|

|

市場調査レポート

商品コード

1579720

表面弾性波(SAW)デバイスの世界市場Surface Acoustic Wave (SAW) Devices |

||||||

|

|||||||

適宜更新あり

|

|||||||

| 表面弾性波(SAW)デバイスの世界市場 |

|

出版日: 2024年10月30日

発行: Market Glass, Inc. (Formerly Global Industry Analysts, Inc.)

ページ情報: 英文 226 Pages

納期: 即日から翌営業日

|

全表示

- 概要

- 目次

表面弾性波(SAW)デバイスの世界市場は2030年までに47億米ドルに達する見込み

2023年に32億米ドルと推定される表面弾性波(SAW)デバイスの世界市場は、分析期間2023-2030年にCAGR 5.7%で成長し、2030年には47億米ドルに達すると予測されます。本レポートで分析しているセグメントの1つであるSAWフィルタは、CAGR 5.8%を記録し、分析期間終了までに18億米ドルに達すると予測されています。SAW発振器セグメントの成長率は、分析期間でCAGR 5.0%と推定されます。

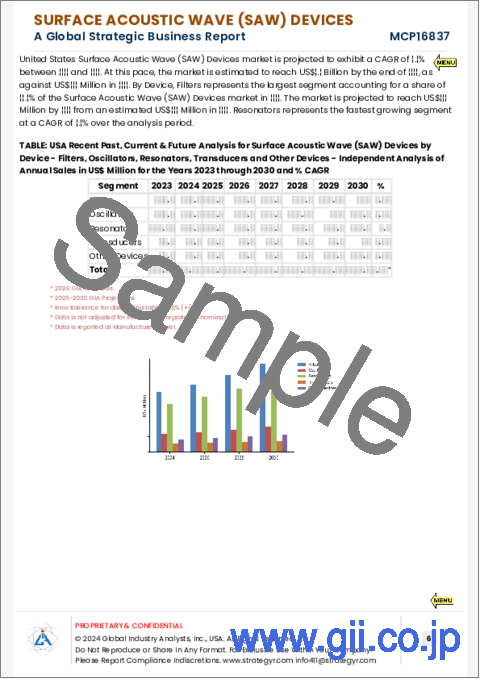

米国市場は8億7,670万米ドル、中国はCAGR 5.2%で成長予測

米国の表面弾性波(SAW)デバイス市場は、2023年に8億7,670万米ドルと推定されます。世界第2位の経済大国である中国は、2023年から2030年にかけてCAGR 5.2%で推移し、2030年には7億3,620万米ドルの市場規模に達すると予測されています。その他の注目すべき地域別市場としては、日本とカナダがあり、分析期間中のCAGRはそれぞれ5.4%と4.6%と予測されています。欧州では、ドイツがCAGR 4.6%で成長すると予測されています。

世界の表面弾性波(SAW)デバイス市場- 主要動向と促進要因まとめ

表面弾性波デバイスとは何か、なぜ現代のエレクトロニクスおよび通信システムに不可欠なのか?

表面弾性波(SAW)デバイスは、材料の表面に沿って音響波が伝播することを利用した高度な電子部品であり、一般的には圧電結晶を使用して電気信号を処理・制御します。これらのデバイスは、通信、家電、自動車、ヘルスケアなど様々な産業において、信号フィルタリング、周波数生成、センシングなどの用途に広く使用されています。SAWデバイスは、高い周波数精度、低消費電力、コンパクトなサイズで知られており、高周波信号処理や無線通信システムでの使用に最適です。SAWデバイスの主な種類には、SAWフィルター、共振器、発振器、センサーなどがあり、それぞれがそれぞれの用途における特定の性能要件を満たすように設計されています。

SAWデバイスの世界の普及の原動力となっているのは、コネクテッド化が進む世界で高性能な信号処理を実現する能力です。通信ミッションでは、SAWフィルターは携帯電話、基地局、衛星通信システムで幅広く使用され、不要な周波数をフィルタリングしてクリアな信号伝送を実現しています。小型で高精度なため、スマートフォンやIoT機器など、小型で高周波数の機器には欠かせない部品となっています。さらに、SAWセンサーは、圧力、温度、ひずみの変化を検出するために自動車や産業用アプリケーションで利用され、厳しい環境下で正確な測定を提供しています。高周波電子機器、ワイヤレス接続、高度なセンシング技術への需要が高まる中、SAWデバイスの使用は複数の分野で拡大しており、世界のSAWデバイス市場の成長を牽引しています。

技術の進歩は表面弾性波デバイスの開発と性能をどのように形成しているか?

