|

|

市場調査レポート

商品コード

1808013

スマートメーターデータ管理市場:提供サービス、機能、展開モデル、用途、ユーザータイプ、公共事業別-2025-2030年世界予測Smart Meter Data Management Market by Offering, Functionality, Deployment Model, Application, User Type, Utilities - Global Forecast 2025-2030 |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| スマートメーターデータ管理市場:提供サービス、機能、展開モデル、用途、ユーザータイプ、公共事業別-2025-2030年世界予測 |

|

出版日: 2025年08月28日

発行: 360iResearch

ページ情報: 英文 188 Pages

納期: 即日から翌営業日

|

全表示

- 概要

- 図表

- 目次

スマートメーターデータ管理市場の2024年の市場規模は19億8,000万米ドルで、2025年には23億米ドル、CAGR16.88%で成長し、2030年には50億5,000万米ドルに達すると予測されています。

| 主な市場の統計 | |

|---|---|

| 基準年2024 | 19億8,000万米ドル |

| 推定年2025 | 23億米ドル |

| 予測年2030 | 50億5,000万米ドル |

| CAGR(%) | 16.88% |

高度な分析とコネクティビティが利害関係者のスマートメーター管理を再定義する、データ主導のユーティリティ・エコシステムへの舞台設定

先進的なスマートメーターの導入が加速していることで、ユーティリティ部門はかつてないほど再構築され、10年前には想像もできなかったような消費パターン、運用効率、システムの信頼性に対する深い洞察が可能になっています。通信プロトコルの革新は、拡大し続けるデータ分析能力と相まって、ユーティリティ企業がコストを削減し、顧客満足度を高め、環境への影響を減少させるリアルタイムのインテリジェンスを導き出すことを可能にしています。このような背景から、スマートメーターのデータ管理は、グリッドの近代化イニシアチブの成功を支えるミッションクリティカルな規律として台頭してきました。

規制、技術、市場の各領域でスマートメーターデータ管理の進化を促進する重要な業界破壊を乗り切る

スマートメーターデータ管理の情勢は、技術的な加速、規制当局の期待の高まり、消費者の要求の進化が重なり、変革的な変化の真っ只中にあります。エッジ・コンピューティング・ソリューションは、データ処理をフィールド・デバイスに近づけ、待ち時間と帯域幅の消費を削減すると同時に、サイバーセキュリティの防御を強化しています。同時に、規制機関はより厳格なデータプライバシーと相互運用性の基準を義務付けており、ユーティリティ企業はイノベーションを阻害することなく顧客情報を保護する包括的なガバナンスフレームワークの採用を余儀なくされています。

2025年に向けて発表された米国の関税がスマートメーターデータ管理のサプライチェーン、コスト、展開戦略に及ぼす重大な影響の評価

米国で2025年に向けて輸入メーター、半導体部品、通信モジュールに新たな関税を課すことが発表されたことで、世界のサプライチェーンに波紋が広がり、メーカーや電力会社は調達戦略の見直しを迫られています。重要なハードウェアに対する関税の引き上げは、国内生産へのシフトを促し、コスト上昇を緩和するための現地製造拠点や戦略的提携への投資を刺激しています。同時に、調達チームは長期契約を活用して価格を固定し、潜在的な供給制約の中で機器の可用性を確保しています。

製品、機能、展開モデル、アプリケーション、ユーザータイプ、公益事業者にまたがる包括的なセグメンテーション別市場ダイナミクスの解明

スマートメーターデータ管理市場は、複数の側面から調査することで、微妙な理解が可能になります。提供サービスに関しては、エンドユーザーはベンダーが提供するソフトウェアプラットフォームとアウトソーシングサービスを組み合わせて利用するようになっており、マネージドサービスは継続的な最適化とスケーラビリティを提供する能力で支持を集めている一方、プロフェッショナルサービスは特注の統合やコンサルティング要件に対応しています。機能面では、効率的なデータ収集と取得を優先するソリューションが、実用的な知見を抽出する高度な処理・分析エンジンによって補完され、堅牢なデータ保存・管理フレームワークや、組織全体のインテリジェンスを民主化する洗練された可視化・レポーティングツールがそれに続きます。

世界の主要市場におけるスマートメーターデータ管理の地域差、投資動向、規制促進要因、成長機会の分析

地域ごとに異なるエコシステムは、スマートメーターデータ管理における独自の規制体制、インフラの成熟度、投資の優先順位を反映しています。南北アメリカでは、送電網の近代化を促進する先進的な法律と脱炭素化へのインセンティブが普及に拍車をかけており、北米の電力会社は堅牢な通信ネットワークを活用して、ほぼリアルタイムの分析と需要応答プログラムを統合しています。中南米市場は、新興市場とはいえ、大規模なデータ管理イニシアチブの基礎を築く、的を絞ったパイロット・プロジェクトと官民パートナーシップを追求しています。

技術、パートナーシップ、卓越したサービスを通じてスマートメーターデータ管理市場を形成する主要イノベーターと戦略的協力者のプロファイリング

先駆的な技術プロバイダーやシステムインテグレーターの一群は、技術革新、戦略的パートナーシップ、卓越したサービスの組み合わせを通じて、スマートメーターデータ管理市場を前進させています。確立されたメータリングの専門企業は、クラウドネイティブな分析プラットフォームでサービスを強化し、データレイクのシームレスな統合と企業資源計画システムとの相互運用性を可能にしています。グローバルエンタープライズソフトウェアベンダーは、請求、顧客エンゲージメント、グリッドオペレーションを単一プラットフォーム上で統合するモジュール型データ管理スイートを導入し、ベンダーの乱立を抑え、ベンダー管理を合理化しています。

スマートメーターデータ管理における新技術の活用、業務の最適化、顧客価値の向上のための業界リーダーのための行動指向の戦略的ロードマップ

業界のリーダーは、スマートメーターデータ管理におけるあらゆる機会を活用するために、3つのアプローチを優先すべきです。第一に、予測モデリングと機械学習を組み合わせた高度な分析フレームワークを統合し、プロアクティブメンテナンス、ダイナミックプライシング戦略、パーソナライズされた顧客エンゲージメントプログラムを推進しなければならないです。このような能力は、コスト回避、収益保護、顧客満足度において定量化可能な利益をもたらします。

定性的・定量的手法を活用した透明で体系的な調査アプローチにより、スマートメーターデータ管理の動向に関する厳密な洞察を提供します

本レポートは、定性的洞察と定量的分析を組み合わせた厳密な調査プロセスから得られた知見を統合したものです。1次調査では、電力会社の上級幹部、技術革新者、規制の専門家に詳細なインタビューを行い、現実の視点と新たな動向を把握しました。2次調査では、業界出版物、規制当局への届出、白書、学術研究など、一般に入手可能な幅広い情報を活用し、1次調査の結果を検証・整理しました。

