 Malaysia Semiconductor Production Equipment Market by Function, 2022 - 2028, USD Million

- TABLE 302 Rest of Asia Pacific Semiconductor Production Equipment Market, 2018 - 2021, USD Million

- TABLE 303 Rest of Asia Pacific Semiconductor Production Equipment Market, 2022 - 2028, USD Million

- TABLE 304 Rest of Asia Pacific Semiconductor Production Equipment Market by Dimension, 2018 - 2021, USD Million

- TABLE 305 Rest of Asia Pacific Semiconductor Production Equipment Market by Dimension, 2022 - 2028, USD Million

- TABLE 306 Rest of Asia Pacific Semiconductor Production Equipment Market by Supply Chain Process, 2018 - 2021, USD Million

- TABLE 307 Rest of Asia Pacific Semiconductor Production Equipment Market by Supply Chain Process, 2022 - 2028, USD Million

- TABLE 308 Rest of Asia Pacific Semiconductor Production Equipment Market by Product Type, 2018 - 2021, USD Million

- TABLE 309 Rest of Asia Pacific Semiconductor Production Equipment Market by Product Type, 2022 - 2028, USD Million

- TABLE 310 Rest of Asia Pacific Semiconductor Production Equipment Market by Function, 2018 - 2021, USD Million

- TABLE 311 Rest of Asia Pacific Semiconductor Production Equipment Market by Function, 2022 - 2028, USD Million

- TABLE 312 LAMEA Semiconductor Production Equipment Market, 2018 - 2021, USD Million

- TABLE 313 LAMEA Semiconductor Production Equipment Market, 2022 - 2028, USD Million

- TABLE 314 LAMEA Semiconductor Production Equipment Market by Dimension, 2018 - 2021, USD Million

- TABLE 315 LAMEA Semiconductor Production Equipment Market by Dimension, 2022 - 2028, USD Million

- TABLE 316 LAMEA 3-Dimension Market by Country, 2018 - 2021, USD Million

- TABLE 317 LAMEA 3-Dimension Market by Country, 2022 - 2028, USD Million

- TABLE 318 LAMEA 2.5-Dimension Market by Country, 2018 - 2021, USD Million

- TABLE 319 LAMEA 2.5-Dimension Market by Country, 2022 - 2028, USD Million

- TABLE 320 LAMEA 2-Dimension Market by Country, 2018 - 2021, USD Million

- TABLE 321 LAMEA 2-Dimension Market by Country, 2022 - 2028, USD Million

- TABLE 322 LAMEA Semiconductor Production Equipment Market by Supply Chain Process, 2018 - 2021, USD Million

- TABLE 323 LAMEA Semiconductor Production Equipment Market by Supply Chain Process, 2022 - 2028, USD Million

- TABLE 324 LAMEA IDM Market by Country, 2018 - 2021, USD Million

- TABLE 325 LAMEA IDM Market by Country, 2022 - 2028, USD Million

- TABLE 326 LAMEA OSAT Market by Country, 2018 - 2021, USD Million

- TABLE 327 LAMEA OSAT Market by Country, 2022 - 2028, USD Million

- TABLE 328 LAMEA Others Market by Country, 2018 - 2021, USD Million

- TABLE 329 LAMEA Others Market by Country, 2022 - 2028, USD Million

- TABLE 330 LAMEA Semiconductor Production Equipment Market by Product Type, 2018 - 2021, USD Million

- TABLE 331 LAMEA Semiconductor Production Equipment Market by Product Type, 2022 - 2028, USD Million

- TABLE 332 LAMEA Front-end Equipment Market by Country, 2018 - 2021, USD Million

- TABLE 333 LAMEA Front-end Equipment Market by Country, 2022 - 2028, USD Million

- TABLE 334 LAMEA Back-end Equipment Market by Country, 2018 - 2021, USD Million

- TABLE 335 LAMEA Back-end Equipment Market by Country, 2022 - 2028, USD Million

- TABLE 336 LAMEA Semiconductor Production Equipment Market by Function, 2018 - 2021, USD Million

- TABLE 337 LAMEA Semiconductor Production Equipment Market by Function, 2022 - 2028, USD Million

- TABLE 338 LAMEA Integrated Circuits Market by Country, 2018 - 2021, USD Million

- TABLE 339 LAMEA Integrated Circuits Market by Country, 2022 - 2028, USD Million

- TABLE 340 LAMEA OSD Market by Country, 2018 - 2021, USD Million

- TABLE 341 LAMEA OSD Market by Country, 2022 - 2028, USD Million

- TABLE 342 LAMEA Semiconductor Production Equipment Market by Country, 2018 - 2021, USD Million

- TABLE 343 LAMEA Semiconductor Production Equipment Market by Country, 2022 - 2028, USD Million

- TABLE 344 Brazil Semiconductor Production Equipment Market, 2018 - 2021, USD Million

- TABLE 345 Brazil Semiconductor Production Equipment Market, 2022 - 2028, USD Million

- TABLE 346 Brazil Semiconductor Production Equipment Market by Dimension, 2018 - 2021, USD Million

- TABLE 347 Brazil Semiconductor Production Equipment Market by Dimension, 2022 - 2028, USD Million

- TABLE 348 Brazil Semiconductor Production Equipment Market by Supply Chain Process, 2018 - 2021, USD Million

- TABLE 349 Brazil Semiconductor Production Equipment Market by Supply Chain Process, 2022 - 2028, USD Million

- TABLE 350 Brazil Semiconductor Production Equipment Market by Product Type, 2018 - 2021, USD Million

