|

|

市場調査レポート

商品コード

1150171

心臓安全性サービスの世界市場規模、シェア、産業動向分析レポート:タイプ別、エンドユーザー別、サービスタイプ別、地域別展望と予測、2022年~2028年Global Cardiac Safety Services Market Size, Share & Industry Trends Analysis Report By Type, By End User, By Type of Service, By Regional Outlook and Forecast, 2022 - 2028 |

||||||

|

|

|||||||

| 心臓安全性サービスの世界市場規模、シェア、産業動向分析レポート:タイプ別、エンドユーザー別、サービスタイプ別、地域別展望と予測、2022年~2028年 |

|

出版日: 2022年09月30日

発行: KBV Research

ページ情報: 英文 212 Pages

納期: 即納可能

|

- 全表示

- 概要

- 図表

- 目次

世界の心臓安全性サービス市場規模は、2028年までに11億米ドルに達し、予測期間中にCAGR11.1%の市場成長率で上昇すると予測されています。

心臓、血管、血液成分など、心血管系のすべての要素は、心血管系と非心血管系の両方の医薬品を含む心血管系安全性負債の影響を受けます。心血管系の副作用は、機能的なものと構造的なもの(病理組織学など)があり、急性または慢性治療後に起こる可能性があります。

世間の目が厳しくなり、ビジネスコストが上昇し、規制当局のリソースが限られている現在、効果的かつ安全な医薬品開発の必要性は、これまで以上に高まっています。年間1790万人が死亡する心血管系疾患(CVD)は、世界で最も一般的な死因となっています。脳血管疾患、冠状動脈性心臓疾患、リウマチ性心臓疾患などは、CVDと呼ばれる心臓や血管の疾患のカテゴリーに含まれます。

COVID-19影響度分析

このため、製薬業界や医療保険業界は、より良いサービスを提供するために、必要な変更を行うようになりました。また、医学の進化に伴い、心臓の健康を専門とする多くの研究機関や組織の関与が必要となっています。コロナウイルス関連の大惨事は、持病のある患者を多数死なせ、心臓安全性サービスに影響を及ぼしました。COVID-19の市場開拓を精力的に進めた結果、心臓安全対策サービス市場全体に好影響を及ぼしました。

市場の成長要因

バイオシミラーやバイオロジクスの研究の増加

多くの企業が、生物学的製剤やバイオシミラー化合物の創製に大きな投資を行っています。探索段階では、ペプチド、タンパク質、モノクローナル抗体などの生物製剤が治療薬候補の半分以上を占めています。製薬会社やバイオ医薬品会社は、新規の生物製剤を開発中、あるいはパイプラインにあるため、その研究開発に多額の資金を投じています。また、バイオシミラー医薬品は、特許を取得している生物学的製剤の後発品であるため、厳しい規制の対象とはならないため、価格が低く抑えられています。

一般人口におけるEchホルターサービスの高い普及率

ECGホルターの普及は、高齢者の増加や心血管疾患の発生率の増加が主な原因となっています。Health System Trackerが発表したデータによると、米国では心臓病が死亡原因のトップです。こうした理由から、心拍を即座に検出し、常に心拍を監視する装置が必要とされています。過去数年間、ヘルスケアシステムはECGモニタリング機器を採用し、心臓の活動に異常がないかを調べています。

市場抑制要因

臨床試験のための有資格者不足

医薬品、バイオテクノロジー、医療機器の研究開発アウトソーシング業界は、常に変化しています。高品質のサービスを提供し、許容されるラボの手順を守り、医療機器や医薬品の研究開発技術や手法の進歩に対応するためには、高度なスキルを持つ専門家が必要となります。CROは、バイオテクノロジー、製薬、医療機器企業、研究・学術機関と、訓練を受けた経験豊富な科学者の獲得で競合しており、高いスキルを持つ人材の獲得と維持が困難な状況にあります。

タイプ別展望

心臓安全性サービス市場は、タイプ別に統合型とスタンドアロン型に分けられます。統合型セグメントは、2021年に最も高い収益シェアで心臓安全性サービス市場を独占しました。これらの最先端のコアラボサービスは、イメージング、TQT、およびプロファイルQTテストを含む、フルレンジの心臓安全性サービスを提供します。心拍とリズムのリアルタイム評価を支援するため、ターゲット外の心血管負債にも目を配り、免許を持つ看護師の監督のもと、現場で多チャンネルテレメトリーを実施します。

サービスの種類別展望

心臓安全性サービス市場は、サービスの種類によって、ECG/ホルター測定、血圧測定、心血管イメージング、QT検査、およびその他のサービスに分けられます。2021年の心臓安全性サービス市場では、ECG/ホルター測定分野が最大の収益シェアを示しています。スマートウォッチやその他のパーソナルエレクトロニクスは、心電図モニタリングを提供します。ホルターモニターと呼ばれる小型のポータブルガジェットは、心拍を捉えるために使用されます。異常な心拍(不整脈)を特定し、その可能性を評価するために採用されます。

エンドユーザーの展望

心臓安全性サービス市場は、エンドユーザーに基づき、製薬・バイオ製薬会社と受託研究機関に分類されます。契約研究機関セグメントは、2021年に心臓安全性サービス市場でかなりの収益シェアを調達しました。臨床試験は、製薬、医療機器、バイオテクノロジー企業、および学術機関、政府機関、財団のために、契約研究機関(CRO)によって実施されます。

地域別の展望

地域別に見ると、心臓安全装置は北米、欧州、アジア太平洋、LAMEAで分析されています。北米地域は、2021年の心臓安全性サービス市場において、最も高い収益シェアを獲得しました。これは、同地域の臨床研究数が増加しており、心臓安全性サービスに対する需要が高まっているためです。心血管疾患(CVD)や冠状動脈性心臓病(CHD)を患う人の増加により、同地域の薬剤開発や研究調査が加速しています。

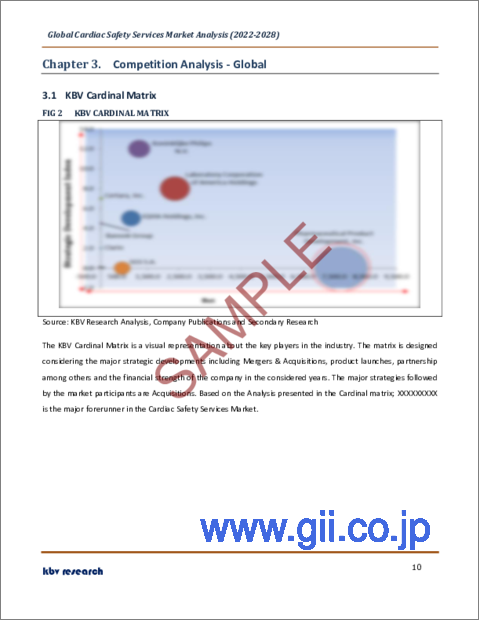

市場参入企業がとる主な戦略は買収です。Cardinalマトリックスで提示された分析によると、Pharmaceutical Product Development, Inc.が心臓安全性サービス市場における主要な先駆者です。Koninklijke Philips N.V.、Laboratory Corporation of America Holdings、IQVIA Holdings, Inc.などの企業は、心臓安全性サービス市場における主要な革新者の一人です。

目次

第1章 市場の範囲と調査手法

- 市場の定義

- 目的

- 市場規模

- セグメンテーション

- 心臓安全性サービスの世界市場、タイプ別

- 心臓安全性サービスの世界市場、エンドユーザー別

- 心臓安全性サービスの世界市場、サービスタイプ別

- 心臓安全性サービスの世界市場、地域別

- 調査手法

第2章 市場概要

- イントロダクション

- 概要説明

- 市場の構成とシナリオ

- 概要説明

- 市場に影響を与える主な要因

- 市場促進要因

- 市場の抑制要因

第3章 競合分析-世界

- KBVカーディナルマトリックス

- 最近の業界全体の戦略的展開

- パートナーシップ、コラボレーション、契約

- 製品上市と製品拡張

- 買収と合併

- 地理的拡大

- 主要成功戦略

- 主要なリーディング戦略:割合の分布(2018-2022年)

第4章 心臓安全性サービスの世界市場:タイプ別

- 世界の統合型市場:地域別

- 世界のスタンドアロン市場:地域別

第5章 心臓安全性サービスの世界市場:エンドユーザー別

- 世界の製薬会社・バイオ製薬会社の地域別市場

- 世界の契約研究機関市場:地域別

第6章 心臓安全性サービスの世界市場:サービスタイプ別

- 心電図・ホルター測定の世界市場:地域別

- 血圧測定の世界市場:地域別

- 心血管イメージングの世界市場:地域別

- QT徹底調査の世界市場:地域別

- 世界の地域別その他市場

第7章 心臓安全性サービスの世界市場:地域別市場

- 北米

- 北米の心臓安全性サービスの国別市場

- 米国

- カナダ

- メキシコ

- 北米以外の地域

- 北米の心臓安全性サービスの国別市場

- 欧州

- 欧州心臓安全性サービス市場:国別

- ドイツ

- 英国

- フランス

- ロシア

- スペイン

- イタリア

- その他欧州

- 欧州心臓安全性サービス市場:国別

- アジア太平洋地域

- アジア太平洋地域の心臓安全性サービスの国別市場

- 中国

- 日本

- インド

- 韓国

- シンガポール

- マレーシア

- その他アジア太平洋地域

- アジア太平洋地域の心臓安全性サービスの国別市場

- LAMEA

- LAMEA心臓安全性サービス市場:国別

- ブラジル

- アルゼンチン

- UAE

- サウジアラビア

- 南アフリカ

- ナイジェリア

- LAMEAの残りの地域

- LAMEA心臓安全性サービス市場:国別

第8章 企業プロファイル

- Koninklijke Philips N.V

- Clario

- IQVIA Holdings, Inc.