技術の進歩は、表面弾性波(SAW)デバイスの開発、機能性、応用を大幅に向上させ、より汎用的、効率的で、現代の電子システムの進化する要求に対応できるものにしています。この分野で最もインパクトのある技術革新のひとつが、温度補償SAW(TC-SAW)とバルク弾性波(BAW)技術の開発です。従来のSAWデバイスは温度感受性を示すことが知られており、さまざまな環境条件下での周波数安定性や性能に影響を及ぼす可能性があります。TC-SAW技術は、温度変化の影響を打ち消す特定の材料の使用や設計などの温度補償技術を取り入れることで、この制限に対処しています。この技術革新により、SAWデバイスはより広い温度範囲で安定した性能を維持できるようになり、極端な温度が一般的な自動車、航空宇宙、産業用アプリケーションでの使用に適しています。同様に、従来のSAWデバイスよりも高い周波数で動作するBAW技術の出現により、より複雑な信号処理タスクを処理できるコンポーネントの開発が可能になり、5Gなどの高度通信システムの成長を支えています。

SAWデバイス市場を牽引するもう一つの重要な技術進歩は、SAWコンポーネントの小型化と集積化です。電子機器の小型化・高性能化の動向は、メーカー各社に小型化・高集積化したSAWデバイスの開発を促しています。例えば、最新のSAWフィルターは、より小さなフットプリントとより低い挿入損失で設計されており、スマートフォン、ウェアラブル機器、IoTモジュールなどの小型機器において、より効率的な信号処理を可能にしています。また、複数のSAWコンポーネントを1つのチップに集積することで、さまざまなフィルタリングやセンシングタスクを同時に実行できる多機能SAWデバイスの作成も可能になっています。このレベルの集積化は、性能を損なうことなくサイズと重量を最小化することが重要な、携帯通信機器や車載電子機器など、スペースに制約のあるアプリケーションにおいて特に価値があります。小型化と集積化の進展により、SAWデバイスは次世代電子システムの要件への適応性を高め、より幅広いアプリケーションへの採用を促進しています。

さらに、材料科学と製造技術の進歩により、SAWデバイスの性能と信頼性が向上しています。タンタル酸リチウム(LiTaO3)やニオブ酸リチウム(LiNbO3)などの新しい圧電材料の使用により、SAWデバイスの電気機械結合効率が向上し、信号トランスミッションの改善とエネルギー損失の低減が実現しています。これらの材料は音響特性に優れているため、より高い周波数で動作し、過酷な環境条件に耐えるSAWデバイスの開発が可能になります。さらに、リソグラフィと成膜プロセスの改善により、より微細なパターンと複雑な形状のSAWデバイスの製造が可能になり、その精度と機能が向上しています。ウエハーレベル・パッケージング(WLP)などの先進パッケージング技術の使用により、SAWデバイスの耐久性と耐環境性がさらに向上し、車載用センシングや産業用モニタリングなどの要求の厳しいアプリケーションでの使用に適しています。このような材料や製造の進歩は、現代の電子機器や通信システムの厳しい要件を満たすことができる高性能SAWデバイスの開発を支え、市場の成長を促進しています。

さまざまな産業や地域で表面弾性波デバイスの採用を促進している要因とは?

表面弾性波(SAW)デバイスの採用は、ワイヤレス通信システムの需要増加、自動車や産業用アプリケーションにおける精密センシングのニーズの高まり、民生用電子機器における小型化の動向など、いくつかの重要な要因によって推進されています。主な要因のひとつは、特に通信やネットワーク分野における無線通信システムの需要増です。SAWフィルターは、不要な周波数をフィルタリングし、干渉を防ぐことで、クリアで信頼性の高い信号トランスミッションを可能にする上で重要な役割を果たしています。5Gネットワークの急速な展開とIoTデバイスの普及に伴い、複数の通信帯域をサポートし、高いデータレートに対応できる高周波かつ低損失のSAWフィルターへのニーズが高まっています。基地局、モバイル機器、無線インフラにおけるSAWデバイスの使用は、最新の通信システムに不可欠な要素として、これらのコンポーネントの採用を後押ししています。この動向は、5GインフラやIoTエコシステムへの投資が高性能SAWデバイスの需要を促進しているアジア太平洋や北米などの地域で特に顕著です。

