|

|

市場調査レポート

商品コード

1803709

半導体ICテストハンドラの世界市場:ハンドラタイプ、テストステージ、温度範囲、用途、エンドユーザー別-2025-2030年予測Semiconductor IC Test Handler Market by Handler Type, Test Stage, Temperature Range, Application, End-User - Global Forecast 2025-2030 |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 半導体ICテストハンドラの世界市場:ハンドラタイプ、テストステージ、温度範囲、用途、エンドユーザー別-2025-2030年予測 |

|

出版日: 2025年08月28日

発行: 360iResearch

ページ情報: 英文 182 Pages

納期: 即日から翌営業日

|

全表示

- 概要

- 図表

- 目次

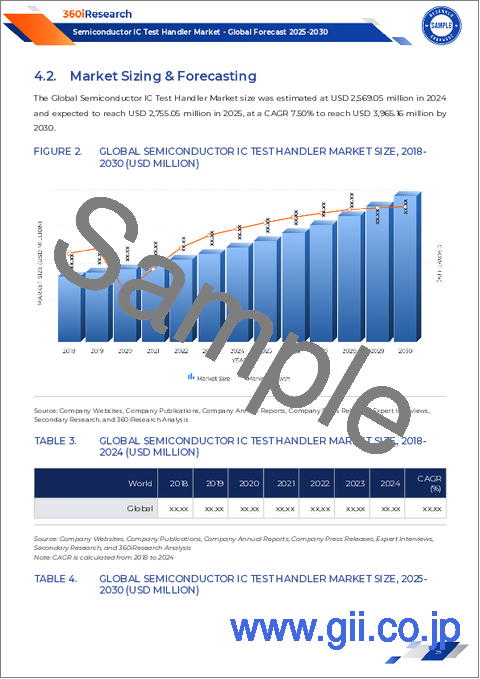

半導体ICテストハンドラ市場は、2024年には25億6,000万米ドルとなり、2025年には27億4,000万米ドル、CAGR 7.50%で成長し、2030年には39億5,000万米ドルに達すると予測されています。

| 主な市場の統計 | |

|---|---|

| 基準年2024 | 25億6,000万米ドル |

| 推定年2025 | 27億4,000万米ドル |

| 予測年2030 | 39億5,000万米ドル |

| CAGR(%) | 7.50% |

半導体ICテストハンドラの包括的なイントロダクションより、主要市場力学と戦略的重要性が明らかになる

半導体産業の進化は、ウエハー製造と最終品質保証の重要な橋渡し役であるテストハンドラーの精度と信頼性にかかっています。近年、デバイスアーキテクチャの多様化、テスト量の急増、性能要件の厳格化に伴い、これらの自動化システムは大きな変貌を遂げています。このような背景から、ICテスト・ハンドラ開発を形作る動作原理、技術革新、戦略的動向を理解することは、スループットの最適化、テスト・コストの最小化、最高品質基準の維持を目指す意思決定者にとって不可欠です。

持続可能で適応性のあるソリューションで半導体ICテスト・ハンドラの状況を形成する、前例のない技術と運用の変化

ここ数年、半導体ICテスト・ハンドラの分野では、技術革新と顧客要求の進化の両方が原動力となり、変革的なシフトが起きています。異種集積を特徴とする開発デバイスは、ウエハ・プロービングと最終的なシステムレベル評価の間をシームレスに移行できるテスト・ハンドラを必要とするようになり、サプライヤはモジュール式プラットフォームの開発を促しています。同時に、より高いスループットを求める動きが自動化の進歩を加速させ、ロボットアームの精度や並列テストアーキテクチャが標準機能となっています。

2025年米国関税制度が半導体ICテストハンドラーサプライチェーンに与える包括的影響の深層分析

米国が2025年に改正関税を発動したことで、半導体ICテストハンドラ分野を支えるサプライチェーンに大きな複雑さがもたらされました。特定の地域から調達される部品には高い関税が課されるようになり、メーカーやエンドユーザーは調達戦略の見直しを迫られています。多くのサプライヤーは、より関税の低い地域の代替ベンダーを探したり、コスト圧力を緩和するために現地生産を増やしたりしています。

ハンドラーのタイプ、テストステージ、温度範囲、用途、エンドユーザーが戦略的購買をどのように形成するかを明らかにする市場セグメンテーションの洞察に満ちた検討

市場セグメンテーションを理解することは、テストハンドラーの能力を多様な業務ニーズに合致させるために極めて重要です。ハンドラータイプを評価する際には、より穏やかなデバイスローディングを得意とするグラビティハンドラーや、並列処理を最大化するハイスループットハンドラーが提供する明確な利点を認識することが不可欠です。ピック・アンド・プレース・ハンドラーは、混合されたデバイス・ポートフォリオに対する柔軟性に貢献し、タレット・ハンドラーは、特殊な試験プロトコルのための正確な方向制御を保証します。各ハンドラーのカテゴリーには、購入の判断材料となる独自の設計と性能のトレードオフがあります。

南北アメリカ、中東・アフリカ、アジア太平洋がテストハンドラの革新と需要パターンをどのように牽引しているかを示す包括的な地域別洞察

地域ダイナミックスは、半導体ICテストハンドラの採用と技術革新に強力な影響を及ぼします。南北アメリカでは、次世代車載センサとエッジコンピューティングデバイスに重点が置かれ、厳格な信頼性スクリーニングと迅速な展開が可能なハンドラへの需要が高まっています。北米の研究クラスタも、リアルタイムの異常検出のための機械学習を統合した新しいハンドラアーキテクチャを探求しており、この地域をインテリジェントテストソリューションの最前線に位置付けています。

革新、サービスネットワーク、戦略的提携がいかに市場リーダーシップを定義するかを示す業界大手企業の詳細分析

大手装置プロバイダーは、絶え間ないイノベーション、戦略的パートナーシップ、グローバルサービスネットワークを通じて、ICテストハンドラ市場の軌道を形成しています。これらの企業は研究開発に多額の投資を行い、精密ロボット工学、熱均一性、統合診断などの機能強化に注力しています。また、アップグレードを簡素化し、エンドユーザーの総所有コストを削減するモジュラー・アーキテクチャを提供することで差別化を図っています。

技術とパートナーシップを通じてテストハンドラの回復力、効率性、持続可能性を強化するための業界リーダーへの実行可能な戦略的提言

複雑な半導体ICテストハンドラ環境を乗り切るために、業界リーダーは多方面からの戦略的アプローチを採用すべきです。まず、ハンドラ・プラットフォームに予測分析を統合することで、性能低下を先取りし、メンテナンス・スケジュールを最適化することができます。ロボットシステムとサーマルモジュール全体にAI対応モニタリングを導入することで、企業はダウンタイムを最小限に抑え、資産寿命を延ばすことができます。