- Laboratory Corporation of America Holdings

- Pharmaceutical Product Development, Inc.(Thermo Fisher Scientific)

- SGS S.A

- Banook Group

- Biotrial Research SAS

- Certara, Inc.

- Celerion

LIST OF TABLES

- TABLE 1 Global Cardiac Safety Services Market, 2018 - 2021, USD Million

- TABLE 2 Global Cardiac Safety Services Market, 2022 - 2028, USD Million

- TABLE 3 Partnerships, Collaborations and Agreements - Cardiac Safety Services Market

- TABLE 4 Product Launches And Product Expansions - Cardiac Safety Services Market

- TABLE 5 Acquisition and Mergers - Cardiac Safety Services Market

- TABLE 6 Geographical Expansion- Cardiac Safety Services Market

- TABLE 7 Global Cardiac Safety Services Market by Type, 2018 - 2021, USD Million

- TABLE 8 Global Cardiac Safety Services Market by Type, 2022 - 2028, USD Million

- TABLE 9 Global Integrated Market by Region, 2018 - 2021, USD Million

- TABLE 10 Global Integrated Market by Region, 2022 - 2028, USD Million

- TABLE 11 Global Standalone Market by Region, 2018 - 2021, USD Million

- TABLE 12 Global Standalone Market by Region, 2022 - 2028, USD Million

- TABLE 13 Global Cardiac Safety Services Market by End User, 2018 - 2021, USD Million

- TABLE 14 Global Cardiac Safety Services Market by End User, 2022 - 2028, USD Million

- TABLE 15 Global Pharmaceutical & Biopharmaceutical Companies Market by Region, 2018 - 2021, USD Million

- TABLE 16 Global Pharmaceutical & Biopharmaceutical Companies Market by Region, 2022 - 2028, USD Million

- TABLE 17 Global Contract Research Organizations Market by Region, 2018 - 2021, USD Million

- TABLE 18 Global Contract Research Organizations Market by Region, 2022 - 2028, USD Million

- TABLE 19 Global Cardiac Safety Services Market by Type of Service, 2018 - 2021, USD Million

- TABLE 20 Global Cardiac Safety Services Market by Type of Service, 2022 - 2028, USD Million

- TABLE 21 Global ECG/Holter Measurement Market by Region, 2018 - 2021, USD Million

- TABLE 22 Global ECG/Holter Measurement Market by Region, 2022 - 2028, USD Million

- TABLE 23 Global Blood Pressure Measurement Market by Region, 2018 - 2021, USD Million

- TABLE 24 Global Blood Pressure Measurement Market by Region, 2022 - 2028, USD Million

- TABLE 25 Global Cardiovascular Imaging Market by Region, 2018 - 2021, USD Million

- TABLE 26 Global Cardiovascular Imaging Market by Region, 2022 - 2028, USD Million

- TABLE 27 Global Thorough QT Studies Market by Region, 2018 - 2021, USD Million

- TABLE 28 Global Thorough QT Studies Market by Region, 2022 - 2028, USD Million

- TABLE 29 Global Others Market by Region, 2018 - 2021, USD Million

- TABLE 30 Global Others Market by Region, 2022 - 2028, USD Million

- TABLE 31 Global Cardiac Safety Services Market by Region, 2018 - 2021, USD Million

- TABLE 32 Global Cardiac Safety Services Market by Region, 2022 - 2028, USD Million

- TABLE 33 North America Cardiac Safety Services Market, 2018 - 2021, USD Million

- TABLE 34 North America Cardiac Safety Services Market, 2022 - 2028, USD Million

- TABLE 35 North America Cardiac Safety Services Market by Type, 2018 - 2021, USD Million

- TABLE 36 North America Cardiac Safety Services Market by Type, 2022 - 2028, USD Million

- TABLE 37 North America Integrated Market by Country, 2018 - 2021, USD Million

- TABLE 38 North America Integrated Market by Country, 2022 - 2028, USD Million

- TABLE 39 North America Standalone Market by Country, 2018 - 2021, USD Million

- TABLE 40 North America Standalone Market by Country, 2022 - 2028, USD Million

- TABLE 41 North America Cardiac Safety Services Market by End User, 2018 - 2021, USD Million

- TABLE 42 North America Cardiac Safety Services Market by End User, 2022 - 2028, USD Million

- TABLE 43 North America Pharmaceutical & Biopharmaceutical Companies Market by Country, 2018 - 2021, USD Million

- TABLE 44 North America Pharmaceutical & Biopharmaceutical Companies Market by Country, 2022 - 2028, USD Million

- TABLE 45 North America Contract Research Organizations Market by Country, 2018 - 2021, USD Million

- TABLE 46 North America Contract Research Organizations Market by Country, 2022 - 2028, USD Million

- TABLE 47 North America Cardiac Safety Services Market by Type of Service, 2018 - 2021, USD Million

- TABLE 48 North America Cardiac Safety Services Market by Type of Service, 2022 - 2028, USD Million

- TABLE 49 North America ECG/Holter Measurement Market by Country, 2018 - 2021, USD Million

- TABLE 50 North America ECG/Holter Measurement Market by Country, 2022 - 2028, USD Million

- TABLE 51 North America Blood Pressure Measurement Market by Country, 2018 - 2021, USD Million

- TABLE 52 North America Blood Pressure Measurement Market by Country, 2022 - 2028, USD Million

- TABLE 53 North America Cardiovascular Imaging Market by Country, 2018 - 2021, USD Million

- TABLE 54 North America Cardiovascular Imaging Market by Country, 2022 - 2028, USD Million

- TABLE 55 North America Thorough QT Studies Market by Country, 2018 - 2021, USD Million

- TABLE 56 North America Thorough QT Studies Market by Country, 2022 - 2028, USD Million

- TABLE 57 North America Others Market by Country, 2018 - 2021, USD Million

- TABLE 58 North America Others Market by Country, 2022 - 2028, USD Million

- TABLE 59 North America Cardiac Safety Services Market by Country, 2018 - 2021, USD Million

- TABLE 60 North America Cardiac Safety Services Market by Country, 2022 - 2028, USD Million

- TABLE 61 US Cardiac Safety Services Market, 2018 - 2021, USD Million

- TABLE 62 US Cardiac Safety Services Market, 2022 - 2028, USD Million

- TABLE 63 US Cardiac Safety Services Market by Type, 2018 - 2021, USD Million

- TABLE 64 US Cardiac Safety Services Market by Type, 2022 - 2028, USD Million

- TABLE 65 US Cardiac Safety Services Market by End User, 2018 - 2021, USD Million

- TABLE 66 US Cardiac Safety Services Market by End User, 2022 - 2028, USD Million

- TABLE 67 US Cardiac Safety Services Market by Type of Service, 2018 - 2021, USD Million

- TABLE 68 US Cardiac Safety Services Market by Type of Service, 2022 - 2028, USD Million

- TABLE 69 Canada Cardiac Safety Services Market, 2018 - 2021, USD Million

- TABLE 70 Canada Cardiac Safety Services Market, 2022 - 2028, USD Million

- TABLE 71 Canada Cardiac Safety Services Market by Type, 2018 - 2021, USD Million

- TABLE 72 Canada Cardiac Safety Services Market by Type, 2022 - 2028, USD Million

- TABLE 73 Canada Cardiac Safety Services Market by End User, 2018 - 2021, USD Million

- TABLE 74 Canada Cardiac Safety Services Market by End User, 2022 - 2028, USD Million

- TABLE 75 Canada Cardiac Safety Services Market by Type of Service, 2018 - 2021, USD Million

- TABLE 76 Canada Cardiac Safety Services Market by Type of Service, 2022 - 2028, USD Million

- TABLE 77 Mexico Cardiac Safety Services Market, 2018 - 2021, USD Million

- TABLE 78 Mexico Cardiac Safety Services Market, 2022 - 2028, USD Million

- TABLE 79 Mexico Cardiac Safety Services Market by Type, 2018 - 2021, USD Million

- TABLE 80 Mexico Cardiac Safety Services Market by Type, 2022 - 2028, USD Million

- TABLE 81 Mexico Cardiac Safety Services Market by End User, 2018 - 2021, USD Million

- TABLE 82 Mexico Cardiac Safety Services Market by End User, 2022 - 2028, USD Million

- TABLE 83 Mexico Cardiac Safety Services Market by Type of Service, 2018 - 2021, USD Million

- TABLE 84 Mexico Cardiac Safety Services Market by Type of Service, 2022 - 2028, USD Million

- TABLE 85 Rest of North America Cardiac Safety Services Market, 2018 - 2021, USD Million

- TABLE 86 Rest of North America Cardiac Safety Services Market, 2022 - 2028, USD Million

- TABLE 87 Rest of North America Cardiac Safety Services Market by Type, 2018 - 2021, USD Million

- TABLE 88 Rest of North America Cardiac Safety Services Market by Type, 2022 - 2028, USD Million

- TABLE 89 Rest of North America Cardiac Safety Services Market by End User, 2018 - 2021, USD Million

- TABLE 90 Rest of North America Cardiac Safety Services Market by End User, 2022 - 2028, USD Million