- TABLE 351 Brazil Semiconductor Production Equipment Market by Product Type, 2022 - 2028, USD Million

- TABLE 352 Brazil Semiconductor Production Equipment Market by Function, 2018 - 2021, USD Million

- TABLE 353 Brazil Semiconductor Production Equipment Market by Function, 2022 - 2028, USD Million

- TABLE 354 Argentina Semiconductor Production Equipment Market, 2018 - 2021, USD Million

- TABLE 355 Argentina Semiconductor Production Equipment Market, 2022 - 2028, USD Million

- TABLE 356 Argentina Semiconductor Production Equipment Market by Dimension, 2018 - 2021, USD Million

- TABLE 357 Argentina Semiconductor Production Equipment Market by Dimension, 2022 - 2028, USD Million

- TABLE 358 Argentina Semiconductor Production Equipment Market by Supply Chain Process, 2018 - 2021, USD Million

- TABLE 359 Argentina Semiconductor Production Equipment Market by Supply Chain Process, 2022 - 2028, USD Million

- TABLE 360 Argentina Semiconductor Production Equipment Market by Product Type, 2018 - 2021, USD Million

- TABLE 361 Argentina Semiconductor Production Equipment Market by Product Type, 2022 - 2028, USD Million

- TABLE 362 Argentina Semiconductor Production Equipment Market by Function, 2018 - 2021, USD Million

- TABLE 363 Argentina Semiconductor Production Equipment Market by Function, 2022 - 2028, USD Million

- TABLE 364 UAE Semiconductor Production Equipment Market, 2018 - 2021, USD Million

- TABLE 365 UAE Semiconductor Production Equipment Market, 2022 - 2028, USD Million

- TABLE 366 UAE Semiconductor Production Equipment Market by Dimension, 2018 - 2021, USD Million

- TABLE 367 UAE Semiconductor Production Equipment Market by Dimension, 2022 - 2028, USD Million

- TABLE 368 UAE Semiconductor Production Equipment Market by Supply Chain Process, 2018 - 2021, USD Million

- TABLE 369 UAE Semiconductor Production Equipment Market by Supply Chain Process, 2022 - 2028, USD Million

- TABLE 370 UAE Semiconductor Production Equipment Market by Product Type, 2018 - 2021, USD Million

- TABLE 371 UAE Semiconductor Production Equipment Market by Product Type, 2022 - 2028, USD Million

- TABLE 372 UAE Semiconductor Production Equipment Market by Function, 2018 - 2021, USD Million

- TABLE 373 UAE Semiconductor Production Equipment Market by Function, 2022 - 2028, USD Million

- TABLE 374 Saudi Arabia Semiconductor Production Equipment Market, 2018 - 2021, USD Million

- TABLE 375 Saudi Arabia Semiconductor Production Equipment Market, 2022 - 2028, USD Million

- TABLE 376 Saudi Arabia Semiconductor Production Equipment Market by Dimension, 2018 - 2021, USD Million

- TABLE 377 Saudi Arabia Semiconductor Production Equipment Market by Dimension, 2022 - 2028, USD Million

- TABLE 378 Saudi Arabia Semiconductor Production Equipment Market by Supply Chain Process, 2018 - 2021, USD Million

- TABLE 379 Saudi Arabia Semiconductor Production Equipment Market by Supply Chain Process, 2022 - 2028, USD Million

- TABLE 380 Saudi Arabia Semiconductor Production Equipment Market by Product Type, 2018 - 2021, USD Million

- TABLE 381 Saudi Arabia Semiconductor Production Equipment Market by Product Type, 2022 - 2028, USD Million

- TABLE 382 Saudi Arabia Semiconductor Production Equipment Market by Function, 2018 - 2021, USD Million

- TABLE 383 Saudi Arabia Semiconductor Production Equipment Market by Function, 2022 - 2028, USD Million

- TABLE 384 South Africa Semiconductor Production Equipment Market, 2018 - 2021, USD Million

- TABLE 385 South Africa Semiconductor Production Equipment Market, 2022 - 2028, USD Million

- TABLE 386 South Africa Semiconductor Production Equipment Market by Dimension, 2018 - 2021, USD Million

- TABLE 387 South Africa Semiconductor Production Equipment Market by Dimension, 2022 - 2028, USD Million

- TABLE 388 South Africa Semiconductor Production Equipment Market by Supply Chain Process, 2018 - 2021, USD Million

- TABLE 389 South Africa Semiconductor Production Equipment Market by Supply Chain Process, 2022 - 2028, USD Million

- TABLE 390 South Africa Semiconductor Production Equipment Market by Product Type, 2018 - 2021, USD Million

- TABLE 391 South Africa Semiconductor Production Equipment Market by Product Type, 2022 - 2028, USD Million

- TABLE 392 South Africa Semiconductor Production Equipment Market by Function, 2018 - 2021, USD Million

- TABLE 393 South Africa Semiconductor Production Equipment Market by Function, 2022 - 2028, USD Million

- TABLE 394 Nigeria Semiconductor Production Equipment Market, 2018 - 2021, USD Million

- TABLE 395 Nigeria Semiconductor Production Equipment Market, 2022 - 2028, USD Million

- TABLE 396 Nigeria Semiconductor Production Equipment Market by Dimension, 2018 - 2021, USD Million

- TABLE 397 Nigeria Semiconductor Production Equipment Market by Dimension, 2022 - 2028, USD Million