意思決定者がスマートメーターデータ管理の将来を導くための重要な発見と将来展望の統合

技術革新、規制状況の進化、市場力学の合流は、スマートメーターデータ管理の状況を再形成し、電力会社とサービスプロバイダーに課題と機会の両方を提示しています。関税とサプライチェーンの複雑さが、機敏な調達と弾力性のあるアーキテクチャの必要性を際立たせる中、新たなアナリティクス機能は、業務パフォーマンスと顧客行動に対する前例のない洞察を約束します。地域ごとの違いは、成功には地域の規制枠組み、インフラの成熟度、投資能力を考慮した独自の戦略が必要であることを浮き彫りにしています。

目次

第1章 序文

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場の概要

第5章 市場力学

- リアルタイムのエネルギー負荷予測とバランス調整のためのAI駆動型予測分析フレームワーク

- クラウドベースのスマートメーターデータ管理ソリューションへの移行を加速

- エッジコンピューティングモジュールをスマートメーターインフラに統合し、瞬時に異常を検知

- スマートメーターのテレメトリと顧客請求データを保護するためのブロックチェーンベースのアーキテクチャの導入

- 分散型エネルギー資源およびEV充電ネットワークとのMDMシステム統合

- 高度な計測インフラデータ管理システムにおけるGDPRおよびCCPAに準拠したプライバシー制御の実装

第6章 市場洞察

- ポーターのファイブフォース分析

- PESTEL分析

第7章 米国の関税の累積的な影響2025

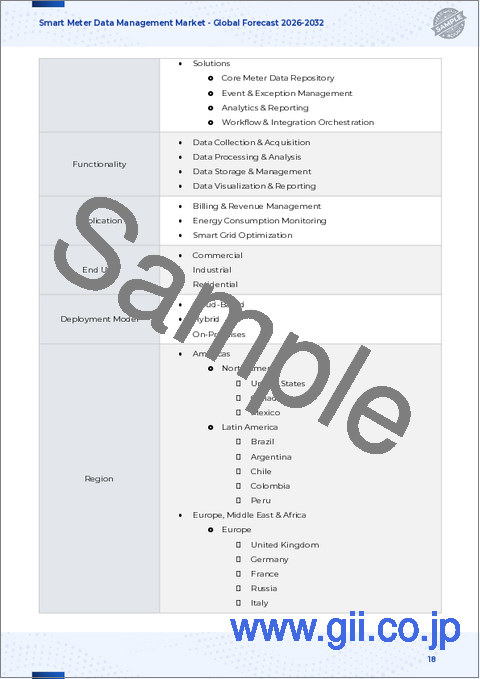

第8章 スマートメーターデータ管理市場:提供別

- サービス

- マネージドサービス

- プロフェッショナルサービス

- ソフトウェア

第9章 スマートメーターデータ管理市場:機能性別

- データ収集と取得

- データ処理と分析

- データの保存と管理

- データの可視化とレポート

第10章 スマートメーターデータ管理市場展開モデル別

- クラウドベースのソリューション

- ハイブリッドソリューション

- オンプレミスソリューション

第11章 スマートメーターデータ管理市場:用途別

- 請求と収益管理

- エネルギー消費監視

- スマートグリッド最適化

第12章 スマートメーターデータ管理市場ユーザータイプ別

- 商業用

- 産業

- 住宅用

第13章 スマートメーターデータ管理市場ユーティリティ別

- 電力会社

- ガス公益事業

- 水道事業

第14章 南北アメリカのスマートメーターデータ管理市場

- 米国

- カナダ

- メキシコ

- ブラジル

- アルゼンチン

第15章 欧州・中東・アフリカのスマートメーターデータ管理市場

- 英国

- ドイツ

- フランス

- ロシア

- イタリア

- スペイン

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- デンマーク

- オランダ

- カタール

- フィンランド

- スウェーデン

- ナイジェリア

- エジプト

- トルコ

- イスラエル

- ノルウェー

- ポーランド

- スイス

第16章 アジア太平洋地域のスマートメーターデータ管理市場

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- インドネシア

- タイ

- フィリピン

- マレーシア

- シンガポール

- ベトナム

- 台湾

第17章 競合情勢

- 市場シェア分析, 2024

- FPNVポジショニングマトリックス, 2024

- 競合分析

- Amazon Web Services, Inc.

- Diehl Stiftung & Co. KG

- Eaton Corporation PLC

- Hansen Technologies Limited by Roper Technologies

- International Business Machines Corporation

- Itron, Inc.

- NEC Corporation

- Oracle Corporation

- Robotron Datenbank-Software GmbH

- SAP SE

- Schneider Electric SE

- Siemens AG

- Toshiba Corporation

- Xylem, Inc.

第18章 リサーチAI

第19章 リサーチ統計

第20章 リサーチコンタクト

第21章 リサーチ記事

第22章 付録

LIST OF FIGURES

- FIGURE 1. SMART METER DATA MANAGEMENT MARKET RESEARCH PROCESS

- FIGURE 2. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, 2018-2030 (USD MILLION)

- FIGURE 3. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY REGION, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 4. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY COUNTRY, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 5. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2024 VS 2030 (%)

- FIGURE 6. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 7. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2024 VS 2030 (%)

- FIGURE 8. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 9. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2024 VS 2030 (%)

- FIGURE 10. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 11. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2024 VS 2030 (%)

- FIGURE 12. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 13. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2024 VS 2030 (%)

- FIGURE 14. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 15. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2024 VS 2030 (%)

- FIGURE 16. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 17. AMERICAS SMART METER DATA MANAGEMENT MARKET SIZE, BY COUNTRY, 2024 VS 2030 (%)

- FIGURE 18. AMERICAS SMART METER DATA MANAGEMENT MARKET SIZE, BY COUNTRY, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 19. UNITED STATES SMART METER DATA MANAGEMENT MARKET SIZE, BY STATE, 2024 VS 2030 (%)

- FIGURE 20. UNITED STATES SMART METER DATA MANAGEMENT MARKET SIZE, BY STATE, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 21. EUROPE, MIDDLE EAST & AFRICA SMART METER DATA MANAGEMENT MARKET SIZE, BY COUNTRY, 2024 VS 2030 (%)

- FIGURE 22. EUROPE, MIDDLE EAST & AFRICA SMART METER DATA MANAGEMENT MARKET SIZE, BY COUNTRY, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 23. ASIA-PACIFIC SMART METER DATA MANAGEMENT MARKET SIZE, BY COUNTRY, 2024 VS 2030 (%)

- FIGURE 24. ASIA-PACIFIC SMART METER DATA MANAGEMENT MARKET SIZE, BY COUNTRY, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 25. SMART METER DATA MANAGEMENT MARKET SHARE, BY KEY PLAYER, 2024