- TABLE 91 Rest of North America Cardiac Safety Services Market by Type of Service, 2018 - 2021, USD Million

- TABLE 92 Rest of North America Cardiac Safety Services Market by Type of Service, 2022 - 2028, USD Million

- TABLE 93 Europe Cardiac Safety Services Market, 2018 - 2021, USD Million

- TABLE 94 Europe Cardiac Safety Services Market, 2022 - 2028, USD Million

- TABLE 95 Europe Cardiac Safety Services Market by Type, 2018 - 2021, USD Million

- TABLE 96 Europe Cardiac Safety Services Market by Type, 2022 - 2028, USD Million

- TABLE 97 Europe Integrated Market by Country, 2018 - 2021, USD Million

- TABLE 98 Europe Integrated Market by Country, 2022 - 2028, USD Million

- TABLE 99 Europe Standalone Market by Country, 2018 - 2021, USD Million

- TABLE 100 Europe Standalone Market by Country, 2022 - 2028, USD Million

- TABLE 101 Europe Cardiac Safety Services Market by End User, 2018 - 2021, USD Million

- TABLE 102 Europe Cardiac Safety Services Market by End User, 2022 - 2028, USD Million

- TABLE 103 Europe Pharmaceutical & Biopharmaceutical Companies Market by Country, 2018 - 2021, USD Million

- TABLE 104 Europe Pharmaceutical & Biopharmaceutical Companies Market by Country, 2022 - 2028, USD Million

- TABLE 105 Europe Contract Research Organizations Market by Country, 2018 - 2021, USD Million

- TABLE 106 Europe Contract Research Organizations Market by Country, 2022 - 2028, USD Million

- TABLE 107 Europe Cardiac Safety Services Market by Type of Service, 2018 - 2021, USD Million

- TABLE 108 Europe Cardiac Safety Services Market by Type of Service, 2022 - 2028, USD Million

- TABLE 109 Europe ECG/Holter Measurement Market by Country, 2018 - 2021, USD Million

- TABLE 110 Europe ECG/Holter Measurement Market by Country, 2022 - 2028, USD Million

- TABLE 111 Europe Blood Pressure Measurement Market by Country, 2018 - 2021, USD Million

- TABLE 112 Europe Blood Pressure Measurement Market by Country, 2022 - 2028, USD Million

- TABLE 113 Europe Cardiovascular Imaging Market by Country, 2018 - 2021, USD Million

- TABLE 114 Europe Cardiovascular Imaging Market by Country, 2022 - 2028, USD Million

- TABLE 115 Europe Thorough QT Studies Market by Country, 2018 - 2021, USD Million

- TABLE 116 Europe Thorough QT Studies Market by Country, 2022 - 2028, USD Million

- TABLE 117 Europe Others Market by Country, 2018 - 2021, USD Million

- TABLE 118 Europe Others Market by Country, 2022 - 2028, USD Million

- TABLE 119 Europe Cardiac Safety Services Market by Country, 2018 - 2021, USD Million

- TABLE 120 Europe Cardiac Safety Services Market by Country, 2022 - 2028, USD Million

- TABLE 121 Germany Cardiac Safety Services Market, 2018 - 2021, USD Million

- TABLE 122 Germany Cardiac Safety Services Market, 2022 - 2028, USD Million

- TABLE 123 Germany Cardiac Safety Services Market by Type, 2018 - 2021, USD Million

- TABLE 124 Germany Cardiac Safety Services Market by Type, 2022 - 2028, USD Million

- TABLE 125 Germany Cardiac Safety Services Market by End User, 2018 - 2021, USD Million

- TABLE 126 Germany Cardiac Safety Services Market by End User, 2022 - 2028, USD Million

- TABLE 127 Germany Cardiac Safety Services Market by Type of Service, 2018 - 2021, USD Million

- TABLE 128 Germany Cardiac Safety Services Market by Type of Service, 2022 - 2028, USD Million

- TABLE 129 UK Cardiac Safety Services Market, 2018 - 2021, USD Million

- TABLE 130 UK Cardiac Safety Services Market, 2022 - 2028, USD Million

- TABLE 131 UK Cardiac Safety Services Market by Type, 2018 - 2021, USD Million

- TABLE 132 UK Cardiac Safety Services Market by Type, 2022 - 2028, USD Million

- TABLE 133 UK Cardiac Safety Services Market by End User, 2018 - 2021, USD Million

- TABLE 134 UK Cardiac Safety Services Market by End User, 2022 - 2028, USD Million

- TABLE 135 UK Cardiac Safety Services Market by Type of Service, 2018 - 2021, USD Million

- TABLE 136 UK Cardiac Safety Services Market by Type of Service, 2022 - 2028, USD Million

- TABLE 137 France Cardiac Safety Services Market, 2018 - 2021, USD Million

- TABLE 138 France Cardiac Safety Services Market, 2022 - 2028, USD Million

- TABLE 139 France Cardiac Safety Services Market by Type, 2018 - 2021, USD Million

- TABLE 140 France Cardiac Safety Services Market by Type, 2022 - 2028, USD Million

- TABLE 141 France Cardiac Safety Services Market by End User, 2018 - 2021, USD Million

- TABLE 142 France Cardiac Safety Services Market by End User, 2022 - 2028, USD Million

- TABLE 143 France Cardiac Safety Services Market by Type of Service, 2018 - 2021, USD Million

- TABLE 144 France Cardiac Safety Services Market by Type of Service, 2022 - 2028, USD Million

- TABLE 145 Russia Cardiac Safety Services Market, 2018 - 2021, USD Million

- TABLE 146 Russia Cardiac Safety Services Market, 2022 - 2028, USD Million

- TABLE 147 Russia Cardiac Safety Services Market by Type, 2018 - 2021, USD Million

- TABLE 148 Russia Cardiac Safety Services Market by Type, 2022 - 2028, USD Million

- TABLE 149 Russia Cardiac Safety Services Market by End User, 2018 - 2021, USD Million

- TABLE 150 Russia Cardiac Safety Services Market by End User, 2022 - 2028, USD Million

- TABLE 151 Russia Cardiac Safety Services Market by Type of Service, 2018 - 2021, USD Million

- TABLE 152 Russia Cardiac Safety Services Market by Type of Service, 2022 - 2028, USD Million

- TABLE 153 Spain Cardiac Safety Services Market, 2018 - 2021, USD Million

- TABLE 154 Spain Cardiac Safety Services Market, 2022 - 2028, USD Million

- TABLE 155 Spain Cardiac Safety Services Market by Type, 2018 - 2021, USD Million

- TABLE 156 Spain Cardiac Safety Services Market by Type, 2022 - 2028, USD Million

- TABLE 157 Spain Cardiac Safety Services Market by End User, 2018 - 2021, USD Million

- TABLE 158 Spain Cardiac Safety Services Market by End User, 2022 - 2028, USD Million

- TABLE 159 Spain Cardiac Safety Services Market by Type of Service, 2018 - 2021, USD Million

- TABLE 160 Spain Cardiac Safety Services Market by Type of Service, 2022 - 2028, USD Million

- TABLE 161 Italy Cardiac Safety Services Market, 2018 - 2021, USD Million

- TABLE 162 Italy Cardiac Safety Services Market, 2022 - 2028, USD Million

- TABLE 163 Italy Cardiac Safety Services Market by Type, 2018 - 2021, USD Million

- TABLE 164 Italy Cardiac Safety Services Market by Type, 2022 - 2028, USD Million

- TABLE 165 Italy Cardiac Safety Services Market by End User, 2018 - 2021, USD Million

- TABLE 166 Italy Cardiac Safety Services Market by End User, 2022 - 2028, USD Million

- TABLE 167 Italy Cardiac Safety Services Market by Type of Service, 2018 - 2021, USD Million

- TABLE 168 Italy Cardiac Safety Services Market by Type of Service, 2022 - 2028, USD Million

- TABLE 169 Rest of Europe Cardiac Safety Services Market, 2018 - 2021, USD Million

- TABLE 170 Rest of Europe Cardiac Safety Services Market, 2022 - 2028, USD Million

- TABLE 171 Rest of Europe Cardiac Safety Services Market by Type, 2018 - 2021, USD Million

- TABLE 172 Rest of Europe Cardiac Safety Services Market by Type, 2022 - 2028, USD Million

- TABLE 173 Rest of Europe Cardiac Safety Services Market by End User, 2018 - 2021, USD Million

- TABLE 174 Rest of Europe Cardiac Safety Services Market by End User, 2022 - 2028, USD Million

- TABLE 175 Rest of Europe Cardiac Safety Services Market by Type of Service, 2018 - 2021, USD Million

- TABLE 176 Rest of Europe Cardiac Safety Services Market by Type of Service, 2022 - 2028, USD Million

- TABLE 177 Asia Pacific Cardiac Safety Services Market, 2018 - 2021, USD Million

- TABLE 178 Asia Pacific Cardiac Safety Services Market, 2022 - 2028, USD Million

- TABLE 179 Asia Pacific Cardiac Safety Services Market by Type, 2018 - 2021, USD Million

- TABLE 180 Asia Pacific Cardiac Safety Services Market by Type, 2022 - 2028, USD Million

