|

|

市場調査レポート

商品コード

1837206

システムオンチップ市場:タイプ別、集積タイプ別、アプリケーション別-2025-2032年の世界予測System on Chip Market by Type, Integration Type, Application - Global Forecast 2025-2032 |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| システムオンチップ市場:タイプ別、集積タイプ別、アプリケーション別-2025-2032年の世界予測 |

|

出版日: 2025年09月30日

発行: 360iResearch

ページ情報: 英文 188 Pages

納期: 即日から翌営業日

|

概要

システムオンチップ市場は、2032年までにCAGR 8.65%で3,266億4,000万米ドルの成長が予測されています。

| 主な市場の統計 | |

|---|---|

| 基準年2024 | 1,682億米ドル |

| 推定年2025 | 1,817億1,000万米ドル |

| 予測年2032 | 3,266億4,000万米ドル |

| CAGR(%) | 8.65% |

システムオンチップの設計サイクルと業界連携を再定義する戦略的背景と技術的必須事項を確立する権威あるイントロダクション

システムオンチップ(SoC)の状況は、半導体の技術革新、ソフトウェアのエコシステム、そして進化するエンドマーケットの要求の収束点に位置しています。プロセス・ノード、パッケージング技術、ヘテロジニアス・インテグレーションの先進は、より多くの機能を単一のシリコン・プラットフォームに統合することを可能にし、ハードウェア・アーキテクチャとシステムレベル・ソフトウェア間の緊密な結合を推進しています。その結果、製品ロードマップでは、ワットあたりの性能、セキュリティー、特定分野に特化したアクセラレーターが、設計の中心的な推進力としてますます優先されるようになっています。

このイントロダクションでは、エンジニアリング・リーダー、プロダクト・マネージャー、サプライチェーン戦略担当者が、最新のSoCプログラムの技術的・商業的複雑性に対処する際に考慮しなければならない戦略的要件を整理しています。設計手法と製造制約の相互作用を強調し、モジュールIPの再利用、検証フローの近代化、EDA、IP、鋳造パートナー間の協力の重要性を強調しています。このようなダイナミクスを明確にすることで、読者は後続のセクションで、開発スケジュール、ベンダーの関与、リスク軽減に対する実際的な影響に目を向けることができます。

今後、SoCの領域は、専門性とプログラマビリティのバランスによって形成され続けると思われます。その結果、機能横断的なプロセスを調整し、システムレベルの検証に投資する組織は、シリコンのイノベーションを差別化された製品と測定可能な市場投入期間の優位性に容易に変換できるようになります。

システムオンチップアーキテクチャのサプライチェーンとソフトウェア統合モデルを再構築する技術的・商業的変革の鋭い分析

SoCの状況は、技術革新と再編成された商業的インセンティブに牽引され、変革の時を迎えています。ヘテロジニアス・インテグレーションと先進パッケージングは、システム分割の決定をシフトさせ、モノリシック・プロセスのスケーリングを必要とすることなく、ロジック、メモリ、アナログ・コンポーネントの緊密な同居を可能にしています。これと並行して、AI推論、センサー・フュージョン、セキュア・トラスト・アンカーなど、ドメインに特化したアクセラレータの普及が進み、アーキテクトはカスタム・ブロックとプログラマブル・ファブリックを融合させ、ワークロードに特化したメトリクスに最適化する必要に迫られています。

さらに、Software-Defined Hardwareパラダイムは、ライフサイクル・サポートとシリコン後の機能進化に対する期待を変化させています。この移行により、企業は、ファームウェアと上位レベルのオーケストレーション・スタックの両方をカバーする、堅牢な検証フレームワークとともに、セキュアでバージョン管理されたブートとアップデートのメカニズムを採用する必要に迫られています。サプライチェーンのダイナミクスも同様に適応しており、キャパシティや地政学的な混乱を緩和するために、製造業向け設計のコラボレーションやセカンドソース戦略をより重視しています。

これらの動向を総合すると、統合のスピード、エコシステム・パートナーシップ、システム・レベルの性能とセキュリティを顧客の状況で実証する能力が商業的成功を左右する、新たな競争フロンティアが生まれつつあります。分野横断的なチームを受け入れ、モジュール化された検証可能なIPに投資する組織は、こうしたシフトから最大の価値を獲得する立場にあります。