信頼性の高い市場洞察のための1次インタビュー、2次データ分析、テーマ別統合を概説する堅牢なマルチモーダル調査手法

本調査手法では、半導体ICテストハンドラ市場の全体像を把握するため、1次調査と2次調査を組み合わせた厳密な調査手法を採用しました。一次的な洞察は、装置メーカー、テストエンジニアリングリーダー、調達スペシャリストとのインタビューを通じて収集しました。これらの対話を通じて、現在の課題、技術採用パターン、将来の投資優先順位などを探り、分析に質的な深みを与えています。

進化するテストハンドラ業界で成功するための柱として、敏捷性、地域性、統合エコシステムを重視した戦略的結論

半導体ICテストハンドラ領域は、急速な技術進歩、進化する規制状況、貿易政策のシフトの影響を受け、極めて重要な岐路に立たされています。市場参入企業は、複雑化するデバイスアーキテクチャの要求に応えるため、モジュール設計とAI主導のアナリティクスを活用し、俊敏性を維持しなければならないです。同時に、戦略的なサプライチェーンの多様化と現地生産化は、関税リスクを軽減し、タイムリーな納入を確保するために不可欠となります。

目次

第1章 序文

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場の概要

第5章 市場力学

- リアルタイムICテストハンドラーの歩留まり最適化のための機械学習アルゴリズムの統合

- パーティクル汚染リスクを最小限に抑えるための真空ベースのウエハーハンドリング技術の採用

- 大量ICスループット要件を満たすマルチサイト並列テストアーキテクチャの開発

- 高度な半導体テストキャリブレーションのための現場熱監視モジュールの実装

- ミックスドシグナルおよびRF ICテストアプリケーションをサポートするユニバーサルハンドラープラットフォームへの移行

- ICテスト装置におけるIoT対応のリモート診断と予知保全の出現

- ファンアウトウェーハを含む異種パッケージタイプ向けのハンドラーインターフェースのカスタマイズ

- ロボットと自動誘導車両の統合により、ICテストハンドラーの物流をシームレスに

第6章 市場洞察

- ポーターのファイブフォース分析

- PESTEL分析

第7章 米国の関税の累積的な影響2025

第8章 半導体ICテストハンドラ市場ハンドラータイプ別

- 重力ハンドラー

- 高スループットハンドラー

- ピックアンドプレースハンドラー

- タレットハンドラー

第9章 半導体ICテストハンドラ市場テストステージ別

- 最終テスト(FT)

- システムレベルテスト(SLT)

- ウエハーテスト(プロービング)

第10章 半導体ICテストハンドラ市場温度範囲別

- 常温ハンドラー

- コールドテストハンドラー

- 拡張範囲ハンドラー

- ホットテストハンドラー

- トライテンプハンドラー

第11章 半導体ICテストハンドラ市場:用途別

- アナログ・デバイセズ

- ロジックおよびメモリデバイス

- ミックスドシグナルIC

- パワーデバイスとMEMS

- RFデバイス

第12章 半導体ICテストハンドラ市場:エンドユーザー別

- IDM(統合デバイスメーカー)

- OSAT(アウトソーシングパッケージングおよびテストプロバイダー)

- 研究開発機関およびパッケージングプロバイダー

第13章 南北アメリカの半導体ICテストハンドラ市場

- 米国

- カナダ

- メキシコ

- ブラジル

- アルゼンチン

第14章 欧州・中東・アフリカの半導体ICテストハンドラ市場

- 英国

- ドイツ

- フランス

- ロシア

- イタリア

- スペイン

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- デンマーク

- オランダ

- カタール

- フィンランド

- スウェーデン

- ナイジェリア

- エジプト

- トルコ

- イスラエル

- ノルウェー

- ポーランド

- スイス

第15章 アジア太平洋地域の半導体ICテストハンドラ市場

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- インドネシア

- タイ

- フィリピン

- マレーシア

- シンガポール

- ベトナム

- 台湾

第16章 競合情勢

- 市場シェア分析, 2024

- FPNVポジショニングマトリックス, 2024

- 競合分析

- Advantest Corporation

- Cohu, Inc.

- 4JMSolutions(Malta)Ltd.

- Amfax Limited

- Boston Semi Equipment

- Chroma ATE Inc.

- esmo AG

- Hangzhou Changchuan Technology Co., Ltd.

- Hon Precision, Inc.

- Innogrity Pte Ltd

- Kanematsu Corporation

- Komachine Inc.

- MICRONICS JAPAN CO.,LTD.

- SMTmax

- SPEA S.p.A.

- SYNAX Co., Ltd.

- Teradyne, Inc.

- TESEC Corporation

- Tianjin JHT Design Co., Ltd.

- UENO SEIKI CO.,LTD.

- YAC Systems Singapore Pte.

- Yamaichi Electronics Co., Ltd.

- YoungTek Electronics Corp.

第17章 リサーチAI

第18章 リサーチ統計

第19章 リサーチコンタクト

第20章 リサーチ記事

第21章 付録

LIST OF FIGURES

- FIGURE 1. SEMICONDUCTOR IC TEST HANDLER MARKET RESEARCH PROCESS

- FIGURE 2. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, 2018-2030 (USD MILLION)

- FIGURE 3. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY REGION, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 4. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY COUNTRY, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 5. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2024 VS 2030 (%)

- FIGURE 6. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 7. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2024 VS 2030 (%)

- FIGURE 8. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 9. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2024 VS 2030 (%)

- FIGURE 10. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 11. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2024 VS 2030 (%)

- FIGURE 12. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 13. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2024 VS 2030 (%)

- FIGURE 14. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 15. AMERICAS SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY COUNTRY, 2024 VS 2030 (%)

- FIGURE 16. AMERICAS SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY COUNTRY, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 17. UNITED STATES SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY STATE, 2024 VS 2030 (%)

- FIGURE 18. UNITED STATES SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY STATE, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 19. EUROPE, MIDDLE EAST & AFRICA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY COUNTRY, 2024 VS 2030 (%)

- FIGURE 20. EUROPE, MIDDLE EAST & AFRICA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY COUNTRY, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 21. ASIA-PACIFIC SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY COUNTRY, 2024 VS 2030 (%)

- FIGURE 22. ASIA-PACIFIC SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY COUNTRY, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 23. SEMICONDUCTOR IC TEST HANDLER MARKET SHARE, BY KEY PLAYER, 2024

