|

|

市場調査レポート

商品コード

1321379

北米の酸素濃縮器の市場規模、シェア、動向分析レポート:製品別、技術別、用途別、国別、セグメント別予測、2023年~2030年North America Oxygen Concentrators Market Size, Share & Trends Analysis Report By Product (Portable, Fixed), By Technology (Continuous Flow, Pulse Flow), By Application, By Region, And Segment Forecasts, 2023 - 2030 |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| 北米の酸素濃縮器の市場規模、シェア、動向分析レポート:製品別、技術別、用途別、国別、セグメント別予測、2023年~2030年 |

|

出版日: 2023年07月13日

発行: Grand View Research

ページ情報: 英文 250 Pages

納期: 2~10営業日

|

- 全表示

- 概要

- 図表

- 目次

北米の酸素濃縮器市場の成長と動向

Grand View Research社の最新レポートによると、北米の酸素濃縮器の市場規模は2030年までに19億4,000万米ドルに達すると予測されています。

2023年から2030年までのCAGRは5.4%と予測されています。同市場の成長は、先進的な製品の提供、事業運営の拡大、呼吸器疾患の罹患率の増加、在宅酸素療法への嗜好の高まりなど、さまざまな要因によってもたらされます。例えば、2022年5月、Sanrai International社はDrive DeVilbiss社との協業により1060AW 10L Stationary Oxygen Concentratorを発売し、業界の技術革新への取り組みを浮き彫りにしました。さらに同市場は、導入が大幅に増加しているポータブル酸素濃縮器の需要拡大からも恩恵を受ける態勢が整っています。

2015年から2021年にかけて、米国市場ではポータブル酸素濃縮器の普及率が8%から22%に上昇しました。この動向は予測期間中の市場成長を促進するとみられます。COVID-19パンデミックは地域市場に限定的なプラスの影響を与えました。入院患者の急増により、医療施設は人工呼吸器の供給が限られているため、重症患者に呼吸補助を提供する際の課題に直面しました。その結果、代替ソリューションとしての酸素濃縮器の需要が増加しました。さらに、患者の意識を高めるための政府の取り組みも市場の成長に寄与しています。例えば、米国政府は2021年6月、米国国際開発庁(USAID)を通じて、COVID-19パンデミック対策としてハイチに酸素濃縮器50台を寄贈しました。

この寄贈は、医療インフラを強化し、ハイチの医療を支援するための先進技術と酸素機器を提供するという、より広範なイニシアティブに沿ったものです。さらに、医療インフラ整備のための政府資金は、先進的で費用対効果の高い機器の需要を促進すると予想されます。モノのインターネット(IoT)技術の統合は医療機器業界に革命をもたらし、従来の方法に比べて大きなメリットをもたらしています。IoT対応の酸素濃縮器は遠隔モニタリングと管理を可能にし、医療プロバイダーはリアルタイムで酸素濃度をモニタリングし、より良い患者の転帰のために流量を調整することができます。

この統合が予測期間中の市場成長を促進すると予測されています。レスピロニクス社、イノジェン社、ケアメディカル社など、業界の有力企業は、製品ラインアップとリーチを拡大するための戦略的イニシアチブを実施しています。こうした取り組みには、買収、提携、事業拡大、新製品の発売などが含まれます。例えば、Inogen社は2023年1月のプレスリリースで、2022年12月9日に新しい携帯型酸素濃縮器Rove 4の米国FDAからの認可を取得したと発表しました。この進歩により、携帯型酸素濃縮器市場におけるInogen社の地位はさらに強固なものとなると思われます。

北米の酸素濃縮器市場レポートハイライト

- 製品別では、ポータブル医療用酸素濃縮器(POC)セグメントが2022年の売上高で53.8%の最大市場シェアを占めました。この優位性は、POCに関連する多くの利点によるものです。

- 用途別では、在宅ケアセグメントが市場を独占し、2022年の市場収益シェアの66.1%を占めました。優位性の主な要因は、在宅医療に対する需要の増加と、快適で便利な治療に対する患者の嗜好の変化です。

- 技術別では、連続フロー技術セグメントが2022年の収益シェア61.7%で市場を独占しました。このセグメントの成長は、急速な技術進歩と呼吸器疾患を患う患者の多さに起因しています。