米国の最近の関税政策が、調達慣行やサプライチェーンの弾力性、設計適格性評価アプローチにどのような変化をもたらしているかを包括的に評価します

最近の関税措置と貿易政策の動向は、SoCエコシステム全体の調達決定、製造フットプリント、サプライヤー契約に累積的な影響を及ぼしています。設計サービス、製造、テストを国境を越えて調達している企業は、コスト構造の変化や規制遵守義務を考慮し、契約条件、リードタイムの想定、在庫戦略を再調整しています。企業が適応するにつれて、プログラムの弾力性を維持するために、サプライヤーのスコアカードや地域の認定計画に関税リスクを組み込む傾向が強まっています。

実際的には、その影響は、短期的な調達の柔軟性と代替製造パートナーの地域的適格性に改めて焦点が当てられるという形で現れています。企業は、長期供給契約を見直し、貿易の途絶と関税に明確に対処する不可抗力条項を盛り込むようにし、また、国境を越えた暴露によって容認できないオペレーショナル・リスクが生じる場合には、特定のプロセスステップをローカライズする取り組みを加速させています。同時に、エンジニアリング・チームは、高関税部品への依存度を低減したり、異なる地理的管轄区域での組み立てを容易にするような設計上の微調整を評価しています。

全体として、関税は商業的な複雑さを一層もたらすが、同時に、より規律あるシナリオプランニング、調達とエンジニアリング間のより強力なコラボレーション、製品バリエーション間のコスト・ツー・サーブの明確な提示を促しています。このような調整は、より強固な継続計画をサポートし、政策情勢の変化にもかかわらず、企業が戦略的プログラムのタイムラインを維持することを可能にします。

セグメンテーションに基づく詳細な調査により、タイプ統合とアプリケーション固有の要件が、設計の焦点と検証ニーズ、および商品化戦略をどのように決定するかを明らかにします

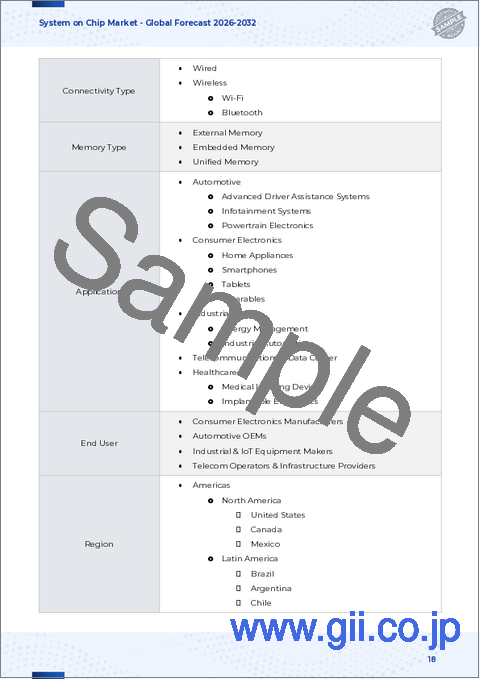

セグメンテーションの洞察により、技術的な選択肢が最終市場の要件や統合戦略とどのように交差するかが明らかになり、独自の製品や市場投入アプローチが形成されます。タイプ別に、アナログ、デジタル、ミックスドシグナルを調査し、アナログフロントエンドの複雑さと純粋なデジタル処理のバランスが、検証の焦点とIPの選択にどのように影響するかを明らかにします。インテグレーション・タイプ別では、フルカスタム・インテグレーション、セミカスタム・インテグレーション、スタンダード・セルについて調査し、設計手法の決定がコスト構造、市場投入期間、長期保守性を左右することを明らかにしています。アプリケーション別では、自動車、家電、産業、通信・データセンターについて調査しており、これらのアプリケーションは信頼性、レイテンシ、機能安全に対する要求が異なることを示しています。自動車分野ではさらに、ADAS(先進運転支援システム)、インフォテインメント・システム、パワートレイン・エレクトロニクスが調査対象となり、それぞれ異なる検証レジームとサプライヤー・エコシステムが要求されます。コンシューマー・エレクトロニクスの分野では、家電、スマートフォン、タブレット、ウェアラブルを対象とし、ユーザー・エクスペリエンス、消費電力、小型化が主要な設計制約となっています。産業分野では、予測可能なライフサイクルと堅牢性が信頼性重視の設計を決定する、エネルギー管理と産業オートメーションがさらに検討されます。