SAWデバイスの採用を促進するもう1つの重要な要因は、自動車や産業用アプリケーションで精密センシングのニーズが高まっていることです。SAWセンサーは、圧力、温度、トルク、ひずみなどの物理パラメータの測定に広く使用されており、プロセス制御や安全監視に正確なリアルタイムデータを提供しています。自動車業界では、SAWセンサーは、信頼性と精度が重要なタイヤ空気圧監視システム(TPMS)、エンジン制御、シャシ安定性システムなどのアプリケーションで使用されています。SAWセンサーは外部電源なしでワイヤレスで動作するため、過酷な環境やアクセスが困難な場所での使用に最適です。同様に、産業用アプリケーションでは、SAWセンサーは状態監視、構造健全性評価、プロセス最適化に使用され、産業界の業務効率向上とダウンタイム削減に貢献しています。これらの分野でSAWセンサーの採用が拡大していることは、耐久性、精度、統合の容易さを提供する高度なセンシング・ソリューションを産業界が求めていることから、SAWデバイス市場の拡大を支えています。

さらに、民生用電子機器の小型化動向の高まりが、さまざまな地域でSAWデバイスの採用に影響を与えています。スマートフォン、ウェアラブル、スマートホーム製品などの電子機器が小型化し、機能が豊富になるにつれて、限られたスペースで高性能を発揮できる小型部品が求められています。小型で高い周波数処理能力を持つSAWデバイスは、小型の電子機器設計に組み込むのに適しています。SAWフィルターやレゾネーターは、複数の通信帯域、GPS機能、スマートフォンやウェアラブル端末の無線接続をサポートするRFフロントエンド・モジュールに使用されています。民生用電子機器の製造が集中するアジア太平洋地域などでは、小型で多機能な電子機器への需要が高まっており、SAWデバイスの採用が進んでいます。メーカー各社は、小型化と消費電力の削減を図りながら、製品の性能と機能の向上を目指しており、この動向は今後も続くと予想されます。

表面弾性波デバイスの世界市場成長の原動力は?

世界の表面弾性波(SAW)デバイス市場の成長は、通信・ネットワークインフラへの投資の増加、自動車の安全性とコネクティビティへの注目の高まり、ヘルスケアや環境モニタリングアプリケーションにおけるSAWデバイスの採用増加など、いくつかの要因によって牽引されています。主な成長要因の1つは、特に5Gの展開とIoTの拡大に伴う通信・ネットワークインフラへの投資の増加です。5Gネットワークが世界的に展開されるにつれて、複数の帯域をサポートし、5G通信に関連する高いデータレートを処理できる高周波SAWフィルターと共振器のニーズが高まっています。SAWデバイスは、信頼性の高い無線接続と信号処理機能を提供するため、IoTモジュールやスマートデバイスにも使用されています。5Gインフラの拡大とIoTデバイスの普及は、SAWデバイスに対する大きな需要を生み出し、先進地域と新興国市場の両方で市場の成長を促進しています。

市場成長のもう一つの大きな促進要因は、自動車の安全性とコネクティビティへの注目が高まっていることです。自動車業界は、ADAS(先進運転支援システム)、V2X(Vehicle-to-Everything)通信、自律走行技術の採用により変革期を迎えています。SAWセンサーは、TPMS、エンジン管理、シャシー制御など、正確な測定とリアルタイムデータが車両性能と安全性に不可欠な重要な安全アプリケーションで使用されています。SAWセンサーの自動車エレクトロニクスへの統合は、コネクテッドカーや自律走行車の開発をサポートし、安全性、効率性、運転体験を向上させています。自動車の安全規制が厳しい欧州や北米などの地域では、こうした技術の普及が進んでいるため、自動車分野でのSAWデバイスの需要が高まり、市場の成長に寄与しています。

さらに、ヘルスケアや環境モニタリング用途でのSAWデバイスの採用が増加していることも、市場の成長を支えています。ヘルスケアでは、呼吸数や心拍数などのバイタルサインをモニタリングする医療機器や、高精度と高感度が求められる診断機器にSAWセンサーが採用されています。SAWセンサーは非侵襲的でワイヤレスであるため、ウェアラブル健康モニターや遠隔患者モニタリングシステムでの使用に最適です。同様に、環境モニタリングでは、SAWセンサーは空気の質、湿度、化学組成の変化を検出するために使用され、汚染防止や環境保護のためのリアルタイムデータを提供しています。健康と環境の持続可能性への関心の高まりが、信頼性が高く正確なセンシング機能を提供するSAWデバイスの需要を促進しています。この動向は、環境規制やヘルスケアへの取り組みが高度なセンシング技術の採用を後押ししているアジア太平洋や欧州などの地域で特に顕著です。

