|

|

市場調査レポート

商品コード

1233243

感染性呼吸器疾患診断の米国市場規模、シェア、動向分析レポート製品タイプ別(機器、消耗品、サービス)、サンプルタイプ別、技術別、用途別最終用途別、セグメント予測、2023年~2030年U.S. Infectious Respiratory Disease Diagnostics Market Size, Share & Trends Analysis Report By Product Type (Instruments, Consumables, Services), By Sample Type, By Technology, By Application By End-use, And Segment Forecasts, 2023 - 2030 |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| 感染性呼吸器疾患診断の米国市場規模、シェア、動向分析レポート製品タイプ別(機器、消耗品、サービス)、サンプルタイプ別、技術別、用途別最終用途別、セグメント予測、2023年~2030年 |

|

出版日: 2023年02月24日

発行: Grand View Research

ページ情報: 英文 112 Pages

納期: 2~10営業日

|

- 全表示

- 概要

- 図表

- 目次

米国の感染性呼吸器疾患診断市場の成長と動向

Grand View Research, Inc.の最新レポートによると、米国の感染性呼吸器疾患診断市場は、2023年から2030年にかけて-10.1%のCAGRを記録し、2030年までに92億米ドルに達すると予測されています。

COVID-19検査の減少により、市場は減少すると予測されています。しかし、米国の感染性呼吸器疾患診断市場は、技術の進歩、感染性呼吸器疾患の有病率の増加、市場の需要増に対応するための新規・革新的な製品を開発するための主要企業、政府、NGOによる高い研究開発投資によって牽引されると予測されます。

例えば、2021年1月、Biomedical Advanced Research and Development Authority(BARDA)は、QIAGEN LLCとDiaSorin Molecular LLCにそれぞれ598,000米ドルと679,000米ドルを資金提供してCOVID-19テストキットと機器の開発を強化しました。

疾病診断に使用される革新的な製品のイントロダクションは、米国の呼吸器感染症市場の成長を促進すると予想されます。2020年4月、Bio-Rad Laboratories, Inc.は、COVID-19患者の診断のためのイムノアッセイ試験キットを発表しました。これらは血液ベースのイムノアッセイ検査キットでした。イムノアッセイの初期予備性能において、このテストキットは700人以上の患者で99.0%以上の特異性を示しました。

また、パーキンエルマー社は、2022年9月に米国FDAから、結核スポットの自動化にT細胞選択試薬検査キットを使用することの承認を得ました。同製品は、世界的に規制されている酵素結合免疫吸着スポット(ELISPOT)インターフェロン-γ放出アッセイを用いて、潜在性結核感染症を検出します。このELISPOT検査により、検査室は潜在性結核患者に対して正確な結果を提供することができます。このように、感染性呼吸器疾患診断の技術的進歩が市場を活性化させています。

さらに、分子診断薬は、迅速かつ効果的な結果を提供することで、感染症検査において重要な役割を担っています。米国疾病予防センター(CDC)によると、2021年時点での結核の推定罹患率は人口10万人あたり2.4件でした。同様に、米国胸部学会によると、肺炎は年間約100万人が罹患し、5万人がこの病気で死亡しています。このように、呼吸器感染症の発生率の増加は、調査期間中、米国の感染性呼吸器疾患診断市場を牽引すると予想されます。

一方、規制の枠組みが曖昧であることや診断薬の価格が高いことが、調査期間中の米国感染性呼吸器疾患診断市場の妨げになる可能性があります。分子・免疫測定検査に関連するコストが高いこと、代替検査製品がないことも、米国における感染性呼吸器疾患診断製品の価格上昇の主な理由となっています。

しかし、ヘルスケア当局は、メーカーの高コスト負担を軽減するための措置を講じています。米国FDAから取得したCOVID-19検査のEUAは、開発コストを最小化し、より多くの検査施設で利用できるようにするためのプロセスを加速させることが期待されます。したがって、開発コストの削減は、医療従事者や患者にとって検査の購入しやすさを向上させると予想されます。

米国の感染性呼吸器疾患診断市場レポートハイライト。

- 2022年の感染性呼吸器疾患診断市場は、消耗品分野が約65.78%の収益シェアを占め、高い使用率に起因していると考えられます。アッセイや検査キットの研究開発の増加と、カウンター&セルフテスト製品に加え、ポイントオブケアに対する需要の増加が、このセグメントの成長を促進すると予想されます。