- FIGURE 26. SMART METER DATA MANAGEMENT MARKET, FPNV POSITIONING MATRIX, 2024

- FIGURE 27. SMART METER DATA MANAGEMENT MARKET: RESEARCHAI

- FIGURE 28. SMART METER DATA MANAGEMENT MARKET: RESEARCHSTATISTICS

- FIGURE 29. SMART METER DATA MANAGEMENT MARKET: RESEARCHCONTACTS

- FIGURE 30. SMART METER DATA MANAGEMENT MARKET: RESEARCHARTICLES

LIST OF TABLES

- TABLE 1. SMART METER DATA MANAGEMENT MARKET SEGMENTATION & COVERAGE

- TABLE 2. UNITED STATES DOLLAR EXCHANGE RATE, 2018-2024

- TABLE 3. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, 2018-2024 (USD MILLION)

- TABLE 4. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, 2025-2030 (USD MILLION)

- TABLE 5. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY REGION, 2018-2024 (USD MILLION)

- TABLE 6. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY REGION, 2025-2030 (USD MILLION)

- TABLE 7. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY COUNTRY, 2018-2024 (USD MILLION)

- TABLE 8. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 9. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2018-2024 (USD MILLION)

- TABLE 10. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 11. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, BY REGION, 2018-2024 (USD MILLION)

- TABLE 12. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, BY REGION, 2025-2030 (USD MILLION)

- TABLE 13. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY MANAGED SERVICES, BY REGION, 2018-2024 (USD MILLION)

- TABLE 14. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY MANAGED SERVICES, BY REGION, 2025-2030 (USD MILLION)

- TABLE 15. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY PROFESSIONAL SERVICES, BY REGION, 2018-2024 (USD MILLION)

- TABLE 16. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY PROFESSIONAL SERVICES, BY REGION, 2025-2030 (USD MILLION)

- TABLE 17. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2018-2024 (USD MILLION)

- TABLE 18. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2025-2030 (USD MILLION)

- TABLE 19. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY SOFTWARE, BY REGION, 2018-2024 (USD MILLION)

- TABLE 20. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY SOFTWARE, BY REGION, 2025-2030 (USD MILLION)

- TABLE 21. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2018-2024 (USD MILLION)

- TABLE 22. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2025-2030 (USD MILLION)

- TABLE 23. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY DATA COLLECTION & ACQUISITION, BY REGION, 2018-2024 (USD MILLION)

- TABLE 24. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY DATA COLLECTION & ACQUISITION, BY REGION, 2025-2030 (USD MILLION)

- TABLE 25. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY DATA PROCESSING & ANALYSIS, BY REGION, 2018-2024 (USD MILLION)

- TABLE 26. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY DATA PROCESSING & ANALYSIS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 27. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY DATA STORAGE & MANAGEMENT, BY REGION, 2018-2024 (USD MILLION)

- TABLE 28. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY DATA STORAGE & MANAGEMENT, BY REGION, 2025-2030 (USD MILLION)

- TABLE 29. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY DATA VISUALIZATION & REPORTING, BY REGION, 2018-2024 (USD MILLION)

- TABLE 30. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY DATA VISUALIZATION & REPORTING, BY REGION, 2025-2030 (USD MILLION)

- TABLE 31. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2018-2024 (USD MILLION)

- TABLE 32. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2025-2030 (USD MILLION)

- TABLE 33. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY CLOUD-BASED SOLUTIONS, BY REGION, 2018-2024 (USD MILLION)

- TABLE 34. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY CLOUD-BASED SOLUTIONS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 35. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY HYBRID SOLUTIONS, BY REGION, 2018-2024 (USD MILLION)

- TABLE 36. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY HYBRID SOLUTIONS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 37. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY ON-PREMISES SOLUTIONS, BY REGION, 2018-2024 (USD MILLION)

- TABLE 38. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY ON-PREMISES SOLUTIONS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 39. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 40. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 41. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY BILLING & REVENUE MANAGEMENT, BY REGION, 2018-2024 (USD MILLION)

- TABLE 42. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY BILLING & REVENUE MANAGEMENT, BY REGION, 2025-2030 (USD MILLION)

- TABLE 43. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY ENERGY CONSUMPTION MONITORING, BY REGION, 2018-2024 (USD MILLION)

- TABLE 44. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY ENERGY CONSUMPTION MONITORING, BY REGION, 2025-2030 (USD MILLION)

- TABLE 45. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY SMART GRID OPTIMIZATION, BY REGION, 2018-2024 (USD MILLION)

- TABLE 46. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY SMART GRID OPTIMIZATION, BY REGION, 2025-2030 (USD MILLION)

- TABLE 47. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2018-2024 (USD MILLION)

- TABLE 48. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2025-2030 (USD MILLION)

- TABLE 49. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY COMMERCIAL, BY REGION, 2018-2024 (USD MILLION)

- TABLE 50. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY COMMERCIAL, BY REGION, 2025-2030 (USD MILLION)

- TABLE 51. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY INDUSTRIAL, BY REGION, 2018-2024 (USD MILLION)

- TABLE 52. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY INDUSTRIAL, BY REGION, 2025-2030 (USD MILLION)

- TABLE 53. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY RESIDENTIAL, BY REGION, 2018-2024 (USD MILLION)

- TABLE 54. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY RESIDENTIAL, BY REGION, 2025-2030 (USD MILLION)

- TABLE 55. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2018-2024 (USD MILLION)

- TABLE 56. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2025-2030 (USD MILLION)

- TABLE 57. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY ELECTRICITY UTILITIES, BY REGION, 2018-2024 (USD MILLION)

- TABLE 58. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY ELECTRICITY UTILITIES, BY REGION, 2025-2030 (USD MILLION)

- TABLE 59. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY GAS UTILITIES, BY REGION, 2018-2024 (USD MILLION)

- TABLE 60. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY GAS UTILITIES, BY REGION, 2025-2030 (USD MILLION)

- TABLE 61. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY WATER UTILITIES, BY REGION, 2018-2024 (USD MILLION)

- TABLE 62. GLOBAL SMART METER DATA MANAGEMENT MARKET SIZE, BY WATER UTILITIES, BY REGION, 2025-2030 (USD MILLION)

- TABLE 63. AMERICAS SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2018-2024 (USD MILLION)

- TABLE 64. AMERICAS SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 65. AMERICAS SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2018-2024 (USD MILLION)

- TABLE 66. AMERICAS SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2025-2030 (USD MILLION)

- TABLE 67. AMERICAS SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2018-2024 (USD MILLION)