さらに、製品のイノベーションと付加価値の高いSAWデバイスの開拓に注力する傾向が強まっていることも、市場の成長に影響を与えています。メーカー各社は研究開発(R&D)に投資し、より高い周波数ハンドリング、低消費電力、熱安定性の向上などの性能向上を実現するSAWデバイスを開発しています。無線通信モジュールを内蔵したSAWデバイスの開発により、無線でデータを送信できるスマートセンサーが実現し、産業用モノのインターネット(IIoT)やスマート製造構想の成長を支えています。化学物質の検出やバイオセンシングなど、ニッチな用途向けの新しいSAWセンサーのイントロダクションは、SAWデバイスの応用範囲を拡大し、市場に新たな成長機会をもたらしています。これらの要因が世界のエレクトロニクスとセンシングの状況を形成し続ける中、表面弾性波デバイス市場は、通信とネットワーキング・インフラへの投資の増加、自動車の安全性とコネクティビティへの注目の高まり、ヘルスケアと環境モニタリング・アプリケーションにおけるSAWデバイスの採用増加によって、力強い成長が見込まれます。

調査対象企業の例(全48件)

- API Technologies Corporation

- AVX Corporation

- Boston Piezo-Optics Inc.

- ITF Co., Ltd.

- Kyocera Corporation

- Murata Manufacturing Co., Ltd.

- Oscilent Corporation

- Skyworks Solutions, Inc.

- Tai-Saw Technology Co., Ltd.

- Taiyo Yuden Co., Ltd.

目次

第1章 調査手法

第2章 エグゼクティブサマリー

- 市場概要

- 主要企業

- 市場動向と促進要因

- 世界市場の見通し

第3章 市場分析

- 米国

- カナダ

- 日本

- 中国

- 欧州

- フランス

- ドイツ

- イタリア

- 英国

- その他欧州

- アジア太平洋

- その他の地域

第4章 競合

Global Surface Acoustic Wave (SAW) Devices Market to Reach US$4.7 Billion by 2030

The global market for Surface Acoustic Wave (SAW) Devices estimated at US$3.2 Billion in the year 2023, is expected to reach US$4.7 Billion by 2030, growing at a CAGR of 5.7% over the analysis period 2023-2030. SAW Filters, one of the segments analyzed in the report, is expected to record a 5.8% CAGR and reach US$1.8 Billion by the end of the analysis period. Growth in the SAW Oscillators segment is estimated at 5.0% CAGR over the analysis period.

The U.S. Market is Estimated at US$876.7 Million While China is Forecast to Grow at 5.2% CAGR

The Surface Acoustic Wave (SAW) Devices market in the U.S. is estimated at US$876.7 Million in the year 2023. China, the world's second largest economy, is forecast to reach a projected market size of US$736.2 Million by the year 2030 trailing a CAGR of 5.2% over the analysis period 2023-2030. Among the other noteworthy geographic markets are Japan and Canada, each forecast to grow at a CAGR of 5.4% and 4.6% respectively over the analysis period. Within Europe, Germany is forecast to grow at approximately 4.6% CAGR.

Global Surface Acoustic Wave (SAW) Devices Market - Key Trends & Drivers Summarized

What Are Surface Acoustic Wave Devices and Why Are They Essential in Modern Electronics and Communication Systems?

Surface Acoustic Wave (SAW) devices are sophisticated electronic components that utilize the propagation of acoustic waves along the surface of a material, typically a piezoelectric crystal, to process and control electrical signals. These devices are widely used for signal filtering, frequency generation, and sensing applications in various industries, including telecommunications, consumer electronics, automotive, and healthcare. SAW devices are known for their high frequency precision, low power consumption, and compact size, making them ideal for use in high-frequency signal processing and wireless communication systems. The primary types of SAW devices include SAW filters, resonators, oscillators, and sensors, each designed to meet specific performance requirements in their respective applications.