- TABLE 181 Asia Pacific Integrated Market by Country, 2018 - 2021, USD Million

- TABLE 182 Asia Pacific Integrated Market by Country, 2022 - 2028, USD Million

- TABLE 183 Asia Pacific Standalone Market by Country, 2018 - 2021, USD Million

- TABLE 184 Asia Pacific Standalone Market by Country, 2022 - 2028, USD Million

- TABLE 185 Asia Pacific Cardiac Safety Services Market by End User, 2018 - 2021, USD Million

- TABLE 186 Asia Pacific Cardiac Safety Services Market by End User, 2022 - 2028, USD Million

- TABLE 187 Asia Pacific Pharmaceutical & Biopharmaceutical Companies Market by Country, 2018 - 2021, USD Million

- TABLE 188 Asia Pacific Pharmaceutical & Biopharmaceutical Companies Market by Country, 2022 - 2028, USD Million

- TABLE 189 Asia Pacific Contract Research Organizations Market by Country, 2018 - 2021, USD Million

- TABLE 190 Asia Pacific Contract Research Organizations Market by Country, 2022 - 2028, USD Million

- TABLE 191 Asia Pacific Cardiac Safety Services Market by Type of Service, 2018 - 2021, USD Million

- TABLE 192 Asia Pacific Cardiac Safety Services Market by Type of Service, 2022 - 2028, USD Million

- TABLE 193 Asia Pacific ECG/Holter Measurement Market by Country, 2018 - 2021, USD Million

- TABLE 194 Asia Pacific ECG/Holter Measurement Market by Country, 2022 - 2028, USD Million

- TABLE 195 Asia Pacific Blood Pressure Measurement Market by Country, 2018 - 2021, USD Million

- TABLE 196 Asia Pacific Blood Pressure Measurement Market by Country, 2022 - 2028, USD Million

- TABLE 197 Asia Pacific Cardiovascular Imaging Market by Country, 2018 - 2021, USD Million

- TABLE 198 Asia Pacific Cardiovascular Imaging Market by Country, 2022 - 2028, USD Million

- TABLE 199 Asia Pacific Thorough QT Studies Market by Country, 2018 - 2021, USD Million

- TABLE 200 Asia Pacific Thorough QT Studies Market by Country, 2022 - 2028, USD Million

- TABLE 201 Asia Pacific Others Market by Country, 2018 - 2021, USD Million

- TABLE 202 Asia Pacific Others Market by Country, 2022 - 2028, USD Million

- TABLE 203 Asia Pacific Cardiac Safety Services Market by Country, 2018 - 2021, USD Million

- TABLE 204 Asia Pacific Cardiac Safety Services Market by Country, 2022 - 2028, USD Million

- TABLE 205 China Cardiac Safety Services Market, 2018 - 2021, USD Million

- TABLE 206 China Cardiac Safety Services Market, 2022 - 2028, USD Million

- TABLE 207 China Cardiac Safety Services Market by Type, 2018 - 2021, USD Million

- TABLE 208 China Cardiac Safety Services Market by Type, 2022 - 2028, USD Million

- TABLE 209 China Cardiac Safety Services Market by End User, 2018 - 2021, USD Million

- TABLE 210 China Cardiac Safety Services Market by End User, 2022 - 2028, USD Million

- TABLE 211 China Cardiac Safety Services Market by Type of Service, 2018 - 2021, USD Million

- TABLE 212 China Cardiac Safety Services Market by Type of Service, 2022 - 2028, USD Million

- TABLE 213 Japan Cardiac Safety Services Market, 2018 - 2021, USD Million

- TABLE 214 Japan Cardiac Safety Services Market, 2022 - 2028, USD Million

- TABLE 215 Japan Cardiac Safety Services Market by Type, 2018 - 2021, USD Million

- TABLE 216 Japan Cardiac Safety Services Market by Type, 2022 - 2028, USD Million

- TABLE 217 Japan Cardiac Safety Services Market by End User, 2018 - 2021, USD Million

- TABLE 218 Japan Cardiac Safety Services Market by End User, 2022 - 2028, USD Million

- TABLE 219 Japan Cardiac Safety Services Market by Type of Service, 2018 - 2021, USD Million

- TABLE 220 Japan Cardiac Safety Services Market by Type of Service, 2022 - 2028, USD Million

- TABLE 221 India Cardiac Safety Services Market, 2018 - 2021, USD Million

- TABLE 222 India Cardiac Safety Services Market, 2022 - 2028, USD Million

- TABLE 223 India Cardiac Safety Services Market by Type, 2018 - 2021, USD Million

- TABLE 224 India Cardiac Safety Services Market by Type, 2022 - 2028, USD Million

- TABLE 225 India Cardiac Safety Services Market by End User, 2018 - 2021, USD Million

- TABLE 226 India Cardiac Safety Services Market by End User, 2022 - 2028, USD Million

- TABLE 227 India Cardiac Safety Services Market by Type of Service, 2018 - 2021, USD Million

- TABLE 228 India Cardiac Safety Services Market by Type of Service, 2022 - 2028, USD Million

- TABLE 229 South Korea Cardiac Safety Services Market, 2018 - 2021, USD Million

- TABLE 230 South Korea Cardiac Safety Services Market, 2022 - 2028, USD Million

- TABLE 231 South Korea Cardiac Safety Services Market by Type, 2018 - 2021, USD Million

- TABLE 232 South Korea Cardiac Safety Services Market by Type, 2022 - 2028, USD Million

- TABLE 233 South Korea Cardiac Safety Services Market by End User, 2018 - 2021, USD Million

- TABLE 234 South Korea Cardiac Safety Services Market by End User, 2022 - 2028, USD Million

- TABLE 235 South Korea Cardiac Safety Services Market by Type of Service, 2018 - 2021, USD Million

- TABLE 236 South Korea Cardiac Safety Services Market by Type of Service, 2022 - 2028, USD Million

- TABLE 237 Singapore Cardiac Safety Services Market, 2018 - 2021, USD Million

- TABLE 238 Singapore Cardiac Safety Services Market, 2022 - 2028, USD Million

- TABLE 239 Singapore Cardiac Safety Services Market by Type, 2018 - 2021, USD Million

- TABLE 240 Singapore Cardiac Safety Services Market by Type, 2022 - 2028, USD Million

- TABLE 241 Singapore Cardiac Safety Services Market by End User, 2018 - 2021, USD Million

- TABLE 242 Singapore Cardiac Safety Services Market by End User, 2022 - 2028, USD Million

- TABLE 243 Singapore Cardiac Safety Services Market by Type of Service, 2018 - 2021, USD Million

- TABLE 244 Singapore Cardiac Safety Services Market by Type of Service, 2022 - 2028, USD Million

- TABLE 245 Malaysia Cardiac Safety Services Market, 2018 - 2021, USD Million

- TABLE 246 Malaysia Cardiac Safety Services Market, 2022 - 2028, USD Million

- TABLE 247 Malaysia Cardiac Safety Services Market by Type, 2018 - 2021, USD Million

- TABLE 248 Malaysia Cardiac Safety Services Market by Type, 2022 - 2028, USD Million

- TABLE 249 Malaysia Cardiac Safety Services Market by End User, 2018 - 2021, USD Million

- TABLE 250 Malaysia Cardiac Safety Services Market by End User, 2022 - 2028, USD Million

- TABLE 251 Malaysia Cardiac Safety Services Market by Type of Service, 2018 - 2021, USD Million

- TABLE 252 Malaysia Cardiac Safety Services Market by Type of Service, 2022 - 2028, USD Million

- TABLE 253 Rest of Asia Pacific Cardiac Safety Services Market, 2018 - 2021, USD Million

- TABLE 254 Rest of Asia Pacific Cardiac Safety Services Market, 2022 - 2028, USD Million

- TABLE 255 Rest of Asia Pacific Cardiac Safety Services Market by Type, 2018 - 2021, USD Million

- TABLE 256 Rest of Asia Pacific Cardiac Safety Services Market by Type, 2022 - 2028, USD Million

- TABLE 257 Rest of Asia Pacific Cardiac Safety Services Market by End User, 2018 - 2021, USD Million

- TABLE 258 Rest of Asia Pacific Cardiac Safety Services Market by End User, 2022 - 2028, USD Million

- TABLE 259 Rest of Asia Pacific Cardiac Safety Services Market by Type of Service, 2018 - 2021, USD Million

- TABLE 260 Rest of Asia Pacific Cardiac Safety Services Market by Type of Service, 2022 - 2028, USD Million

- TABLE 261 LAMEA Cardiac Safety Services Market, 2018 - 2021, USD Million

- TABLE 262 LAMEA Cardiac Safety Services Market, 2022 - 2028, USD Million

- TABLE 263 LAMEA Cardiac Safety Services Market by Type, 2018 - 2021, USD Million

- TABLE 264 LAMEA Cardiac Safety Services Market by Type, 2022 - 2028, USD Million

- TABLE 265 LAMEA Integrated Market by Country, 2018 - 2021, USD Million

- TABLE 266 LAMEA Integrated Market by Country, 2022 - 2028, USD Million

- TABLE 267 LAMEA Standalone Market by Country, 2018 - 2021, USD Million

- TABLE 268 LAMEA Standalone Market by Country, 2022 - 2028, USD Million

- TABLE 269 LAMEA Cardiac Safety Services Market by End User, 2018 - 2021, USD Million

- TABLE 270 LAMEA Cardiac Safety Services Market by End User, 2022 - 2028, USD Million

- TABLE 271 LAMEA Pharmaceutical & Biopharmaceutical Companies Market by Country, 2018 - 2021, USD Million

