|

|

市場調査レポート

商品コード

1398976

先を行くために - 半導体産業分析 (2023年):レポートセット (7冊) - 台湾・中国・世界のIC設計・IC製造 (ファウンドリ、メモリ)・IC OSAT産業の洞察とサプライチェーンStay Ahead - 2023 Semiconductor Industry Research Value Pack: 7 Reports Bundle Encompasses IC Design, IC Manufacturing (Foundry, Memory) and IC OSAT Industry Insights and Supply Chains in Taiwan, China, and the World |

||||||

|

|

|||||||

|

|||||||

| 先を行くために - 半導体産業分析 (2023年):レポートセット (7冊) - 台湾・中国・世界のIC設計・IC製造 (ファウンドリ、メモリ)・IC OSAT産業の洞察とサプライチェーン |

|

出版日: 2023年11月24日

発行: MIC - Market Intelligence & Consulting Institute

ページ情報: 英文 80 Pages

納期: 即納可能

|

- 全表示

- 概要

- 図表

- 目次

エグゼクティブサマリー

このレポートパックでは、世界および中国・台湾のIC設計・IC製造 (ファウンドリ、メモリ)・IC OSAT (半導体組立・検査アウトソーシング) 業界について包括的に分析すると共に、各々のサプライチェーンの構造や最新情勢 (2022~2023年) について調査しております。

高いインフレ率やロシア・ウクライナ戦争などの悪材料にもかかわらず、世界の半導体産業は2022年を通じて二桁台の成長を維持しています。この動きを支えているのが、上半期の増収や、ネットワーク・データセンター用チップの堅調な販売です。世界の半導体の市場規模は2023年に、マクロ経済環境全般の影響を受け、10.1%減の5,161億米ドルになると予想されます。なかでもメモリーIC部門は今年最も大きな影響を受けました。幸いなことに、2023年第1四半期以降、世界の主要メモリICメーカーは減産制御を実施し、出荷価格を安定させました。前年比成長率が46.3%と予想されたメモリIC業界では、2024年に市場規模が1,343億米ドルに達し、2025年と2026年にもそれぞれ前年比成長率38.7%と13.1%の高成長が続くと予想されます。この分野は今後3年間、世界半導体市場の成長を牽引する主要な原動力になると予想されます。

目次

世界のIC設計業界:概要 (2022年) と発展 (2023年)

第1章 世界のIC設計産業の発展 (2022年)

- 世界のIC設計企業トップ10のランキング (2022年)

- IC設計業界の全体的な業績 (2022年)

第2章 大手IC設計企業の事業展開状況 (2022年)

- Qualcomm、MediaTek

- Nvidia、AMD

- Broadcom、Marvell

第3章 世界のIC設計産業の発展 (2023年)

- スマートフォン・PC市場の回復の遅れにより、2023年下半期の見通しは不透明となる

- AI向け用途の台頭が、クラウドサーバーとエッジコンピューティングチップの機会を促進する

付録

- 企業一覧

- 世界の半導体ファウンドリ業界:概要 (2022年) と発展 (2023年)

第1章 世界のファウンドリ業界の概要 (2022年)

- 世界の半導体ファウンドリの市場規模 (2022年)

- 世界の半導体ファウンドリ上位10社のランキング (2022年)

- 半導体ファウンドリ業界の全体的な業績 (2022年)

第2章 主要な半導体ファウンドリの開発動向 (2022年)

- TSMC

- Samsung

- UMC、PSMC、Vanguard

- SMIC

- GlobalFoundries

第3章 世界の半導体ファウンドリ産業の発展(2023年)

- ファウンドリの操業状態は2023年上半期に底打ちする見込みの一方、回復ペースは2023年下半期も不透明

- Intelの新しいIFSビジネスモデルが、世界の半導体ファウンドリの情勢を変える

付録

- 企業一覧

- 世界のICパッケージング・検査業界:総括 (2022年) と発展 (2023年)

第1章 世界のICパッケージング・検査業界の概要 (2022年)

- 世界のICパッケージング・検査業界の市場規模と、上位10社のOSATランキング (2022年)

- 世界のICパッケージング・検査業界の全体的な業績 (2022年)

第2章 主要OSAT企業の経営実績 (2022年)