- サンプルタイプ別では、迅速抗原検出検査、直接蛍光抗体、ポリメラーゼ連鎖反応など様々な検査の実施に広く応用され、需要の増加と相まって、2022年の市場は鼻咽頭スワブが60.61%の推定シェアで支配していました。

- 2022年には、COVID-19、インフルエンザ、RSVなどの診断に使用されるRT-PCRテストの需要増により、分子診断セグメントが63.74%の収益シェアで感染性呼吸器疾患診断市場を独占しました。

- COVID-19セグメントは、高い発症率、製品承認の増加、革新的な製品に係る研究開発の増加により、2022年に91.65%のシェアで米国の感染性呼吸器疾患診断市場を独占しました。しかし、米国で実施されている大規模なワクチン接種の推進により、病気の発生率が低下するため、2030年には69.97%までシェアが低下すると予想されます。

目次

第1章 調査手法と範囲

- 市場セグメンテーションと範囲

- セグメントの範囲

- 調査手法

- 情報調達

- 購入したデータベース:

- Gvrの内部データベース

- 二次情報

- 1次調査

- 1次調査の詳細

- 情報またはデータ分析

- データ分析モデル

- 市場の策定と検証

- モデルの詳細

- コモディティフロー分析

- アプローチ:商品フローアプローチ

- コモディティフロー分析

- 調査の仮定

- 二次情報のリスト

- 略語一覧

- 目的

第2章 エグゼクティブサマリー

- 市場のスナップショット

- セグメントのスナップショット(1/3)

- セグメントのスナップショット(2/3)

- セグメントのスナップショット(3/3)

- 競合情勢のスナップショット

第3章 米国の感染性呼吸器疾患診断市場の変数、動向、および範囲

- 親市場の見通し

- 浸透と成長の見通しのマッピング

- 市場促進要因分析

- 米国における感染性呼吸器疾患の有病率の高さ

- 呼吸器疾患検査における技術の進歩

- 呼吸器疾患検査への研究開発投資の増加

- 市場抑制要因分析

- 診断製品の高価格

- あいまいな規制枠組みの存在

- SWOT分析、要因別(政治と法律、経済、技術)

- 業界分析- ポーターズ

- 規制の枠組み

- 償還シナリオ

第4章 米国の感染性呼吸器疾患診断市場:セグメント分析、製品タイプ別、2018年から2030年(百万米ドル)

- 定義と範囲

- 米国の感染性呼吸器疾患診断市場:製品タイプの変動分析

- 機器

- 画像検査

- 呼吸計測機器

- その他の楽器

- 消耗品

- サービス

第5章 米国の感染性呼吸器疾患診断市場:セグメント分析、サンプルタイプ別、2018年から2030年(百万米ドル)

- 定義と範囲

- 米国の感染性呼吸器疾患診断市場:サンプルタイプの変動分析

- 唾液

- 鼻咽頭スワブ(Nps)

- 前鼻領域

- 血

- その他

第6章 米国の感染性呼吸器疾患診断市場:セグメント分析、技術別、2018年から2030年(百万米ドル)

- 定義と範囲

- 米国の感染性呼吸器疾患診断市場:技術変動分析

- イムノアッセイ

- 分子診断学

- 微生物学

- その他の技術

第7章 米国の感染性呼吸器疾患診断市場:セグメント分析、アプリケーション別、2018年から2030年(百万米ドル)('000年代)

- 米国の感染性呼吸器疾患診断市場:アプリケーションの変動分析

- COVID-19

- COVID-19市場、2018~2030年(ボリューム'000s)

- インフルエンザ

- インフルエンザ市場、2018~2030年(ボリューム'000s)

- RSウイルス

- 呼吸器合胞体ウイルス市場、2018~2030年(ボリューム'000s)

- 結核

- 結核市場、2018~2030年(ボリューム'000s)

- 連鎖球菌検査

- レンサ球菌検査市場、2018年から2030年(ボリューム'000s)

- その他の呼吸器疾患検査

- その他の呼吸器疾患検査市場、2018年~2030年(ボリューム'000s)

第8章 米国の感染性呼吸器疾患診断市場:セグメント分析、最終用途別、2018年から2030年(百万米ドル)