- TABLE 272 LAMEA Pharmaceutical & Biopharmaceutical Companies Market by Country, 2022 - 2028, USD Million

- TABLE 273 LAMEA Contract Research Organizations Market by Country, 2018 - 2021, USD Million

- TABLE 274 LAMEA Contract Research Organizations Market by Country, 2022 - 2028, USD Million

- TABLE 275 LAMEA Cardiac Safety Services Market by Type of Service, 2018 - 2021, USD Million

- TABLE 276 LAMEA Cardiac Safety Services Market by Type of Service, 2022 - 2028, USD Million

- TABLE 277 LAMEA ECG/Holter Measurement Market by Country, 2018 - 2021, USD Million

- TABLE 278 LAMEA ECG/Holter Measurement Market by Country, 2022 - 2028, USD Million

- TABLE 279 LAMEA Blood Pressure Measurement Market by Country, 2018 - 2021, USD Million

- TABLE 280 LAMEA Blood Pressure Measurement Market by Country, 2022 - 2028, USD Million

- TABLE 281 LAMEA Cardiovascular Imaging Market by Country, 2018 - 2021, USD Million

- TABLE 282 LAMEA Cardiovascular Imaging Market by Country, 2022 - 2028, USD Million

- TABLE 283 LAMEA Thorough QT Studies Market by Country, 2018 - 2021, USD Million

- TABLE 284 LAMEA Thorough QT Studies Market by Country, 2022 - 2028, USD Million

- TABLE 285 LAMEA Others Market by Country, 2018 - 2021, USD Million

- TABLE 286 LAMEA Others Market by Country, 2022 - 2028, USD Million

- TABLE 287 LAMEA Cardiac Safety Services Market by Country, 2018 - 2021, USD Million

- TABLE 288 LAMEA Cardiac Safety Services Market by Country, 2022 - 2028, USD Million

- TABLE 289 Brazil Cardiac Safety Services Market, 2018 - 2021, USD Million

- TABLE 290 Brazil Cardiac Safety Services Market, 2022 - 2028, USD Million

- TABLE 291 Brazil Cardiac Safety Services Market by Type, 2018 - 2021, USD Million

- TABLE 292 Brazil Cardiac Safety Services Market by Type, 2022 - 2028, USD Million

- TABLE 293 Brazil Cardiac Safety Services Market by End User, 2018 - 2021, USD Million

- TABLE 294 Brazil Cardiac Safety Services Market by End User, 2022 - 2028, USD Million

- TABLE 295 Brazil Cardiac Safety Services Market by Type of Service, 2018 - 2021, USD Million

- TABLE 296 Brazil Cardiac Safety Services Market by Type of Service, 2022 - 2028, USD Million

- TABLE 297 Argentina Cardiac Safety Services Market, 2018 - 2021, USD Million

- TABLE 298 Argentina Cardiac Safety Services Market, 2022 - 2028, USD Million

- TABLE 299 Argentina Cardiac Safety Services Market by Type, 2018 - 2021, USD Million

- TABLE 300 Argentina Cardiac Safety Services Market by Type, 2022 - 2028, USD Million

- TABLE 301 Argentina Cardiac Safety Services Market by End User, 2018 - 2021, USD Million

- TABLE 302 Argentina Cardiac Safety Services Market by End User, 2022 - 2028, USD Million

- TABLE 303 Argentina Cardiac Safety Services Market by Type of Service, 2018 - 2021, USD Million

- TABLE 304 Argentina Cardiac Safety Services Market by Type of Service, 2022 - 2028, USD Million

- TABLE 305 UAE Cardiac Safety Services Market, 2018 - 2021, USD Million

- TABLE 306 UAE Cardiac Safety Services Market, 2022 - 2028, USD Million

- TABLE 307 UAE Cardiac Safety Services Market by Type, 2018 - 2021, USD Million

- TABLE 308 UAE Cardiac Safety Services Market by Type, 2022 - 2028, USD Million

- TABLE 309 UAE Cardiac Safety Services Market by End User, 2018 - 2021, USD Million

- TABLE 310 UAE Cardiac Safety Services Market by End User, 2022 - 2028, USD Million

- TABLE 311 UAE Cardiac Safety Services Market by Type of Service, 2018 - 2021, USD Million

- TABLE 312 UAE Cardiac Safety Services Market by Type of Service, 2022 - 2028, USD Million

- TABLE 313 Saudi Arabia Cardiac Safety Services Market, 2018 - 2021, USD Million

- TABLE 314 Saudi Arabia Cardiac Safety Services Market, 2022 - 2028, USD Million

- TABLE 315 Saudi Arabia Cardiac Safety Services Market by Type, 2018 - 2021, USD Million

- TABLE 316 Saudi Arabia Cardiac Safety Services Market by Type, 2022 - 2028, USD Million

- TABLE 317 Saudi Arabia Cardiac Safety Services Market by End User, 2018 - 2021, USD Million

- TABLE 318 Saudi Arabia Cardiac Safety Services Market by End User, 2022 - 2028, USD Million

- TABLE 319 Saudi Arabia Cardiac Safety Services Market by Type of Service, 2018 - 2021, USD Million

- TABLE 320 Saudi Arabia Cardiac Safety Services Market by Type of Service, 2022 - 2028, USD Million

- TABLE 321 South Africa Cardiac Safety Services Market, 2018 - 2021, USD Million

- TABLE 322 South Africa Cardiac Safety Services Market, 2022 - 2028, USD Million

- TABLE 323 South Africa Cardiac Safety Services Market by Type, 2018 - 2021, USD Million

- TABLE 324 South Africa Cardiac Safety Services Market by Type, 2022 - 2028, USD Million

- TABLE 325 South Africa Cardiac Safety Services Market by End User, 2018 - 2021, USD Million

- TABLE 326 South Africa Cardiac Safety Services Market by End User, 2022 - 2028, USD Million

- TABLE 327 South Africa Cardiac Safety Services Market by Type of Service, 2018 - 2021, USD Million

- TABLE 328 South Africa Cardiac Safety Services Market by Type of Service, 2022 - 2028, USD Million

- TABLE 329 Nigeria Cardiac Safety Services Market, 2018 - 2021, USD Million

- TABLE 330 Nigeria Cardiac Safety Services Market, 2022 - 2028, USD Million

- TABLE 331 Nigeria Cardiac Safety Services Market by Type, 2018 - 2021, USD Million

- TABLE 332 Nigeria Cardiac Safety Services Market by Type, 2022 - 2028, USD Million

- TABLE 333 Nigeria Cardiac Safety Services Market by End User, 2018 - 2021, USD Million

- TABLE 334 Nigeria Cardiac Safety Services Market by End User, 2022 - 2028, USD Million

- TABLE 335 Nigeria Cardiac Safety Services Market by Type of Service, 2018 - 2021, USD Million

- TABLE 336 Nigeria Cardiac Safety Services Market by Type of Service, 2022 - 2028, USD Million

- TABLE 337 Rest of LAMEA Cardiac Safety Services Market, 2018 - 2021, USD Million

- TABLE 338 Rest of LAMEA Cardiac Safety Services Market, 2022 - 2028, USD Million

- TABLE 339 Rest of LAMEA Cardiac Safety Services Market by Type, 2018 - 2021, USD Million

- TABLE 340 Rest of LAMEA Cardiac Safety Services Market by Type, 2022 - 2028, USD Million

- TABLE 341 Rest of LAMEA Cardiac Safety Services Market by End User, 2018 - 2021, USD Million

- TABLE 342 Rest of LAMEA Cardiac Safety Services Market by End User, 2022 - 2028, USD Million

- TABLE 343 Rest of LAMEA Cardiac Safety Services Market by Type of Service, 2018 - 2021, USD Million

- TABLE 344 Rest of LAMEA Cardiac Safety Services Market by Type of Service, 2022 - 2028, USD Million

- TABLE 345 Key Information - Koninklijke Philips N.V.

- TABLE 346 key information - Clario

- TABLE 347 Key information - IQVIA Holdings, Inc.

- TABLE 348 Key Information - Laboratory Corporation of America holdings

- TABLE 349 key information - Pharmaceutical Product Development, Inc.

- TABLE 350 Key Information - SGS S.A.

- TABLE 351 Key Information - Banook Group

- TABLE 352 Key Information - Biotrial Research SAS

- TABLE 353 Key Information - Certara, Inc.

- TABLE 354 Key Information - Celerion

List of Figures

- FIG 1 Methodology for the research

- FIG 2 KBV Cardinal Matrix

- FIG 3 Key Leading Strategies: Percentage Distribution (2018-2022)

- FIG 4 Global Cardiac Safety Services Market share by Type, 2021

- FIG 5 Global Cardiac Safety Services Market share by Type, 2028

- FIG 6 Global Cardiac Safety Services Market by Type, 2018 - 2028, USD Million

- FIG 7 Global Cardiac Safety Services Market share by End User, 2021

- FIG 8 Global Cardiac Safety Services Market share by End User, 2028

- FIG 9 Global Cardiac Safety Services Market by End User, 2018 - 2028, USD Million

- FIG 10 Global Cardiac Safety Services Market share by Type of Service, 2021

- FIG 11 Global Cardiac Safety Services Market share by Type of Service, 2028

- FIG 12 Global Cardiac Safety Services Market by Type of Service, 2018 - 2028, USD Million

- FIG 13 Global Cardiac Safety Services Market share by Region, 2021

- FIG 14 Global Cardiac Safety Services Market share by Region, 2028

- FIG 15 Global Cardiac Safety Services Market by Region, 2018 - 2028, USD Million

- FIG 16 Recent strategies and developments: Koninklijke Philips N.V.

