|

市場調査レポート

商品コード

1269624

水素燃料電池乗用車の世界市場、2023年Global Market for Hydrogen Fuel Cell Passenger Vehicles, 2023 |

||||||

|

|||||||

| 水素燃料電池乗用車の世界市場、2023年 |

|

出版日: 2023年05月10日

発行: Information Trends, LLC

ページ情報: 英文 232 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

2022年末までに世界で6万台近くの水素燃料電池乗用車が販売されました。このうち3万台以上が2021年と2022年の過去2年間に販売されており、今後の大きな伸びが見込まれています。アジア太平洋と欧州では、導入のスピードが加速しています。米国では、カリフォルニア州を除いて、特に連邦レベルでの対策が不十分なため、この技術の導入に遅れをとっています。

当レポートでは、世界の水素燃料電池乗用車市場について調査し、市場の概要とともに、地域別の動向、競合情勢、および市場に参入する企業のプロファイルなどを提供しています。

目次

第1章 概要と範囲

第2章 概要

- イントロダクション

- 水素の特徴

- 市場の発展

- 市場成長

- 売上と収益

第3章 市場の動向

- 水素燃料電池乗用車(FCV)のメリット

- 電池技術の強み

- 水素燃料電池乗用車(FCV)の長所と短所

第4章 FCVの成長に影響を与える要因

- 気候変動との闘い

- 政府と世界組織の関与

- 新興の水素エコシステム

第5章 販売/リース

- 世界の販売/リース

- アジア太平洋の販売/リース

- EMEAの販売/リース

- アメリカの販売/リース

第6章 アジア太平洋のFCVの発売

- 概要

- オーストラリア

- 中国

- インド

- 日本

- マレーシア

- 韓国

- ニュージーランド

- その他

第7章 欧州(北欧を除く)諸国のFCV発売

- 概要

- オーストリア

- ベルギー

- チェコ共和国

- エストニア

- フランス

- ドイツ

- イタリア

- ラトビア

- オランダ

- ポーランド

- スロベニア

- スペイン

- スイス

- 英国

- その他の欧州諸国(北欧を除く)

第8章 北欧諸国

- デンマーク

- フィンランド

- アイスランド

- ノルウェー

- スウェーデン

第9章 中東・アフリカのFCVの発売

- イスラエル

- その他の中東諸国

第10章 北米のFCVの発売

- 米国

- 米国西海岸

- 東海岸

- カナダ

第11章 CALAのFCVの発売

- ブラジル

- その他

第12章 アジア太平洋の自動車メーカー

- Great Wall Motor Company Ltd.

- Grove Hydrogen Automotive

- Honda Motor Company

- Hyundai Motor Company

- Kia

- Mahindra & Mahindra

- Mazda

- Mitsubishi Motors

- Nissan

- SAIC Motor

- Suzuki Motors

- Tata Motors

- Toyota

- BAIC Motor

- その他

第13章 欧州の自動車メーカー

- BMW

- Daimler

- Jaguar Land Rover Automotive

- Pininfarina S.p.A

- Stellantis N.V.