- 業界各社は、革新的な製品の開発と先進技術の導入に注力しています。

目次

第1章 調査手法と範囲

- 市場セグメンテーションと範囲

- 市場の定義

- 調査手法

- 調査手法

- 調査範囲と前提条件

- データソースのリスト

第2章 エグゼクティブサマリー

第3章 北米の酸素濃縮器市場の変数、動向、および範囲

- 酸素濃縮器市場系統の見通し

- 親市場の見通し

- 付随市場の見通し

- 市場力学

- 市場促進要因の分析

- 市場抑制要因分析

- 業界の課題

- 北米の酸素濃縮器市場分析ツール

- 業界分析- ポーター

- PEST分析

- 規制と償還の枠組み

- COVID-19感染症の影響分析

- 国別の主要な疾患の推定有病率(2018年から2030年)

第4章 北米の酸素濃縮器市場:製品の推定・動向分析

- 定義と範囲

- 北米の酸素濃縮器市場:製品の変動分析、2022年および2030年

- ポータブル

- 固定

第5章 北米の酸素濃縮器市場:技術の推定・動向分析

- 定義と範囲

- 北米の酸素濃縮器市場:技術の変動分析、2022年および2030年

- 連続フロー

- パルスフロー

第6章 北米の酸素濃縮器市場:用途の推定・動向分析

- 定義と範囲

- 北米の酸素濃縮器市場:用途の変動分析、2022年および2030年

- 在宅ケア

- 非在宅ケア

第7章 北米の酸素濃縮器市場:国別の推定・動向分析

- 北米の市場シェア分析、2022年と2030年

- 北米の市場ダッシュボード

- 北米の市場スナップショット

- 北米の市場シェアと主要企業、2022年

- 市場規模、予測、数量および動向分析、2018年から2030年まで

- 北米

- 市場推計・予測、2018~2030年(金額・数量)

- 米国

- カナダ

第8章 競合分析

- 主要市場参入企業による最近の動向と影響分析

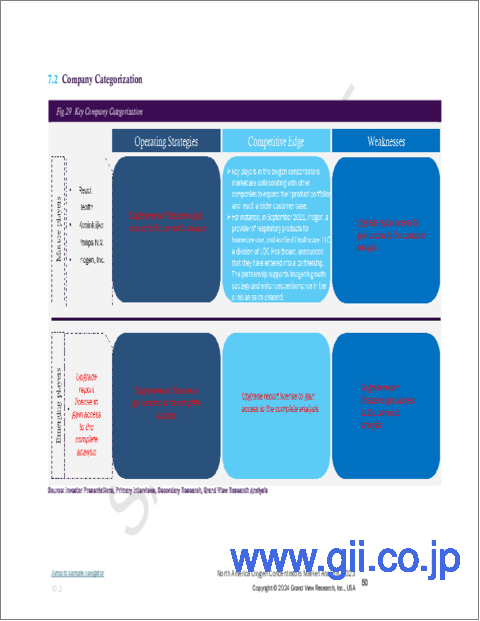

- 企業/競合の分類

- 企業の市場地位と市場シェアの分析

第9章 競合情勢

- 企業プロファイル

- Inogen, Inc.

- Respironics(a subsidiary of Koninklijke Philips NV)

- Invacare Corporation

- Caire Medical(a subsidiary of NGK Spark Plug)

- DeVilbiss Healthcare(a subsidiary of Drive Medical)

- O2 Concepts

- Nidek Medical Products, Inc.

List of Tables

- Table 1 List of Secondary Sources

- Table 2 List of Abbreviations

- Table 3 COPD estimated prevalence

- Table 4 Intertitial lung disease estimated prevalence

- Table 5 Key companies involved in M&As

- Table 6 Key companies undergoing collaborations and partnerships

- Table 7 Key companies undertaking other strategies

- Table 8 North America Oxygen Concentrators Market, By Country, 2018 - 2030 (USD Million)

- Table 9 North America Oxygen Concentrators Market, By Product, 2018 - 2030 (USD Million)

- Table 10 North America Oxygen Concentrators Market, By Application, 2018 - 2030 (USD Million)

- Table 11 North America Oxygen Concentrators Market, By Technology, 2018 - 2030 (USD Million)

- Table 12 U.S. Oxygen Concentrators Market, By Product, 2018 - 2030 (USD Million)

- Table 13 U.S. Oxygen Concentrators Market, By Application, 2018 - 2030 (USD Million)

- Table 14 U.S. Oxygen Concentrators Market, By Technology, 2018 - 2030 (USD Million)

- Table 15 Canada Oxygen Concentrators Market, By Product, 2018 - 2030 (USD Million)