The Global Cardiac Safety Services Market size is expected to reach $1.1 billion by 2028, rising at a market growth of 11.1% CAGR during the forecast period.

Cardiac safety services assist and design clinical studies & trials and other research necessary for the monitoring of heart safety. These are primarily concerned with tracking the full cardiac safety profile through all clinical trial phases, from Phase I through Phase IV. Guidelines and regulations given by most major and recognized medical authorities of various countries and other regulating agencies are followed while developing cardiac safety clinical trials and studies.

These services include physiologic stress testing, non-invasive cardiac imaging, platelet aggregation, ambulatory blood pressure monitoring, and other services in addition to the QT tests. Due to the grouping of services with an emphasis on end-to-end development, integrated services that provide cardiac safety services are generally favored over standalone services because of the peculiarity of standalone services.

All elements of the cardiovascular system, including the heart, blood vessels, and blood constituents, are affected by cardiovascular safety liabilities, which include both cardiovascular and non-cardiovascular pharmaceuticals. Cardiovascular adverse effects can be functional or structural (such as histopathology) in nature and can happen after acute or chronic treatment.

The need for effective yet secure drug development is more critical than ever in a time of growing public scrutiny, rising business expenses, and limited resources at regulatory agencies. With 17.9 million deaths per year, cardiovascular diseases (CVDs) are the most common cause of death worldwide. Cerebrovascular disease, coronary heart disease, rheumatic heart disease, and other illnesses are among the category of heart and blood vessel disorders known as CVDs.

COVID-19 Impact Analysis

This prompted the pharmaceutical and health insurance industries to make the necessary changes to their offerings in order to include better provisions and facilities. In order to progress the evolution of medicine, this compelled the engagement of numerous research institutions and organizations dedicated to heart health. Coronavirus-related catastrophes caused a significant number of patients with pre-existing unfavorable disorders to succumb to them, which had an effect on cardiac safety services. As a result of COVID-19's vigorous promotion of its development, the market for cardiac safety services was positively affected overall.

Market Growth Factors

Increase In Research For Biosimilars And Biologics

Numerous businesses are making significant investments in the creation of biologics and biosimilar compounds. In the discovery stage, biologics such peptides, proteins, and monoclonal antibodies make up more than half of the therapeutic candidates. Pharmaceutical and biopharmaceutical businesses are heavily putting money into their research and development as novel biologics are being developed or are in the pipeline. Biosimilars are also less expensive because, being generic versions of patented biologic medications, they are not subject to the same strict regulatory standards.

High Prevalence Of Ech Holter Service Among The General Population

The rise in the number of elderly people and the increasing incidence of cardiovascular disorders are mostly to blame for the ECG Holter's expansion. According to data released by Health System Tracker, heart disease is the top cause of mortality in the United States. These reasons make immediate heartbeat detection and constant heart rate monitoring equipment necessary. In the past few years, the healthcare system has employed ECG monitoring devices to look for any abnormalities in cardiac activity.

Market Restraining Factors

Lack Of Qualified Personnel For Clinical Trials

The R&D outsourcing industry for pharmaceuticals, biotechnology, and medical devices is always changing. To deliver high-quality services, adhere to acceptable laboratory procedures, and keep up with the ongoing developments in medical device and pharmaceutical R&D technologies and techniques, highly skilled experts are needed. As they compete for trained and experienced scientists with biotechnology, pharmaceutical, and medical device businesses as well as research and academic organizations, CROs confront difficulties in attracting and keeping highly skilled personnel.

Type Outlook

Based on type, the cardiac safety services market is bifurcated into integrated and standalone. The integrated segment dominated the cardiac safety services market with the highest revenue share in 2021. These cutting-edge core lab services provide a full range of cardiac safety services, including imaging, TQT, and profile QT tests. In order to help with the real-time evaluation of heart rate and rhythm, they also keep an eye on off-target cardiovascular liabilities and conduct onsite multichannel telemetry under the supervision of licensed nurses.

Type of Service Outlook

On the basis of type of service, the cardiac safety services market is divided into ECG/Holter measurement, blood pressure measurement, cardiovascular imaging, thorough QT studies, and other services. The ECG/Holter measurement segment witnessed the largest revenue share in the cardiac safety services market in 2021. Smartwatches and other personal electronics provide electrocardiogram monitoring. A small, portable gadget called a Holter monitor is used to capture heartbeats. It is employed to identify and evaluate the likelihood of aberrant heartbeats (arrhythmias).

End User Outlook

Based on end user, the cardiac safety services market is categorized into pharmaceutical & biopharmaceutical companies and contract research organizations. The contract research organizations segment procured a substantial revenue share in the cardiac safety services market in 2021. Clinical trials are carried out by Contract Research Organizations (CROs) for the pharmaceutical, medical device, and biotechnology businesses as well as for academic institutions, governmental agencies, and foundations.

Regional Outlook

On the basis of region, the cardiac safety devices is analyzed across North America, Europe, Asia Pacific, and LAMEA. The North America region acquired the highest revenue share in the cardiac safety services market in 2021. This is due to the region's growing number of clinical studies, which are fueling demands for cardiac safety services. The rising number of people suffering from cardiovascular diseases (CVD) and coronary heart disease (CHD) have accelerated the drug development and research studies in the region.

The major strategies followed by the market participants are Acquisitions. Based on the Analysis presented in the Cardinal matrix; Pharmaceutical Product Development, Inc. is the major forerunner in the Cardiac Safety Services Market. Companies such as Koninklijke Philips N.V., Laboratory Corporation of America Holdings, IQVIA Holdings, Inc. are some of the key innovators in Cardiac Safety Services Market.

The market research report covers the analysis of key stake holders of the market. Key companies profiled in the report include Koninklijke Philips N.V., Clario, IQVIA Holdings, Inc., Laboratory Corporation of America Holdings, Pharmaceutical Product Development, Inc., SGS S.A., Banook Group, Biotrial Research SAS, Certara, Inc., and Celerion.

Strategies deployed in Cardiac Safety Services Market

Aug-2022: Labcorp acquired RWJBarnabas Health, a network of independent healthcare providers in New Jersey. Through this acquisition, Labcorp planned to offer expanded health plan coverage, enhanced service to rural markets, and the potential for reduced out-of-pocket lab costs for patients.

Jun-2022: The Banook Group expanded its geographical footprint by opening its first US office in Boston, Massachusetts. Through this expansion, Banook aimed to reduce the constraints of time zones and to provide enhanced technical and logistics support to its customers as about 40% of Banook's customers are based in this region. The expansion also allowed the company to offer local support to its 70 current US customers and to grow in the North American market.

Apr-2022: Royal Philips, partnered with Prisma Health, South Carolina's largest non-profit healthcare system. Through this partnership, the companies agreed to help the health system achieve enterprise interoperability, standardize patient monitoring, and drive innovation in enterprise imaging solutions to enhance patient care and improve clinical performance.

Mar-2022: IQVIA unveiled OCE+, the first of several new advancements to its leading life science customer engagement platform. OCE+ adds IQVIA's Next Best recommendation engine to its Orchestrated Customer Engagement (OCE) platform, providing enhanced HCP experiences, improved productivity, and increased ROI. The product uses IQVIA's industry-leading data and advanced analytics to deliver AI-driven recommendations directly into the daily workflows of life sciences commercial teams.

Jan-2022: Clario partnered with ActiGraph, a pioneer and leading provider of activity-sensing wearable technology. From this partnership, Clario expanded its evidence generation platform and portfolio of decentralization technologies and offered ActiGraph technologies to its customers in addition to its suite of eCOA, Precision Motion, Cardiac Safety, Respiratory, Medical Imaging, and Trial Enablement solutions. The partnership also helped clinical trial sites and sponsors to drive up efficiency and accuracy while increasing convenience for study participants.

Dec-2021: Labcorp took over Personal Genome Diagnostics (PGDx), a provider of comprehensive liquid biopsy and tissue-based genomic products and services. From this acquisition, Labcorp aimed to strengthen its next-generation sequencing-based genomic profiling capabilities and accelerate the existing liquid biopsy capabilities.

Nov-2021: Royal Philips acquired Cardiologs, a French medical technology firm. From this acquisition, Royal Philips aimed at expanding its cardiac monitoring and diagnostics portfolio with innovative software technology, electrocardiogram (ECG) analysis, and reporting services.

Sep-2021: The Banook Group acquired Nabios, biotech with strong expertise in cardiac safety assessments in clinical trials of drugs intended for human health. Through this acquisition, the company advanced its steps towards becoming the leader in the cardiac safety market by offering a strong European alternative to those companies operating from North America or India. This acquisition also granted Banook's customers access to new and more competitive services.

Sep-2021: IQVIA collaborated with HealthCore, a leading real-world research organization in the United States. Under the collaboration, the companies focused on advancing real-world evidence (RWE) studies with increased quality and efficiency. The innovative research collaboration focused specifically on real-world studies such as external comparators, pragmatic trials, and enriched studies.

Mar-2021: Certara took over AUTHOR!, a provider of medical writing and statistical analysis of clinical trial data to global pharmaceutical and biotechnology companies. Through this acquisition, Certara enhanced the existing regulatory and biostatistical expertise and helped to fuel the company's strategic expansion in Europe. Additionally, from the acquisition, Certara leveraged AUTHOR!'s seasoned team to provide technology-enabled capabilities to its customers and thus help global clients expertly navigate and accelerate the drug development and regulatory approval process.