- Renault

- Riversimple Movement Ltd

- Symbio

- Volkswagen

- その他

第14章 南北アメリカの自動車メーカー

- Ford

- General Motors

- Ronn Motor Group

- その他

第15章 FCV販売/収益予測

- 販売台数・リース台数

- 収益予測

第16章 結論

- 市場動向

- 市場投入

- 水素FCVとBEVの比較

- 政府の役割

- FCVエコシステム

- 市場の見通し

- 次のステップ

Executive Summary

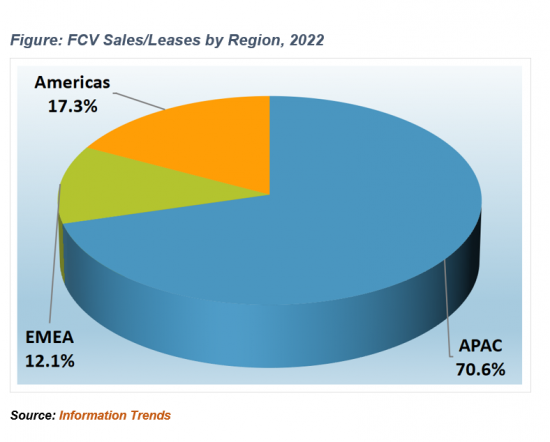

Close to 60 thousand hydrogen fuel cell passenger vehicles were sold worldwide by the end of 2022. More than 30 thousand of these vehicles were sold in the past two years - 2021 and 2022 - reflecting significant traction in the uptake of these vehicles,

The speed of deployments has accelerated in Asia-Pacific and Europe. With the exception of California, the United States has fallen behind in implementing this technology, particularly because of a lack of action at the federal level.

Information Trends believes that the only impediment to the adoption of these vehicles in any region is the unavailability of hydrogen stations. The sales of these vehicles are taking place rapidly in regions that have well-deployed hydrogen fueling infrastructures.

More than half of the fuel cell vehicles sold so far have been in Korea because it has the densest hydrogen fueling infrastructure of any major market. Other regions with strong sales of fuel cell vehicles are Japan and California where significant deployments of hydrogen stations have taken place.

Several automakers, both start-ups and established players, have been making inroads into the fuel cell passenger vehicle market. Hyundai's Nexo has been a clear winner among fuel cell vehicles rolled out so far. Nexo's only other major competitor in the market has been Toyota's Mirai. But as the market gains traction, other major automakers are jumping onto the bandwagon.

Honda is preparing to re-enter this market, beginning with the U.S., where it will launch a fuel cell vehicle in 2024 that will be based on its Honda CR-V. BMW will start mass-producing and selling fuel cell vehicles developed jointly with Toyota in the second half of this decade.

The country with the most automakers making inroads into the fuel cell passenger vehicle market is China. Until now rollouts in the country have mostly been technical demonstrations, mainly because of a lack of hydrogen stations.

Figure 1 shows the share of passenger hydrogen fuel vehicles by region as of year-end 2022.

As fueling infrastructures further expand in the second half of 2020s, hydrogen FCVs will begin to garner greater market acceptance, giving them a more pervasive presence in the market. By 2030, sufficient hydrogen fueling infrastructures will be in place in several regions of the world, giving a boost to the market for these vehicles.

Scope of the Study

Fuel cell technology can be used in virtually every kind of transportation: cars, trucks, buses, forklifts, motorcycles, bicycles, airplanes, boats, submarines, and trams. However, the market is witnessing significant activity in three major types of hydrogen-driven vehicles:

- Passenger FCVs

- Light-duty commercial FCVs

- Fuel cell buses and trucks

The focus of this study is light-duty passenger vehicles, such as sedans, SUVs, and minivans. The study does not cover commercial vehicles.

Unless otherwise stated, all references to hydrogen FCVs in this study imply passenger vehicles. Information Trends defines a light-duty vehicle as one that has a gross weight of up to six metric tons or a North American Class 5 gross vehicle weight rating.

This study conducts an in-depth examination of this emerging market, including an analysis of the strategies of major players with respect to product rollouts and market penetration. The study provides market forecasts for both unit sales/leases and revenue through 2037. The average prices of these vehicles are declining while automakers keep adding more features and enhancements.

Hydrogen FCVs being produced by the automakers fall into one of the following classifications:

- Hydrogen hybrids: These are like gasoline hybrids, but instead of gasoline, they use hydrogen. These vehicles generate electricity through regenerative braking which is either used immediately or stored in the battery until it is needed. The FCVs that have been rolled out by Toyota, Hyundai, and Honda are hydrogen fuel cell hybrids.