The global adoption of SAW devices is driven by their ability to deliver high-performance signal processing in an increasingly connected world. In telecommunications, SAW filters are used extensively in mobile phones, base stations, and satellite communication systems to filter out unwanted frequencies and ensure clear signal transmission. Their small size and high precision make them indispensable components in compact, high-frequency devices such as smartphones and IoT devices. Additionally, SAW sensors are utilized in automotive and industrial applications for detecting changes in pressure, temperature, and strain, providing accurate measurements in challenging environments. With the growing demand for high-frequency electronic devices, wireless connectivity, and advanced sensing technologies, the use of SAW devices is expanding across multiple sectors, driving the growth of the global SAW devices market.

How Are Technological Advancements Shaping the Development and Performance of Surface Acoustic Wave Devices?

Technological advancements are significantly enhancing the development, functionality, and application of Surface Acoustic Wave (SAW) devices, making them more versatile, efficient, and capable of meeting the evolving demands of modern electronic systems. One of the most impactful innovations in this field is the development of temperature-compensated SAW (TC-SAW) and bulk acoustic wave (BAW) technologies. Traditional SAW devices are known to exhibit temperature sensitivity, which can affect their frequency stability and performance in varying environmental conditions. TC-SAW technology addresses this limitation by incorporating temperature compensation techniques, such as the use of specific materials or designs that counteract the effects of temperature variations. This innovation allows SAW devices to maintain stable performance over a wider temperature range, making them suitable for use in automotive, aerospace, and industrial applications where extreme temperatures are common. Similarly, the emergence of BAW technology, which operates at higher frequencies than traditional SAW devices, is enabling the development of components that can handle more complex signal processing tasks, supporting the growth of advanced communication systems such as 5G.

Another key technological advancement driving the SAW devices market is the miniaturization and integration of SAW components. The trend towards smaller, more powerful electronic devices is pushing manufacturers to develop SAW devices with reduced size and higher levels of integration. Modern SAW filters, for example, are being designed with smaller footprints and lower insertion losses, allowing for more efficient signal processing in compact devices such as smartphones, wearable devices, and IoT modules. The integration of multiple SAW components onto a single chip is also gaining traction, enabling the creation of multi-functional SAW devices that can perform various filtering and sensing tasks simultaneously. This level of integration is particularly valuable in space-constrained applications, such as portable communication devices and automotive electronics, where minimizing size and weight without compromising performance is crucial. The advancements in miniaturization and integration are making SAW devices more adaptable to the requirements of next-generation electronic systems, driving their adoption in a broader range of applications.

Furthermore, advancements in material science and fabrication techniques are improving the performance and reliability of SAW devices. The use of new piezoelectric materials, such as lithium tantalate (LiTaO3) and lithium niobate (LiNbO3), is enhancing the electromechanical coupling efficiency of SAW devices, resulting in better signal transmission and lower energy losses. These materials offer superior acoustic properties, enabling the development of SAW devices that can operate at higher frequencies and withstand harsh environmental conditions. Additionally, improvements in lithography and deposition processes are enabling the fabrication of SAW devices with finer patterns and more complex geometries, enhancing their precision and functionality. The use of advanced packaging technologies, such as wafer-level packaging (WLP), is further increasing the durability and environmental resistance of SAW devices, making them suitable for use in demanding applications such as automotive sensing and industrial monitoring. These advancements in materials and fabrication are supporting the development of high-performance SAW devices that can meet the stringent requirements of modern electronics and communication systems, driving the growth of the market.

What Factors Are Driving the Adoption of Surface Acoustic Wave Devices Across Various Industries and Regions?

The adoption of Surface Acoustic Wave (SAW) devices is being driven by several key factors, including the increasing demand for wireless communication systems, the growing need for precision sensing in automotive and industrial applications, and the rising trend of miniaturization in consumer electronics. One of the primary drivers is the increasing demand for wireless communication systems, particularly in the telecommunications and networking sectors. SAW filters play a crucial role in enabling clear and reliable signal transmission by filtering out unwanted frequencies and preventing interference. With the rapid deployment of 5G networks and the proliferation of IoT devices, there is a growing need for high-frequency and low-loss SAW filters that can support multiple communication bands and handle high data rates. The use of SAW devices in base stations, mobile devices, and wireless infrastructure is supporting the adoption of these components as essential elements in modern communication systems. This trend is particularly strong in regions such as Asia-Pacific and North America, where investments in 5G infrastructure and IoT ecosystems are driving demand for high-performance SAW devices.