- 米国の感染性呼吸器疾患診断市場:エンドユースの変動分析

- 病院

- 診断検査室

- 診療所

- その他のエンドユーザー

第9章 米国の感染性呼吸器疾患診断市場:競合分析

- 参加者の概要

- 財務実績

- 参入企業

- 市場のリーダー

- 米国の感染性呼吸器疾患診断市場シェア分析、2022年

- 戦略マッピング

- 拡張

- 取得

- コラボレーション

- 製品/サービスの発売

- パートナーシップ

- その他

- ベンダー情勢

- ディストリビューターおよびチャネルパートナーのリスト

- 主要顧客

- 市場のリーダー

- 競合ダッシュボード分析

- 非公開会社

- 新興企業/テクノロジーディスラプター/イノベーターのリスト

- 地域ネットワークマップ

- Abbott

- Koninklijke Philips N.V.

- Siemens Healthcare GmbH

- BIOMERIEUX

- Danaher

- QIAGEN

- BD

- F. Hoffmann-La Roche Ltd

- Quidel Corporation

- Thermo Fisher Scientific, Inc.

- 非公開会社

List of Tables

- Table 1 List of secondary sources

- Table 2 List of abbreviations

- Table 3 CPT codes reimbursement of diagnostic tests

- Table 4 U.S. infectious respiratory disease diagnostics market by, product type, 2018 - 2030 (USD Million)

- Table 5 U.S. infectious respiratory disease diagnostics market by, sample type, 2018 - 2030 (USD Million)

- Table 6 U.S. infectious respiratory disease diagnostics market by, technology, 2018 - 2030 (USD Million)

- Table 7 U.S. infectious respiratory disease diagnostics market by, application, 2018 - 2030 (USD Million)

- Table 8 U.S. infectious respiratory disease diagnostics market by, end-use, 2018 - 2030 (USD Million)

- Table 9 Participant's overview

- Table 10 Financial performance

- Table 11 Key companies undergoing expansions

- Table 12 Key companies undergoing acquisitions

- Table 13 Key companies undergoing collaborations

- Table 14 Key companies launching new products/services

- Table 15 Key companies undergoing partnerships

- Table 16 Key companies undertaking other strategies

List of Figures

- Fig. 1 U.S. Infectious Respiratory Disease Diagnostics market segmentation

- Fig. 2 Market research process

- Fig. 3 Information procurement

- Fig. 4 Primary research pattern

- Fig. 5 Market research approaches

- Fig. 6 Value-chain-based sizing & forecasting

- Fig. 7 QFD modeling for market share assessment

- Fig. 8 Market formulation & validation

- Fig. 9 Market snapshot

- Fig. 10 Segment snapshot (By product & sample type)

- Fig. 11 Segment snapshot (By technology type & end-use type)

- Fig. 12 Segment snapshot (By application)

- Fig. 13 Competitive landscape snapshot

- Fig. 14 Penetration and growth prospect mapping

- Fig. 15 U.S. infectious respiratory disease diagnostics market driver impact

- Fig. 16 Number of new tuberculosis cases from 2018-2021, in the U. S.

- Fig. 17 Incidence rate trend of tuberculosis from 2018-2021

- Fig. 18 U.S. infectious respiratory disease diagnostics market restraint impact

- Fig. 19 SWOT Analysis, By Factor (Political & Legal, Economic, and Technological)

- Fig. 20 Porter's Five Forces Analysis

- Fig. 21 U.S. healthcare reimbursement and financing structure

- Fig. 22 U.S. infectious respiratory disease diagnostics product type outlook: Key takeaways

- Fig. 23 Infectious respiratory disease diagnostics market: Product type movement analysis (USD Million)

- Fig. 24 Instruments market, 2018 - 2030 (USD Million)

- Fig. 25 Imaging tests market, 2018 - 2030 (USD Million)

- Fig. 26 Respiratory measurement devices market, 2018 - 2030 (USD Million)

- Fig. 27 Other instruments market, 2018 - 2030 (USD Million)

- Fig. 28 Consumables market, 2018 - 2030 (USD Million)

- Fig. 29 Services market, 2018 - 2030 (USD Million)

- Fig. 30 U.S. Infectious respiratory disease diagnostics Sample type outlook: Key takeaways

- Fig. 31 U.S. infectious respiratory disease diagnostics market: Sample type movement analysis (USD Million)