- Hydrogen plug-in hybrids: Like gasoline plug-in hybrids, these vehicles allow the battery to be charged from an electric outlet. The Mercedes Benz GLC F-Cell was the only vehicle to hit the market that was a plug-in hydrogen fuel cell hybrid, but now other automakers are coming out with these vehicles.

Table of Contents

1.0. Summary and Scope

- 1.1. Executive Summary

- 1.2. Scope of the Study

- 1.3. Abbreviations

2.0. Overview

- 2.1. Introduction

- 2.2. Characteristics of Hydrogen

- 2.3. Market Developments

- 2.4. Market Growth

- 2.5. Sales and Revenue

3.0. Market Developments

- 3.1. Advantages of Hydrogen FCVs

- 3.1.1. Rapid and Standardized Fueling

- 3.1.2. Ability to Travel Longer Distances

- 3.1.3. Capability of Carrying Heavier Loads

- 3.2. Strengths of Battery Technology

- 3.3. Pros and Cons of Hydrogen FCVs

- 3.3.1. Pros of Hydrogen FCVs

- 3.3.2. Cons of Hydrogen FCVs

4.0. Factors Impacting Growth of FCVs

- 4.1. Need to Combat Climate Change

- 4.1.1. Greenhouse Gas Emissions

- 4.1.2. Paris Climate Treaty

- 4.2. Engagement of Governments & Global Organizations

- 4.2.1. Regulatory Requirements

- 4.2.2. Government Mandates

- 4.2.3. Subsidies and Incentives

- 4.3. Emerging Hydrogen Ecosystem

- 4.3.1. Cost of Hydrogen

- 4.3.2. Buildout of Hydrogen Fueling Stations

- 4.3.3. Falling Costs of FCV Ownership

5.0. Sales/Leases

- 5.1. Global Sales/Leases

- 5.1.1. Global Sales/Leases by Region

- 5.1.2. Global Sales/Leases by Automaker

- 5.1.3. Global Sales/Leases by Model

- 5.2. APAC Sales/Leases

- 5.3. EMEA Sales/Leases

- 5.4. Americas Sales/Leases

6.0. APAC FCV Launches

- 6.1. Overview

- 6.2. Australia

- 6.2.1. Overview

- 6.2.2. Industry Organizations

- 6.2.3. Government Policies and Initiatives

- 6.2.4. Hydrogen FCVs Rollout

- 6.2.5. Assessment

- 6.3. China

- 6.3.1. Overview

- 6.3.2. Industry Organizations

- 6.3.3. Government Policies and Initiatives

- 6.3.4. Hydrogen FCV Rollout

- 6.3.5. Assessment

- 6.4. India

- 6.4.1. Overview

- 6.4.2. Industry Organizations

- 6.4.3. Government Policies and Initiatives

- 6.4.4. Hydrogen FCV Rollout

- 6.4.5. Assessment

- 6.5. Japan

- 6.5.1. Overview

- 6.5.2. Industry Organizations

- 6.5.3. Government Policies and Initiatives

- 6.5.4. Hydrogen FCV Rollout

- 6.5.5. Assessment

- 6.6. Malaysia

- 6.6.1. Overview

- 6.6.2. Industry Organizations

- 6.6.3. Government Policies and Initiatives

- 6.6.4. Hydrogen FCV Rollout

- 6.6.5. Assessment

- 6.7. South Korea

- 6.7.1. Overview

- 6.7.2. Industry Organizations

- 6.7.3. Government Policies and Initiatives