Another significant factor driving the adoption of SAW devices is the growing need for precision sensing in automotive and industrial applications. SAW sensors are widely used to measure physical parameters such as pressure, temperature, torque, and strain, providing accurate and real-time data for process control and safety monitoring. In the automotive industry, SAW sensors are used in applications such as tire pressure monitoring systems (TPMS), engine control, and chassis stability systems, where reliability and precision are critical. The ability of SAW sensors to operate wirelessly and without external power sources makes them ideal for use in harsh environments and difficult-to-access locations. Similarly, in industrial applications, SAW sensors are used for condition monitoring, structural health assessment, and process optimization, helping industries enhance operational efficiency and reduce downtime. The growing adoption of SAW sensors in these sectors is supporting the expansion of the SAW devices market as industries seek advanced sensing solutions that offer durability, accuracy, and ease of integration.

Moreover, the rising trend of miniaturization in consumer electronics is influencing the adoption of SAW devices across various regions. As electronic devices such as smartphones, wearables, and smart home products become smaller and more feature-rich, there is a need for compact components that can deliver high performance in limited space. SAW devices, with their small size and high frequency handling capabilities, are well-suited for integration into compact electronic designs. SAW filters and resonators are being used in RF front-end modules to support multiple communication bands, GPS functionality, and wireless connectivity in smartphones and wearables. The increasing demand for miniaturized and multi-functional electronic devices in regions such as Asia-Pacific, where consumer electronics manufacturing is concentrated, is driving the adoption of SAW devices. This trend is expected to continue as manufacturers seek to enhance the performance and functionality of their products while reducing size and power consumption.

What Is Driving the Growth of the Global Surface Acoustic Wave Devices Market?

The growth in the global Surface Acoustic Wave (SAW) Devices market is driven by several factors, including rising investments in telecommunications and networking infrastructure, the growing focus on automotive safety and connectivity, and the increasing adoption of SAW devices in healthcare and environmental monitoring applications. One of the primary growth drivers is the rising investment in telecommunications and networking infrastructure, particularly in the context of 5G deployment and IoT expansion. As 5G networks are rolled out globally, there is a growing need for high-frequency SAW filters and resonators that can support multiple bands and handle the high data rates associated with 5G communication. SAW devices are also being used in IoT modules and smart devices to provide reliable wireless connectivity and signal processing capabilities. The expansion of 5G infrastructure and the proliferation of IoT devices are creating significant demand for SAW devices, driving the growth of the market in both developed and emerging regions.

Another significant driver of market growth is the growing focus on automotive safety and connectivity. The automotive industry is undergoing a transformation with the adoption of advanced driver assistance systems (ADAS), vehicle-to-everything (V2X) communication, and autonomous driving technologies. SAW sensors are being used in critical safety applications such as TPMS, engine management, and chassis control, where accurate measurement and real-time data are essential for vehicle performance and safety. The integration of SAW sensors into automotive electronics is supporting the development of connected and autonomous vehicles, enhancing safety, efficiency, and driving experience. The increasing penetration of these technologies in regions such as Europe and North America, where automotive safety regulations are stringent, is driving demand for SAW devices in the automotive sector, contributing to the growth of the market.

Moreover, the increasing adoption of SAW devices in healthcare and environmental monitoring applications is supporting the growth of the market. In healthcare, SAW sensors are being used in medical devices for monitoring vital signs, such as respiratory rate and cardiac activity, as well as for diagnostic equipment that requires high precision and sensitivity. The non-invasive and wireless nature of SAW sensors makes them ideal for use in wearable health monitors and remote patient monitoring systems. Similarly, in environmental monitoring, SAW sensors are used to detect changes in air quality, humidity, and chemical composition, providing real-time data for pollution control and environmental protection. The growing focus on health and environmental sustainability is driving demand for SAW devices that offer reliable and accurate sensing capabilities. This trend is particularly strong in regions such as Asia-Pacific and Europe, where environmental regulations and healthcare initiatives are supporting the adoption of advanced sensing technologies.