- Fig. 32 Saliva market, 2018 - 2030 (USD Million)

- Fig. 33 Nasopharyngeal swabs (NPS) market, 2018 - 2030 (USD Million)

- Fig. 34 Anterior Nasal Region market, 2018 - 2030 (USD Million)

- Fig. 35 Blood market, 2018 - 2030 (USD Million)

- Fig. 36 Others market, 2018 - 2030 (USD Million)

- Fig. 37 U.S. infectious respiratory disease diagnostics technology outlook: Key takeaways

- Fig. 38 U.S. infectious respiratory disease diagnostics market: Technology movement analysis (USD Million)

- Fig. 39 Immunoassay market, 2018 - 2030 (USD Million)

- Fig. 40 Molecular diagnostics market, 2018 - 2030 (USD Million)

- Fig. 41 Microbiology market, 2018 - 2030 (USD Million)

- Fig. 42 Other technologies market, 2018 - 2030 (USD Million)

- Fig. 43 U.S. infectious respiratory disease diagnostics application outlook: Key takeaways

- Fig. 44 U.S. infectious respiratory disease diagnostics application outlook: Key takeaways (Volume 000)

- Fig. 45 U.S. infectious respiratory disease diagnostics market: Application movement analysis (USD Million)

- Fig. 46 U.S. infectious respiratory disease diagnostics market: Application movement analysis (Volume, '000s)

- Fig. 47 COVID-19 market, 2018 - 2030 (USD Million)

- Fig. 48 COVID-19 market, 2018 - 2030 (Volume '000s)

- Fig. 49 Influenza market, 2018 - 2030 (USD Million)

- Fig. 50 Influenza market, 2018 - 2030 (Volume '000s)

- Fig. 51 Respiratory syncytial virus market, 2018 - 2030 (USD Million)

- Fig. 52 Respiratory syncytial virus market, 2018 - 2030 (Volume '000s)

- Fig. 53 Tuberculosis market, 2018 - 2030 (USD Million)

- Fig. 54 Tuberculosis market, 2018 - 2030 (Volume '000s)

- Fig. 55 Streptococcus testing market, 2018 - 2030 (USD Million)

- Fig. 56 Streptococcus testing market, 2018 - 2030 (Volume '000s)

- Fig. 57 Other respiratory disease testing market, 2018 - 2030 (USD Million)

- Fig. 58 Other respiratory disease testing market, 2018 - 2030 (Volume '000s)

- Fig. 59 U.S. Infectious respiratory disease diagnostics end-use outlook: Key takeaways

- Fig. 60 U.S. infectious respiratory disease diagnostics market: End-use movement analysis (USD Million)

- Fig. 61 Hospitals market, 2018 - 2030 (USD Million)

- Fig. 62 Diagnostic laboratories market, 2018 - 2030 (USD Million)

- Fig. 63 Physician offices market, 2018 - 2030 (USD Million)

- Fig. 64 Other end-users' market, 2018 - 2030 (USD Million)

- Fig. 65 Market participant categorization

- Fig. 66 U.S. infectious respiratory disease diagnostics market share analysis, 2022

- Fig. 67 Strategic framework

- Fig. 68 Company market position analysis

- Fig. 69 Regional network map

U.S. Infectious Respiratory Disease Diagnostics Market Growth & Trends:

The U.S. infectious respiratory disease diagnostics market is expected to reach USD 9.20 billion by 2030, registering a CAGR of -10.1% from 2023 to 2030, according to a new report by Grand View Research, Inc. The market is anticipated to decline due to the decrease in COVID-19 testing. However, the U.S. infectious respiratory disease diagnostics market is expected to be driven by technological advancements, an increase in the prevalence of infectious respiratory diseases, and high R&D investments by the key players, government, & NGOs to develop novel & innovative products to address the increased market demand.

For instance, in January 2021, Biomedical Advanced Research and Development Authority (BARDA) funded USD 598,000 and USD 679,000 to QIAGEN LLC and DiaSorin Molecular LLC, respectively to enhance the development of COVID-19 test kits and instruments.

The introduction of innovative products used for disease diagnosis is anticipated to fuel the U.S. respiratory infectious disease market growth. In April 2020, Bio-Rad Laboratories, Inc. introduced immunoassay test kits for the diagnosis of COVID-19 patients. These were blood-based immunoassay test kits. In the initial preliminary performance of the immunoassay, the test kit demonstrated a specificity of more than 99.0% in more than 700 patients.

