生成AI市場:2025年~2030年

Generative AI Market Report 2025-2030- 発行日

- ページ情報

- 英文 263 Pages

- 納期

- 即日から翌営業日

- 商品コード

- 1540311

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

- 通信/IT関連専門 通信/IT関連専門を専門とする市場調査会社です。

概要

生成AIは、変分オートエンコーダー、生成的敵対ネットワーク、およびトランスフォーマーベースのモデルに基づくディープラーニング技術です。

データセンターGPUの市場セグメントは、現代のデータセンターの膨大な計算需要に対応するために設計された特殊なグラフィック処理ユニットを指します。これらのGPUは、高性能コンピューティング、DL、ML、大規模なグラフィック処理タスクなど、さまざまな複雑なワークロードを高速化するように設計されています。この市場には、CPU、コンシューマーグレードのGPU、または特定用途向け集積回路(ASIC)への支出は含まれません。専用のGPUサーバーラックなどのGPUシステムが含まれます。この市場には外部支出のみ含まれ、GoogleのTPUやAWSのTrainiumまたはInferentiumなどの独自のチップの開発への支出は含まれません。

サンプルビュー

サンプルビュー

サンプルビュー

当レポートは、生成AI市場について、IoTアナリティクスによるエンタープライズテクノロジー市場を対象に調査しています。このレポートで提示される情報は、2次調査と定性調査、つまりこの分野の専門家へのインタビューの結果に基づいています。このドキュメントの主な目的は、読者が現在のジェネレーティブAI(生成AI)の情勢と潜在的な使用例を理解できるようにすることです。

目次

第1章 エグゼクティブサマリー

第2章 イントロダクション

第3章 技術概要

- 章の概要:技術の概要

- 生成AI技術スタック:5つの主要ブロック

- 基礎モデル

- 生成AIソフトウェアエコシステム

- コンピューティングハードウェア

第4章 市場モデルと見通し

- 章の概要:市場モデルと展望

- 生成AIエンタープライズ市場

- 生成AI市場:2022年~2030年

- データセンターGPU市場:概要

- データセンターGPU市場:顧客グループ別

- 基盤モデルとモデル管理プラットフォーム市場:概要

- 基盤モデルとモデル管理プラットフォーム市場:業界別

- 基盤モデルとモデル管理プラットフォーム市場:地域別

- 基盤モデルとモデル管理プラットフォーム市場:国別

- 生成AIサービス市場:概要

- 生成AIサービス市場:業界別

- 生成AIサービス市場:地域別

- 生成AIサービス市場:国別

- 視点:生成AIの支出と世界のソフトウェアおよびサービス支出の関係

第5章 競合情勢

- 章の概要:競合情勢

- 2024年の競合情勢:市場シェアの概要

- データセンターGPU:競合情勢(収益)

- データセンターGPU:競合情勢(市場シェア)

- データセンターGPU:NVIDIA

- データセンターGPU:AMD

- データセンターGPU:Intel

- データセンターGPU:Cerebras

- データセンターGPU:Groq

- 基盤モデルとモデル管理プラットフォーム:競合情勢

- 基盤モデルとモデル管理プラットフォーム(市場シェア)

- 基礎モデルとモデル管理プラットフォーム:最高のLLM

- 基盤モデルとモデル管理プラットフォーム:主要なオープンモデル

- 基盤モデルとモデル管理プラットフォーム:Microsoft

- 基盤モデルとモデル管理プラットフォーム:AWS

- 基盤モデルとモデル管理プラットフォーム:Google

- 基盤モデルとモデル管理プラットフォーム:OpenAI

- 基盤モデルとモデル管理プラットフォーム:Hugging Face

- 基盤モデルとモデル管理プラットフォーム:Mistral AI

- 生成AIの主要ソフトウェアプラットフォームの概要:開発プラットフォーム

- 生成AIの主要ソフトウェアプラットフォームの概要:データ管理ツール

- 生成AIの主要ソフトウェアプラットフォームの概要:AI IaaS、GPU-as-a-Service

- 生成AIの主要ソフトウェアプラットフォームの概要:ミドルウェアと統合

- 生成AIの主要ソフトウェアプラットフォームの概要:MLOps

- CEOが選択したLLMとLLMプロバイダーについてどのように議論するか

- 生成AIサービス:競合情勢

- 生成AIサービス:競合情勢(市場シェア)