- FIGURE 24. SEMICONDUCTOR IC TEST HANDLER MARKET, FPNV POSITIONING MATRIX, 2024

- FIGURE 25. SEMICONDUCTOR IC TEST HANDLER MARKET: RESEARCHAI

- FIGURE 26. SEMICONDUCTOR IC TEST HANDLER MARKET: RESEARCHSTATISTICS

- FIGURE 27. SEMICONDUCTOR IC TEST HANDLER MARKET: RESEARCHCONTACTS

- FIGURE 28. SEMICONDUCTOR IC TEST HANDLER MARKET: RESEARCHARTICLES

LIST OF TABLES

- TABLE 1. SEMICONDUCTOR IC TEST HANDLER MARKET SEGMENTATION & COVERAGE

- TABLE 2. UNITED STATES DOLLAR EXCHANGE RATE, 2018-2024

- TABLE 3. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, 2018-2024 (USD MILLION)

- TABLE 4. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, 2025-2030 (USD MILLION)

- TABLE 5. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY REGION, 2018-2024 (USD MILLION)

- TABLE 6. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY REGION, 2025-2030 (USD MILLION)

- TABLE 7. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY COUNTRY, 2018-2024 (USD MILLION)

- TABLE 8. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 9. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2018-2024 (USD MILLION)

- TABLE 10. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2025-2030 (USD MILLION)

- TABLE 11. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY GRAVITY HANDLERS, BY REGION, 2018-2024 (USD MILLION)

- TABLE 12. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY GRAVITY HANDLERS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 13. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HIGH-THROUGHPUT HANDLERS, BY REGION, 2018-2024 (USD MILLION)

- TABLE 14. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HIGH-THROUGHPUT HANDLERS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 15. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY PICK-AND-PLACE HANDLERS, BY REGION, 2018-2024 (USD MILLION)

- TABLE 16. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY PICK-AND-PLACE HANDLERS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 17. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TURRET HANDLERS, BY REGION, 2018-2024 (USD MILLION)

- TABLE 18. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TURRET HANDLERS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 19. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2018-2024 (USD MILLION)

- TABLE 20. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2025-2030 (USD MILLION)

- TABLE 21. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY FINAL TEST (FT), BY REGION, 2018-2024 (USD MILLION)

- TABLE 22. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY FINAL TEST (FT), BY REGION, 2025-2030 (USD MILLION)

- TABLE 23. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY SYSTEM-LEVEL TEST (SLT), BY REGION, 2018-2024 (USD MILLION)

- TABLE 24. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY SYSTEM-LEVEL TEST (SLT), BY REGION, 2025-2030 (USD MILLION)

- TABLE 25. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY WAFER TEST (PROBING), BY REGION, 2018-2024 (USD MILLION)

- TABLE 26. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY WAFER TEST (PROBING), BY REGION, 2025-2030 (USD MILLION)

- TABLE 27. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2018-2024 (USD MILLION)

- TABLE 28. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2025-2030 (USD MILLION)

- TABLE 29. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY AMBIENT TEMPERATURE HANDLERS, BY REGION, 2018-2024 (USD MILLION)

- TABLE 30. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY AMBIENT TEMPERATURE HANDLERS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 31. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY COLD TEST HANDLERS, BY REGION, 2018-2024 (USD MILLION)

- TABLE 32. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY COLD TEST HANDLERS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 33. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY EXTENDED RANGE HANDLERS, BY REGION, 2018-2024 (USD MILLION)

- TABLE 34. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY EXTENDED RANGE HANDLERS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 35. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HOT TEST HANDLERS, BY REGION, 2018-2024 (USD MILLION)

- TABLE 36. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HOT TEST HANDLERS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 37. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TRI-TEMP HANDLERS, BY REGION, 2018-2024 (USD MILLION)

- TABLE 38. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TRI-TEMP HANDLERS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 39. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 40. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 41. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY ANALOG DEVICES, BY REGION, 2018-2024 (USD MILLION)

- TABLE 42. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY ANALOG DEVICES, BY REGION, 2025-2030 (USD MILLION)

- TABLE 43. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY LOGIC & MEMORY DEVICES, BY REGION, 2018-2024 (USD MILLION)

- TABLE 44. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY LOGIC & MEMORY DEVICES, BY REGION, 2025-2030 (USD MILLION)

- TABLE 45. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY MIXED-SIGNAL ICS, BY REGION, 2018-2024 (USD MILLION)

- TABLE 46. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY MIXED-SIGNAL ICS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 47. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY POWER DEVICES & MEMS, BY REGION, 2018-2024 (USD MILLION)

- TABLE 48. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY POWER DEVICES & MEMS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 49. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY RF DEVICES, BY REGION, 2018-2024 (USD MILLION)

- TABLE 50. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY RF DEVICES, BY REGION, 2025-2030 (USD MILLION)

- TABLE 51. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2018-2024 (USD MILLION)

- TABLE 52. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2025-2030 (USD MILLION)

- TABLE 53. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY IDMS (INTEGRATED DEVICE MANUFACTURERS), BY REGION, 2018-2024 (USD MILLION)

- TABLE 54. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY IDMS (INTEGRATED DEVICE MANUFACTURERS), BY REGION, 2025-2030 (USD MILLION)

- TABLE 55. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY OSATS (OUTSOURCED PACKAGING & TEST PROVIDERS), BY REGION, 2018-2024 (USD MILLION)

- TABLE 56. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY OSATS (OUTSOURCED PACKAGING & TEST PROVIDERS), BY REGION, 2025-2030 (USD MILLION)

- TABLE 57. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY R&D INSTITUTIONS AND PACKAGING PROVIDERS, BY REGION, 2018-2024 (USD MILLION)

- TABLE 58. GLOBAL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY R&D INSTITUTIONS AND PACKAGING PROVIDERS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 59. AMERICAS SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2018-2024 (USD MILLION)

- TABLE 60. AMERICAS SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2025-2030 (USD MILLION)

- TABLE 61. AMERICAS SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2018-2024 (USD MILLION)

- TABLE 62. AMERICAS SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2025-2030 (USD MILLION)

- TABLE 63. AMERICAS SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2018-2024 (USD MILLION)

- TABLE 64. AMERICAS SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2025-2030 (USD MILLION)

- TABLE 65. AMERICAS SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 66. AMERICAS SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 67. AMERICAS SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2018-2024 (USD MILLION)

- TABLE 68. AMERICAS SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2025-2030 (USD MILLION)

- TABLE 69. AMERICAS SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY COUNTRY, 2018-2024 (USD MILLION)

- TABLE 70. AMERICAS SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 71. UNITED STATES SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2018-2024 (USD MILLION)

- TABLE 72. UNITED STATES SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2025-2030 (USD MILLION)

- TABLE 73. UNITED STATES SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2018-2024 (USD MILLION)

- TABLE 74. UNITED STATES SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2025-2030 (USD MILLION)

- TABLE 75. UNITED STATES SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2018-2024 (USD MILLION)