In addition, PerkinElmer, Inc. received approval from the U.S. FDA for the use of a T-cell select reagent test kit for the automation of its tuberculosis spot in September 2022. It uses a globally regulated enzyme-linked immunosorbent spot (ELISPOT) interferon-gamma release assay to detect latent tuberculosis infection. This ELISPOT test enables laboratories to offer accurate results to patients with latent tuberculosis. Thus, technological advancements in infectious respiratory disease diagnostics are fueling the market.

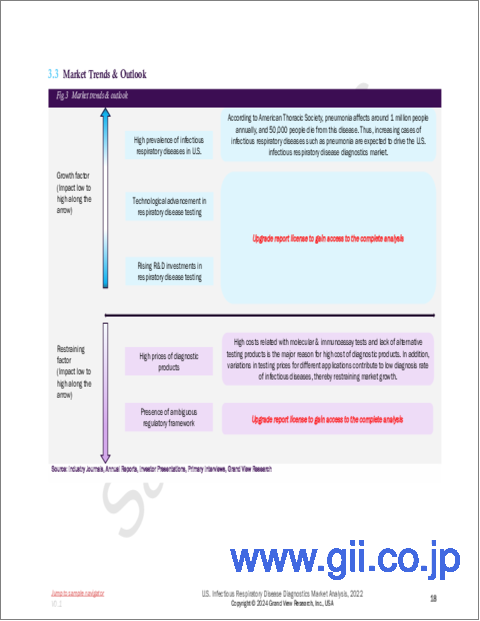

Moreover, molecular diagnostics play an important role in infectious disease testing by offering quick & effective results. According to the Centers for Disease Prevalence and Prevention (CDC), the estimated incidence rate of tuberculosis was 2.4 cases per 100,000 populations as of 2021. Similarly, according to the American Thoracic Society, pneumonia affects around 1.0 million people annually, and 50,000 die from this disease. Thus, the increasing incidence of respiratory infections is expected to drive the U.S. infectious respiratory disease diagnostics market during the study period.

On the other hand, the presence of ambiguous regulatory frameworks and high prices of diagnostics products may hamper the U.S. infectious respiratory disease diagnostics market during the study period. High costs related to molecular & immunoassay tests and lack of alternative testing products are the other major reasons for increased prices of infectious respiratory disease diagnostic products in the U.S.

However, healthcare authorities have taken steps to reduce the burden of high costs on manufacturers. EUA received from the U.S. FDA for COVID-19 tests is expected to minimize development costs and accelerate the process to increase the availability at more testing sites. Hence, a decrease in development costs is anticipated to increase the affordability of tests for healthcare providers and patients.

U.S. Infectious Respiratory Disease Diagnostics Market Report Highlights:

- The consumables segment dominated the infectious respiratory illness diagnostics market in 2022 with a revenue share of around 65.78%, which can be attributed to high usage rates. An increase in R&D for assays and testing kits, coupled with a rise in demand for the point-of-care in addition to the counter & self-test products is expected to drive the segment growth

- Based on the sample type, the market was dominated by nasopharyngeal swabs with an estimated share of 60.61% in 2022, due to wide applications in conducting various tests such as rapid antigen detection tests, direct fluorescent antibody, and polymerase chain reaction coupled with increased demand

- In 2022, the molecular diagnostics segment dominated the infectious respiratory disease diagnostics market with a revenue share of 63.74%, due to the increased demand for RT-PCR tests used for the diagnosis of COVID-19, influenza, RSV, and others

- The COVID-19 segment dominated the U.S. infectious respiratory disease diagnostics market with a share of 91.65% in 2022, due to the high incidence, increased product approvals, and rise in R&D pertaining to innovative products. However, its share is expected to decline to 69.97% by 2030 due to the mass vaccination drives being conducted in the U.S., which, in turn, will reduce the rate of diseases

Table of Contents

Chapter 1 Research Methodology and Scope

- 1.1 Market Segmentation and Scope

- 1.1.1 Segment Scope

- 1.1.2 Estimates And Forecast Timeline

- 1.2 Research Methodology

- 1.3 Information Procurement

- 1.3.1 Purchased Database:

- 1.3.2 Gvr's Internal Database

- 1.3.3 Secondary Sources

- 1.3.4 Primary Research

- 1.3.5 Details Of Primary Research

- 1.4 Information Or Data Analysis

- 1.4.1 Data Analysis Models

- 1.5 Market Formulation & Validation

- 1.6 Model Details

- 1.6.1 Commodity Flow Analysis

- 1.6.1.1 Approach: Commodity Flow Approach

- 1.6.1 Commodity Flow Analysis

- 1.7 Research Assumptions

- 1.8 List Of Secondary Sources

- 1.9 List Of Abbreviations

- 1.10 Objectives

- 1.10.1 Objective 1

- 1.10.2 Objective 2

- 1.10.3 Objective 3

- 1.10.4 Objective 4

Chapter 2 Executive Summary

- 2.1 Market Snapshot

- 2.2 Segment Snapshot (1/3)

- 2.3 Segment Snapshot (2/3)

- 2.4 Segment Snapshot (3/3)

- 2.5 Competitive Landscape Snapshot

Chapter 3 U.S. Infectious Respiratory Disease Diagnostics Market Variables, Trends, And Scope

- 3.1 Parent Market Outlook

- 3.2 Penetration And Growth Prospect Mapping

- 3.3 Market Driver Analysis

- 3.3.1 High Prevalence Of Infectious Respiratory Diseases In U.S.

- 3.3.2 Technological Advancement In Respiratory Disease Testing

- 3.3.3 Rising R&D Investments In Respiratory Disease Testing

- 3.4 Market Restraint Analysis

- 3.4.1 High Prices Of Diagnostic Products

- 3.4.2 Presence Of Ambiguous Regulatory Framework

- 3.5 Swot Analysis, By Factor (Political & Legal, Economic, And Technological)

- 3.6 Industry Analysis - Porter's

- 3.6.1 Regulatory Framework

- 3.6.2 Reimbursement Scenario

Chapter 4 U.S. Infectious Respiratory Disease Diagnostics Market: Segment Analysis, By Product Type, 2018 - 2030 (USD Million)

- 4.1 Definitions And Scope

- 4.2 U.S. Infectious Respiratory Disease Diagnostics Market: Product Type Movement Analysis

- 4.3 Instruments

- 4.3.1 Instruments Market, 2018 - 2030 (USD Million)

- 4.3.2 Imaging Tests

- 4.3.2.1 Imaging Tests Market, 2018 - 2030 (USD Million)

- 4.3.3 Respiratory Measurement Devices

- 4.3.3.1 Respiratory Measurement Devices Market, 2018 - 2030 (USD Million)

- 4.3.4 Other Instruments

- 4.3.4.1 Other Instruments Market, 2018 - 2030 (USD Million)

- 4.4 Consumables

- 4.4.1 Consumables Market, 2018 - 2030 (USD Million)

- 4.5 Services

- 4.5.1 Services Market, 2018 - 2030 (USD Million)

Chapter 5 U.S. Infectious Respiratory Disease Diagnostics Market: Segment Analysis, By Sample Type, 2018 - 2030 (USD Million)

- 5.1 Definitions & Scope

- 5.2 U.S. Infectious Respiratory Disease Diagnostics Market: Sample Type Movement Analysis

- 5.3 Saliva

- 5.3.1 Saliva Market, 2018 - 2030 (USD Million)

- 5.4 Nasopharyngeal Swabs (Nps)

- 5.4.1 Nasopharyngeal Swabs (Nps) Market, 2018 - 2030 (USD Million)

- 5.5 Anterior Nasal Region

- 5.5.1 Anterior Nasal Region Market, 2018 - 2030 (USD Million)

- 5.6 Blood

- 5.6.1 Blood Market, 2018 - 2030 (USD Million)

- 5.7 Others

- 5.7.1 Others Market, 2018 - 2030 (USD Million)

Chapter 6 U.S. Infectious Respiratory Disease Diagnostics Market: Segment Analysis, By Technology, 2018 - 2030 (USD Million)

- 6.1 Definitions And Scope

- 6.2 U.S. Infectious Respiratory Disease Diagnostics Market: Technology Movement Analysis

- 6.3 Immunoassay

- 6.3.1 Immunoassay Market, 2018 - 2030 (USD Million)