- TABLE 68. AMERICAS SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2025-2030 (USD MILLION)

- TABLE 69. AMERICAS SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2018-2024 (USD MILLION)

- TABLE 70. AMERICAS SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2025-2030 (USD MILLION)

- TABLE 71. AMERICAS SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 72. AMERICAS SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 73. AMERICAS SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2018-2024 (USD MILLION)

- TABLE 74. AMERICAS SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2025-2030 (USD MILLION)

- TABLE 75. AMERICAS SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2018-2024 (USD MILLION)

- TABLE 76. AMERICAS SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2025-2030 (USD MILLION)

- TABLE 77. AMERICAS SMART METER DATA MANAGEMENT MARKET SIZE, BY COUNTRY, 2018-2024 (USD MILLION)

- TABLE 78. AMERICAS SMART METER DATA MANAGEMENT MARKET SIZE, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 79. UNITED STATES SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2018-2024 (USD MILLION)

- TABLE 80. UNITED STATES SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 81. UNITED STATES SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2018-2024 (USD MILLION)

- TABLE 82. UNITED STATES SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2025-2030 (USD MILLION)

- TABLE 83. UNITED STATES SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2018-2024 (USD MILLION)

- TABLE 84. UNITED STATES SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2025-2030 (USD MILLION)

- TABLE 85. UNITED STATES SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2018-2024 (USD MILLION)

- TABLE 86. UNITED STATES SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2025-2030 (USD MILLION)

- TABLE 87. UNITED STATES SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 88. UNITED STATES SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 89. UNITED STATES SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2018-2024 (USD MILLION)

- TABLE 90. UNITED STATES SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2025-2030 (USD MILLION)

- TABLE 91. UNITED STATES SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2018-2024 (USD MILLION)

- TABLE 92. UNITED STATES SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2025-2030 (USD MILLION)

- TABLE 93. UNITED STATES SMART METER DATA MANAGEMENT MARKET SIZE, BY STATE, 2018-2024 (USD MILLION)

- TABLE 94. UNITED STATES SMART METER DATA MANAGEMENT MARKET SIZE, BY STATE, 2025-2030 (USD MILLION)

- TABLE 95. CANADA SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2018-2024 (USD MILLION)

- TABLE 96. CANADA SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 97. CANADA SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2018-2024 (USD MILLION)

- TABLE 98. CANADA SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2025-2030 (USD MILLION)

- TABLE 99. CANADA SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2018-2024 (USD MILLION)

- TABLE 100. CANADA SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2025-2030 (USD MILLION)

- TABLE 101. CANADA SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2018-2024 (USD MILLION)

- TABLE 102. CANADA SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2025-2030 (USD MILLION)

- TABLE 103. CANADA SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 104. CANADA SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 105. CANADA SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2018-2024 (USD MILLION)

- TABLE 106. CANADA SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2025-2030 (USD MILLION)

- TABLE 107. CANADA SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2018-2024 (USD MILLION)

- TABLE 108. CANADA SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2025-2030 (USD MILLION)

- TABLE 109. MEXICO SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2018-2024 (USD MILLION)

- TABLE 110. MEXICO SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 111. MEXICO SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2018-2024 (USD MILLION)

- TABLE 112. MEXICO SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2025-2030 (USD MILLION)

- TABLE 113. MEXICO SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2018-2024 (USD MILLION)

- TABLE 114. MEXICO SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2025-2030 (USD MILLION)

- TABLE 115. MEXICO SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2018-2024 (USD MILLION)

- TABLE 116. MEXICO SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2025-2030 (USD MILLION)

- TABLE 117. MEXICO SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 118. MEXICO SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 119. MEXICO SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2018-2024 (USD MILLION)

- TABLE 120. MEXICO SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2025-2030 (USD MILLION)

- TABLE 121. MEXICO SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2018-2024 (USD MILLION)

- TABLE 122. MEXICO SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2025-2030 (USD MILLION)

- TABLE 123. BRAZIL SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2018-2024 (USD MILLION)

- TABLE 124. BRAZIL SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 125. BRAZIL SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2018-2024 (USD MILLION)

- TABLE 126. BRAZIL SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2025-2030 (USD MILLION)

- TABLE 127. BRAZIL SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2018-2024 (USD MILLION)

- TABLE 128. BRAZIL SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2025-2030 (USD MILLION)

- TABLE 129. BRAZIL SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2018-2024 (USD MILLION)

- TABLE 130. BRAZIL SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2025-2030 (USD MILLION)

- TABLE 131. BRAZIL SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 132. BRAZIL SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 133. BRAZIL SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2018-2024 (USD MILLION)

- TABLE 134. BRAZIL SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2025-2030 (USD MILLION)

- TABLE 135. BRAZIL SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2018-2024 (USD MILLION)

- TABLE 136. BRAZIL SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2025-2030 (USD MILLION)

- TABLE 137. ARGENTINA SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2018-2024 (USD MILLION)

- TABLE 138. ARGENTINA SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 139. ARGENTINA SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2018-2024 (USD MILLION)

- TABLE 140. ARGENTINA SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2025-2030 (USD MILLION)

- TABLE 141. ARGENTINA SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2018-2024 (USD MILLION)

- TABLE 142. ARGENTINA SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2025-2030 (USD MILLION)

- TABLE 143. ARGENTINA SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2018-2024 (USD MILLION)

- TABLE 144. ARGENTINA SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2025-2030 (USD MILLION)

- TABLE 145. ARGENTINA SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 146. ARGENTINA SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 147. ARGENTINA SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2018-2024 (USD MILLION)

- TABLE 148. ARGENTINA SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2025-2030 (USD MILLION)

- TABLE 149. ARGENTINA SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2018-2024 (USD MILLION)

- TABLE 150. ARGENTINA SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2025-2030 (USD MILLION)

- TABLE 151. EUROPE, MIDDLE EAST & AFRICA SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2018-2024 (USD MILLION)

- TABLE 152. EUROPE, MIDDLE EAST & AFRICA SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 153. EUROPE, MIDDLE EAST & AFRICA SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2018-2024 (USD MILLION)

- TABLE 154. EUROPE, MIDDLE EAST & AFRICA SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2025-2030 (USD MILLION)

- TABLE 155. EUROPE, MIDDLE EAST & AFRICA SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2018-2024 (USD MILLION)

- TABLE 156. EUROPE, MIDDLE EAST & AFRICA SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2025-2030 (USD MILLION)

- TABLE 157. EUROPE, MIDDLE EAST & AFRICA SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2018-2024 (USD MILLION)

- TABLE 158. EUROPE, MIDDLE EAST & AFRICA SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2025-2030 (USD MILLION)

- TABLE 159. EUROPE, MIDDLE EAST & AFRICA SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 160. EUROPE, MIDDLE EAST & AFRICA SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 161. EUROPE, MIDDLE EAST & AFRICA SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2018-2024 (USD MILLION)