- 6.7.4. Hydrogen FCV Rollout

- 6.7.5. Related Initiatives

- 6.8. New Zealand

- 6.8.1. Overview

- 6.8.2. Industry Organizations

- 6.8.3. Government Policies and Initiatives

- 6.8.4. Hydrogen FCV Rollout

- 6.8.5. Related Initiatives

- 6.9. Other Countries

- 6.9.1. Thailand

- 6.9.2. Nepal

- 6.9.3. Other Locations

7. European (Except Nordic) Countries FCV Launches

- 7.1. Overview

- 7.2. Austria

- 7.2.1. Overview

- 7.2.2. Industry Organizations

- 7.2.3. Government Policies and Initiatives

- 7.2.4. Hydrogen FCV Rollout

- 7.2.5. Assessment

- 7.3. Belgium

- 7.3.1. Overview

- 7.3.2. Industry Organizations

- 7.3.3. Government Policies and Initiatives

- 7.3.4. Hydrogen FCV Rollout

- 7.3.5. Assessment

- 7.4. Czech Republic

- 7.4.1. Overview

- 7.4.2. Industry Organizations

- 7.4.3. Government Policies and Initiatives

- 7.4.4. Hydrogen FCV Rollout

- 7.4.5. Assessment

- 7.5. Estonia

- 7.5.1. Overview

- 7.5.2. Industry Organizations

- 7.5.3. Government Policies and Initiatives

- 7.5.4. Hydrogen FCV Rollout

- 7.5.5. Assessment

- 7.6. France

- 7.6.1. Overview

- 7.6.2. Industry Organizations

- 7.6.3. Government Policies and Initiatives

- 7.6.4. Hydrogen FCV Rollout

- 7.6.5. Assessment

- 7.7. Germany

- 7.7.1. Overview

- 7.7.2. Industry Organizations

- 7.7.3. Government Policies and Initiatives

- 7.7.4. Hydrogen FCV Rollout

- 7.7.5. Assessment

- 7.8. Italy

- 7.8.1. Overview

- 7.8.2. Industry Organizations

- 7.8.3. Government Policies and Initiatives

- 7.8.4. Hydrogen FCV Roll Out

- 7.8.5. Assessment

- 7.9. Latvia

- 7.9.1. Overview

- 7.9.2. Industry Organizations

- 7.9.3. Government Policies and Initiatives

- 7.9.4. Hydrogen FCV Rollout

- 7.9.5. Assessment

- 7.10. The Netherlands

- 7.10.1. Overview

- 7.10.2. Industry Organizations

- 7.10.3. Government Policies and Initiatives

- 7.10.4. Hydrogen FCV Rollout

- 7.10.5. Assessment

- 7.11. Poland

- 7.11.1. Overview

- 7.11.2. Industry Organizations

- 7.11.3. Government Policies and Initiatives

- 7.11.4. Hydrogen FCV Rollout

- 7.11.5. Assessment

- 7.12. Slovenia

- 7.12.1. Overview

- 7.12.2. Industry Organizations

- 7.12.3. Government Policies and Initiatives

- 7.12.4. Hydrogen FCV Rollout

- 7.12.5. Assessment

- 7.13. Spain

- 7.13.1. Overview

- 7.13.2. Industry Organizations

- 7.13.3. Government Policies and Initiatives

- 7.13.4. Hydrogen FCV Rollout

- 7.13.5. Assessment

- 7.14. Switzerland

- 7.14.1. Overview

- 7.14.2. Industry Organizations

- 7.14.3. Government Policies and Initiatives

- 7.14.4. Hydrogen FCV Rollout

- 7.14.5. Assessment

- 7.15. The U.K.