- 生成AIサービス:Accenture

- 生成AIサービス:Deloitte

- 生成AIサービス:Capgemini

- 生成AIサービス:IBM

第6章 エンドユーザーの採用

- 章の概要:エンドユーザーの採用

- 530件の生成AIプロジェクトの分析

- 主なケーススタディ:例-Klarna

- 主なケーススタディ:例-Westnet

- 主なケーススタディ:例-Covered California

- 製造業の深掘り:HMI 2024における20の生成AIソリューションの概要

- 製造業の深掘り:ケーススタディ- シーメンス

- 製造業の深掘り:調査統計- 製造業におけるAIの主な使用事例

- テクノロジーと通信業界の深掘り:MWC 2024で注目される生成AIソリューション

- テクノロジーと通信業界の深掘り:ケーススタディ1-Vodafone

- テクノロジーと通信業界の深掘り:ケーススタディ2-Soracom

- テクノロジーと通信業界の深掘り:ケーススタディ3-SAP

第7章 生成AIの応用情勢とビジネスモデルの検討

第8章 動向と課題

第9章 調査手法

第10章 IoTアナリティクスについて

目次

A 263-page report on the enterprise Generative AI market, incl. market sizing & forecast, competitive landscape, end user adoption, trends, challenges, and more.

The "Generative AI Market Report 2025-2030" is part of IoT Analytics' ongoing coverage of enterprise technology markets. The information presented in this report is based on the results of secondary research and qualitative research, i.e., interviews with experts with experts in the field. The main purpose of this document is to help our readers understand the current Generative AI (GenAI) landscape and potential use cases.

What is Generative AI?

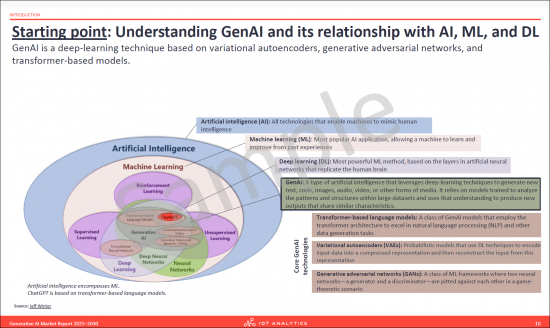

GenAI is a deep-learning technique based on variational autoencoders, generative adversarial networks, and transformer-based models.

SAMPLE VIEW

What is a Data Center GPU?

The market segment for data center GPUs refers to specialized graphics processing units designed to handle the extensive computational demands of modern data centers. These GPUs are engineered to accelerate a variety of complex workloads, including high-performance computing, DL, ML, and large-scale graphics processing tasks. The market does not include spending on CPUs, consumer-grade GPUs, or application-specific integrated circuits (ASICs). It includes GPU systems such as specialized GPU server racks. The market only includes external spending but not spending on developing own chips e.g., Google's TPUs or AWS' Trainium or Inferentium.

SAMPLE VIEW

What are foundational models and model management platforms?

This market segment includes both foundational models and model management platforms.

- 1. Foundational models are large-scale, pre-trained models that can be adapted to a wide variety of tasks without the need for training from scratch, such as language processing, image recognition, and decision-making algorithms.

- 2. Model management platforms are software platforms that enable users to deploy, fine-tune, and call GenAI models. Model management platforms allow the use of different GenAI models and are not limited to one single model vendor. The market does not include chatbots and applications such as ChatGPT.

SAMPLE VIEW

What are Gen AI services?