- TABLE 162. EUROPE, MIDDLE EAST & AFRICA SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2025-2030 (USD MILLION)

- TABLE 163. EUROPE, MIDDLE EAST & AFRICA SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2018-2024 (USD MILLION)

- TABLE 164. EUROPE, MIDDLE EAST & AFRICA SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2025-2030 (USD MILLION)

- TABLE 165. EUROPE, MIDDLE EAST & AFRICA SMART METER DATA MANAGEMENT MARKET SIZE, BY COUNTRY, 2018-2024 (USD MILLION)

- TABLE 166. EUROPE, MIDDLE EAST & AFRICA SMART METER DATA MANAGEMENT MARKET SIZE, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 167. UNITED KINGDOM SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2018-2024 (USD MILLION)

- TABLE 168. UNITED KINGDOM SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 169. UNITED KINGDOM SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2018-2024 (USD MILLION)

- TABLE 170. UNITED KINGDOM SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2025-2030 (USD MILLION)

- TABLE 171. UNITED KINGDOM SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2018-2024 (USD MILLION)

- TABLE 172. UNITED KINGDOM SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2025-2030 (USD MILLION)

- TABLE 173. UNITED KINGDOM SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2018-2024 (USD MILLION)

- TABLE 174. UNITED KINGDOM SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2025-2030 (USD MILLION)

- TABLE 175. UNITED KINGDOM SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 176. UNITED KINGDOM SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 177. UNITED KINGDOM SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2018-2024 (USD MILLION)

- TABLE 178. UNITED KINGDOM SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2025-2030 (USD MILLION)

- TABLE 179. UNITED KINGDOM SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2018-2024 (USD MILLION)

- TABLE 180. UNITED KINGDOM SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2025-2030 (USD MILLION)

- TABLE 181. GERMANY SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2018-2024 (USD MILLION)

- TABLE 182. GERMANY SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 183. GERMANY SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2018-2024 (USD MILLION)

- TABLE 184. GERMANY SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2025-2030 (USD MILLION)

- TABLE 185. GERMANY SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2018-2024 (USD MILLION)

- TABLE 186. GERMANY SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2025-2030 (USD MILLION)

- TABLE 187. GERMANY SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2018-2024 (USD MILLION)

- TABLE 188. GERMANY SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2025-2030 (USD MILLION)

- TABLE 189. GERMANY SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 190. GERMANY SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 191. GERMANY SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2018-2024 (USD MILLION)

- TABLE 192. GERMANY SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2025-2030 (USD MILLION)

- TABLE 193. GERMANY SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2018-2024 (USD MILLION)

- TABLE 194. GERMANY SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2025-2030 (USD MILLION)

- TABLE 195. FRANCE SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2018-2024 (USD MILLION)

- TABLE 196. FRANCE SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 197. FRANCE SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2018-2024 (USD MILLION)

- TABLE 198. FRANCE SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2025-2030 (USD MILLION)

- TABLE 199. FRANCE SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2018-2024 (USD MILLION)

- TABLE 200. FRANCE SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2025-2030 (USD MILLION)

- TABLE 201. FRANCE SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2018-2024 (USD MILLION)

- TABLE 202. FRANCE SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2025-2030 (USD MILLION)

- TABLE 203. FRANCE SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 204. FRANCE SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 205. FRANCE SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2018-2024 (USD MILLION)

- TABLE 206. FRANCE SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2025-2030 (USD MILLION)

- TABLE 207. FRANCE SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2018-2024 (USD MILLION)

- TABLE 208. FRANCE SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2025-2030 (USD MILLION)

- TABLE 209. RUSSIA SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2018-2024 (USD MILLION)

- TABLE 210. RUSSIA SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 211. RUSSIA SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2018-2024 (USD MILLION)

- TABLE 212. RUSSIA SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2025-2030 (USD MILLION)

- TABLE 213. RUSSIA SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2018-2024 (USD MILLION)

- TABLE 214. RUSSIA SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2025-2030 (USD MILLION)

- TABLE 215. RUSSIA SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2018-2024 (USD MILLION)

- TABLE 216. RUSSIA SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2025-2030 (USD MILLION)

- TABLE 217. RUSSIA SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 218. RUSSIA SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 219. RUSSIA SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2018-2024 (USD MILLION)

- TABLE 220. RUSSIA SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2025-2030 (USD MILLION)

- TABLE 221. RUSSIA SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2018-2024 (USD MILLION)

- TABLE 222. RUSSIA SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2025-2030 (USD MILLION)

- TABLE 223. ITALY SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2018-2024 (USD MILLION)

- TABLE 224. ITALY SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 225. ITALY SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2018-2024 (USD MILLION)

- TABLE 226. ITALY SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2025-2030 (USD MILLION)

- TABLE 227. ITALY SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2018-2024 (USD MILLION)

- TABLE 228. ITALY SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2025-2030 (USD MILLION)

- TABLE 229. ITALY SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2018-2024 (USD MILLION)

- TABLE 230. ITALY SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2025-2030 (USD MILLION)

- TABLE 231. ITALY SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 232. ITALY SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 233. ITALY SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2018-2024 (USD MILLION)

- TABLE 234. ITALY SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2025-2030 (USD MILLION)

- TABLE 235. ITALY SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2018-2024 (USD MILLION)

- TABLE 236. ITALY SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2025-2030 (USD MILLION)

- TABLE 237. SPAIN SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2018-2024 (USD MILLION)

- TABLE 238. SPAIN SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 239. SPAIN SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2018-2024 (USD MILLION)

- TABLE 240. SPAIN SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2025-2030 (USD MILLION)

- TABLE 241. SPAIN SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2018-2024 (USD MILLION)

- TABLE 242. SPAIN SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2025-2030 (USD MILLION)

- TABLE 243. SPAIN SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2018-2024 (USD MILLION)

- TABLE 244. SPAIN SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2025-2030 (USD MILLION)

- TABLE 245. SPAIN SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 246. SPAIN SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 247. SPAIN SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2018-2024 (USD MILLION)

- TABLE 248. SPAIN SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2025-2030 (USD MILLION)

- TABLE 249. SPAIN SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2018-2024 (USD MILLION)

- TABLE 250. SPAIN SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2025-2030 (USD MILLION)

- TABLE 251. UNITED ARAB EMIRATES SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2018-2024 (USD MILLION)

- TABLE 252. UNITED ARAB EMIRATES SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 253. UNITED ARAB EMIRATES SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2018-2024 (USD MILLION)

- TABLE 254. UNITED ARAB EMIRATES SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2025-2030 (USD MILLION)

- TABLE 255. UNITED ARAB EMIRATES SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2018-2024 (USD MILLION)