- TABLE 76. UNITED STATES SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2025-2030 (USD MILLION)

- TABLE 77. UNITED STATES SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 78. UNITED STATES SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 79. UNITED STATES SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2018-2024 (USD MILLION)

- TABLE 80. UNITED STATES SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2025-2030 (USD MILLION)

- TABLE 81. UNITED STATES SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY STATE, 2018-2024 (USD MILLION)

- TABLE 82. UNITED STATES SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY STATE, 2025-2030 (USD MILLION)

- TABLE 83. CANADA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2018-2024 (USD MILLION)

- TABLE 84. CANADA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2025-2030 (USD MILLION)

- TABLE 85. CANADA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2018-2024 (USD MILLION)

- TABLE 86. CANADA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2025-2030 (USD MILLION)

- TABLE 87. CANADA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2018-2024 (USD MILLION)

- TABLE 88. CANADA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2025-2030 (USD MILLION)

- TABLE 89. CANADA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 90. CANADA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 91. CANADA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2018-2024 (USD MILLION)

- TABLE 92. CANADA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2025-2030 (USD MILLION)

- TABLE 93. MEXICO SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2018-2024 (USD MILLION)

- TABLE 94. MEXICO SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2025-2030 (USD MILLION)

- TABLE 95. MEXICO SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2018-2024 (USD MILLION)

- TABLE 96. MEXICO SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2025-2030 (USD MILLION)

- TABLE 97. MEXICO SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2018-2024 (USD MILLION)

- TABLE 98. MEXICO SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2025-2030 (USD MILLION)

- TABLE 99. MEXICO SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 100. MEXICO SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 101. MEXICO SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2018-2024 (USD MILLION)

- TABLE 102. MEXICO SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2025-2030 (USD MILLION)

- TABLE 103. BRAZIL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2018-2024 (USD MILLION)

- TABLE 104. BRAZIL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2025-2030 (USD MILLION)

- TABLE 105. BRAZIL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2018-2024 (USD MILLION)

- TABLE 106. BRAZIL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2025-2030 (USD MILLION)

- TABLE 107. BRAZIL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2018-2024 (USD MILLION)

- TABLE 108. BRAZIL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2025-2030 (USD MILLION)

- TABLE 109. BRAZIL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 110. BRAZIL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 111. BRAZIL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2018-2024 (USD MILLION)

- TABLE 112. BRAZIL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2025-2030 (USD MILLION)

- TABLE 113. ARGENTINA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2018-2024 (USD MILLION)

- TABLE 114. ARGENTINA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2025-2030 (USD MILLION)

- TABLE 115. ARGENTINA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2018-2024 (USD MILLION)

- TABLE 116. ARGENTINA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2025-2030 (USD MILLION)

- TABLE 117. ARGENTINA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2018-2024 (USD MILLION)

- TABLE 118. ARGENTINA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2025-2030 (USD MILLION)

- TABLE 119. ARGENTINA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 120. ARGENTINA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 121. ARGENTINA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2018-2024 (USD MILLION)

- TABLE 122. ARGENTINA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2025-2030 (USD MILLION)

- TABLE 123. EUROPE, MIDDLE EAST & AFRICA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2018-2024 (USD MILLION)

- TABLE 124. EUROPE, MIDDLE EAST & AFRICA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2025-2030 (USD MILLION)

- TABLE 125. EUROPE, MIDDLE EAST & AFRICA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2018-2024 (USD MILLION)

- TABLE 126. EUROPE, MIDDLE EAST & AFRICA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2025-2030 (USD MILLION)

- TABLE 127. EUROPE, MIDDLE EAST & AFRICA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2018-2024 (USD MILLION)

- TABLE 128. EUROPE, MIDDLE EAST & AFRICA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2025-2030 (USD MILLION)

- TABLE 129. EUROPE, MIDDLE EAST & AFRICA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 130. EUROPE, MIDDLE EAST & AFRICA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 131. EUROPE, MIDDLE EAST & AFRICA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2018-2024 (USD MILLION)

- TABLE 132. EUROPE, MIDDLE EAST & AFRICA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2025-2030 (USD MILLION)

- TABLE 133. EUROPE, MIDDLE EAST & AFRICA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY COUNTRY, 2018-2024 (USD MILLION)

- TABLE 134. EUROPE, MIDDLE EAST & AFRICA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 135. UNITED KINGDOM SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2018-2024 (USD MILLION)

- TABLE 136. UNITED KINGDOM SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2025-2030 (USD MILLION)

- TABLE 137. UNITED KINGDOM SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2018-2024 (USD MILLION)

- TABLE 138. UNITED KINGDOM SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2025-2030 (USD MILLION)

- TABLE 139. UNITED KINGDOM SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2018-2024 (USD MILLION)

- TABLE 140. UNITED KINGDOM SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2025-2030 (USD MILLION)

- TABLE 141. UNITED KINGDOM SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 142. UNITED KINGDOM SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 143. UNITED KINGDOM SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2018-2024 (USD MILLION)

- TABLE 144. UNITED KINGDOM SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2025-2030 (USD MILLION)

- TABLE 145. GERMANY SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2018-2024 (USD MILLION)

- TABLE 146. GERMANY SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2025-2030 (USD MILLION)

- TABLE 147. GERMANY SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2018-2024 (USD MILLION)

- TABLE 148. GERMANY SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2025-2030 (USD MILLION)

- TABLE 149. GERMANY SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2018-2024 (USD MILLION)

- TABLE 150. GERMANY SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2025-2030 (USD MILLION)

- TABLE 151. GERMANY SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 152. GERMANY SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 153. GERMANY SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2018-2024 (USD MILLION)

- TABLE 154. GERMANY SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2025-2030 (USD MILLION)

- TABLE 155. FRANCE SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2018-2024 (USD MILLION)

- TABLE 156. FRANCE SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2025-2030 (USD MILLION)

- TABLE 157. FRANCE SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2018-2024 (USD MILLION)

- TABLE 158. FRANCE SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2025-2030 (USD MILLION)

- TABLE 159. FRANCE SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2018-2024 (USD MILLION)

- TABLE 160. FRANCE SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2025-2030 (USD MILLION)

- TABLE 161. FRANCE SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 162. FRANCE SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 163. FRANCE SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2018-2024 (USD MILLION)

- TABLE 164. FRANCE SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2025-2030 (USD MILLION)

- TABLE 165. RUSSIA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2018-2024 (USD MILLION)

- TABLE 166. RUSSIA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2025-2030 (USD MILLION)

- TABLE 167. RUSSIA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2018-2024 (USD MILLION)

- TABLE 168. RUSSIA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2025-2030 (USD MILLION)

- TABLE 169. RUSSIA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2018-2024 (USD MILLION)

- TABLE 170. RUSSIA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2025-2030 (USD MILLION)