- 7.15.1. Overview

- 7.15.2. Industry Organizations

- 7.15.3. Government Policies and Initiatives

- 7.15.4. Hydrogen FCV Rollout

- 7.15.5. Assessment

- 7.16. Other European (Except Nordic) Countries

- 7.16.1. Slovakia

- 7.16.2. Bulgaria

- 7.16.3. Luxembourg

- 7.16.4. Russia

- 7.16.5. Ireland

- 7.16.6. Lithuania

8.0. Nordic Region

- 8.1. Denmark

- 8.1.1. Overview

- 8.1.2. Industry Organizations

- 8.1.3. Government Policies and Initiatives

- 8.1.4. Hydrogen FCV Rollout

- 8.1.5. Assessment

- 8.2. Finland

- 8.2.1. Overview

- 8.2.2. Industry Organizations

- 8.2.3. Government Policies and Initiatives

- 8.2.4. Hydrogen FCV Rollout

- 8.2.5. Assessment

- 8.3. Iceland

- 8.3.1. Overview

- 8.3.2. Industry Organizations

- 8.3.3. Government Policies and Initiatives

- 8.3.4. Hydrogen FCV Rollout

- 8.3.5. Assessment

- 8.4. Norway

- 8.4.1. Overview

- 8.4.2. Industry Organizations

- 8.4.3. Government Policies and Initiatives

- 8.4.4. Hydrogen FCV Rollout

- 8.4.5. Assessment

- 8.5. Sweden

- 8.5.1. Overview

- 8.5.2. Industry Organizations

- 8.5.3. Government Policies and Initiatives

- 8.5.4. Hydrogen FCV Rollout

- 8.5.5. Assessment

9.0. Middle East & Africa FCV Launches

- 9.1. Israel

- 9.1.1. Overview

- 9.1.2. Industry Organizations

- 9.1.3. Government Policies & Initiatives

- 9.1.4. Hydrogen FCV Rollout

- 9.1.5. Assessment

- 9.2. Other Middle East Countries

- 9.2.1. Saudi Arabia

- 9.2.2. United Arab Emirates

- 9.2.3. Turkey

- 9.2.4. South Africa

10.0. North America FCV Launches

- 10.1. U.S.

- 10.1.1. Overview

- 10.1.2. Industry Organizations

- 10.1.3. Government Policies and Initiatives

- 10.1.4. Nationwide Hydrogen FCV Rollout

- 10.2. U.S. West Coast

- 10.2.1. Overview

- 10.2.2. Industry Organizations

- 10.2.3. Government Policies and Initiatives

- 10.2.4. Hydrogen FCV Rollout

- 10.2.5. Assessment

- 10.3. East Coast

- 10.3.1. Overview

- 10.3.2. Industry Organizations

- 10.3.3. Government Policies and Initiatives

- 10.3.4. Hydrogen FCV Rollout

- 10.3.5. Assessment

- 10.4. Canada

- 10.4.1. Overview

- 10.4.2. Industry Organizations

- 10.4.3. Government Policies and Initiatives

- 10.4.4. Hydrogen FCV Rollout

- 10.4.5. Assessment

11.0. CALA FCV Launches

- 11.1. Brazil

- 11.1.1. Introduction

- 11.1.2. Industry Organizations

- 11.1.3. Government Policies and Initiatives

- 11.1.4. Hydrogen FCV Rollout

- 11.1.5. Assessment

- 11.2. Other CALA Countries

12.0. Asia-Pacific Automakers

- 12.1. Great Wall Motor Company Ltd.