- ASE Holdings、PTI、KYEC

- Amkor、JCET

第3章 世界のICパッケージング・検査業界の展望

- 家電製品の需要が低迷する中、OSATは車載用チップに焦点を移す

- 大手企業が、HPC・AI向け用途の新たな動向に対応するため、先進パッケージング技術の開発を加速

付録

- 企業一覧

- 中国のIC設計産業の発展と主要企業

第1章 中国のIC設計業界の概要

- IC設計業界の市場規模の推移

- IC設計業界の企業分布

- IC設計企業数の推移

- IC設計企業の分布:規模別

- IC設計製品の分布:カテゴリー別

第2章 中国における大手IC設計企業の展開

- Huawei HiSilicon

- Unisoc

- GigaDevice

- Will Semiconductor

第3章 中国におけるのIC設計産業の発展

- 中国のIC自給率

- EDA輸出禁止のその後の影響

第4章 MICの視点

付録

- 企業一覧

- 中国のICパッケージング・検査業界の発展と主要企業

第1章 中国のICパッケージング・検査産業の発展

- 中国のICパッケージング・検査業界の市場規模と近年の変化

- 中国のICパッケージング・検査業界の企業の地域分布

第2章 中国におけるの主要なICパッケージング・検査企業の発展

- 中国のICパッケージング・検査企業:上位10社のランキング

- 中国のICパッケージング・検査企業:上位3社の近年の業績

- JCET

- Tongfu Microelectronics

- Huatian Technology

第3章 業界の展望

- 国家集積回路産業投資基金の効果

- 米中対立の影響と中国からのデカップリング

- 中国は先進プロセス技術の障害を受けて、車載用半導体に焦点を移す

付録

- 企業一覧

- 台湾の半導体業界の情勢:2023年およびそれ以降

- 世界の半導体産業における台湾の地位と発展

- 台湾の半導体産業の主要分野の発展

- 台湾の半導体産業の主な発展 (2023年第3四半期以降)

第1章 半導体産業の発展

- IC設計

- ピークシーズンの業績は、期待に応えられない (2023年下半期)

- AIブームが続く中、IC設計企業は複数の用途に多角化

- IC製造

- ウエハーファウンドリの見通しは慎重:受注の可視性が低いため

- メモリの需要・供給は、2023年第4四半期から2024年上半期にかけて安定すると予想

- ICパッケージング・検査

- 消費者市場の勢いの回復に応じたピークシーズンの影響

- HPC・AI用途の新たな動向による、先進パッケージング・検査需要の継続的拡大

付録

- 企業一覧

List of Topics

Development of the global, China, and Taiwan IC design industry in 2022-2023, covering respective company rankings, their performance overview in 2022, and development strategies of major players such as Qualcomm, MediaTek, Nvidia, AMD, Broadcom, Marvell, Huawei Hisilicon, Unisoc, GigaDevice, Will Semiconductor, etc.

Development of the global and Taiwan semiconductor foundry industry in 2022-2023, addressing respective foundry rankings, their performance overview in 2022, and development strategies of key players such as TSMC, Samsung, UMC, PSMC, VSI (Vanguard), SMIC, GlobalFoundries, etc.

Development of the global, China, and Taiwan IC OSAT (Outsourced Semiconductor Assembly and Testing) industry in 2022-2023, including respective foundry rankings, their performance overview, and development strategies of key players such as ASE, PTI, KYEC, Amkor, JCET, Tongfu Microelectronics, Huatian Technology, etc.