- TABLE 171. RUSSIA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 172. RUSSIA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 173. RUSSIA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2018-2024 (USD MILLION)

- TABLE 174. RUSSIA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2025-2030 (USD MILLION)

- TABLE 175. ITALY SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2018-2024 (USD MILLION)

- TABLE 176. ITALY SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2025-2030 (USD MILLION)

- TABLE 177. ITALY SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2018-2024 (USD MILLION)

- TABLE 178. ITALY SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2025-2030 (USD MILLION)

- TABLE 179. ITALY SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2018-2024 (USD MILLION)

- TABLE 180. ITALY SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2025-2030 (USD MILLION)

- TABLE 181. ITALY SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 182. ITALY SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 183. ITALY SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2018-2024 (USD MILLION)

- TABLE 184. ITALY SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2025-2030 (USD MILLION)

- TABLE 185. SPAIN SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2018-2024 (USD MILLION)

- TABLE 186. SPAIN SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2025-2030 (USD MILLION)

- TABLE 187. SPAIN SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2018-2024 (USD MILLION)

- TABLE 188. SPAIN SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2025-2030 (USD MILLION)

- TABLE 189. SPAIN SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2018-2024 (USD MILLION)

- TABLE 190. SPAIN SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2025-2030 (USD MILLION)

- TABLE 191. SPAIN SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 192. SPAIN SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 193. SPAIN SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2018-2024 (USD MILLION)

- TABLE 194. SPAIN SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2025-2030 (USD MILLION)

- TABLE 195. UNITED ARAB EMIRATES SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2018-2024 (USD MILLION)

- TABLE 196. UNITED ARAB EMIRATES SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2025-2030 (USD MILLION)

- TABLE 197. UNITED ARAB EMIRATES SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2018-2024 (USD MILLION)

- TABLE 198. UNITED ARAB EMIRATES SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2025-2030 (USD MILLION)

- TABLE 199. UNITED ARAB EMIRATES SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2018-2024 (USD MILLION)

- TABLE 200. UNITED ARAB EMIRATES SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2025-2030 (USD MILLION)

- TABLE 201. UNITED ARAB EMIRATES SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 202. UNITED ARAB EMIRATES SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 203. UNITED ARAB EMIRATES SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2018-2024 (USD MILLION)

- TABLE 204. UNITED ARAB EMIRATES SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2025-2030 (USD MILLION)

- TABLE 205. SAUDI ARABIA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2018-2024 (USD MILLION)

- TABLE 206. SAUDI ARABIA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2025-2030 (USD MILLION)

- TABLE 207. SAUDI ARABIA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2018-2024 (USD MILLION)

- TABLE 208. SAUDI ARABIA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2025-2030 (USD MILLION)

- TABLE 209. SAUDI ARABIA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2018-2024 (USD MILLION)

- TABLE 210. SAUDI ARABIA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2025-2030 (USD MILLION)

- TABLE 211. SAUDI ARABIA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 212. SAUDI ARABIA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 213. SAUDI ARABIA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2018-2024 (USD MILLION)

- TABLE 214. SAUDI ARABIA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2025-2030 (USD MILLION)

- TABLE 215. SOUTH AFRICA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2018-2024 (USD MILLION)

- TABLE 216. SOUTH AFRICA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2025-2030 (USD MILLION)

- TABLE 217. SOUTH AFRICA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2018-2024 (USD MILLION)

- TABLE 218. SOUTH AFRICA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2025-2030 (USD MILLION)

- TABLE 219. SOUTH AFRICA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2018-2024 (USD MILLION)

- TABLE 220. SOUTH AFRICA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2025-2030 (USD MILLION)

- TABLE 221. SOUTH AFRICA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 222. SOUTH AFRICA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 223. SOUTH AFRICA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2018-2024 (USD MILLION)

- TABLE 224. SOUTH AFRICA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2025-2030 (USD MILLION)

- TABLE 225. DENMARK SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2018-2024 (USD MILLION)

- TABLE 226. DENMARK SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2025-2030 (USD MILLION)

- TABLE 227. DENMARK SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2018-2024 (USD MILLION)

- TABLE 228. DENMARK SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2025-2030 (USD MILLION)

- TABLE 229. DENMARK SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2018-2024 (USD MILLION)

- TABLE 230. DENMARK SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2025-2030 (USD MILLION)

- TABLE 231. DENMARK SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 232. DENMARK SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 233. DENMARK SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2018-2024 (USD MILLION)

- TABLE 234. DENMARK SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2025-2030 (USD MILLION)

- TABLE 235. NETHERLANDS SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2018-2024 (USD MILLION)

- TABLE 236. NETHERLANDS SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2025-2030 (USD MILLION)

- TABLE 237. NETHERLANDS SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2018-2024 (USD MILLION)

- TABLE 238. NETHERLANDS SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2025-2030 (USD MILLION)

- TABLE 239. NETHERLANDS SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2018-2024 (USD MILLION)

- TABLE 240. NETHERLANDS SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2025-2030 (USD MILLION)

- TABLE 241. NETHERLANDS SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 242. NETHERLANDS SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 243. NETHERLANDS SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2018-2024 (USD MILLION)

- TABLE 244. NETHERLANDS SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2025-2030 (USD MILLION)

- TABLE 245. QATAR SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2018-2024 (USD MILLION)

- TABLE 246. QATAR SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2025-2030 (USD MILLION)

- TABLE 247. QATAR SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2018-2024 (USD MILLION)

- TABLE 248. QATAR SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2025-2030 (USD MILLION)

- TABLE 249. QATAR SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2018-2024 (USD MILLION)

- TABLE 250. QATAR SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2025-2030 (USD MILLION)

- TABLE 251. QATAR SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 252. QATAR SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 253. QATAR SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2018-2024 (USD MILLION)

- TABLE 254. QATAR SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2025-2030 (USD MILLION)

- TABLE 255. FINLAND SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2018-2024 (USD MILLION)

- TABLE 256. FINLAND SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2025-2030 (USD MILLION)

- TABLE 257. FINLAND SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2018-2024 (USD MILLION)

- TABLE 258. FINLAND SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2025-2030 (USD MILLION)

- TABLE 259. FINLAND SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2018-2024 (USD MILLION)

- TABLE 260. FINLAND SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2025-2030 (USD MILLION)

- TABLE 261. FINLAND SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 262. FINLAND SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 263. FINLAND SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2018-2024 (USD MILLION)

- TABLE 264. FINLAND SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2025-2030 (USD MILLION)

- TABLE 265. SWEDEN SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2018-2024 (USD MILLION)

- TABLE 266. SWEDEN SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2025-2030 (USD MILLION)

- TABLE 267. SWEDEN SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2018-2024 (USD MILLION)

- TABLE 268. SWEDEN SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2025-2030 (USD MILLION)