- TABLE 256. UNITED ARAB EMIRATES SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2025-2030 (USD MILLION)

- TABLE 257. UNITED ARAB EMIRATES SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2018-2024 (USD MILLION)

- TABLE 258. UNITED ARAB EMIRATES SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2025-2030 (USD MILLION)

- TABLE 259. UNITED ARAB EMIRATES SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 260. UNITED ARAB EMIRATES SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 261. UNITED ARAB EMIRATES SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2018-2024 (USD MILLION)

- TABLE 262. UNITED ARAB EMIRATES SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2025-2030 (USD MILLION)

- TABLE 263. UNITED ARAB EMIRATES SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2018-2024 (USD MILLION)

- TABLE 264. UNITED ARAB EMIRATES SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2025-2030 (USD MILLION)

- TABLE 265. SAUDI ARABIA SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2018-2024 (USD MILLION)

- TABLE 266. SAUDI ARABIA SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 267. SAUDI ARABIA SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2018-2024 (USD MILLION)

- TABLE 268. SAUDI ARABIA SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2025-2030 (USD MILLION)

- TABLE 269. SAUDI ARABIA SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2018-2024 (USD MILLION)

- TABLE 270. SAUDI ARABIA SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2025-2030 (USD MILLION)

- TABLE 271. SAUDI ARABIA SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2018-2024 (USD MILLION)

- TABLE 272. SAUDI ARABIA SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2025-2030 (USD MILLION)

- TABLE 273. SAUDI ARABIA SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 274. SAUDI ARABIA SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 275. SAUDI ARABIA SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2018-2024 (USD MILLION)

- TABLE 276. SAUDI ARABIA SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2025-2030 (USD MILLION)

- TABLE 277. SAUDI ARABIA SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2018-2024 (USD MILLION)

- TABLE 278. SAUDI ARABIA SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2025-2030 (USD MILLION)

- TABLE 279. SOUTH AFRICA SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2018-2024 (USD MILLION)

- TABLE 280. SOUTH AFRICA SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 281. SOUTH AFRICA SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2018-2024 (USD MILLION)

- TABLE 282. SOUTH AFRICA SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2025-2030 (USD MILLION)

- TABLE 283. SOUTH AFRICA SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2018-2024 (USD MILLION)

- TABLE 284. SOUTH AFRICA SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2025-2030 (USD MILLION)

- TABLE 285. SOUTH AFRICA SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2018-2024 (USD MILLION)

- TABLE 286. SOUTH AFRICA SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2025-2030 (USD MILLION)

- TABLE 287. SOUTH AFRICA SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 288. SOUTH AFRICA SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 289. SOUTH AFRICA SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2018-2024 (USD MILLION)

- TABLE 290. SOUTH AFRICA SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2025-2030 (USD MILLION)

- TABLE 291. SOUTH AFRICA SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2018-2024 (USD MILLION)

- TABLE 292. SOUTH AFRICA SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2025-2030 (USD MILLION)

- TABLE 293. DENMARK SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2018-2024 (USD MILLION)

- TABLE 294. DENMARK SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 295. DENMARK SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2018-2024 (USD MILLION)

- TABLE 296. DENMARK SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2025-2030 (USD MILLION)

- TABLE 297. DENMARK SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2018-2024 (USD MILLION)

- TABLE 298. DENMARK SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2025-2030 (USD MILLION)

- TABLE 299. DENMARK SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2018-2024 (USD MILLION)

- TABLE 300. DENMARK SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2025-2030 (USD MILLION)

- TABLE 301. DENMARK SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 302. DENMARK SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 303. DENMARK SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2018-2024 (USD MILLION)

- TABLE 304. DENMARK SMART METER DATA MANAGEMENT MARKET SIZE, BY USER TYPE, 2025-2030 (USD MILLION)

- TABLE 305. DENMARK SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2018-2024 (USD MILLION)

- TABLE 306. DENMARK SMART METER DATA MANAGEMENT MARKET SIZE, BY UTILITIES, 2025-2030 (USD MILLION)

- TABLE 307. NETHERLANDS SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2018-2024 (USD MILLION)

- TABLE 308. NETHERLANDS SMART METER DATA MANAGEMENT MARKET SIZE, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 309. NETHERLANDS SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2018-2024 (USD MILLION)

- TABLE 310. NETHERLANDS SMART METER DATA MANAGEMENT MARKET SIZE, BY SERVICES, 2025-2030 (USD MILLION)

- TABLE 311. NETHERLANDS SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2018-2024 (USD MILLION)

- TABLE 312. NETHERLANDS SMART METER DATA MANAGEMENT MARKET SIZE, BY FUNCTIONALITY, 2025-2030 (USD MILLION)

- TABLE 313. NETHERLANDS SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2018-2024 (USD MILLION)

- TABLE 314. NETHERLANDS SMART METER DATA MANAGEMENT MARKET SIZE, BY DEPLOYMENT MODEL, 2025-2030 (USD MILLION)

- TABLE 315. NETHERLANDS SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 316. NETHERLANDS SMART METER DATA MANAGEMENT MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 317. NETHERL

The Smart Meter Data Management Market was valued at USD 1.98 billion in 2024 and is projected to grow to USD 2.30 billion in 2025, with a CAGR of 16.88%, reaching USD 5.05 billion by 2030.

| KEY MARKET STATISTICS | |

|---|---|

| Base Year [2024] | USD 1.98 billion |

| Estimated Year [2025] | USD 2.30 billion |

| Forecast Year [2030] | USD 5.05 billion |

| CAGR (%) | 16.88% |

Setting the Stage for a Data-Driven Utility Ecosystem Where Advanced Analytics and Connectivity Are Redefining Smart Meter Management for Stakeholders

The accelerating deployment of advanced smart meters is reshaping the utility sector as never before, enabling a depth of insight into consumption patterns, operational efficiency, and system reliability that was unimaginable a decade ago. Innovations in communication protocols, coupled with ever-expanding data analytics capabilities, now allow utilities to derive real-time intelligence that reduces cost, enhances customer satisfaction, and diminishes environmental impact. Against this backdrop, smart meter data management has emerged as a mission-critical discipline underpinning every successful grid modernization initiative.

By centralizing high-velocity data streams from millions of endpoints and applying sophisticated processing frameworks, utilities can anticipate demand fluctuations, optimize load balancing, and identify anomalies before they escalate into outages or revenue losses. Yet the full promise of this technological evolution depends on an integrated strategy that spans service delivery, software platforms, and robust data governance. As stakeholders navigate an increasingly complex landscape, a clear understanding of emerging trends, regulatory shifts, and strategic segmentation is essential for achieving sustainable growth and resilience.