- Table 16 Canada Oxygen Concentrators Market, By Application, 2018 - 2030 (USD Million)

- Table 17 Canada Oxygen Concentrators Market, By Technology, 2018 - 2030 (USD Million)

- Table 18 COPD estimated prevalence

- Table 19 Interstitial lung disease estimated prevalence

List of Figures

- Fig. 1 North America Oxygen Concentrators Market segmentation

- Fig. 2 Market research process

- Fig. 3 Information procurement

- Fig. 4 Primary research pattern

- Fig. 5 Market research approaches

- Fig. 6 Value chain-based sizing & forecasting

- Fig. 7 QFD modelling for market share assessment

- Fig. 8 Market formulation & validation

- Fig. 9 U.S. specific research methodology

- Fig. 10 U.S. specific research methodology

- Fig. 11 U.S. specific research methodology

- Fig. 12 U.S. specific research methodology

- Fig. 13 U.S. specific research methodology

- Fig. 14 U.S. specific research methodology

- Fig. 15 Oxygen Concentrators Market snapshot

- Fig. 16 Oxygen concentrators Segment Snapshot

- Fig. 17 Oxygen concentrators Segment Snapshot (continued)

- Fig. 18 Oxygen Concentrators Market competitive landscape snapshot

- Fig. 19 Market research process

- Fig. 20 Oxygen Concentrators Market: Parent market outlook (2022)

- Fig. 21 Market research process

- Fig. 22 Market driver analysis (Current & future impact)

- Fig. 23 Market restraints analysis (Current & future impact)

- Fig. 24 List of 24 notable U.S. FDA-approved POCs, 2021

- Fig. 25 Value-chain-based sizing & forecasting

- Fig. 26 North America Oxygen concentrators market: Product movement analysis, 2018 - 2030 (USD Million)

- Fig. 27 North America Oxygen concentrators market share analysis, 2022 & 2030

- Fig. 28 North America Fixed medical oxygen concentrators market, 2018 - 2030 (USD Million)

- Fig. 29 North America Portable medical oxygen concentrators market, 2018 - 2030 (USD Million)

- Fig. 30 North America Oxygen concentrators market: Application movement analysis, 2018 - 2030 (USD Million)

- Fig. 31 North America Oxygen concentrators market share analysis, 2022 & 2030

- Fig. 32 North America Homecare market, 2018 - 2030 (USD Million)

- Fig. 33 North America Non-home healthcare market, 2018 - 2030 (USD Million)

- Fig. 34 North America Oxygen concentrators market: Technology movement analysis, 2018 - 2030 (USD Million)

- Fig. 35 North America Oxygen concentrators market share analysis, 2022 & 2030

- Fig. 36 North America Continuous flow market, 2018 - 2030 (USD Million)

- Fig. 37 North America Pulse flow market, 2018 - 2030 (USD Million)

- Fig. 38 North America marketplace: Key takeaways

- Fig. 39 North America Oxygen concentrators market: Regional outlook, 2022 & 2030 (USD Million)

- Fig. 40 North America oxygen concentrators market, 2018 - 2030 (USD Million)

- Fig. 41 U.S. oxygen concentrators market, 2018 - 2030 (USD Million)

- Fig. 42 Canada oxygen concentrators market, 2018 - 2030 (USD Million)

- Fig. 43 Heat map analysis

North America Oxygen Concentrators Market Growth & Trends

The North American oxygen concentrators market size is projected to reach USD 1.94 billion by 2030, according to a new report by Grand View Research, Inc. It is anticipated to witness a CAGR of 5.4% from 2023 to 2030. The market's growth is driven by various factors, such as advanced product offerings, expanding business operations, increasing respiratory disease incidence, and a rising preference for home-based oxygen therapy. For instance, in May 2022, Sanrai International's collaboration with Drive DeVilbiss resulted in the launch of the 1060AW 10L Stationary Oxygen Concentrator, highlighting the industry's commitment to innovation. Moreover, the market is poised to benefit from the growing demand for portable oxygen concentrators, which have seen a significant increase in adoption.

From 2015 to 2021, the U.S. market witnessed a rise in portable oxygen concentrator penetration from 8% to 22%, as per U.S. Medicare claims data. This trend is expected to drive market growth in the forecast period. The COVID-19 pandemic had a limited positive impact on the regional market. Due to the surge in hospitalizations, medical facilities faced challenges in providing respiratory support to critically ill patients due to the limited availability of ventilators. As a result, the demand for oxygen concentrators as an alternative solution increased. In addition, government initiatives to raise patient awareness have contributed to market growth. For instance, in June 2021, the U.S. government, through the U.S. Agency for International Development (USAID), donated 50 oxygen concentrators to Haiti to combat the COVID-19 pandemic.