- TABLE 269. SWEDEN SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2018-2024 (USD MILLION)

- TABLE 270. SWEDEN SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2025-2030 (USD MILLION)

- TABLE 271. SWEDEN SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 272. SWEDEN SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 273. SWEDEN SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2018-2024 (USD MILLION)

- TABLE 274. SWEDEN SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2025-2030 (USD MILLION)

- TABLE 275. NIGERIA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2018-2024 (USD MILLION)

- TABLE 276. NIGERIA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2025-2030 (USD MILLION)

- TABLE 277. NIGERIA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2018-2024 (USD MILLION)

- TABLE 278. NIGERIA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2025-2030 (USD MILLION)

- TABLE 279. NIGERIA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2018-2024 (USD MILLION)

- TABLE 280. NIGERIA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2025-2030 (USD MILLION)

- TABLE 281. NIGERIA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 282. NIGERIA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 283. NIGERIA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2018-2024 (USD MILLION)

- TABLE 284. NIGERIA SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2025-2030 (USD MILLION)

- TABLE 285. EGYPT SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2018-2024 (USD MILLION)

- TABLE 286. EGYPT SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2025-2030 (USD MILLION)

- TABLE 287. EGYPT SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2018-2024 (USD MILLION)

- TABLE 288. EGYPT SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2025-2030 (USD MILLION)

- TABLE 289. EGYPT SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2018-2024 (USD MILLION)

- TABLE 290. EGYPT SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2025-2030 (USD MILLION)

- TABLE 291. EGYPT SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 292. EGYPT SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 293. EGYPT SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2018-2024 (USD MILLION)

- TABLE 294. EGYPT SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2025-2030 (USD MILLION)

- TABLE 295. TURKEY SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2018-2024 (USD MILLION)

- TABLE 296. TURKEY SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2025-2030 (USD MILLION)

- TABLE 297. TURKEY SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2018-2024 (USD MILLION)

- TABLE 298. TURKEY SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2025-2030 (USD MILLION)

- TABLE 299. TURKEY SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2018-2024 (USD MILLION)

- TABLE 300. TURKEY SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 2025-2030 (USD MILLION)

- TABLE 301. TURKEY SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 302. TURKEY SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 303. TURKEY SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2018-2024 (USD MILLION)

- TABLE 304. TURKEY SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY END-USER, 2025-2030 (USD MILLION)

- TABLE 305. ISRAEL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2018-2024 (USD MILLION)

- TABLE 306. ISRAEL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY HANDLER TYPE, 2025-2030 (USD MILLION)

- TABLE 307. ISRAEL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2018-2024 (USD MILLION)

- TABLE 308. ISRAEL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEST STAGE, 2025-2030 (USD MILLION)

- TABLE 309. ISRAEL SEMICONDUCTOR IC TEST HANDLER MARKET SIZE, BY TEMPERATURE RANGE, 201

The Semiconductor IC Test Handler Market was valued at USD 2.56 billion in 2024 and is projected to grow to USD 2.74 billion in 2025, with a CAGR of 7.50%, reaching USD 3.95 billion by 2030.

| KEY MARKET STATISTICS | |

|---|---|

| Base Year [2024] | USD 2.56 billion |

| Estimated Year [2025] | USD 2.74 billion |

| Forecast Year [2030] | USD 3.95 billion |

| CAGR (%) | 7.50% |

Comprehensive Introduction to Semiconductor IC Test Handlers Illuminating Key Market Dynamics and Strategic Imperatives

The semiconductor industry's evolution hinges on the precision and reliability of test handlers, which serve as the critical bridge between wafer fabrication and final quality assurance. In recent years, these automated systems have undergone a significant transformation as device architectures diversify, test volumes surge, and performance requirements tighten. Against this backdrop, understanding the operational principles, technological innovations, and strategic trends shaping IC test handler development is essential for decision-makers seeking to optimize throughput, minimize test costs, and maintain the highest quality standards.

This executive summary lays the groundwork for a comprehensive exploration of the semiconductor IC test handler landscape. It begins by outlining the core functions of these systems, detailing their role in accelerating test cycles and ensuring device integrity. Subsequently, the summary highlights emerging challenges, including the need for multi-temperature handling capabilities, integration with advanced probing systems, and adaptation to shrinking form factors. Throughout this section, we underscore the importance of aligning handler strategies with broader manufacturing objectives, ensuring that investments in handler technology translate into measurable gains in yield, cost efficiency, and time to market.

Unprecedented Technological and Operational Shifts Reshaping the Semiconductor IC Test Handler Landscape with Sustainable and Adaptive Solutions

In recent years, the semiconductor IC test handler arena has witnessed transformative shifts driven by both technological innovation and evolving customer demands. Devices featuring heterogeneous integration now require test handlers that can seamlessly transition between wafer probing and final system-level evaluations, prompting suppliers to develop modular platforms. Concurrently, the push for higher throughput has accelerated automation advancements, with robotic arm precision and parallel testing architectures becoming standard features.

Moreover, environmental sustainability has emerged as a core consideration, leading to the adoption of energy-efficient components and closed-loop temperature management systems. This integration of green engineering principles reduces operational costs while aligning with corporate responsibility goals. At the same time, the rise of artificial intelligence-enhanced diagnostics is empowering predictive maintenance protocols, minimizing downtime and extending equipment lifecycles. As a result, test handler providers are forging strategic partnerships with software firms, creating cohesive ecosystems that deliver intelligent analytics and real-time performance optimization.

These converging forces are reshaping procurement criteria, driving end users to seek versatile, data-driven solutions capable of supporting an expanding array of device types. In navigating this dynamic environment, stakeholders must anticipate continued advancements in handler design, ensuring that infrastructure investments remain future-proof and scalable.

Deep Analysis of the 2025 United States Tariff Regime's Comprehensive Impact on Semiconductor IC Test Handler Supply Chains

The United States' imposition of revised tariffs in 2025 has introduced significant complexity to the supply chains underpinning the semiconductor IC test handler sector. Components sourced from certain regions now incur elevated duties, compelling manufacturers and end users to reassess their procurement strategies. The immediate effect has been a realignment of component sourcing, with many suppliers seeking alternative vendors in lower-tariff jurisdictions or increasing local production to mitigate cost pressures.

These adjustments, however, have created ripple effects throughout the industry. Lead times for critical subsystems such as robotic actuators and thermal control units have lengthened as erstwhile suppliers relocate or expand capacity under new trade constraints. Concurrently, end users have begun consolidating their test handler orders around established vendors capable of offering tariff-inclusive pricing and just-in-time delivery models. This transition has accelerated partnerships and joint ventures aimed at localizing key manufacturing steps, thereby reducing exposure to cross-border trade uncertainties.