Navigating Pivotal Industry Disruptions That Drive the Evolution of Smart Meter Data Management Across Regulatory, Technological, and Market Domains

The smart meter data management landscape is in the midst of transformative shifts driven by a confluence of technological acceleration, heightened regulatory expectations, and evolving consumer demands. Edge computing solutions are bringing data processing closer to field devices, reducing latency and bandwidth consumption while reinforcing cybersecurity defenses. Simultaneously, regulatory bodies are mandating stricter data privacy and interoperability standards, compelling utilities to adopt comprehensive governance frameworks that protect customer information without stifling innovation.

Moreover, the rise of Internet of Things (IoT) integrations is expanding the role of smart meters from mere measurement instruments into intelligent nodes within an interconnected energy ecosystem. This shift is complemented by growing investments in artificial intelligence and machine learning, enabling predictive maintenance, advanced load forecasting, and dynamic tariff structuring. As stakeholders navigate these converging forces, they must reimagine legacy architectures, foster cross-industry partnerships, and embrace modular platforms that can adapt to future disruptions.

Assessing the Profound Effects of United States Tariffs Announced for 2025 on Smart Meter Data Management Supply Chains, Costs, and Deployment Strategies

The announcement of new tariffs on imported meters, semiconductor components, and communication modules in the United States for 2025 has reverberated across global supply chains, compelling manufacturers and utilities to reassess sourcing strategies. Increased duties on critical hardware are prompting a shift toward domestic production, stimulating investment in local manufacturing hubs and strategic alliances to mitigate cost escalations. Concurrently, procurement teams are leveraging long-term contracts to lock in pricing and ensure equipment availability amid potential supply constraints.

On the downstream side, utilities are recalibrating deployment timelines and allocating contingency budgets to accommodate anticipated expenses without compromising modernization roadmaps. Providers of software and services are responding by offering flexible, consumption-based pricing models and managed services that absorb a portion of tariff-driven cost variability. In aggregate, these adjustments are challenging traditional procurement paradigms and accelerating a move toward agile, resilient procurement frameworks that balance economic efficiency with operational continuity.

Uncovering Market Dynamics Through Comprehensive Segmentation Spanning Offerings, Functionalities, Deployment Models, Applications, User Types, and Utilities

A nuanced understanding of the smart meter data management market emerges when examined across multiple dimensions. In terms of offerings, end users increasingly rely on a blend of vendor-provided software platforms and outsourced services, with managed services gaining traction for their ability to deliver ongoing optimization and scalability while professional services address bespoke integration and consulting requirements. From a functionality perspective, solutions that prioritize efficient data collection and acquisition are complemented by advanced processing and analysis engines that extract actionable insights, followed by robust data storage and management frameworks and sophisticated visualization and reporting tools that democratize intelligence across the organization.

Deployment preferences are evolving toward cloud-based solutions that offer elasticity and lower upfront investment, while hybrid models deliver a balanced approach for those requiring on-premises control alongside cloud agility, and pure on-premises deployments persist in security-sensitive environments. Applications span from billing and revenue management systems that reconcile consumption with tariff structures, to energy consumption monitoring platforms that empower users with granular usage data, and smart grid optimization tools that coordinate distributed energy resources and enforce grid stability. User segments differ in requirements, as commercial entities demand detailed analytics for consumption forecasting, industrial operators focus on operational continuity and reliability, and residential customers seek user-friendly dashboards and self-service capabilities. Finally, the utility vertical is itself diverse, with electricity providers leading adoption, gas utilities exploring advanced metering, and water utilities gradually integrating data management to enhance conservation and leak detection.

Analyzing Regional Variations in Smart Meter Data Management Adoption, Investment Trends, Regulatory Drivers, and Growth Opportunities Across Major Global Markets

Distinct regional ecosystems reflect unique regulatory regimes, infrastructure maturity, and investment priorities in smart meter data management. In the Americas, progressive legislation promoting grid modernization and incentives for decarbonization have fueled widespread deployments, while North American utilities leverage robust telecommunications networks to integrate near real-time analytics and demand response programs. Latin American markets, though emerging, are pursuing targeted pilot projects and public-private partnerships that lay the foundation for scaled data management initiatives.

Across Europe, the Middle East, and Africa, European Union directives on data privacy and interoperability have set high standards, prompting utilities to deploy unified platforms that support cross-border data exchange and harmonized security protocols. Gulf Cooperation Council nations are fast-tracking smart grid programs to bolster energy security and accommodate renewable integration, while African utilities are piloting solar and microgrid solutions supported by cloud-based data management to overcome infrastructure limitations. In the Asia-Pacific region, a blend of highly digitized markets and nascent economies drives a dual approach: mature markets invest heavily in analytics-driven operational optimization, whereas emerging nations prioritize cost-effective, scalable deployments that leapfrog legacy architectures.

Profiling Leading Innovators and Strategic Collaborators Shaping the Smart Meter Data Management Market Through Technology, Partnerships, and Service Excellence

A cadre of pioneering technology providers and systems integrators is propelling the smart meter data management market forward through a combination of innovation, strategic partnerships, and service excellence. Established metering specialists have enhanced their offerings with cloud-native analytics platforms, enabling seamless integration of data lakes and interoperability with enterprise resource planning systems. Global enterprise software vendors have introduced modular data management suites that unify billing, customer engagement, and grid operations on a single platform, reducing vendor sprawl and streamlining vendor management.

Leading startups and niche players are differentiating through targeted capabilities such as edge analytics appliances that preprocess data at remote sites, AI-driven anomaly detection engines, and advanced visualization portals optimized for mobile and web. Collaborative initiatives between hardware manufacturers, telecommunications carriers, and software developers are accelerating the rollout of secure, end-to-end solutions that address both technical complexity and evolving regulatory requirements. As incumbents and disruptors converge around open standards and developer ecosystems, end users benefit from an expanding palette of interoperable tools and specialized consulting services.

Action-Oriented Strategic Roadmap for Industry Leaders to Leverage Emerging Technologies, Optimize Operations, and Enhance Customer Value in Smart Meter Data Management

Industry leaders should prioritize a three-pronged approach to capitalize on the full spectrum of opportunities in smart meter data management. First, they must integrate advanced analytics frameworks that combine predictive modeling and machine learning to drive proactive maintenance, dynamic pricing strategies, and personalized customer engagement programs. Such capabilities yield quantifiable benefits in cost avoidance, revenue protection, and customer satisfaction.

Second, organizations should establish robust data governance and cybersecurity protocols that align with emerging regulatory mandates and industry best practices. This includes deploying encryption at rest and in transit, enforcing role-based access controls, and instituting continuous monitoring and incident response processes. Third, forging strategic partnerships across the value chain-spanning hardware vendors, software developers, telecommunications providers, and systems integrators-will accelerate time to value, reduce integration complexity, and foster co-innovation. By weaving these elements into a cohesive digital roadmap, decision-makers can unlock sustained performance gains and position themselves at the vanguard of utility transformation.