This contribution aligns with broader initiatives to enhance the medical infrastructure and provide advanced technology and oxygen equipment to support healthcare in Haiti. Furthermore, government funding for healthcare infrastructure development is expected to fuel the demand for advanced and cost-effective devices. Integrating Internet of Things (IoT) technology has revolutionized the medical device industry, providing significant benefits compared to traditional methods. IoT-enabled oxygen concentrators enable remote monitoring and management, allowing healthcare providers to monitor oxygen levels in real time and adjust the flow rate for better patient outcomes.

This integration is projected to drive market growth in the forecast period. Prominent players in the industry, including Respironics, Inogen, and Caire Medical, are implementing strategic initiatives to expand their product offerings and reach. These initiatives include acquisitions, collaborations, expansions, and new product launches. For instance, Inogen announced in a press release in January 2023 that the company received clearance from the U.S. FDA for their new portable oxygen concentrator, Rove 4, on December 9, 2022. This advancement would further solidify Inogen's position in the portable oxygen concentrators market.

North America Oxygen Concentrators Market Report Highlights

- In the product segment, the Portable Medical Oxygen Concentrators (POCs) segment held the largest market share of 53.8% in terms of revenue in 2022. This dominance is owing to the large number of benefits associated with POCs

- In the application segment, the home care segment dominated the market and accounted for 66.1% of the revenue share in the market in 2022. The key factors responsible for the dominance are the increasing demand for home healthcare therapies and changing patients' preferences for comfortable and convenient therapy

- On the basis of technology, the continuous flow technology segment dominated the market with a revenue share of 61.7% in 2022. The segment growth was attributed to rapid technological advancements and a high number of patients suffering from respiratory disorders

- Industry players are focusing on developing innovative products and adopting advanced technologies

Table of Contents

Chapter 1. Methodology and Scope

- 1.1. Market Segmentation and Scope

- 1.2. Market Definition

- 1.3. Research Methodology

- 1.3.1. Information Procurement

- 1.3.1.1. Purchased database

- 1.3.1.2. GVR's internal database

- 1.3.2. Primary Research

- 1.3.1. Information Procurement

- 1.4. Research Methodology

- 1.4.1. Approach - 1: Commodity Flow Analysis

- 1.4.2. Approach - 2: Volume Price Analysis

- 1.4.3. Segment Level Market Estimation

- 1.4.4. U.S. Specific And Other Research Methodology

- 1.5. Research Scope and Assumptions

- 1.6. List to Data Sources

Chapter 2. Executive Summary

- 2.1. Market Outlook

- 2.2. Segment Outlook (Product and Technology)

- 2.3. Segment Outlook (Application)

- 2.4. Competitive Insights

Chapter 3. North America Oxygen Concentrators Market Variables, Trends, & Scope

- 3.1. Oxygen Concentrators Market Lineage Outlook

- 3.1.1. Parent Market Outlook

- 3.1.2. Ancillary Market Outlook

- 3.2. Market Dynamics

- 3.2.1. Market Driver Analysis

- 3.2.2. Market Restraint Analysis

- 3.2.3. Industry Challenge

- 3.3. North America Oxygen Concentrators Market Analysis Tools

- 3.3.1. Industry Analysis - Porter's

- 3.3.1.1. Bargaining power of the suppliers

- 3.3.1.2. Bargaining power of the buyers

- 3.3.1.3. Threats of substitution

- 3.3.1.4. Threats from new entrants

- 3.3.1.5. Competitive rivalry

- 3.3.2. PEST Analysis

- 3.3.2.1. Political landscape

- 3.3.2.2. Economic and Social landscape

- 3.3.2.3. Technological landscape

- 3.3.3. Regulatory and Reimbursement Framework

- 3.3.4. COVID-19 Impact Analysis

- 3.3.4.1. COVID-19 Impact On Notable Market Players

- 3.3.4.1.1. Philips

- 3.3.4.1.2. Invacare Corporation

- 3.3.4.1.3. Inogen, Inc.