- 12.1.1. Introduction

- 12.1.2. Hydrogen FCV Rollouts

- 12.1.3. Key Partnerships

- 12.1.4. Strategic Direction

- 12.2. Grove Hydrogen Automotive

- 12.2.1. Introduction

- 12.2.2. Hydrogen FCV Rollouts

- 12.2.3. Key Partnerships

- 12.2.4. Strategic Direction

- 12.3. Honda Motor Company

- 12.3.1. Introduction

- 12.3.2. Hydrogen FCV Rollout

- 12.3.3. Key Partnerships

- 12.3.4. Hydrogen FCV Pricing

- 12.3.5. Hydrogen FCV Sales/Leases

- 12.3.6. Strategic Direction

- 12.4. Hyundai Motor Company

- 12.4.1. Introduction

- 12.4.2. Hydrogen FCV Roll Out

- 12.4.3. Hydrogen FCV Sales/Leases

- 12.4.4. Key Partnerships139

- 12.4.5. Strategic Direction

- 12.5. Kia

- 12.5.1. Introduction

- 12.5.2. Hydrogen FCV Rollouts

- 12.5.3. Key Partnerships

- 12.5.4. Strategic Direction

- 12.6. Mahindra & Mahindra

- 12.6.1. Introduction

- 12.6.2. Hydrogen FCV Rollouts

- 12.6.3. Key Partnerships

- 12.6.4. Strategic Direction

- 12.7. Mazda

- 12.7.1. Introduction

- 12.7.2. Hydrogen FCV Rollouts

- 12.7.3. Key Partnerships

- 12.7.4. Strategic Direction

- 12.8. Mitsubishi Motors

- 12.8.1. Introduction

- 12.8.2. Hydrogen FCV Rollouts

- 12.8.3. Key Partnerships

- 12.8.4. Strategic Direction

- 12.9. Nissan

- 12.9.1. Introduction

- 12.9.2. Hydrogen FCV Rollouts

- 12.9.3. Key Partnerships

- 12.9.4. Strategic Direction

- 12.10. SAIC Motor

- 12.10.1. Introduction

- 12.10.2. Hydrogen FCV Rollouts

- 12.10.3. Key Partnerships

- 12.10.4. Hydrogen FCV Pricing

- 12.10.5. Strategic Direction

- 12.11. Suzuki Motors

- 12.11.1. Introduction

- 12.11.2. Hydrogen FCV Rollouts

- 12.11.3. Key Partnerships

- 12.11.4. Strategic Direction

- 12.12. Tata Motors

- 12.12.1. Introduction

- 12.12.2. Hydrogen FCV Rollouts

- 12.12.3. Key Partnerships

- 12.12.4. Strategic Direction

- 12.13. Toyota

- 12.13.1. Introduction

- 12.13.2. Hydrogen FCV Rollouts

- 12.13.3. Hydrogen FCV Sales/Leases

- 12.13.4. Hydrogen FCV Pricing

- 12.13.5. Key Partnerships

- 12.13.6. Strategic Direction

- 12.14. BAIC Motor

- 12.14.1. Introduction

- 12.14.2. Hydrogen FCV Rollout

- 12.14.3. Key Partnerships

- 12.14.4. Strategic Direction

- 12.15. Other APAC Automakers

- 12.15.1. Aiways Automobiles

- 12.15.2. Changan Automobile

- 12.15.3. Chery Automobile

- 12.15.4. Dongfeng Motor

- 12.15.5. FAW Group

- 12.15.6. GAC Motor

- 12.15.7. H2X Global

- 12.15.8. Haima Automobile

13.0. European Automakers

- 13.1. BMW

- 13.1.1. Introduction

- 13.1.2. Hydrogen FCV Rollouts

- 13.1.3. Key Partnerships

- 13.1.4. Strategic Direction

- 13.2. Daimler

- 13.2.1. Introduction

- 13.2.2. Hydrogen FCV Rollouts

- 13.2.3. Key Partnerships

- 13.2.4. Strategic Direction

- 13.3. Jaguar Land Rover Automotive

- 13.3.1. Introduction

- 13.3.2. Hydrogen FCV Rollouts

- 13.3.3. Key Partnerships

- 13.3.4. Strategic Direction

- 13.4. Pininfarina S.p.A.

- 13.4.1. Introduction

- 13.4.2. Hydrogen FCV Rollouts

- 13.4.3. Key Partnerships

- 13.4.4. Strategic Direction

- 13.5. Stellantis N.V.

- 13.5.1. Introduction

- 13.5.2. Hydrogen FCV Rollouts

- 13.5.3. Key Partnerships

- 13.5.4. Strategic Direction

- 13.6. Renault

- 13.6.1. Introduction

- 13.6.2. Hydrogen FCV Rollouts

- 13.6.3. Key Partnerships

- 13.6.4. Strategic Direction

- 13.7. Riversimple Movement Ltd.