Transparent and Systematic Research Approach Leveraging Qualitative and Quantitative Techniques to Deliver Rigorous Insights into Smart Meter Data Management Trends

This report synthesizes findings from a rigorous research process that combines qualitative insights with quantitative analysis. Primary research involved in-depth interviews with senior utility executives, technology innovators, and regulatory experts to capture real-world perspectives and emerging trends. Secondary research drew upon a wide array of publicly available sources, including industry publications, regulatory filings, white papers, and academic studies, to validate and contextualize primary input.

Data triangulation was employed to reconcile diverse data points and ensure consistency across sources. Customizable financial models and scenario analyses were developed to assess the impact of key variables such as tariff adjustments, technology adoption rates, and regulatory shifts. Expert validation workshops with subject-matter authorities served to refine assumptions, validate methodologies, and stress-test conclusions. The result is a comprehensive, transparent framework designed to support strategic planning, investment decisions, and performance benchmarking.

Synthesis of Critical Findings and Forward-Looking Perspectives to Guide Decision-Makers in Navigating the Future of Smart Meter Data Management

The confluence of technological innovation, regulatory evolution, and market dynamics is reshaping the smart meter data management landscape, presenting both challenges and opportunities for utilities and service providers. As tariffs and supply chain complexities underscore the need for agile procurement and resilient architectures, emerging analytics capabilities promise unprecedented insights into operational performance and customer behavior. Regional distinctions highlight that success requires tailored strategies that account for local regulatory frameworks, infrastructure maturity, and investment capacity.

Ultimately, organizations that embrace an integrated approach-blending advanced analytics, robust governance, and strategic partnerships-will be best positioned to harness the transformative power of smart meter data. By aligning digital roadmaps with actionable insights and fostering a culture of continuous innovation, decision-makers can navigate uncertainty, unlock new value streams, and drive sustainable growth in an increasingly data-centric utility ecosystem.

Table of Contents

1. Preface

- 1.1. Objectives of the Study

- 1.2. Market Segmentation & Coverage

- 1.3. Years Considered for the Study

- 1.4. Currency & Pricing

- 1.5. Language

- 1.6. Stakeholders

2. Research Methodology

- 2.1. Define: Research Objective

- 2.2. Determine: Research Design

- 2.3. Prepare: Research Instrument

- 2.4. Collect: Data Source

- 2.5. Analyze: Data Interpretation

- 2.6. Formulate: Data Verification

- 2.7. Publish: Research Report

- 2.8. Repeat: Report Update

3. Executive Summary

4. Market Overview

- 4.1. Introduction

- 4.2. Market Sizing & Forecasting

5. Market Dynamics

- 5.1. AI-driven predictive analytics frameworks for real-time energy load forecasting and balancing

- 5.2. Accelerated shift toward cloud-based smart meter data management solutions

- 5.3. Integration of edge computing modules into smart meter infrastructures for instantaneous anomaly detection

- 5.4. Deployment of blockchain-based architectures to secure smart meter telemetry and customer billing data

- 5.5. MDM system integration with distributed energy resources and EV charging networks

- 5.6. Implementation of GDPR and CCPA aligned privacy controls in advanced metering infrastructure data management systems

6. Market Insights

- 6.1. Porter's Five Forces Analysis

- 6.2. PESTLE Analysis

7. Cumulative Impact of United States Tariffs 2025

8. Smart Meter Data Management Market, by Offering

- 8.1. Introduction

- 8.2. Services

- 8.2.1. Managed Services

- 8.2.2. Professional Services

- 8.3. Software

9. Smart Meter Data Management Market, by Functionality

- 9.1. Introduction

- 9.2. Data Collection & Acquisition

- 9.3. Data Processing & Analysis

- 9.4. Data Storage & Management

- 9.5. Data Visualization & Reporting

10. Smart Meter Data Management Market, by Deployment Model

- 10.1. Introduction

- 10.2. Cloud-Based Solutions

- 10.3. Hybrid Solutions

- 10.4. On-Premises Solutions

11. Smart Meter Data Management Market, by Application

- 11.1. Introduction

- 11.2. Billing & Revenue Management

- 11.3. Energy Consumption Monitoring

- 11.4. Smart Grid Optimization

12. Smart Meter Data Management Market, by User Type

- 12.1. Introduction

- 12.2. Commercial

- 12.3. Industrial

- 12.4. Residential

13. Smart Meter Data Management Market, by Utilities

- 13.1. Introduction

- 13.2. Electricity Utilities

- 13.3. Gas Utilities

- 13.4. Water Utilities

14. Americas Smart Meter Data Management Market

- 14.1. Introduction

- 14.2. United States

- 14.3. Canada

- 14.4. Mexico

- 14.5. Brazil

- 14.6. Argentina

15. Europe, Middle East & Africa Smart Meter Data Management Market

- 15.1. Introduction

- 15.2. United Kingdom

- 15.3. Germany

- 15.4. France

- 15.5. Russia

- 15.6. Italy

- 15.7. Spain

- 15.8. United Arab Emirates

- 15.9. Saudi Arabia

- 15.10. South Africa

- 15.11. Denmark

- 15.12. Netherlands

- 15.13. Qatar

- 15.14. Finland

- 15.15. Sweden

- 15.16. Nigeria

- 15.17. Egypt

- 15.18. Turkey

- 15.19. Israel

- 15.20. Norway

- 15.21. Poland

- 15.22. Switzerland

16. Asia-Pacific Smart Meter Data Management Market

- 16.1. Introduction

- 16.2. China

- 16.3. India

- 16.4. Japan

- 16.5. Australia

- 16.6. South Korea

- 16.7. Indonesia

- 16.8. Thailand

- 16.9. Philippines

- 16.10. Malaysia

- 16.11. Singapore

- 16.12. Vietnam

- 16.13. Taiwan

17. Competitive Landscape

- 17.1. Market Share Analysis, 2024

- 17.2. FPNV Positioning Matrix, 2024

- 17.3. Competitive Analysis

- 17.3.1. Amazon Web Services, Inc.

- 17.3.2. Diehl Stiftung & Co. KG

- 17.3.3. Eaton Corporation PLC

- 17.3.4. Hansen Technologies Limited by Roper Technologies

- 17.3.5. International Business Machines Corporation

- 17.3.6. Itron, Inc.

- 17.3.7. NEC Corporation

- 17.3.8. Oracle Corporation

- 17.3.9. Robotron Datenbank-Software GmbH

- 17.3.10. SAP SE

- 17.3.11. Schneider Electric SE

- 17.3.12. Siemens AG

- 17.3.13. Toshiba Corporation

- 17.3.14. Xylem, Inc.