- TABLE 398 Nigeria Semiconductor Production Equipment Market by Supply Chain Process, 2018 - 2021, USD Million

- TABLE 399 Nigeria Semiconductor Production Equipment Market by Supply Chain Process, 2022 - 2028, USD Million

- TABLE 400 Nigeria Semiconductor Production Equipment Market by Product Type, 2018 - 2021, USD Million

- TABLE 401 Nigeria Semiconductor Production Equipment Market by Product Type, 2022 - 2028, USD Million

- TABLE 402 Nigeria Semiconductor Production Equipment Market by Function, 2018 - 2021, USD Million

- TABLE 403 Nigeria Semiconductor Production Equipment Market by Function, 2022 - 2028, USD Million

- TABLE 404 Rest of LAMEA Semiconductor Production Equipment Market, 2018 - 2021, USD Million

- TABLE 405 Rest of LAMEA Semiconductor Production Equipment Market, 2022 - 2028, USD Million

- TABLE 406 Rest of LAMEA Semiconductor Production Equipment Market by Dimension, 2018 - 2021, USD Million

- TABLE 407 Rest of LAMEA Semiconductor Production Equipment Market by Dimension, 2022 - 2028, USD Million

- TABLE 408 Rest of LAMEA Semiconductor Production Equipment Market by Supply Chain Process, 2018 - 2021, USD Million

- TABLE 409 Rest of LAMEA Semiconductor Production Equipment Market by Supply Chain Process, 2022 - 2028, USD Million

- TABLE 410 Rest of LAMEA Semiconductor Production Equipment Market by Product Type, 2018 - 2021, USD Million

- TABLE 411 Rest of LAMEA Semiconductor Production Equipment Market by Product Type, 2022 - 2028, USD Million

- TABLE 412 Rest of LAMEA Semiconductor Production Equipment Market by Function, 2018 - 2021, USD Million

- TABLE 413 Rest of LAMEA Semiconductor Production Equipment Market by Function, 2022 - 2028, USD Million

- TABLE 414 Key Information - KLA Corporation

- TABLE 415 Key Information - Teradyne, Inc.

- TABLE 416 Key Information - ASML Holding N.V

- TABLE 417 Key Information - Applied Materials, Inc.

- TABLE 418 Key Information - SCREEN Holdings Co., Ltd

- TABLE 419 Key Information - Veeco Instruments, Inc.

- TABLE 420 Key Information - Nikon Corporation

- TABLE 421 key Information - Carl Zeiss AG

- TABLE 422 Key Information - Lam Research Corporation

- TABLE 423 Key Information - Alsil Material

List of Figures

- FIG 1 Methodology for the research

- FIG 2 KBV Cardinal Matrix

- FIG 3 Key Leading Strategies: Percentage Distribution (2018-2022)

- FIG 4 Global Semiconductor Production Equipment Market Share by Dimension, 2021

- FIG 5 Global Semiconductor Production Equipment Market Share by Dimension, 2028

- FIG 6 Global Semiconductor Production Equipment Market by Dimension, 2018 - 2028, USD Million

- FIG 7 Global Semiconductor Production Equipment Market Share by Supply Chain Process, 2021

- FIG 8 Global Semiconductor Production Equipment Market Share by Supply Chain Process, 2028

- FIG 9 Global Semiconductor Production Equipment Market by Supply Chain Process, 2018 - 2028, USD Million

- FIG 10 Global Semiconductor Production Equipment Market Share by Product Type, 2021

- FIG 11 Global Semiconductor Production Equipment Market Share by Product Type, 2028

- FIG 12 Global Semiconductor Production Equipment Market by Product Type, 2018 - 2028, USD Million

- FIG 13 Global Semiconductor Production Equipment Market Share by Function, 2021

- FIG 14 Global Semiconductor Production Equipment Market Share by Function, 2028

- FIG 15 Global Semiconductor Production Equipment Market by Function, 2018 - 2028, USD Million

- FIG 16 Global Semiconductor Production Equipment Market Share by Region, 2021

- FIG 17 Global Semiconductor Production Equipment Market Share by Region, 2028

- FIG 18 Global Semiconductor Production Equipment Market by Region, 2018 - 2028, USD Million

- FIG 19 Recent strategies and developments: KLA Corporation

- FIG 20 Recent strategies and developments: Teradyne, Inc.

The Global Semiconductor Production Equipment Market size is expected to reach $153.8 billion by 2028, rising at a market growth of 9.2% CAGR during the forecast period.

Semiconductor production equipment is used to manufacture memory chips, semiconductor circuits, and other components. The ability of free electrons to easily move between atoms in semiconductors allows the free flow of electricity through them. This ability makes semiconductors ideal for designing and developing compounds like wafers, integrated circuits, diodes, etc., used in many electronic devices and systems.

The semiconductor industry is expanding quickly, which is helping to boost sales of modern semiconductor production equipment and propel the market upward. Consumers' rising desire for electronic gadgets drives the demand for chips, which is anticipated to indirectly raise the requirement for semiconductor production equipment. The demand for consumer electronics is rising globally, which can be linked to the growing necessity for user-friendly electronic products as well as the expanding residential sector. For example, MEMS, optoelectronics, and MOEMS devices are used in the mass manufacturing of electronic items, including wearables, smartphones, and white goods.

Due to the delicate nature of semiconductor processing, precise supervision of automated steps, including cutting, drying, washing, etching, and assembly, as well as total control over working parameters like temperature and humidity, are required. A solution for improved control of these parameters, along with other automated processes, and the environment where semiconductors are made, is provided by semiconductor production equipment. Semiconductor production equipment provides numerous advantages like improved production, greater output & dependability, fewer production & design errors, decreased process & equipment downtime, and enhanced workplace security.