- 13.7.1. Introduction

- 13.7.2. Hydrogen FCV Rollouts

- 13.7.3. Key Partnerships

- 13.7.4. Strategic Direction

- 13.8. Symbio

- 13.8.1. Introduction

- 13.8.2. Hydrogen FCV Rollouts

- 13.8.3. Key Partnerships

- 13.8.4. Strategic Direction

- 13.9. Volkswagen

- 13.9.1. Introduction

- 13.9.2. Hydrogen FCV Rollouts

- 13.9.3. Key Partnerships

- 13.9.4. Strategic Direction

- 13.10. Others

- 13.10.1. Ferrari

- 13.10.2. H2O E-mobile GmbH

- 13.10.3. HMC Group

- 13.10.4. NamX

- 13.10.5. Ineos Automotive Ltd.

- 13.10.6. Microcab

- 13.10.7. Viritech

14.0. Americas Automakers

- 14.1. Ford

- 14.1.1. Introduction

- 14.1.2. Hydrogen FCV Rollouts

- 14.1.3. Key Partnerships

- 14.1.4. Strategic Direction

- 14.2. General Motors

- 14.2.1. Introduction

- 14.2.2. Hydrogen FCV Rollouts

- 14.2.3. Key Partnerships

- 14.2.4. Strategic Direction

- 14.3. Ronn Motor Group

- 14.3.1. Introduction

- 14.3.2. Hydrogen FCV Rollouts

- 14.3.3. Key Partnerships

- 14.3.4. Strategic Direction

- 14.4. Others

- 14.4.1. Hyperion

- 14.4.2. Glickenhaus

15.0. FCVs Sales/Revenue Forecast

- 15.1. Unit Sales/Leases

- 15.1.1. Factors Impacting Sales/Leases

- 15.1.2. Global Unit Sales/Leases Overview

- 15.1.3. Global Unit Sales/Leases Forecast

- 15.1.4. APAC Unit Sales/Leases Forecast

- 15.1.5. EMEA Unit Sales/Leases Forecast

- 15.1.6. Americas Unit Sales/Leases Forecast

- 15.2. Revenue Forecast

- 15.2.1. Pricing Trends

- 15.2.2. Global Revenue Forecast

- 15.2.3. APAC Revenue Forecast

- 15.2.4. EMEA Revenue Forecast

- 15.2.5. Americas Revenue Forecast

16. Conclusions

- 16.1. Market Trends

- 16.2. Market Launches

- 16.3. Hydrogen FCVs vs. BEVs

- 16.4. Role of Governments

- 16.5. FCVs Ecosystem

- 16.6. Market Outlook

- 16.7. Next Steps

Figures

- Figure 1: FCV New Sales/Leases by Region, 2022

- Figure 2: Annual Global FCV Sales/Leases, 2014-2022

- Figure 3: APAC FCV Sales/Leases, 2014-2022

- Figure 4: EMEA FCV Sales/Leases, 2014-2020

- Figure 5: Americas FCV Sales/Leases, 2014-2020

- Figure 6: Global FCV Sales/Leases Share by Major Region, 2014-2022

- Figure 7: Global FCV Sales/Leases Share by Major Region, 2022

- Figure 8: Global FCV Sales/Leases Share by Automaker, 2014-2022

- Figure 9: Global FCV Sales/Leases Share by Automaker, 2022

- Figure 10: Global FCV Sales/Leases Share by Model, 2014-2020

- Figure 11: Global FCV Sales/Leases Share by Model, 2022

- Figure 12: APAC FCV Sales/Leases Share by Model, 2014-2022

- Figure 13: APAC FCV Sales/Leases Share by Model, 2022

- Figure 14: EMEA FCV Sales/Leases Share by Model, 2014-2022

- Figure 15: EMEA FCV Sales/Leases Share by Model, 2022

- Figure 16: Americas FCV Sales/Leases Share by Model, 2014-2022

- Figure 17: Americas FCVs Sales/Leases Share by Model, 2022

- Figure 18: Honda Clarity FC Sales/Leases Share by Region, 2014-2022