GenAI services represent a specialized market segment dedicated to consulting, integration, and implementation support for organizations aiming to integrate GenAI capabilities. These services are tailored to help businesses conceptualize, develop, and execute strategies that leverage GenAI technologies for enhanced innovation, efficiency, and value creation. Services includes consulting, integration, and managed services.

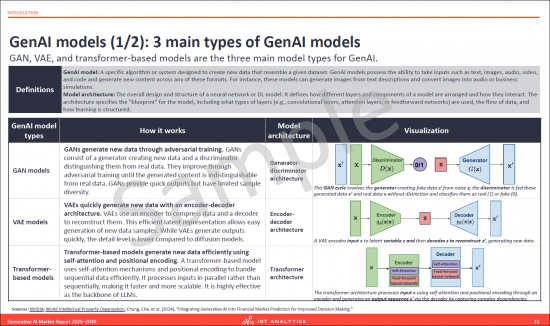

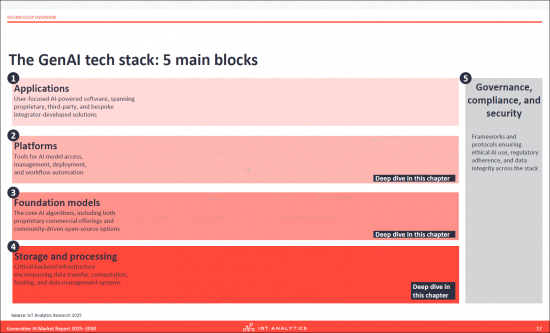

Five building blocks make up the Generative AI stack

The GenAI tech stack includes 5 building blocks:

- 1. Applications (e.g., AI-powered software solutions)

- 2. Platform tools for deployment and management

- 3. Foundation models like OpenAI's GPT 4

- 4. Critical backend infrastructure such as data processing and GPUs

- 5. Governance frameworks for security and compliance

The report includes a structured repository of 530 generative AI projects.*

Database structure

| Column name | Description |

|---|---|

| Company | Name of the company that implemented the project. |

| Industry (ISIC classification) | Industry classification (ISIC code) of the customer |

| Project description | A brief description of the project |

| Country | Country that the project took place in |

| Region | Region that the project took place in |

| Vendor | Name of the vendor that has published the case study/project on their website |

| Year | Year that the project was implemented |

| Link | Unique identifier of each case study/project |

| Key department and activities that are improved by each project | Each project is grouped into one or more of the follogin departments: Sales, Marketing, Operations/mfg, Maintenance/field service, Finance and account, Human resources, IT/technology, Research and development, Customer service/support, Legal and compliance, Procurement, Logistics and supply chain, Corporate strategy/business development, Facility management. A project can touch mulitple departments. Each department is broken down into key activities. |

The database is suited for:

- AI strategy/business case development

- Sector scan+Customer/vendor selection

- Competitive analysis

- Go-to-market/market entry strategy

- And more

Questions answered:

- What is GenAI, and what are its technological components?

- Which GenAI use cases and applications are being prioritized by enterprises right now?

- What is the current market size for GenAI, and what are the market shares of key players ?

- Who is leading the market for GenAI models and platforms?

- Which companies offer AI accelerators beyond NVIDIA?

- Which consulting and professional services companies are selling the most GenAI projects?

- How do the leading GenAI models compare?

- What are some of the important implementation considerations for GenAI?

- What are the current and next trends and challenges around GenAI?

Companies mentioned:

A selection of companies mentioned in the report.