COVID-19 Impact Analysis

The pandemic had a negative impact on the semiconductor production equipment market. During the COVID-19 pandemic, the electronics industry suffered adversely, as the pandemic also created a significant shortage in the semiconductor supply chain. Due to the COVID-19 lockdown, numerous semiconductor sector components could not be produced, which led to a shortage of semiconductors worldwide. In addition, end-users of semiconductors originally cut back on their production equipment purchases due to the recession. After the decline in cases, several businesses have displayed considerable indications of recovery.

Market Growth Factors

Growing demand for consumer electronics worldwide

The increasing demand for semiconductor chips from producers of consumer electronics, medical devices, and sensor systems is driving the rise of the semiconductor business. Since more people are using consumer electronics like cell phones, laptops, televisions, and other devices, the industry is growing. The need for production equipment is expected to rise because semiconductors are crucial to many sectors related to consumer electronic products, including telecommunications, information technology, machine automation, power & solar photovoltaic, and others. Rising digital content and improved connectivity, as well as mobility in the coming years, will further promote market expansion.

Rising semiconductor usage in the automotive industry

The automotive industry continues to be a significant source of demand as well as a source of potential for semiconductor vendors, despite recent recessions and demand variations. Trends like the rise in demand for autonomous & electric vehicles and the increasing number of semiconductor components per vehicle are key motivators for semiconductor manufacturers. As more semiconductor components, such as sensors, microcontrollers, and radar chips, are utilized in automobiles, the market for semiconductor production equipment expands.

Market Restraining Factors

High costs of machines and interruptions to the supply chain

The supply chain for the semiconductor production equipment market has a large number of participants. However, the coronavirus pandemic significantly hindered the market's supply chain. The locations of semiconductor production plants must be in tidy areas. Moreover, there should be no flaws in the equipment supplied for making semiconductors. Most importantly, semiconductor equipment is expensive and requires a significant upfront investment. Machine price volatility is anticipated to impede market expansion.

Dimension Outlook

On the basis of dimension, the semiconductor production equipment market is fragmented into 2 dimension, 2.5 dimension, and 3 dimension. The 2 dimension segment acquired a substantial revenue share in the semiconductor production equipment market in 2021. The 2 dimension semiconductors allow reduced length as well as reusability, which further reduces time and system cost. This aspect is causing the segment for equipment used in 2D semiconductor fabrication to grow more quickly.

Supply Chain Process Outlook

Based on supply chain process, the semiconductor production equipment market is categorized into IDM, OSAT, and foundry. The OSAT segment procured a considerable growth rate in the semiconductor production equipment market in 2021. OSAT (Outsourced semiconductor assembly and test) companies provide test services as well as third-party IC packaging. These companies' test and package silicon products made by foundries before putting them on the market.

Product Type Outlook

On the basis of product type, the semiconductor production equipment market is divided into front-end equipment and back-end equipment. The front-end equipment segment acquired the largest revenue share in the semiconductor production equipment market in 2021. All of the manufacturing tools used to produce semiconductors are included in the front-end equipment. The rising demand for chips that are highly efficient and dense for use in IoT devices, CPUs, GPUs, and other devices is partially responsible for the expansion of the segment.

Function Outlook

Based on function, the semiconductor production equipment market is segmented into integrated circuits and OSD. The integrated circuits (ICs) segment witnessed the maximum revenue share in the semiconductor production equipment market in 2021. An Integrated Device Manufacturer (IDM) oversees each step of the production and sales processes in the semiconductor industry. IDMs help reduce costs, maintain the optimum operation of manufacturing plants, and aid in the development of market strategies. These benefits of IDMs are attributed to the growth of the segment.

Regional Outlook

On the basis of region, the semiconductor production equipment market is analyzed across North America, Europe, Asia Pacific, and LAMEA. The Asia Pacific region recorded the largest revenue share in the semiconductor production equipment market in 2021. The region's sizable semiconductor industry, which benefits from the demand for semiconductors, is responsible for the segment's rise. This has a favorable impact on the prognosis for the market for semiconductor production equipment in the region.

The major strategies followed by the market participants are Acquisition. Based on the Analysis presented in the Cardinal matrix; Applied Materials, Inc., ASML Holdings N.V., Lam Research Corporation and KLA Corporation are the forerunners in the Semiconductor Production Equipment Market. Companies such as Carl Zeiss AG, Teradyne, Inc. and Screen Holdings are some of the key innovators in Semiconductor Production Equipment Market.

The market research report covers the analysis of key stake holders of the market. Key companies profiled in the report include Alsil Material, ASML Holdings N.V., SCREEN Holdings Co., Ltd., Teradyne, Inc., Applied Materials, Inc., Veeco Instruments, Inc., KLA Corporation, Nikon Corporation, Carl Zeiss AG, and Lam Research Corporation.

Recent Strategies deployed in Semiconductor Production Equipment Market

Partnerships, Collaborations & Agreements

Oct-2022: Applied Materials, Inc. collaborated with BE Semiconductor Industries N.V., a company engaged in the manufacturing of semiconductors. Through this collaboration, the combining companies would create a solution for die-based hybrid bonding, a chip-to-chip interconnect technology that enables subsystem designs and heterogeneous chips for applications involving 5G, AI and high-performance computing. Additionally, this would accelerate heterogeneous integration technology and enhance the types of equipment.