On a strategic level, the tariff environment has prompted a reevaluation of total cost of ownership calculations, compelling organizations to factor in duty escalations, inventory carrying costs, and logistics complexities. As the industry adapts, those entities that proactively invest in diversified supply networks and transparent cost modeling will maintain their competitive edge in an increasingly protectionist trade landscape.

Insightful Examination of Market Segmentation Revealing How Handler Type, Test Stage, Temperature Range, Application and End-User Shape Strategic Purchasing

Understanding market segmentation is pivotal for aligning test handler capabilities with diverse operational needs. When evaluating handler type, it is essential to recognize the distinct advantages offered by gravity handlers, which excel at gentler device loading, as well as high-throughput handlers that maximize parallel processing. Pick-and-place handlers contribute flexibility for mixed-device portfolios, while turret handlers ensure precise orientation control for specialized test protocols. Each handler category presents unique design and performance trade-offs that inform purchase decisions.

Equally important are the variations in test stage requirements. Final test solutions must deliver exhaustive electrical characterization under full operational stress, whereas system-level test configurations simulate real-world device interactions to validate endpoint functionality. Wafer test probing systems demand sub-micron alignment accuracy and minimal contact resistance to avoid perturbing delicate circuits. Stakeholders must therefore match the handler architecture to the intended test stage to optimize throughput and data fidelity.

Temperature range segmentation introduces additional complexity: ambient temperature handlers facilitate routine testing without specialized thermal controls, while cold test configurations support devices requiring extreme low-temperature cycling. Extended range and hot test handlers expand operational envelopes for power devices and automotive-grade semiconductors, and tri-temp models integrate multiple thermal zones into a single platform. In parallel, application-based distinctions highlight the need for tailored solutions for analog devices, logic and memory ICs, mixed-signal components, power electronics, MEMS, and RF devices. Lastly, end-user categories differentiate the priorities of integrated device manufacturers, outsourced packaging and test providers, and research institutions, each emphasizing unique criteria such as customization, throughput, or experimental flexibility.

Comprehensive Regional Insights Demonstrating How Americas, Europe Middle East and Africa, and Asia-Pacific Drive Distinct Test Handler Innovations and Demand Patterns

Regional dynamics exert a powerful influence on semiconductor IC test handler adoption and innovation. In the Americas, the emphasis on next-generation automotive sensors and edge computing devices has driven demand for handlers capable of stringent reliability screening and rapid deployment. North American research clusters are also exploring novel handler architectures that integrate machine learning for real-time anomaly detection, positioning the region at the forefront of intelligent test solutions.

Moving eastward, Europe, the Middle East and Africa workspace is characterized by rigorous regulatory standards and a growing focus on sustainable semiconductor manufacturing. Test handler suppliers in the region are responding with energy-optimized designs and enhanced traceability features that support compliance with environmental directives. Additionally, the region's burgeoning microelectronics hubs are fostering collaborative development efforts to reduce time to market and bolster supply chain resilience.

In the Asia-Pacific corridor, aggressive capacity expansions and robust contract manufacturing ecosystems have created a fertile environment for handler innovation. Providers are leveraging scale to lower capital costs while introducing modular platforms that accommodate high-volume logic, memory, and power device testing. Strategic partnerships between local fabless firms and global equipment manufacturers further accelerate technology transfer and local customization, ensuring that Asia-Pacific remains the largest demand center for advanced IC test handling solutions.

In-Depth Analysis of Leading Industry Players Demonstrating How Innovation, Service Networks, and Strategic Alliances Define Market Leadership

Leading equipment providers are shaping the trajectory of the IC test handler market through relentless innovation, strategic partnerships, and global service networks. These companies invest heavily in research and development, focusing on enhancements such as precision robotics, thermal uniformity, and integrated diagnostics. In turn, they differentiate themselves by offering modular architectures that simplify upgrades, reducing total cost of ownership for end users.

In addition to product innovation, top-tier providers expand their competitive moats through worldwide calibration facilities and predictive maintenance services, ensuring uptime for global customers. They also form ecosystem alliances with probing system manufacturers and test software developers to deliver cohesive solutions. As a result, these industry leaders capture premium segments by addressing the full spectrum of test requirements, from high-volume consumer electronics to stringent automotive and aerospace certifications.

Looking ahead, the competitive landscape will favor those companies that balance localized support with centralized technology excellence. Providers that anticipate regional regulatory shifts, leverage AI for adaptive testing, and maintain agile supply chains will continue to lead, while smaller challengers must carve out specialized niches or strategic partnerships to remain relevant.

Actionable Strategic Recommendations for Industry Leaders to Enhance Test Handler Resilience, Efficiency, and Sustainability Through Technology and Partnerships

To navigate the complex semiconductor IC test handler environment, industry leaders should adopt a multipronged strategic approach. First, integrating predictive analytics into handler platforms can preempt performance degradations and optimize maintenance schedules. By deploying AI-enabled monitoring across robotic systems and thermal modules, organizations will minimize downtime and extend asset life.

Second, fostering supply chain diversity is essential to mitigate tariff exposure and component bottlenecks. Establishing multiple sourcing arrangements across geographies and qualifying local suppliers will enhance resilience. Simultaneously, investing in scalable modular designs allows rapid reconfiguration of handler fleets to accommodate shifting device portfolios without extensive capital outlays.

Third, aligning with sustainability objectives through energy-efficient hardware and closed-loop temperature control not only reduces operational expenditure but also supports corporate environmental targets. Organizations should collaborate with service providers to benchmark power consumption and implement continuous improvement programs. Finally, cultivating strategic partnerships with software vendors will ensure seamless integration of handler automation, data analytics, and test flow management, empowering decision-makers with real-time insights and driving competitive differentiation.

Robust Multimodal Research Methodology Outlining Primary Interviews, Secondary Data Analysis, and Thematic Synthesis for Reliable Market Insights

This research employed a rigorous methodology combining primary and secondary data collection to capture a holistic view of the semiconductor IC test handler market. Primary insights were gathered through interviews with equipment manufacturers, test engineering leaders, and procurement specialists. These conversations explored current challenges, technology adoption patterns, and future investment priorities, providing qualitative depth to the analysis.

Complementing the primary research, secondary sources included trade association publications, technical white papers, and academic studies that detail the engineering principles underpinning handler design. Patent filings and conference proceedings were also reviewed to identify emerging innovations and competitive strategies. Data triangulation techniques were applied throughout, ensuring consistency between interview findings and documented industry trends.

Finally, thematic analysis was conducted to distill strategic imperatives across segments, regions, and company profiles. This structured approach guarantees that the conclusions and recommendations presented are grounded in both empirical evidence and expert judgment, offering a robust foundation for stakeholders seeking to make informed decisions.