|

|

Table of Contents

1. Executive Summary

2. Introduction

- Chapter overview: Introduction

- Starting point: Understanding GenAI and its relationship with AI, ML, and DL

- The history of GenAI

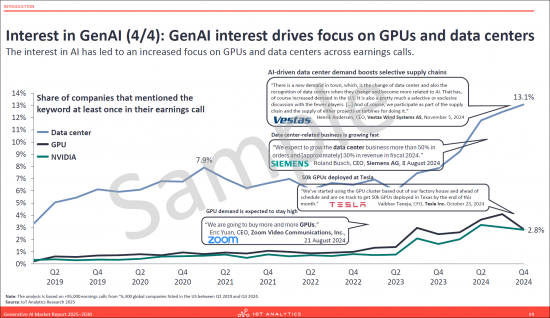

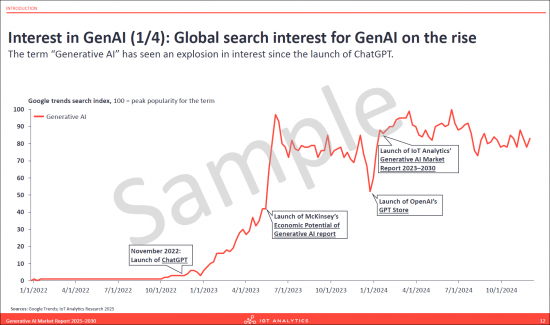

- Interest in GenAI

- Investments in GenAI start-ups

- AI advances: (Gen)AI surpasses human capabilities in many tasks

- GenAI models

- GenAI adoption by industry

- GenAI adoption by business function

- Negative consequences of GenAI adoption

- GenAI model building/integration approaches

- Case study: AI at Thomson Reuters

- Beneficiaries of GenAI tech spending

3. Technology overview

- Chapter overview: Technology Overview

- The GenAI tech stack: 5 main blocks

- Foundation models: The transformer architecture

- Foundation models: What are foundation models?

- Foundation models: Type - Language models

- Foundation models: Type - Vision models

- Foundation models: Type - Speech/audio models

- Foundation models: Type - Multimodal models

- Foundation models: Type - Industry-specific models

- Foundation models: Optimization techniques

- Foundation models: Comparing GenAI models

- Foundation models: Best-performing models

- Foundation models: Open models

- GenAI software ecosystem: The five main types of platforms

- GenAI software ecosystem: The foundation model value chain

- GenAI software ecosystem: Databases

- GenAI software ecosystem: IaaS/GPU-as-a-service

- GenAI software ecosystem: Development platforms

- GenAI software ecosystem: Middleware & integration tools

- Computing hardware: AI chips overview

- Computing hardware: Types of AI chips and their capabilities

- Computing hardware: AI chips' power consumption

- Computing hardware: Training vs. Inference

- Computing hardware: NVIDIA vs. AMD chips

- Computing hardware: Emergence of new AI chips

- Computing hardware: GPU types in research papers

- Computing hardware: Data center infrastructure

4. Market model & outlook

- Chapter overview: Market model & outlook

- GenAI enterprise market: What is included and what is not

- GenAI market 2022-2030

- 1. Data center GPU market: Overview

- 1. Data center GPU market: By customer group

- 2. Foundation models & model mgmt. platforms market: Overview

- 2. Foundation models & model mgmt. platforms market: By vertical

- 2. Foundation models & model mgmt. platforms market: By region

- 2. Foundation models & model mgmt. platforms market: By country

- 3. GenAI services market: Overview

- 3. GenAI services market: By vertical

- 3. GenAI services market: By region

- 3. GenAI services market: By country

- Perspective: GenAI spending in relation to global software and services spending

5. Competitive landscape

- Chapter overview: Competitive landscape

- Competitive landscape 2024: Market Share Overview

- Data center GPUs: Competitive landscape (revenue)

- Data center GPUs: Competitive landscape (market share)

- Data center GPUs: NVIDIA

- Data center GPUs: AMD

- Data Center GPUs: Intel

- Data Center GPUs: Cerebras

- Data center GPUs: Groq

- Foundation models & model mgmt. platforms: Competitive landscape

- Foundation models & model mgmt. platforms (market share)