Jan-2022: ASML Holding N.V. collaborated with Intel Corporation, a semiconductor chip manufacturer. This move would help in boosting semiconductor lithography technology. This collaboration would ensure cost-efficient manufacturing of chips by providing lithographic improvements in lesser cycle time, energy, cost and complexity.

Product Launches and Product Expansions

Dec-2022: KLA Corporation unveiled Axion T2000 X-ray metrology system to help memory chip manufacturers. This product can count high aspect ratio device features along with exceptional accuracy, speed, precision and resolution. Axion T2000 confirms the smooth production of memory chips utilized for artificial intelligence, edge computing, 5G and data centers.

Jun-2021: KLA Corporation released four new products: C205 broadband plasma patterned wafer inspection system, I-PAT® inline defect part average testing screening solution, Surfscan® SP A2/A3 unpatterned wafer inspection system and 8935 high productivity patterned wafer inspection system. These launched products would deliver a creative solution for inline screening and finding possible reliability defects. Additionally, these products would assist microchip manufacturing plants in achieving reliability and quality chips to maximize output.

Sep-2020: KLA unveiled three semiconductor packaging techniques: ICOS T3/T7 Series, Kronos 1190 wafer inspection system and ICOS F160XP die sorting and inspection system. These launched systems help the customers to master the challenges in integrated circuits. Additionally, these products would permit users to advance the fabrication of semiconductor devices.

Acquisition and Mergers

Nov-2022: Lam Research Corp. completed the acquisition of SEMSYSCO GmbH. With the addition of SEMSYSCO, Lam gains capabilities in advanced packaging, ideal for leading-edge logic chips and chiplet-based solutions for high-performance computing (HPC), artificial intelligence (AI) and other data-intensive applications.

Nov-2022: Lam Research Corp. acquired SEMSYSCO GmbH, a semiconductor manufacturing company. This acquisition would enhance the of company's packaging capabilities which is suitable for chip-based solutions, artificial intelligence, data-intensive applications and data-intensive applications.

Oct-2022: ASML took over Berliner Glas Group, a company supplying components for EUV and DUV lithography. This acquisition would lead to the addition of the capabilities of both the companies in manufacturing and R&D to assist further growth and launches of EUV systems to deliver important services to the customers.

Jun-2022: Applied Materials completed the acquisition of Picosun Oy, a company manufacturing semiconductor equipment. This acquisition would broaden the suite of Applied Materials and customer involvement. Moreover, this would help the company to support customers in putting more functionality and intelligence in various edge computing equipment.

Geographical Expansions

Nov-2022: ZEISS is expanding its geographical footprint in Germany by building a multifunctional factory. This facility is accompanied by technical operations building in which compressed air can be generated. This expansion would help in manufacturing high-tech products like lithography optics that need special conditions.

Dec-2021: Lam Research Corp. (Nasdaq: LRCX) today announced the expansion of its manufacturing footprint in Oregon. The new facility is Lam's fifth manufacturing site in the United States and will further enhance its resilience and ability to meet increasing customer demand, as chip suppliers seek to ramp up production globally.

Dec-2021: Lam Research Corp. is expanding its geographical footprint by opening a manufacturing facility in Oregon, USA. This would enhance the company's ability to meet the demands of customer and ramp up the chip supplies globally.

Scope of the Study

Market Segments covered in the Report:

By Dimension

- 3-Dimension

- 2.5-Dimension

- 2-Dimension

By Supply Chain Process

- IDM

- OSAT

- Others

By Product Type

- Front-end Equipment

- Back-end Equipment

By Function

- Integrated Circuits

- OSD

By Geography

- North America

- US

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- UK

- France

- Russia

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Singapore

- Malaysia

- Rest of Asia Pacific

- LAMEA

- Brazil

- Argentina

- UAE

- Saudi Arabia

- South Africa

- Nigeria

- Rest of LAMEA

Companies Profiled

- Alsil Material

- ASML Holdings N.V.

- SCREEN Holdings Co., Ltd

- Teradyne, Inc.

- Applied Materials, Inc.

- Veeco Instruments, Inc.

- KLA Corporation

- Nikon Corporation

- Carl Zeiss AG

- Lam Research Corporation

Unique Offerings from KBV Research

- Exhaustive coverage

- Highest number of market tables and figures

- Subscription based model available

- Guaranteed best price

- Assured post sales research support with 10% customization free

Table of Contents

Chapter 1. Market Scope & Methodology

- 1.1 Market Definition

- 1.2 Objectives

- 1.3 Market Scope

- 1.4 Segmentation

- 1.4.1 Global Semiconductor Production Equipment Market, by Dimension

- 1.4.2 Global Semiconductor Production Equipment Market, by Supply Chain Process

- 1.4.3 Global Semiconductor Production Equipment Market, by Product Type Process

- 1.4.4 Global Semiconductor Production Equipment Market, by Function

- 1.4.5 Global Semiconductor Production Equipment Market, by Geography

- 1.5 Methodology for the research

Chapter 2. Market Overview

- 2.1 Introduction

- 2.1.1 Overview

- 2.1.1.1 Market Composition & Scenario

- 2.1.1 Overview

- 2.2 Key Factors Impacting the Market

- 2.2.1 Market Drivers

- 2.2.2 Market Restraints

Chapter 3. Competition Analysis - Global

- 3.1 KBV Cardinal Matrix

- 3.2 Recent Industry Wide Strategic Developments

- 3.2.1 Partnerships, Collaborations and Agreements

- 3.2.2 Product Launches and Product Expansions

- 3.2.3 Acquisition and Mergers

- 3.1 Top Winning Strategies

- 3.1.1 Key Leading Strategies: Percentage Distribution (2018-2022)