- Figure 19: Honda Clarity FC Sales/Leases Share by Region, 2022

- Figure 20: Hyundai FCV Sales/Leases Share by Region, 2014-2022

- Figure 21: Hyundai FCV Sales/Leases Share by Region, 2022

- Figure 22: Toyota Mirai Sales/Leases Share by Region, 2014-2022

- Figure 23: Toyota Mirai Sales/Leases Share by Region, 2022

- Figure 24: Global Aggregate FCV Unit Sales/Leases, 2022-2037

- Figure 25: CAGR of Aggregate FCVs Sales Globally, 2022-2037

- Figure 26: APAC Aggregate FCV Unit Sales/Leases, 2022-2037

- Figure 27: CAGR of Aggregate FCVs in APAC, 2022-2037

- Figure 28: EMEA Aggregate FCV Unit Sales/Leases, 2022-2037

- Figure 29: CAGR of Aggregate FCVs in EMEA, 2022-2037

- Figure 30: Americas Aggregate FCV Unit Sales/Leases, 2022-2037

- Figure 31: CAGR of Aggregate FCVs in Americas, 2022-2037

- Figure 32: CAGR of FCV Sales Revenue Globally, 2022-2037

- Figure 33: APAC FCV Sales/Leases Revenue in USD, 2022-2037

- Figure 34: CAGR of FCV Sales Revenue in APAC, 2022-2037

- Figure 35: CAGR of FCV Sales Revenue in EMEA, 2022-2037

- Figure 36: Americas FCV Sales/Leases Revenue in USD, 2022-2037

Tables

- Table 1: Global FCV Sales/Leases by Major Region, 2014-2022

- Table 2: Global FCV Sales/Leases by Automaker, 2014-2022

- Table 3: Global FCV Sales/Leases by Model, 2014-2022

- Table 4: APAC FCV Sales/Leases by Model, 2014-2022

- Table 5: EMEA FCV Sales/Leases by Model, 2014-2022

- Table 6: Americas FCV Sales/Leases by Model, 2014-2022

- Table 7: Honda Clarity Fuel Cell Sales/Leases, 2014-2022

- Table 8: Hyundai's Combined FCV Sales/Leases, 2014-2022

- Table 9: Hyundai Nexo Sales/Leases, 2014-2022

- Table 10: Hyundai Tucson ix35 FCEV Sales/Leases, 2014-2022

- Table 11: Toyota Mirai Sales/Leases, 2014-2022

- Table 12: Global FCV Sales/Leases by Major Region, 2014-2037

- Table 13: Global Cumulative FCV Sales/Leases by Major Region, 2022-2029

- Table 14: Global Cumulative FCV Sales/Leases by Major Region, 2030-2037

- Table 15: APAC Cumulative FCV Sales/Leases by Region/Country, 2022-2029

- Table 16: APAC Cumulative FCV Sales/Leases by Region/Country, 2030-2037

- Table 17: EMEA Cumulative FCV Sales/Leases by Region/Country, 2022-2029

- Table 18: EMEA Cumulative FCV Sales/Leases by Region/Country, 2030-2037

- Table 19: Americas Cumulative FCV Sales/Leases by Region/Country, 2022-2029

- Table 20: Americas Cumulative FCV Sales/Leases by Region/Country, 2030-2037

- Table 21: Global FCV Revenue by Major Region, 2022-2029

- Table 22: Global FCV Revenue by Major Region, 2030-2037

- Table 23: APAC FCV Revenue by Region/Country, 2022-2029

- Table 24: APAC FCV Revenue by Region/Country, 2030-2037

- Table 25: EMEA FCV Revenue by Region/Country, 2022-2029

- Table 26: EMEA FCV Revenue by Region/Country, 2030-2037

- Table 27: Americas FCV Revenue by Region/Country, 2022-2029

- Table 28: Americas FCV Revenue by Region/Country, 2030-2037