Companies covered

Alchip

Amazon

AMD

Amkor

Apple

Ardentec

ASE Group

ASEN Semiconductors

Baidu

Biren

Bitmain

Cadence

Geely

Bosch

Broadcom

China Wafer Level

Chipmore Technology

ChipMOS

Chrysler

DB HiTek

Dell

Denso

Episil

Faraday

FlipChip International

FocalTech

Ford

Forehope Electronic

Formosa Advanced

General Motors

GigaDevice

Global Unichip

GlobalFoundries

Google

Hana Microelectronics

Himax

HiSilicon

Hongxin Semiconductor

HP

HSMC

Huawei

Jinan Quanxin

Macronix

Hua Hong Semiconductor

Huahong Group

Huatian Technology

Infineon

Intel

Inventec

JCET

Kore Semiconductor

KYEC

Lingsen Precision

Macronix

Marvell

MediaTek

MediaTek

Micron

OmniVision

Qualcomm

RDA Microelectronics

Siemens

Silead

Micron

Mosel

Nanya Technology

Nepes

Nexchip

Novatek

Nuvoton

Nvidia

NXP

Onsemi

Open AI

Orient Semiconductor

Payton Technology

Powertech Technology

PSMC

Qorvo

Qualcomm

Quanta

Realtek

Samsung

SFA

Sigurd Microelectronics

Siliconware

SJ Semiconductor

SK Hynix

Skyworks

SMIC

Sony

Spreadtrum

Synopsys

STATS ChipPAC

STMicroelectronics

Sunplus

Supermicro

Texas Instruments

Tongfu Electronics

Tower

Tsinghua Unigroup

TSMC

UMC

Unimos Microelectronics

Unisem

Unisoc

Unitech Holdings

UTAC

Vanguard

VIS

Walton Advanced Engineering

Will Semiconductor

Winbond

Wise Road Capital

Wistron

Xilinx

YTEC

Executive Summary

This pack offers comprehensive insights into the IC design, IC manufacturing (foundry, memory), and IC OSAT (Outsourced Semiconductor Assembly and Testing) sectors, covering global, Taiwan, and China, along with their respective supply chains for the period 2022-2023 and beyond.

Despite adverse factors such as high inflation rates and the Russia-Ukraine war, the global semiconductor industry sustained double-digit growth throughout 2022, supported by higher revenue in the first half and robust sales of networking and data center chips. In 2023, the global semiconductor market is expected to have declined by 10.1% to US$516.1 billion under the influence of the overall macroeconomic environment. Among them, the memory IC sector has been the most affected this year. Fortunately, since the first quarter of 2023, major global memory IC manufacturers have implemented production reduction controls, stabilizing shipment prices. With an expected year-on-year growth of 46.3%, the memory IC sector is anticipated to reach US$134.3 billion in 2024 and continue high growth in 2025 and 2026, with year-on-year growth rates of 38.7% and 13.1%, respectively. This sector is expected to be a major driving force for the global semiconductor market growth in the next three years.

Table of Contents

- 2022 Recap and 2023 Development of the Global IC Design Industry

1.Development of the Global IC Design Industry in 2022

- 1.1 Ranking of Global Top Ten IC Design Companies in 2022

- 1.2 IC Design Industry's Overall Performance in 2022

2. Major IC Design Companies' Business Operations in 2022

- 2.1 Qualcomm & MediaTek

- 2.2 Nvidia & AMD

- 2.3 Broadcom & Marvell

3.Development of the Global IC Design Industry in 2023

- 3.1 Uncertain Outlook for 2H23 Due to Slow Recovery in the Smartphone and PC Markets

- 3.2 Rise of AI Applications Driving Opportunities for Cloud Server and Edge Computing Chips

Appendix

- List of Companies

- 2022 Recap and 2023 Development of the Worldwide Semiconductor Foundry Industry

1.Global Foundry Industry Recap 2022

- 1.1 Global Semiconductor Foundry Market Size in 2022

- 1.2 Top Ten Global Semiconductor Foundry Rankings in 2022

- 1.3 Overall Performance of the Semiconductor Foundry Industry in 2022

2. Development Trends of Major Semiconductor Foundries in 2022

- 2.1 TSMC

- 2.2 Samsung

- 2.3 UMC, PSMC, Vanguard

- 2.4 SMIC

- 2.5 GlobalFoundries

3. Global Semiconductor Foundry Industry Development in 2023

- 3.1 Foundry Operations Expected to Bottom Out in 1H23, Recovery Pace Remains Uncertain in 2H23

- 3.2 Intel’s New IFS Business Model to Change the Global Semiconductor Foundry Landscape

Appendix

- List of Companies

- 2022 Recap and 2023 Development of the Global IC Packaging and Testing Industry

1. Recap of the Global IC Packaging and Testing Industry in 2022

- 1.1 Market Size and Top Ten OSAT Rankings in the Global IC Packaging and Testing Industry in 2022

- 1.2 Overall Performance of the Global IC Packaging and Testing Industry in 2022

2.Operational Performance of Major OSAT Companies in 2022

- 2.1 ASE Holdings, PTI, KYEC

- 2.2 Amkor, JCET

3. Outlook for the Global IC Packaging and Testing Industry

- 3.1 OSATs Shifting Focus to Automotive Chips While Consumer Electronics Demand Weakening