Strategic Conclusion Emphasizing Agility, Regional Nuances, and Integrated Ecosystems as Pillars for Success in the Evolving Test Handler Industry

The semiconductor IC test handler domain stands at a pivotal juncture, influenced by rapid technological advancements, evolving regulatory landscapes, and trade policy shifts. Key market participants must remain agile, leveraging modular designs and AI-driven analytics to meet the demands of increasingly complex device architectures. Concurrently, strategic supply chain diversification and localized manufacturing will be critical to mitigating tariff risks and ensuring timely deliveries.

Regional nuances underscore the importance of tailored approaches: the Americas will prioritize intelligent test solutions, EMEA will focus on sustainability and compliance, while Asia-Pacific's scale and innovation networks will continue to drive throughput-centric developments. Meanwhile, market leaders are distinguished by their ability to integrate hardware, software, and service ecosystems, delivering end-to-end solutions that address the full spectrum of test requirements.

Moving forward, organizations that invest in predictive maintenance, energy efficiency, and strategic partnerships will secure competitive advantages and foster resilience. By synthesizing the insights presented in this report, stakeholders can confidently navigate the complexities of the IC test handler landscape and position themselves for sustained growth in an increasingly dynamic industry.

Table of Contents

1. Preface

- 1.1. Objectives of the Study

- 1.2. Market Segmentation & Coverage

- 1.3. Years Considered for the Study

- 1.4. Currency & Pricing

- 1.5. Language

- 1.6. Stakeholders

2. Research Methodology

- 2.1. Define: Research Objective

- 2.2. Determine: Research Design

- 2.3. Prepare: Research Instrument

- 2.4. Collect: Data Source

- 2.5. Analyze: Data Interpretation

- 2.6. Formulate: Data Verification

- 2.7. Publish: Research Report

- 2.8. Repeat: Report Update

3. Executive Summary

4. Market Overview

- 4.1. Introduction

- 4.2. Market Sizing & Forecasting

5. Market Dynamics

- 5.1. Integration of machine learning algorithms for real-time IC test handler yield optimization

- 5.2. Adoption of vacuum-based wafer handling technologies to minimize particle contamination risks

- 5.3. Development of multi-site parallel testing architectures for high-volume IC throughput requirements

- 5.4. Implementation of in situ thermal monitoring modules for advanced semiconductor test calibration

- 5.5. Transition to universal handler platforms supporting mixed-signal and RF IC test applications

- 5.6. Emergence of IoT-enabled remote diagnostics and predictive maintenance in IC test equipment

- 5.7. Customization of handler interfaces for heterogeneous packaging types including fan-out wafers

- 5.8. Integration of robotics and automated guided vehicles for seamless IC test handler logistics

6. Market Insights

- 6.1. Porter's Five Forces Analysis

- 6.2. PESTLE Analysis

7. Cumulative Impact of United States Tariffs 2025

8. Semiconductor IC Test Handler Market, by Handler Type

- 8.1. Introduction

- 8.2. Gravity Handlers

- 8.3. High-Throughput Handlers

- 8.4. Pick-and-Place Handlers

- 8.5. Turret Handlers

9. Semiconductor IC Test Handler Market, by Test Stage

- 9.1. Introduction

- 9.2. Final Test (FT)

- 9.3. System-Level Test (SLT)

- 9.4. Wafer Test (Probing)

10. Semiconductor IC Test Handler Market, by Temperature Range

- 10.1. Introduction

- 10.2. Ambient Temperature Handlers

- 10.3. Cold Test Handlers

- 10.4. Extended Range Handlers

- 10.5. Hot Test Handlers

- 10.6. Tri-Temp Handlers

11. Semiconductor IC Test Handler Market, by Application

- 11.1. Introduction

- 11.2. Analog Devices

- 11.3. Logic & Memory Devices

- 11.4. Mixed-Signal ICs

- 11.5. Power Devices & MEMS

- 11.6. RF Devices

12. Semiconductor IC Test Handler Market, by End-User

- 12.1. Introduction

- 12.2. IDMs (Integrated Device Manufacturers)

- 12.3. OSATs (Outsourced Packaging & Test Providers)

- 12.4. R&D Institutions and Packaging Providers

13. Americas Semiconductor IC Test Handler Market

- 13.1. Introduction

- 13.2. United States

- 13.3. Canada

- 13.4. Mexico

- 13.5. Brazil

- 13.6. Argentina

14. Europe, Middle East & Africa Semiconductor IC Test Handler Market

- 14.1. Introduction

- 14.2. United Kingdom

- 14.3. Germany

- 14.4. France

- 14.5. Russia

- 14.6. Italy

- 14.7. Spain

- 14.8. United Arab Emirates

- 14.9. Saudi Arabia

- 14.10. South Africa

- 14.11. Denmark

- 14.12. Netherlands

- 14.13. Qatar

- 14.14. Finland

- 14.15. Sweden

- 14.16. Nigeria

- 14.17. Egypt

- 14.18. Turkey

- 14.19. Israel

- 14.20. Norway

- 14.21. Poland

- 14.22. Switzerland

15. Asia-Pacific Semiconductor IC Test Handler Market

- 15.1. Introduction

- 15.2. China

- 15.3. India

- 15.4. Japan

- 15.5. Australia

- 15.6. South Korea

- 15.7. Indonesia

- 15.8. Thailand

- 15.9. Philippines

- 15.10. Malaysia

- 15.11. Singapore

- 15.12. Vietnam

- 15.13. Taiwan

16. Competitive Landscape

- 16.1. Market Share Analysis, 2024

- 16.2. FPNV Positioning Matrix, 2024

- 16.3. Competitive Analysis

- 16.3.1. Advantest Corporation

- 16.3.2. Cohu, Inc.

- 16.3.3. 4JMSolutions (Malta) Ltd.

- 16.3.4. Amfax Limited

- 16.3.5. Boston Semi Equipment

- 16.3.6. Chroma ATE Inc.

- 16.3.7. esmo AG

- 16.3.8. Hangzhou Changchuan Technology Co., Ltd.

- 16.3.9. Hon Precision, Inc.

- 16.3.10. Innogrity Pte Ltd

- 16.3.11. Kanematsu Corporation

- 16.3.12. Komachine Inc.

- 16.3.13. MICRONICS JAPAN CO.,LTD.

- 16.3.14. SMTmax

- 16.3.15. SPEA S.p.A.

- 16.3.16. SYNAX Co., Ltd.

- 16.3.17. Teradyne, Inc.

- 16.3.18. TESEC Corporation

- 16.3.19. Tianjin JHT Design Co., Ltd.

- 16.3.20. UENO SEIKI CO.,LTD.

- 16.3.21. YAC Systems Singapore Pte.

- 16.3.22. Yamaichi Electronics Co., Ltd.

- 16.3.23. YoungTek Electronics Corp.