これらのセグメンテーションから、アナログとミックスドシグナルに関する専門知識は依然として乏しいが、高価値のアプリケーションには不可欠である一方、セミカスタムとスタンダードセルのルートはソフトウェア主導の市場での商品化を加速させることが明らかになりました。さらに、アプリケーション要件が多様化していることから、コンフィギュラブルなセキュリティアーキテクチャと、ドメイン固有のコンプライアンスを損なうことなくさまざまな製品に再利用できるモジュール型検証資産の必要性が浮き彫りになっています。

南北アメリカ、欧州、中東&アフリカ、アジア太平洋地域が、それぞれ設計パートナーシップと製造規模、規制コンプライアンスにどのような影響を与えるかを明らかにする戦略的地域分析

地域ダイナミックスは、技術採用の道筋、サプライヤーのエコシステム、SoCプログラムの規制コンプライアンス要件に強力な影響を及ぼします。南北アメリカでは、技術革新の中心地、強力な設計サービス・エコシステム、迅速なプロトタイピングと緊密なIP連携を求める戦略的顧客の集中が重視されています。この地域は、システムレベルのソフトウエア統合とエンドアプリケーションの検証をリードすることが多く、その結果、深い共同エンジニアリング関係の需要が高まっています。

欧州、中東・アフリカでは、規制の枠組み、機能安全に関する基準、多様な産業基盤が、製品ライフサイクルの長期化と相互運用性と堅牢性に対するより高い期待を形成しています。この地域で事業を展開する企業は、認証された開発フローとマルチベンダーの相互運用性テストを優先することが多いです。一方、アジア太平洋地域では、製造規模、緻密な供給網、競争力のある鋳造と組立の競合情勢が組み合わさって、迅速な反復とコストの最適化を支えているが、知的財産権の保護と国境を越えたロジスティクスの積極的な管理も必要です。

これらの地域特性を総合すると、成功する企業は地域特有の関与モデルを採用することが示唆されます。イノベーション中心市場では共同研究開発と初期段階の検証を優先し、規制市場では厳格な認証パイプラインに準拠し、大量生産回廊ではコストと時間の効率化のために密集した生産エコシステムを活用します。

知的財産に特化したパートナーシップと統合能力が、どのように競合のポジショニングとプログラムの成功を左右するかを浮き彫りにする企業レベルの詳細な考察

主要な企業レベルのダイナミクスは、IPの専門化、戦略的パートナーシップ、シリコン、ファームウェア、クラウド対応サービスを組み合わせた垂直統合型の提供による能力の差別化を強調しています。大手企業は、特定分野に特化したアクセラレータ、強固なセキュリティ・サブシステム、顧客との迅速な統合を可能にするモジュール型ソフトウェア・スタックに投資することで差別化を図っています。同時に、中堅のデザインハウスは、アナログ統合やパッケージングの専門知識が高価値の差別化要因となるような、特化したニッチを活用しています。

IPプロバイダー、鋳造所、システムインテグレーター間のコラボレーションは、共同検証プログラムや検証資産の共有を優先し、重複作業を減らすなど、より成果にフォーカスしたものとなっています。戦略的M&Aやマイノリティ投資は、ドメインの専門知識を獲得し、市場投入までの時間を短縮するためのメカニズムであり続け、標準インターフェイスを中心としたパートナーシップは、新しいタイプのアクセラレータに対するエコシステムの採用を拡大するのに役立っています。