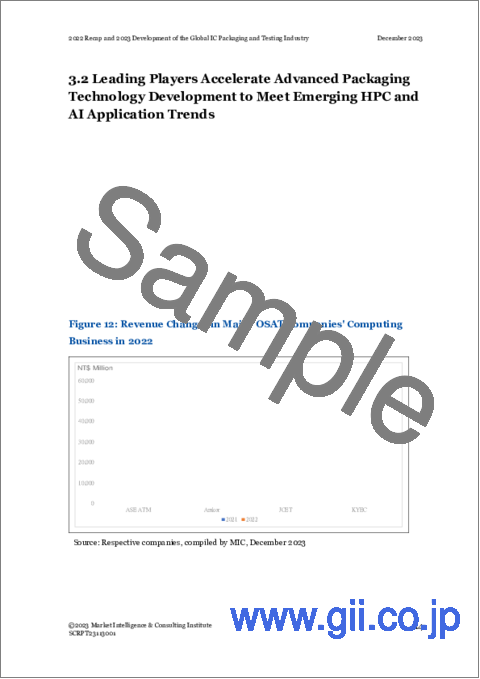

- 3.2 Leading Players Accelerate Advanced Packaging Technology Development to Meet Emerging HPC and AI Application Trends

Appendix

- List of Companies

- Development of the IC Design Industry and Major Players in China

1.Overview of the IC Design Industry in China

- 1.1 Changes in the Market Size of the IC Design Industry

- 1.2 Distribution of IC Design Industry Players

- 1.2.1 Changes in the Number of IC Design Companies

- 1.2.2 Distribution of IC Design Industry Players by Scale

- 1.2.3 Distribution of IC Design Products by Category

2. Development of Major IC Design Companies in China

- 2.1 Huawei HiSilicon

- 2.2 Unisoc

- 2.3 GigaDevice

- 2.4 Will Semiconductor

3. Development of the IC Design Industry in China

- 3.1 Independent IC Supply Rate in China

- 3.2 The Subsequent Impact of the EDA Ban

4.MIC Perspective

Appendix

- List of Companies

- Development of the China IC Packaging and Testing Industry and Key Players

1.Development of China IC Packaging and Testing Industry

- 1.1 Market Size and Recent Changes in China's IC Packaging and Testing Industry

- 1.2 Regional Distribution of IC Packaging and Testing Industry Players in China

2.Development of major IC Packaging and Testing Players in China

- 2.1 Ranking of the Top-10 Chinese IC Packaging and Testing Companies

- 2.2 Recent Performance of the Top-3 Chinese IC Packaging and Testing Companies

- 2.2.1 JCET

- 2.2.2 Tongfu Microelectronics

- 2.2.3 Huatian Technology

3.Outlook for the Industry

- 3.1 Effects of National Integrated Circuit Industry Investment Fund

- 3.2 Impact of US-China Conflict and Decoupling from China

- 3.3 China Shifting Focus to Automotive Semiconductors Following Obstacles in Advanced Process Technology

Appendix

- List of Companies

- Taiwanese Semiconductor Industry Landscape, 2023 and Beyond

- Taiwan's Global Position and Development in the Semiconductor Industry

- Development of Taiwan's Major Semiconductor Industry Sectors

- Key Developments in the Taiwan Semiconductor Industry, 3Q 2023 and Beyond

1.Development of the Semiconductor Industry

- 1.1 IC Design

- 1.1.1 Peak Season Performance Fails to Meet Expectations in 2H23

- 1.1.2 IC Design Firms Diversify into Multiple Applications amid Continued AI Boom

- 1.2 IC Manufacturing

- 1.2.1 Wafer Foundry Outlook Cautious due to Low Order Visibility

- 1.2.2 Memory Supply and Demand Expected to Stabilize during 4Q23 to 1H24

- 1.3 IC Packaging and Testing

- 1.3.1 Peak Season Effect Depending on Consumer Market Momentum Pickups

- 1.3.2 Emerging Trends in HPC and AI Applications Continue to Drive Demand for Advanced Packaging and Testing

Appendix

- List of Companies

List of Tables

- 2022 Recap and 2023 Development of the Global IC Design Industry

- Table 1 Ranking of Global Top Ten IC Design Companies in 2022

- 2022 Recap and 2023 Development of the Worldwide Semiconductor Foundry Industry

- Table 1: Top Ten Global Semiconductor Foundry Rankings in 2022

- 2022 Recap and 2023 Development of the Global IC Packaging and Testing Industry