- 6.4 Molecular Diagnostics

- 6.4.1 Molecular Diagnostics Market, 2018 - 2030 (USD Million)

- 6.5 Microbiology

- 6.5.1 Microbiology Market, 2018 - 2030 (USD Million)

- 6.6 Other Technologies

- 6.6.1 Other Technologies Market, 2018 - 2030 (USD Million)

Chapter 7 U.S. Infectious Respiratory Disease Diagnostics Market: Segment Analysis, By Application, 2018 - 2030 (USD Million) ('000s)

- 7.1 U.S. Infectious Respiratory Disease Diagnostics Market: Application Movement Analysis

- 7.2 Covid-19

- 7.2.1 Covid-19 Market, 2018 - 2030 (USD Million)

- 7.2.2 Covid-19 Market, 2018 - 2030 (Volume '000s)

- 7.3 Influenza

- 7.3.1 Influenza Market, 2018 - 2030 (USD Million)

- 7.3.2 Influenza Market, 2018 - 2030 (Volume '000s)

- 7.4 Respiratory Syncytial Virus

- 7.4.1 Respiratory Syncytial Virus Market, 2018 - 2030 (USD Million)

- 7.4.2 Respiratory Syncytial Virus Market, 2018 - 2030 (Volume '000s)

- 7.5 Tuberculosis

- 7.5.1 Tuberculosis Market, 2018 - 2030 (USD Million)

- 7.5.2 Tuberculosis Market, 2018 - 2030 (Volume '000s)

- 7.6 Streptococcus Testing

- 7.6.1 Streptococcus Testing Market, 2018 - 2030 (USD Million)

- 7.6.2 Streptococcus Testing Market, 2018 - 2030 (Volume '000s)

- 7.7 Other Respiratory Disease Testing

- 7.7.1 Other Respiratory Disease Testing Market, 2018 - 2030 (USD Million)

- 7.7.2 Other Respiratory Disease Testing Market, 2018 - 2030 (Volume '000s)

Chapter 8 U.S. Infectious Respiratory Disease Diagnostics Market: Segment Analysis, By End Use, 2018 - 2030 (USD Million)

- 8.1 U.S. Infectious Respiratory Disease Diagnostics Market: End-Use Movement Analysis

- 8.2 Hospitals

- 8.2.1 Hospitals Market, 2018 - 2030 (USD Million)

- 8.3 Diagnostic Laboratories

- 8.3.1 Diagnostic Laboratories Market, 2018 - 2030 (USD Million)

- 8.4 Physician Offices

- 8.4.1 Physician Offices Market, 2018 - 2030 (USD Million)

- 8.5 Other End Users

- 8.5.1 Other End-Users Market, 2018 - 2030 (USD Million)

Chapter 9 U.S. Infectious Respiratory Disease Diagnostics Market: Competitive Analysis

- 9.1 Participants' Overview

- 9.2 Financial Performance

- 9.3 Participant Categorization

- 9.3.1 Market Leaders

- 9.3.1.1 U.S. Infectious Respiratory Disease Diagnostics Market Share Analysis, 2022

- 9.3.2 Strategy Mapping

- 9.3.2.1 Expansion

- 9.3.2.2 Acquisition

- 9.3.2.3 Collaborations

- 9.3.2.4 Product/Service Launch

- 9.3.2.5 Partnerships

- 9.3.2.6 Others

- 9.3.3 Vendor Landscape

- 9.3.3.1 List Of Distributors And Channel Partners

- 9.3.3.2 Key Customers

- 9.3.1 Market Leaders

- 9.4 Competitive Dashboard Analysis

- 9.4.1 Private Companies

- 9.4.1.1 List of Emerging Companies/Technology Disruptors/ Innovators

- 9.4.1.2 Regional Network Map include:

- 9.4.1.2.1 Abbott

- 9.4.1.2.2 Koninklijke Philips N.V.

- 9.4.1.2.3 Siemens Healthcare GmbH

- 9.4.1.2.4 BIOMERIEUX

- 9.4.1.2.5 Danaher

- 9.4.1.2.6 QIAGEN

- 9.4.1.2.7 BD

- 9.4.1.2.8 F. Hoffmann-La Roche Ltd

- 9.4.1.2.9 Quidel Corporation

- 9.4.1.2.10 Thermo Fisher Scientific, Inc.

- 9.4.1 Private Companies