Chapter 4. Global Semiconductor Production Equipment Market by Dimension

- 4.1 Global 3-Dimension Market by Region

- 4.2 Global 2.5-Dimension Market by Region

- 4.3 Global 2-Dimension Market by Region

Chapter 5. Global Semiconductor Production Equipment Market by Supply Chain Process

- 5.1 Global IDM Market by Region

- 5.2 Global OSAT Market by Region

- 5.3 Global Others Market by Region

Chapter 6. Global Semiconductor Production Equipment Market by Product Type

- 6.1 Global Front-end Equipment Market by Region

- 6.2 Global Back-end Equipment Market by Region

Chapter 7. Global Semiconductor Production Equipment Market by Function

- 7.1 Global Integrated Circuits Market by Region

- 7.2 Global OSD Market by Region

Chapter 8. Global Semiconductor Production Equipment Market by Region

- 8.1 North America Semiconductor Production Equipment Market

- 8.1.1 North America Semiconductor Production Equipment Market by Dimension

- 8.1.1.1 North America 3-Dimension Market by Country

- 8.1.1.2 North America 2.5-Dimension Market by Country

- 8.1.1.3 North America 2-Dimension Market by Country

- 8.1.2 North America Semiconductor Production Equipment Market by Supply Chain Process

- 8.1.2.1 North America IDM Market by Country

- 8.1.2.2 North America OSAT Market by Country

- 8.1.2.3 North America Others Market by Country

- 8.1.3 North America Semiconductor Production Equipment Market by Product Type

- 8.1.3.1 North America Front-end Equipment Market by Country

- 8.1.3.2 North America Back-end Equipment Market by Country

- 8.1.4 North America Semiconductor Production Equipment Market by Function

- 8.1.4.1 North America Integrated Circuits Market by Country

- 8.1.4.2 North America OSD Market by Country

- 8.1.5 North America Semiconductor Production Equipment Market by Country

- 8.1.5.1 US Semiconductor Production Equipment Market

- 8.1.5.1.1 US Semiconductor Production Equipment Market by Dimension

- 8.1.5.1.2 US Semiconductor Production Equipment Market by Supply Chain Process

- 8.1.5.1.3 US Semiconductor Production Equipment Market by Product Type

- 8.1.5.1.4 US Semiconductor Production Equipment Market by Function

- 8.1.5.2 Canada Semiconductor Production Equipment Market

- 8.1.5.2.1 Canada Semiconductor Production Equipment Market by Dimension

- 8.1.5.2.2 Canada Semiconductor Production Equipment Market by Supply Chain Process

- 8.1.5.2.3 Canada Semiconductor Production Equipment Market by Product Type

- 8.1.5.2.4 Canada Semiconductor Production Equipment Market by Function

- 8.1.5.3 Mexico Semiconductor Production Equipment Market

- 8.1.5.3.1 Mexico Semiconductor Production Equipment Market by Dimension

- 8.1.5.3.2 Mexico Semiconductor Production Equipment Market by Supply Chain Process

- 8.1.5.3.3 Mexico Semiconductor Production Equipment Market by Product Type

- 8.1.5.3.4 Mexico Semiconductor Production Equipment Market by Function

- 8.1.5.4 Rest of North America Semiconductor Production Equipment Market

- 8.1.5.4.1 Rest of North America Semiconductor Production Equipment Market by Dimension

- 8.1.5.4.2 Rest of North America Semiconductor Production Equipment Market by Supply Chain Process

- 8.1.5.4.3 Rest of North America Semiconductor Production Equipment Market by Product Type

- 8.1.5.4.4 Rest of North America Semiconductor Production Equipment Market by Function

- 8.1.5.1 US Semiconductor Production Equipment Market

- 8.1.1 North America Semiconductor Production Equipment Market by Dimension

- 8.2 Europe Semiconductor Production Equipment Market

- 8.2.1 Europe Semiconductor Production Equipment Market by Dimension

- 8.2.1.1 Europe 3-Dimension Market by Country

- 8.2.1.2 Europe 2.5-Dimension Market by Country

- 8.2.1.3 Europe 2-Dimension Market by Country

- 8.2.2 Europe Semiconductor Production Equipment Market by Supply Chain Process

- 8.2.2.1 Europe IDM Market by Country

- 8.2.2.2 Europe OSAT Market by Country

- 8.2.2.3 Europe Others Market by Country

- 8.2.3 Europe Semiconductor Production Equipment Market by Product Type

- 8.2.3.1 Europe Front-end Equipment Market by Country

- 8.2.3.2 Europe Back-end Equipment Market by Country

- 8.2.4 Europe Semiconductor Production Equipment Market by Function

- 8.2.4.1 Europe Integrated Circuits Market by Country

- 8.2.4.2 Europe OSD Market by Country

- 8.2.5 Europe Semiconductor Production Equipment Market by Country

- 8.2.5.1 Germany Semiconductor Production Equipment Market

- 8.2.5.1.1 Germany Semiconductor Production Equipment Market by Dimension

- 8.2.5.1.2 Germany Semiconductor Production Equipment Market by Supply Chain Process