Feb-2021: Royal Philips took over BioTelemetry, a leading U.S.-based provider of remote cardiac diagnostics and monitoring. Through this acquisition, Royal Philips expanded its cardiac care portfolio, and its strategy to transform the delivery of care along the health continuum with integrated solutions.

Feb-2021: Philips formed a partnership with SAZ hospital network, a Dutch Hospital network comprising 28 hospitals. Under this partnership, Philips offered advanced patient monitoring and population health management solutions to the SAZ network hospitals. In addition, Philips solutions enabled SAZ to enhance monitoring, observation, and self-management of patients across the care journey, both inside and outside the hospitals.

Mar-2018: Certara introduced Quantitative Systems Pharmacology (QSP) Immuno-oncology Simulator Consortium. The product combines computational modeling and experimental methods to examine the mechanistic relationships between a drug, the biological system, and the disease process. In addition, QSP integrates quantitative drug data with the knowledge of the drug's mechanism of action.

Scope of the Study

Market Segments covered in the Report:

By Type

- Integrated

- Standalone

By End User

- Pharmaceutical & Biopharmaceutical Companies

- Contract Research Organizations

By Type of Service

- ECG/Holter Measurement

- Blood Pressure Measurement

- Cardiovascular Imaging

- Thorough QT Studies

- Others

By Geography

- North America

- US

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- UK

- France

- Russia

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Singapore

- Malaysia

- Rest of Asia Pacific

- LAMEA

- Brazil

- Argentina

- UAE

- Saudi Arabia

- South Africa

- Nigeria

- Rest of LAMEA

Companies Profiled

- Koninklijke Philips N.V.

- Clario

- IQVIA Holdings, Inc.

- Laboratory Corporation of America Holdings

- Pharmaceutical Product Development, Inc.

- SGS S.A.

- Banook Group

- Biotrial Research SAS

- Certara, Inc.

- Celerion

Unique Offerings from KBV Research

- Exhaustive coverage

- Highest number of market tables and figures

- Subscription based model available

- Guaranteed best price

- Assured post sales research support with 10% customization free

Table of Contents

Chapter 1. Market Scope & Methodology

- 1.1 Market Definition

- 1.2 Objectives

- 1.3 Market Scope

- 1.4 Segmentation

- 1.4.1 Global Cardiac Safety Services Market, by Type

- 1.4.2 Global Cardiac Safety Services Market, by End User

- 1.4.3 Global Cardiac Safety Services Market, by Type of Service

- 1.4.4 Global Cardiac Safety Services Market, by Geography

- 1.5 Methodology for the research

Chapter 2. Market Overview

- 2.1 Introduction

- 2.1.1 Overview

- 2.1.1.1 Market Composition and Scenario

- 2.1.1 Overview

- 2.2 Key Factors Impacting the Market

- 2.2.1 Market Drivers

- 2.2.2 Market Restraints

Chapter 3. Competition Analysis - Global

- 3.1 KBV Cardinal Matrix

- 3.2 Recent Industry Wide Strategic Developments

- 3.2.1 Partnerships, Collaborations and Agreements

- 3.2.2 Product Launches and Product Expansions

- 3.2.3 Acquisition and Mergers

- 3.2.4 Geographical Expansion

- 3.3 Top Winning Strategies

- 3.3.1 Key Leading Strategies: Percentage Distribution (2018-2022)

Chapter 4. Global Cardiac Safety Services Market by Type

- 4.1 Global Integrated Market by Region

- 4.2 Global Standalone Market by Region

Chapter 5. Global Cardiac Safety Services Market by End User

- 5.1 Global Pharmaceutical & Biopharmaceutical Companies Market by Region

- 5.2 Global Contract Research Organizations Market by Region

Chapter 6. Global Cardiac Safety Services Market by Type of Service

- 6.1 Global ECG/Holter Measurement Market by Region

- 6.2 Global Blood Pressure Measurement Market by Region

- 6.3 Global Cardiovascular Imaging Market by Region

- 6.4 Global Thorough QT Studies Market by Region

- 6.5 Global Others Market by Region

Chapter 7. Global Cardiac Safety Services Market by Region

- 7.1 North America Cardiac Safety Services Market

- 7.1.1 North America Cardiac Safety Services Market by Type

- 7.1.1.1 North America Integrated Market by Country

- 7.1.1.2 North America Standalone Market by Country

- 7.1.2 North America Cardiac Safety Services Market by End User

- 7.1.2.1 North America Pharmaceutical & Biopharmaceutical Companies Market by Country

- 7.1.2.2 North America Contract Research Organizations Market by Country

- 7.1.3 North America Cardiac Safety Services Market by Type of Service

- 7.1.3.1 North America ECG/Holter Measurement Market by Country

- 7.1.3.2 North America Blood Pressure Measurement Market by Country

- 7.1.3.3 North America Cardiovascular Imaging Market by Country

- 7.1.3.4 North America Thorough QT Studies Market by Country

- 7.1.3.5 North America Others Market by Country

- 7.1.4 North America Cardiac Safety Services Market by Country

- 7.1.4.1 US Cardiac Safety Services Market

- 7.1.4.1.1 US Cardiac Safety Services Market by Type

- 7.1.4.1.2 US Cardiac Safety Services Market by End User

- 7.1.4.1.3 US Cardiac Safety Services Market by Type of Service

- 7.1.4.2 Canada Cardiac Safety Services Market

- 7.1.4.2.1 Canada Cardiac Safety Services Market by Type

- 7.1.4.2.2 Canada Cardiac Safety Services Market by End User

- 7.1.4.2.3 Canada Cardiac Safety Services Market by Type of Service

- 7.1.4.3 Mexico Cardiac Safety Services Market

- 7.1.4.3.1 Mexico Cardiac Safety Services Market by Type

- 7.1.4.3.2 Mexico Cardiac Safety Services Market by End User

- 7.1.4.3.3 Mexico Cardiac Safety Services Market by Type of Service

- 7.1.4.4 Rest of North America Cardiac Safety Services Market

- 7.1.4.4.1 Rest of North America Cardiac Safety Services Market by Type

- 7.1.4.4.2 Rest of North America Cardiac Safety Services Market by End User

- 7.1.4.4.3 Rest of North America Cardiac Safety Services Market by Type of Service

- 7.1.4.1 US Cardiac Safety Services Market

- 7.1.1 North America Cardiac Safety Services Market by Type

- 7.2 Europe Cardiac Safety Services Market

- 7.2.1 Europe Cardiac Safety Services Market by Type

- 7.2.1.1 Europe Integrated Market by Country

- 7.2.1.2 Europe Standalone Market by Country

- 7.2.2 Europe Cardiac Safety Services Market by End User

- 7.2.2.1 Europe Pharmaceutical & Biopharmaceutical Companies Market by Country

- 7.2.2.2 Europe Contract Research Organizations Market by Country

- 7.2.3 Europe Cardiac Safety Services Market by Type of Service

- 7.2.3.1 Europe ECG/Holter Measurement Market by Country

- 7.2.3.2 Europe Blood Pressure Measurement Market by Country

- 7.2.3.3 Europe Cardiovascular Imaging Market by Country

- 7.2.3.4 Europe Thorough QT Studies Market by Country

- 7.2.3.5 Europe Others Market by Country

- 7.2.4 Europe Cardiac Safety Services Market by Country

- 7.2.4.1 Germany Cardiac Safety Services Market

- 7.2.4.1.1 Germany Cardiac Safety Services Market by Type

- 7.2.4.1.2 Germany Cardiac Safety Services Market by End User

- 7.2.4.1.3 Germany Cardiac Safety Services Market by Type of Service

- 7.2.4.2 UK Cardiac Safety Services Market

- 7.2.4.2.1 UK Cardiac Safety Services Market by Type

- 7.2.4.2.2 UK Cardiac Safety Services Market by End User

- 7.2.4.2.3 UK Cardiac Safety Services Market by Type of Service

- 7.2.4.3 France Cardiac Safety Services Market

- 7.2.4.3.1 France Cardiac Safety Services Market by Type

- 7.2.4.3.2 France Cardiac Safety Services Market by End User

- 7.2.4.3.3 France Cardiac Safety Services Market by Type of Service

- 7.2.4.4 Russia Cardiac Safety Services Market

- 7.2.4.4.1 Russia Cardiac Safety Services Market by Type

- 7.2.4.4.2 Russia Cardiac Safety Services Market by End User

- 7.2.4.4.3 Russia Cardiac Safety Services Market by Type of Service

- 7.2.4.5 Spain Cardiac Safety Services Market

- 7.2.4.5.1 Spain Cardiac Safety Services Market by Type

- 7.2.4.5.2 Spain Cardiac Safety Services Market by End User

- 7.2.4.5.3 Spain Cardiac Safety Services Market by Type of Service

- 7.2.4.6 Italy Cardiac Safety Services Market

- 7.2.4.6.1 Italy Cardiac Safety Services Market by Type

- 7.2.4.6.2 Italy Cardiac Safety Services Market by End User

- 7.2.4.6.3 Italy Cardiac Safety Services Market by Type of Service

- 7.2.4.7 Rest of Europe Cardiac Safety Services Market

- 7.2.4.7.1 Rest of Europe Cardiac Safety Services Market by Type

- 7.2.4.7.2 Rest of Europe Cardiac Safety Services Market by End User

- 7.2.4.7.3 Rest of Europe Cardiac Safety Services Market by Type of Service

- 7.2.4.1 Germany Cardiac Safety Services Market

- 7.2.1 Europe Cardiac Safety Services Market by Type

- 7.3 Asia Pacific Cardiac Safety Services Market

- 7.3.1 Asia Pacific Cardiac Safety Services Market by Type

- 7.3.1.1 Asia Pacific Integrated Market by Country

- 7.3.1.2 Asia Pacific Standalone Market by Country

- 7.3.2 Asia Pacific Cardiac Safety Services Market by End User

- 7.3.2.1 Asia Pacific Pharmaceutical & Biopharmaceutical Companies Market by Country