競合情勢を見渡しても、反復可能な設計フロー、透明性の高いセキュリティ証明、実績のある製造移行プロセスを実証する企業は、より高いレベルの企業採用を獲得しています。同様に重要なことは、フィールド・アップデートが可能なファームウェアや、長期的なコンポーネントの継続計画を含む、ポスト・シリコン・サポートに投資している企業は、規制されたミッション・クリティカルなアプリケーションでの契約を確保するために、より有利な立場にあるということです。

SoC開発を加速させ、回復力を強化し、商業的成果を最大化するために、エンジニアリング調達チームと経営陣に対して、実践的で優先順位をつけた推奨事項を示します

業界のリーダーは、アーキテクチャの選択、サプライヤとの関係、業務慣行にまたがる一連の協調的な行動を追求し、SoC開発の進化する機会を捉えるべきです。第一に、アーキテクチャとソフトウエアのロードマップを早期に整合させ、アクセラレータとセキュリティモジュールが測定可能なシステムレベルの利益をもたらすようにします。第二に、代替の鋳造所、アセンブリパートナー、IPベンダーの認定を行うことで、サプライヤーとの関わりを多様化し、認定の厳密性を犠牲にすることなく、戦術的な柔軟性を生み出します。

第三に、テストサイクルを短縮し、欠陥の可視性を向上させるために、プロジェクト間で再利用可能なモジュール式検証資産と自動検証フレームワークに投資します。第四に、関税と規制のシナリオ・プランニングを調達と製品プランニングのサイクルに組み込み、設計決定が必要な場合に地域の製造シフトに対応できるようにします。第五に、製品ライフサイクルを通じてデバイスの完全性と顧客の信頼を維持するため、セキュアな更新メカニズムやフィールド診断により、ポストシリコンサポート能力を強化します。

これらの推奨事項を並行して実行することで、企業は市場投入までの時間を短縮し、外部からの衝撃に対する耐性を向上させ、技術革新と商業目標を一致させるスケーラブルで反復可能なSoCプログラムの基盤を構築することができます。

一次情報インタビュー、技術レビュー、マルチソース・トライアンギュレーションを組み合わせた透明性の高い混合調査手法により、運用上実用的な洞察を得る

調査手法は、厳密でバランスの取れた視点を確保するために、1次インタビュー、対象技術レビュー、体系的な2次分析を組み合わせた混合手法に基づいています。一次インプットには、システムアーキテクト、検証リード、調達エグゼクティブ、テストエンジニアとの構造化インタビューが含まれ、これらはすべて、実際のプロジェクトで観察された意思決定要因、一般的な故障モード、実践的な緩和戦略を捕捉することを目的としています。これらの定性的な洞察は、設計フロー、パッケージングの選択、および検証ツールチェインに関する技術的なレビューによって補完され、業界の慣行を文脈化します。

二次分析では、公開技術文献、会議録、標準化文書を統合し、検証およびセキュリティフレームワークに関する新たなプラクティスとコンセンサスをマッピングします。データの三角測量は、複数のエビデンスの流れに適用して、テーマ別の結論を検証し、さらなる調査に値する不確実な領域を特定します。調査全体を通じて、前提条件の透明性、分析手順の再現性、観察された実践と解釈上の推奨事項の明確な区別を重視しています。

この調査手法により、エンジニアリング・プログラムの現実と、経営陣が利用できる戦略的手段の両方を反映した、実用的な洞察が得られます。

統合の検証と弾力性のある供給の選択が、SoCイノベーションが持続可能な商業的優位性につながるかどうかを決定することを強調する決定的な統合

結論として、システムオンチップ領域は、統合の選択、ソフトウェアとハードウェアの共同設計、弾力性のある供給戦略が商業的成果を共同で決定する状況へと成熟しつつあります。ヘテロジニアス・インテグレーションとドメイン固有のアクセラレーションにおける技術的進歩は、強力な機会を生み出すが、その可能性を実現するには、規律ある検証、明確なサプライヤー戦略、将来を見据えた規制・関税計画が必要です。卓越したエンジニアリングを戦略的な調達手法とモジュール化された検証能力と組み合わせる組織は、持続的な競争優位性を達成することができます。