- 8.2.5.1.3 Germany Semiconductor Production Equipment Market by Product Type

- 8.2.5.1.4 Germany Semiconductor Production Equipment Market by Function

- 8.2.5.2 UK Semiconductor Production Equipment Market

- 8.2.5.2.1 UK Semiconductor Production Equipment Market by Dimension

- 8.2.5.2.2 UK Semiconductor Production Equipment Market by Supply Chain Process

- 8.2.5.2.3 UK Semiconductor Production Equipment Market by Product Type

- 8.2.5.2.4 UK Semiconductor Production Equipment Market by Function

- 8.2.5.3 France Semiconductor Production Equipment Market

- 8.2.5.3.1 France Semiconductor Production Equipment Market by Dimension

- 8.2.5.3.2 France Semiconductor Production Equipment Market by Supply Chain Process

- 8.2.5.3.3 France Semiconductor Production Equipment Market by Product Type

- 8.2.5.3.4 France Semiconductor Production Equipment Market by Function

- 8.2.5.4 Russia Semiconductor Production Equipment Market

- 8.2.5.4.1 Russia Semiconductor Production Equipment Market by Dimension

- 8.2.5.4.2 Russia Semiconductor Production Equipment Market by Supply Chain Process

- 8.2.5.4.3 Russia Semiconductor Production Equipment Market by Product Type

- 8.2.5.4.4 Russia Semiconductor Production Equipment Market by Function

- 8.2.5.5 Spain Semiconductor Production Equipment Market

- 8.2.5.5.1 Spain Semiconductor Production Equipment Market by Dimension

- 8.2.5.5.2 Spain Semiconductor Production Equipment Market by Supply Chain Process

- 8.2.5.5.3 Spain Semiconductor Production Equipment Market by Product Type

- 8.2.5.5.4 Spain Semiconductor Production Equipment Market by Function

- 8.2.5.6 Italy Semiconductor Production Equipment Market

- 8.2.5.6.1 Italy Semiconductor Production Equipment Market by Dimension

- 8.2.5.6.2 Italy Semiconductor Production Equipment Market by Supply Chain Process

- 8.2.5.6.3 Italy Semiconductor Production Equipment Market by Product Type

- 8.2.5.6.4 Italy Semiconductor Production Equipment Market by Function

- 8.2.5.7 Rest of Europe Semiconductor Production Equipment Market

- 8.2.5.7.1 Rest of Europe Semiconductor Production Equipment Market by Dimension

- 8.2.5.7.2 Rest of Europe Semiconductor Production Equipment Market by Supply Chain Process

- 8.2.5.7.3 Rest of Europe Semiconductor Production Equipment Market by Product Type

- 8.2.5.7.4 Rest of Europe Semiconductor Production Equipment Market by Function

- 8.2.5.1 Germany Semiconductor Production Equipment Market

- 8.2.1 Europe Semiconductor Production Equipment Market by Dimension

- 8.3 Asia Pacific Semiconductor Production Equipment Market

- 8.3.1 Asia Pacific Semiconductor Production Equipment Market by Dimension

- 8.3.1.1 Asia Pacific 3-Dimension Market by Country

- 8.3.1.2 Asia Pacific 2.5-Dimension Market by Country

- 8.3.1.3 Asia Pacific 2-Dimension Market by Country

- 8.3.2 Asia Pacific Semiconductor Production Equipment Market by Supply Chain Process

- 8.3.2.1 Asia Pacific IDM Market by Country

- 8.3.2.2 Asia Pacific OSAT Market by Country

- 8.3.2.3 Asia Pacific Others Market by Country

- 8.3.3 Asia Pacific Semiconductor Production Equipment Market by Product Type

- 8.3.3.1 Asia Pacific Front-end Equipment Market by Country

- 8.3.3.2 Asia Pacific Back-end Equipment Market by Country

- 8.3.4 Asia Pacific Semiconductor Production Equipment Market by Function

- 8.3.4.1 Asia Pacific Integrated Circuits Market by Country

- 8.3.4.2 Asia Pacific OSD Market by Country

- 8.3.5 Asia Pacific Semiconductor Production Equipment Market by Country

- 8.3.5.1 China Semiconductor Production Equipment Market

- 8.3.5.1.1 China Semiconductor Production Equipment Market by Dimension

- 8.3.5.1.2 China Semiconductor Production Equipment Market by Supply Chain Process

- 8.3.5.1.3 China Semiconductor Production Equipment Market by Product Type

- 8.3.5.1.4 China Semiconductor Production Equipment Market by Function

- 8.3.5.2 Japan Semiconductor Production Equipment Market

- 8.3.5.2.1 Japan Semiconductor Production Equipment Market by Dimension

- 8.3.5.2.2 Japan Semiconductor Production Equipment Market by Supply Chain Process

- 8.3.5.2.3 Japan Semiconductor Production Equipment Market by Product Type

- 8.3.5.2.4 Japan Semiconductor Production Equipment Market by Function

- 8.3.5.3 India Semiconductor Production Equipment Market

- 8.3.5.3.1 India Semiconductor Production Equipment Market by Dimension

- 8.3.5.3.2 India Semiconductor Production Equipment Market by Supply Chain Process

- 8.3.5.3.3 India Semiconductor Production Equipment Market by Product Type

- 8.3.5.3.4 India Semiconductor Production Equipment Market by Function

- 8.3.5.4 South Korea Semiconductor Production Equipment Market

- 8.3.5.4.1 South Korea Semiconductor Production Equipment Market by Dimension

- 8.3.5.4.2 South Korea Semiconductor Production Equipment Market by Supply Chain Process

- 8.3.5.4.3 South Korea Semiconductor Production Equipment Market by Product Type