- 7.3.2.2 Asia Pacific Contract Research Organizations Market by Country

- 7.3.3 Asia Pacific Cardiac Safety Services Market by Type of Service

- 7.3.3.1 Asia Pacific ECG/Holter Measurement Market by Country

- 7.3.3.2 Asia Pacific Blood Pressure Measurement Market by Country

- 7.3.3.3 Asia Pacific Cardiovascular Imaging Market by Country

- 7.3.3.4 Asia Pacific Thorough QT Studies Market by Country

- 7.3.3.5 Asia Pacific Others Market by Country

- 7.3.4 Asia Pacific Cardiac Safety Services Market by Country

- 7.3.4.1 China Cardiac Safety Services Market

- 7.3.4.1.1 China Cardiac Safety Services Market by Type

- 7.3.4.1.2 China Cardiac Safety Services Market by End User

- 7.3.4.1.3 China Cardiac Safety Services Market by Type of Service

- 7.3.4.2 Japan Cardiac Safety Services Market

- 7.3.4.2.1 Japan Cardiac Safety Services Market by Type

- 7.3.4.2.2 Japan Cardiac Safety Services Market by End User

- 7.3.4.2.3 Japan Cardiac Safety Services Market by Type of Service

- 7.3.4.3 India Cardiac Safety Services Market

- 7.3.4.3.1 India Cardiac Safety Services Market by Type

- 7.3.4.3.2 India Cardiac Safety Services Market by End User

- 7.3.4.3.3 India Cardiac Safety Services Market by Type of Service

- 7.3.4.4 South Korea Cardiac Safety Services Market

- 7.3.4.4.1 South Korea Cardiac Safety Services Market by Type

- 7.3.4.4.2 South Korea Cardiac Safety Services Market by End User

- 7.3.4.4.3 South Korea Cardiac Safety Services Market by Type of Service

- 7.3.4.5 Singapore Cardiac Safety Services Market

- 7.3.4.5.1 Singapore Cardiac Safety Services Market by Type

- 7.3.4.5.2 Singapore Cardiac Safety Services Market by End User

- 7.3.4.5.3 Singapore Cardiac Safety Services Market by Type of Service

- 7.3.4.6 Malaysia Cardiac Safety Services Market

- 7.3.4.6.1 Malaysia Cardiac Safety Services Market by Type

- 7.3.4.6.2 Malaysia Cardiac Safety Services Market by End User

- 7.3.4.6.3 Malaysia Cardiac Safety Services Market by Type of Service

- 7.3.4.7 Rest of Asia Pacific Cardiac Safety Services Market

- 7.3.4.7.1 Rest of Asia Pacific Cardiac Safety Services Market by Type

- 7.3.4.7.2 Rest of Asia Pacific Cardiac Safety Services Market by End User

- 7.3.4.7.3 Rest of Asia Pacific Cardiac Safety Services Market by Type of Service

- 7.3.4.1 China Cardiac Safety Services Market

- 7.3.1 Asia Pacific Cardiac Safety Services Market by Type

- 7.4 LAMEA Cardiac Safety Services Market

- 7.4.1 LAMEA Cardiac Safety Services Market by Type

- 7.4.1.1 LAMEA Integrated Market by Country

- 7.4.1.2 LAMEA Standalone Market by Country

- 7.4.2 LAMEA Cardiac Safety Services Market by End User

- 7.4.2.1 LAMEA Pharmaceutical & Biopharmaceutical Companies Market by Country

- 7.4.2.2 LAMEA Contract Research Organizations Market by Country

- 7.4.3 LAMEA Cardiac Safety Services Market by Type of Service

- 7.4.3.1 LAMEA ECG/Holter Measurement Market by Country

- 7.4.3.2 LAMEA Blood Pressure Measurement Market by Country

- 7.4.3.3 LAMEA Cardiovascular Imaging Market by Country

- 7.4.3.4 LAMEA Thorough QT Studies Market by Country

- 7.4.3.5 LAMEA Others Market by Country

- 7.4.4 LAMEA Cardiac Safety Services Market by Country

- 7.4.4.1 Brazil Cardiac Safety Services Market

- 7.4.4.1.1 Brazil Cardiac Safety Services Market by Type

- 7.4.4.1.2 Brazil Cardiac Safety Services Market by End User

- 7.4.4.1.3 Brazil Cardiac Safety Services Market by Type of Service

- 7.4.4.2 Argentina Cardiac Safety Services Market

- 7.4.4.2.1 Argentina Cardiac Safety Services Market by Type

- 7.4.4.2.2 Argentina Cardiac Safety Services Market by End User

- 7.4.4.2.3 Argentina Cardiac Safety Services Market by Type of Service

- 7.4.4.3 UAE Cardiac Safety Services Market

- 7.4.4.3.1 UAE Cardiac Safety Services Market by Type

- 7.4.4.3.2 UAE Cardiac Safety Services Market by End User

- 7.4.4.3.3 UAE Cardiac Safety Services Market by Type of Service

- 7.4.4.4 Saudi Arabia Cardiac Safety Services Market

- 7.4.4.4.1 Saudi Arabia Cardiac Safety Services Market by Type

- 7.4.4.4.2 Saudi Arabia Cardiac Safety Services Market by End User

- 7.4.4.4.3 Saudi Arabia Cardiac Safety Services Market by Type of Service

- 7.4.4.5 South Africa Cardiac Safety Services Market

- 7.4.4.5.1 South Africa Cardiac Safety Services Market by Type

- 7.4.4.5.2 South Africa Cardiac Safety Services Market by End User

- 7.4.4.5.3 South Africa Cardiac Safety Services Market by Type of Service

- 7.4.4.6 Nigeria Cardiac Safety Services Market

- 7.4.4.6.1 Nigeria Cardiac Safety Services Market by Type

- 7.4.4.6.2 Nigeria Cardiac Safety Services Market by End User

- 7.4.4.6.3 Nigeria Cardiac Safety Services Market by Type of Service

- 7.4.4.7 Rest of LAMEA Cardiac Safety Services Market

- 7.4.4.7.1 Rest of LAMEA Cardiac Safety Services Market by Type

- 7.4.4.7.2 Rest of LAMEA Cardiac Safety Services Market by End User

- 7.4.4.7.3 Rest of LAMEA Cardiac Safety Services Market by Type of Service

- 7.4.4.1 Brazil Cardiac Safety Services Market

- 7.4.1 LAMEA Cardiac Safety Services Market by Type

Chapter 8. Company Profiles

- 8.1 Koninklijke Philips N.V.

- 8.1.1 Company Overview

- 8.1.2 Financial Analysis

- 8.1.3 Segmental and Regional Analysis

- 8.1.4 Research & Development Expense

- 8.1.5 Recent strategies and developments:

- 8.1.5.1 Partnerships, Collaborations, and Agreements:

- 8.1.5.2 Acquisition and Mergers:

- 8.2 Clario

- 8.2.1 Company Overview

- 8.2.2 Recent strategies and developments:

- 8.2.2.1 Partnerships, Collaborations, and Agreements:

- 8.3 IQVIA Holdings, Inc.

- 8.3.1 Company Overview

- 8.3.2 Financial Analysis

- 8.3.3 Segmental and Regional Analysis

- 8.3.4 Recent strategies and developments:

- 8.3.4.1 Partnerships, Collaborations, and Agreements:

- 8.3.4.2 Product Launches and Product Expansions:

- 8.4 Laboratory Corporation of America Holdings

- 8.4.1 Company Overview

- 8.4.2 Financial Analysis

- 8.4.3 Segmental and Regional Analysis

- 8.4.4 Recent strategies and developments:

- 8.4.4.1 Acquisition and Mergers:

- 8.5 Pharmaceutical Product Development, Inc. (Thermo Fisher Scientific)

- 8.5.1 Company Overview

- 8.5.2 Financial Analysis

- 8.5.3 Segmental and Regional Analysis

- 8.5.4 Research & Development Expenses

- 8.6 SGS S.A.

- 8.6.1 Company Overview

- 8.6.2 Financial Analysis

- 8.6.3 Segmental and Regional Analysis

- 8.7 Banook Group

- 8.7.1 Company Overview

- 8.7.2 Recent strategies and developments:

- 8.7.2.1 Acquisition and Mergers:

- 8.7.2.2 Geographical Expansions:

- 8.8 Biotrial Research SAS

- 8.8.1 Company Overview

- 8.9 Certara, Inc.

- 8.9.1 Company Overview

- 8.9.2 Financial Analysis

- 8.9.3 Regional Analysis

- 8.9.4 Research & Development Expenses

- 8.9.5 Recent strategies and developments:

- 8.9.5.1 Product Launches and Product Expansions:

- 8.9.5.2 Acquisition and Mergers:

- 8.10. Celerion

- 8.10.1 Company Overview