- Table 1 Global Top Ten OSAT Rankings in 2022

- Development of the China IC Packaging and Testing Industry and Key Players

- Table 1 Ranking of the Top-10 Chinese IC Packaging and Testing Companies in 2022

List of Figures

- 2022 Recap and 2023 Development of the Global IC Design Industry

- Figure 1 Leading IC Design Companies' Changes in Inventory Turnover Days, 1Q21 - 1Q23

- Figure 2 Leading IC Design Companies' Revenue Changes, 1Q22 - 1Q23

- Figure 3 Qualcomm's 2022 Revenue by Product Line

- Figure 4 MediaTek's 2022 Revenue by Product Line

- Figure 5 Nvidia's 2022 Revenue by Product Line

- Figure 6 AMD's 2022 Revenue by Product Line

- Figure 7 Broadcom's 2022 Revenue by Semiconductor Solutions Product Line

- Figure 8 Marvell's 2022 Revenue by Product Line

- 2022 Recap and 2023 Development of the Worldwide Semiconductor Foundry Industry

- Figure 1 Comparison of Major Foundries’ Gross Margin Changes, 2021 - 2022

- Figure 2 TSMC’s Revenue Changes by Product Applications, 2021-2022

- Figure 3 Samsung’s Revenue Changes by Business Segments, 2021-2022

- Figure 4 UMC’s Revenue Changes by Product Applications, 2021-2022

- Figure 5 PSMC’s Revenue Changes by Product Applications, 2021-2022

- Figure 6 Vanguard’s Revenue Changes by Product Applications, 2020-2021

- Figure 7 SMIC’s Revenue Changes by Product Applications, 2021-2022

- Figure 8 GlobalFoundries’ Revenue Changes by Product Applications, 2021-2022

- Figure 9 Intel's IDM 2.0 Business Model

- 2022 Recap and 2023 Development of the Global IC Packaging and Testing Industry

- Figure 1: Revenue Changes of Major OSAT Companies, 1Q22 - 2Q23

- Figure 2: Gross Margin Changes of Major OSAT Companies, 1Q22 - 2Q23

- Figure 3: ASE ATM’s Revenue Changes by Product Application, 2020 - 2022

- Figure 4: ASE ATM’s Revenue Changes by Packaging & Testing Product Portfolio, 2020 - 2022

- Figure 5: PTI's Revenue Changes by Services, 2020 - 2022

- Figure 6: PTI's Revenue Changes by Products, 2020 - 2022

- Figure 7: KYEC's Revenue Changes by Process Nodes, 2020 - 2022

- Figure 8: KYEC's Revenue Changes by Product Applications, 2020 - 2022

- Figure 9: Amkor's Revenue Changes by Packaging & Testing Types, 2020 - 2022

- Figure 10: Amkor's Revenue Changes by End Product Applications, 2020 - 2022

- Figure 11: JCET's Revenue Changes by End-Product Applications, 2021 - 2022

- Figure 12: Revenue Changes in Major OSAT Companies' Computing Business in 2022

- Development of the IC Design Industry and Major Players in China

- Figure 1. Shipment Value of the Semiconductor Industry in China, 2017-2021

- Figure 2. IC Design Market Size and Changes in China, 2017-2022

- Figure 3. Changes in the number of IC Design Companies in China from 2016 to 2022

- Figure 4. Scale Distribution of IC Design Industry in China in 2022

- Figure 5. Distribution of IC Design Product Revenue and Number of IC Design Companies in China

- Figure 6. GigaDevice’s Financial Report Performance from the First Quarter of 2021 to the Third Quarter of 2022

- Figure 7. GigaDevice's Revenue Proportion of Each Product Line, 1H 2020 - 1H 2022

- Figure 8. Will Semiconductor's Financial Report Performance, 1Q 2021 - 3Q2022

- Figure 9. Revenue Proportion of Will Semiconductor’s Product Lines in 2019-2021

- Figure 10. Changes in IC Self-Sufficiency Rate in China, 2010-2026

- Development of the China IC Packaging and Testing Industry and Key Players

- Figure 1 Chinese IC Packaging and Testing Shipment Value, 2018-2022

- Figure 2 Regional Distribution of IC Packaging and Testing Brands in China

- Figure 3 Financial Information of JCET, 2018-2022

- Figure 4 Revenue of JCET by Product Application, 2021-2022

- Figure 5 Financial Information of Tongfu Microelectronics, 2018-2022

- Figure 6 Financial Information of Huatian Technology, 2018-2022