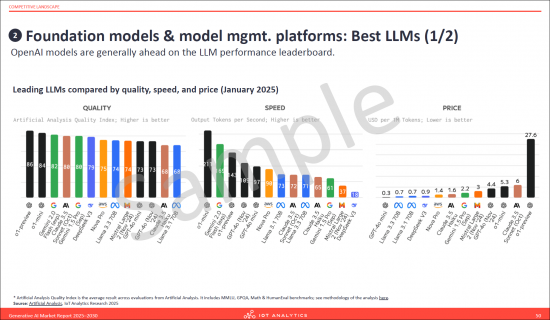

- Foundation models & model mgmt. platforms: Best LLMs

- Foundation models & model mgmt. platforms: Leading open models

- Foundation models & model mgmt. platforms: Microsoft

- Foundation models & model mgmt. platforms: AWS

- Foundation models & model mgmt. platforms: Google

- Foundation models & model mgmt. platforms: OpenAI

- Foundation models & model mgmt. platforms: Hugging Face

- Foundation models & model mgmt. platforms: Mistral AI

- Overview of key software platforms for GenAI: 1. Development Platforms

- Overview of key software platforms for GenAI: 2. Data Management Tools

- Overview of key software platforms for GenAI: 3. AI IaaS, GPU-as-a-Service

- Overview of key software platforms for GenAI: 4. Middleware & Integration

- Overview of key software platforms for GenAI: 5. MLOps

- How CEOs discuss selected LLMs and LLM providers

- GenAI services: Competitive landscape

- GenAI services: Competitive landscape (market share)

- GenAI services: Accenture

- GenAI services: Deloitte

- GenAI services: Capgemini

- GenAI services: IBM

6. End user adoption

- Chapter overview: End user adoption

- Analysis of 530 GenAI projects: Overview

- Analysis of 530 GenAI projects: By department

- Analysis of 530 GenAI projects: By department and activity

- Analysis of 530 GenAI projects: By industry

- Analysis of 530 GenAI projects: By industry and department

- Analysis of 530 GenAI projects: Crossing the chasm

- Key case studies: Example - Klarna

- Key case studies: Example - Westnet

- Key case studies: Example - Covered California

- Manufacturing deep dive: Overview of 20 GenAI solutions at HMI 24

- Manufacturing deep dive: GenAI solutions highlighted at HMI 2024

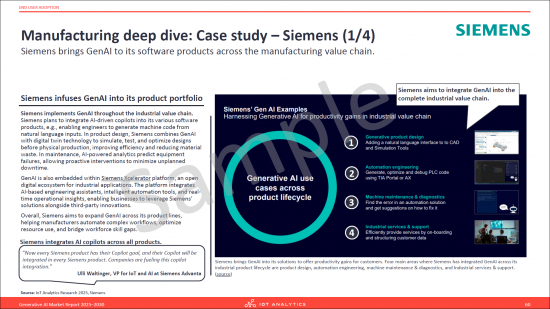

- Manufacturing deep dive: Case study - Siemens

- Manufacturing deep dive: Survey stats - Top AI use cases in manufacturing

- Tech & TelCo deep dive: GenAI solutions highlighted at MWC 2024

- Tech & TelCo deep dive: Case study 1 - Vodafone

- Tech & TelCo deep dive: Case study 2 - Soracom

- Tech & TelCo deep dive: Case study 3 - SAP

7. GenAI applications landscape & business model considerations

- Chapter overview: GenAI application landscape & business model considerations

- GenAI applications landscape 2024

- Considerations on GenAI business models

- Consideration 1

- Consideration 2

- Consideration 3

- Consideration 4

- Consideration 5

- Consideration 6

- Consideration 7

8. Trends & challenges

- Chapter overview: Trends & challenges

- Trend 1

- Trend 2

- Trend 3

- Trend 4

- Trend 5

- Trend 6

- Trend 7

- Trend 8

- Trend 9

- Challenge 1

- Challenge 2

- Challenge 3

- Challenge 4

- Challenge 5

- Challenge 6

- Challenge 7: Other challenges

9. Methodology

10. About IoT Analytics

- 発行日

- 発行

- IoT Analytics GmbH

- ページ情報

- 英文 263 Pages

- 納期

- 即日から翌営業日