- 8.3.5.4.4 South Korea Semiconductor Production Equipment Market by Function

- 8.3.5.5 Singapore Semiconductor Production Equipment Market

- 8.3.5.5.1 Singapore Semiconductor Production Equipment Market by Dimension

- 8.3.5.5.2 Singapore Semiconductor Production Equipment Market by Supply Chain Process

- 8.3.5.5.3 Singapore Semiconductor Production Equipment Market by Product Type

- 8.3.5.5.4 Singapore Semiconductor Production Equipment Market by Function

- 8.3.5.6 Malaysia Semiconductor Production Equipment Market

- 8.3.5.6.1 Malaysia Semiconductor Production Equipment Market by Dimension

- 8.3.5.6.2 Malaysia Semiconductor Production Equipment Market by Supply Chain Process

- 8.3.5.6.3 Malaysia Semiconductor Production Equipment Market by Product Type

- 8.3.5.6.4 Malaysia Semiconductor Production Equipment Market by Function

- 8.3.5.7 Rest of Asia Pacific Semiconductor Production Equipment Market

- 8.3.5.7.1 Rest of Asia Pacific Semiconductor Production Equipment Market by Dimension

- 8.3.5.7.2 Rest of Asia Pacific Semiconductor Production Equipment Market by Supply Chain Process

- 8.3.5.7.3 Rest of Asia Pacific Semiconductor Production Equipment Market by Product Type

- 8.3.5.7.4 Rest of Asia Pacific Semiconductor Production Equipment Market by Function

- 8.3.5.1 China Semiconductor Production Equipment Market

- 8.3.1 Asia Pacific Semiconductor Production Equipment Market by Dimension

- 8.4 LAMEA Semiconductor Production Equipment Market

- 8.4.1 LAMEA Semiconductor Production Equipment Market by Dimension

- 8.4.1.1 LAMEA 3-Dimension Market by Country

- 8.4.1.2 LAMEA 2.5-Dimension Market by Country

- 8.4.1.3 LAMEA 2-Dimension Market by Country

- 8.4.2 LAMEA Semiconductor Production Equipment Market by Supply Chain Process

- 8.4.2.1 LAMEA IDM Market by Country

- 8.4.2.2 LAMEA OSAT Market by Country

- 8.4.2.3 LAMEA Others Market by Country

- 8.4.3 LAMEA Semiconductor Production Equipment Market by Product Type

- 8.4.3.1 LAMEA Front-end Equipment Market by Country

- 8.4.3.2 LAMEA Back-end Equipment Market by Country

- 8.4.4 LAMEA Semiconductor Production Equipment Market by Function

- 8.4.4.1 LAMEA Integrated Circuits Market by Country

- 8.4.4.2 LAMEA OSD Market by Country

- 8.4.5 LAMEA Semiconductor Production Equipment Market by Country

- 8.4.5.1 Brazil Semiconductor Production Equipment Market

- 8.4.5.1.1 Brazil Semiconductor Production Equipment Market by Dimension

- 8.4.5.1.2 Brazil Semiconductor Production Equipment Market by Supply Chain Process

- 8.4.5.1.3 Brazil Semiconductor Production Equipment Market by Product Type

- 8.4.5.1.4 Brazil Semiconductor Production Equipment Market by Function

- 8.4.5.2 Argentina Semiconductor Production Equipment Market

- 8.4.5.2.1 Argentina Semiconductor Production Equipment Market by Dimension

- 8.4.5.2.2 Argentina Semiconductor Production Equipment Market by Supply Chain Process

- 8.4.5.2.3 Argentina Semiconductor Production Equipment Market by Product Type

- 8.4.5.2.4 Argentina Semiconductor Production Equipment Market by Function

- 8.4.5.3 UAE Semiconductor Production Equipment Market

- 8.4.5.3.1 UAE Semiconductor Production Equipment Market by Dimension

- 8.4.5.3.2 UAE Semiconductor Production Equipment Market by Supply Chain Process

- 8.4.5.3.3 UAE Semiconductor Production Equipment Market by Product Type

- 8.4.5.3.4 UAE Semiconductor Production Equipment Market by Function

- 8.4.5.4 Saudi Arabia Semiconductor Production Equipment Market

- 8.4.5.4.1 Saudi Arabia Semiconductor Production Equipment Market by Dimension

- 8.4.5.4.2 Saudi Arabia Semiconductor Production Equipment Market by Supply Chain Process

- 8.4.5.4.3 Saudi Arabia Semiconductor Production Equipment Market by Product Type

- 8.4.5.4.4 Saudi Arabia Semiconductor Production Equipment Market by Function

- 8.4.5.5 South Africa Semiconductor Production Equipment Market

- 8.4.5.5.1 South Africa Semiconductor Production Equipment Market by Dimension

- 8.4.5.5.2 South Africa Semiconductor Production Equipment Market by Supply Chain Process

- 8.4.5.5.3 South Africa Semiconductor Production Equipment Market by Product Type

- 8.4.5.5.4 South Africa Semiconductor Production Equipment Market by Function

- 8.4.5.6 Nigeria Semiconductor Production Equipment Market

- 8.4.5.6.1 Nigeria Semiconductor Production Equipment Market by Dimension

- 8.4.5.6.2 Nigeria Semiconductor Production Equipment Market by Supply Chain Process

- 8.4.5.6.3 Nigeria Semiconductor Production Equipment Market by Product Type

- 8.4.5.6.4 Nigeria Semiconductor Production Equipment Market by Function