さらに、地域的なニュアンスやアプリケーション固有の要件が、適応可能なエンゲージメントモデルとコンフィギュラブルな設計資産の必要性を際立たせています。自動車安全システム、民生機器、産業用制御、クラウド規模のインフラストラクチャのいずれをターゲットとする場合でも、チームは、各領域特有の信頼性、セキュリティ、および性能の期待値に合わせて内部プロセスを調整する必要があります。最終的に、この分野での成功は、強固なパートナーシップと、俊敏性とリスクを考慮した計画を優先する運営倫理に支えられ、シリコンレベルのイノベーションを顧客の展開におけるシステムレベルの実証可能な価値に変換できるかどうかにかかっています。

目次

第1章 序文

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場の概要

第5章 市場洞察

- AIアクセラレータとニューラルプロセッシングユニットを統合し、クラウドに依存せずにデバイス上の推論パフォーマンスを向上

- チップレットベースの異種統合の採用により、カスタマイズ可能なシステムオンチップ設計が可能になり、歩留まりが向上します。

- バッテリー駆動のIoTおよびウェアラブルデバイスにおけるエッジコンピューティングに最適化された超低消費電力SoCの需要の高まり

- RISC-Vベースのオープンソースアーキテクチャの出現により、従来の独自命令セットの優位性が崩れつつある

- 3Dスタッキングとシリコンインターポーザー技術による先進パッケージングの革新により、チップのスケーリングを拡張します。

- サイバーセキュリティの耐性を高めるためのSoC設計において、セキュアエンクレーブやルートオブトラストなどのハードウェアベースのセキュリティ機能の重要性が高まっています。

- 5G mmWave統合SoCの普及により、消費者向けデバイスと産業用接続アプリケーションの成長が促進

- 自動運転・ADASシステム向けISO 26262準拠の車載グレード機能安全SoCの開発

第6章 米国の関税の累積的な影響, 2025

第7章 AIの累積的影響, 2025

第8章 システムオンチップ市場:タイプ別

- アナログ

- デジタル

- ミックスシグナル

第9章 システムオンチップ市場統合タイプ別

- 完全なカスタム統合

- セミカスタム統合

- 標準セル

第10章 システムオンチップ市場:用途別

- 自動車

- ADAS(先進運転支援システム)

- インフォテインメントシステム

- パワートレインエレクトロニクス

- 家電

- 家電製品

- スマートフォン

- タブレット

- ウェアラブル

- 産業

- エネルギー管理

- 産業オートメーション

- 通信・データセンター

第11章 システムオンチップ市場:地域別

- 南北アメリカ

- 北米

- ラテンアメリカ

- 欧州・中東・アフリカ

- 欧州

- 中東

- アフリカ

- アジア太平洋地域

第12章 システムオンチップ市場:グループ別

- ASEAN

- GCC

- EU

- BRICS

- G7

- NATO

第13章 システムオンチップ市場:国別

- 米国

- カナダ

- メキシコ

- ブラジル

- 英国

- ドイツ

- フランス

- ロシア

- イタリア

- スペイン

- 中国

- インド

- 日本

- オーストラリア

- 韓国

第14章 競合情勢

- 市場シェア分析, 2024

- FPNVポジショニングマトリックス, 2024

- 競合分析

- Advanced Micro Devices, Inc.

- AMBARELLA, INC.

- Analog Devices, Inc.

- Apple Inc.

- Arm Holdings PLC

- Broadcom Inc.

- Efinix, Inc.

- Esperanto Technologies

- Espressif Systems

- Fujitsu Limited

- Huawei Investment & Holding Co., Ltd.

- InCore

- Infineon Technologies AG

- Intel Corporation

- Kneron, Inc.

- Marvell Technology, Inc.

- Microchip Technology Incoporated

- Novatek Microelectronics Corp.

- NVIDIA Corporation

- NXP Semiconductors N.V.

- Qualcomm Technologies, Inc.

- QUICKLOGIC CORPORATION

- Realtek Semiconductor Corp

- Renesas Electronics Corporation

- Samsung Electronics Co. Ltd.

- STMicroelectronics N.V.

- Taiwan Semiconductor Manufacturing Company Limited

- Texas Instruments Incorporated

- UNISOC(Shanghai)Technology Co., Ltd.