- 3.3.5. Estimated Prevalence of Key Conditions, by Country (2018 to 2030)

- 3.3.5.1. COPD

- 3.3.5.2. Interstitial Lung Disease

- 3.3.1. Industry Analysis - Porter's

Chapter 4. North America Oxygen Concentrators Market: Product Estimates & Trend Analysis

- 4.1. Definitions and Scope

- 4.2. North America Oxygen Concentrators Market: Product Movement Analysis, 2022 & 2030 (USD Million)

- 4.3. Portable Medical Oxygen Concentrators

- 4.3.1. North America portable medical oxygen concentrators market estimates and forecasts, 2018 - 2030 (USD Million)

- 4.4. Fixed Medical Oxygen Concentrators

- 4.4.1. North America fixed medical oxygen concentrators market estimates and forecasts, 2018 - 2030 (USD Million)

Chapter 5. Chapter 5 North America Oxygen Concentrators Market: Technology Estimates & Trend Analysis

- 5.1. Definitions & Scope

- 5.2. North America Oxygen Concentrators Market: Technology Movement Analysis, 2022 & 2030 (USD Million)

- 5.3. Continuous Flow

- 5.3.1. North America continuous flow market estimates and forecasts, 2018 - 2030 (USD Million)

- 5.4. Pulse Flow

- 5.4.1. North America pulse flow market estimates and forecasts, 2018 - 2030 (USD Million)

Chapter 6. North America Oxygen Concentrators Market: Application Estimates & Trend Analysis

- 6.1. Definitions & Scope

- 6.2. North America Oxygen Concentrators Market: Application Movement Analysis, 2022 & 2030 (USD Million)

- 6.3. Home Care

- 6.3.1. North America home care market estimates and forecasts, 2018 - 2030 (USD Million)

- 6.4. Non-home Care

- 6.4.1. North America non-home care market estimates and forecasts, 2018 - 2030 (USD Million)

Chapter 7. North America Oxygen Concentrators Market: Regional Estimates & Trend Analysis

- 7.1. North America market share analysis, 2022 & 2030

- 7.2. North America Market Dashboard

- 7.3. North America Market Snapshot

- 7.4. North America Market Share and Leading Players, 2022

- 7.5. Market Size, & Forecasts, Volume and Trend Analysis, 2018 to 2030

- 7.6. North America

- 7.6.1. Market estimates and forecast, 2018 - 2030 (Value & Volume)

- 7.6.2. U.S.

- 7.6.2.1. Market estimates and forecast, 2018 - 2030 (Value & Volume)

- 7.6.3. Canada

- 7.6.3.1. Market estimates and forecast, 2018 - 2030 (Value & Volume)

Chapter 8. Competitive Analysis

- 8.1. Recent Developments & Impact Analysis, By Key Market Participants

- 8.2. Company/Competition Categorization

- 8.3. Company Market Position and Market Share Analysis

Chapter 9. Competitive Landscape

- 9.1. Company Profiles

- 9.1.1. Inogen, Inc.

- 9.1.1.1. Company overview

- 9.1.1.2. Financial performance

- 9.1.1.3. Product benchmarking

- 9.1.1.4. Strategic initiatives

- 9.1.2. Respironics (a subsidiary of Koninklijke Philips N.V.)

- 9.1.2.1. Company overview

- 9.1.2.2. Financial performance

- 9.1.2.3. Product benchmarking

- 9.1.2.4. Strategic initiatives

- 9.1.3. Invacare Corporation

- 9.1.3.1. Company overview

- 9.1.3.2. Financial performance

- 9.1.3.3. Product benchmarking

- 9.1.3.4. Strategic initiatives

- 9.1.4. Caire Medical (a subsidiary of NGK Spark Plug)

- 9.1.4.1. Company overview

- 9.1.4.2. Financial performance

- 9.1.4.3. Product benchmarking

- 9.1.4.4. Strategic initiatives

- 9.1.5. DeVilbiss Healthcare (a subsidiary of Drive Medical)

- 9.1.5.1. Company overview

- 9.1.5.2. Financial performance

- 9.1.5.3. Product benchmarking

- 9.1.5.4. Strategic initiatives

- 9.1.6. O2 Concepts

- 9.1.6.1. Company overview

- 9.1.6.2. Financial performance

- 9.1.6.3. Product benchmarking

- 9.1.6.4. Strategic initiatives

- 9.1.7. Nidek Medical Products, Inc.

- 9.1.7.1. Company overview

- 9.1.7.2. Financial performance

- 9.1.7.3. Product benchmarking

- 9.1.7.4. Strategic initiatives

- 9.1.1. Inogen, Inc.