Furthermore, the increasing focus on product innovation and the development of value-added SAW devices is influencing the growth of the market. Manufacturers are investing in research and development (R&D) to create SAW devices that offer enhanced performance, such as higher frequency handling, lower power consumption, and improved thermal stability. The development of SAW devices with integrated wireless communication modules is enabling the creation of smart sensors that can transmit data wirelessly, supporting the growth of the Industrial Internet of Things (IIoT) and smart manufacturing initiatives. The introduction of novel SAW sensors for niche applications, such as chemical detection and biosensing, is expanding the application scope of SAW devices, providing new growth opportunities for the market. As these factors continue to shape the global electronics and sensing landscape, the Surface Acoustic Wave Devices market is expected to experience robust growth, driven by rising investments in telecommunications and networking infrastructure, the growing focus on automotive safety and connectivity, and the increasing adoption of SAW devices in healthcare and environmental monitoring applications.

Select Competitors (Total 48 Featured) -

- API Technologies Corporation

- AVX Corporation

- Boston Piezo-Optics Inc.

- ITF Co., Ltd.

- Kyocera Corporation

- Murata Manufacturing Co., Ltd.

- Oscilent Corporation

- Skyworks Solutions, Inc.

- Tai-Saw Technology Co., Ltd.

- Taiyo Yuden Co., Ltd.

TABLE OF CONTENTS

I. METHODOLOGY

II. EXECUTIVE SUMMARY

- 1. MARKET OVERVIEW

- Influencer Market Insights

- World Market Trajectories

- Surface Acoustic Wave (SAW) Devices - Global Key Competitors Percentage Market Share in 2024 (E)

- Competitive Market Presence - Strong/Active/Niche/Trivial for Players Worldwide in 2024 (E)

- 2. FOCUS ON SELECT PLAYERS

- 3. MARKET TRENDS & DRIVERS

- Increased Adoption of SAW Devices in Consumer Electronics Fuels Market Growth

- Surge in Use of SAW Filters in Mobile Communication and 5G Networks Expands Addressable Market

- Growing Adoption of SAW Devices in Automotive and Transportation Applications Strengthens Business Case for Market Growth

- Expansion of Internet of Things (IoT) Networks Sets the Stage for Market Growth

- Rising Utilization of SAW Sensors in Industrial and Environmental Monitoring Fuels Market Demand

- Surge in Demand for SAW Devices in RF and Microwave Applications Bodes Well for Market Expansion

- Increased Use of SAW Devices in Defense and Aerospace Applications Expands Market Opportunities

- Rising Adoption of SAW Devices in Healthcare and Medical Diagnostics Strengthens Market Opportunities

- Growing Use of SAW Filters in Wireless Communication Equipment Fuels Market Demand

- Surge in Demand for SAW Devices in Radar and Satellite Communication Expands Market Opportunities

- Rising Use of SAW Devices in Smart Home and Connected Devices Fuels Market Demand

- 4. GLOBAL MARKET PERSPECTIVE

- TABLE 1: World Surface Acoustic Wave (SAW) Devices Market Analysis of Annual Sales in US$ Million for Years 2014 through 2030

- TABLE 2: World Recent Past, Current & Future Analysis for Surface Acoustic Wave (SAW) Devices by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2023 through 2030 and % CAGR

- TABLE 3: World Historic Review for Surface Acoustic Wave (SAW) Devices by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 4: World 16-Year Perspective for Surface Acoustic Wave (SAW) Devices by Geographic Region - Percentage Breakdown of Value Sales for USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets for Years 2014, 2024 & 2030

- TABLE 5: World Recent Past, Current & Future Analysis for Filters by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2023 through 2030 and % CAGR

- TABLE 6: World Historic Review for Filters by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 7: World 16-Year Perspective for Filters by Geographic Region - Percentage Breakdown of Value Sales for USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World for Years 2014, 2024 & 2030

- TABLE 8: World Recent Past, Current & Future Analysis for Oscillators by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2023 through 2030 and % CAGR

- TABLE 9: World Historic Review for Oscillators by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 10: World 16-Year Perspective for Oscillators by Geographic Region - Percentage Breakdown of Value Sales for USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World for Years 2014, 2024 & 2030

- TABLE 11: World Recent Past, Current & Future Analysis for Resonators by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2023 through 2030 and % CAGR

- TABLE 12: World Historic Review for Resonators by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 13: World 16-Year Perspective for Resonators by Geographic Region - Percentage Breakdown of Value Sales for USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World for Years 2014, 2024 & 2030

- TABLE 14: World Recent Past, Current & Future Analysis for Transducers by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2023 through 2030 and % CAGR

- TABLE 15: World Historic Review for Transducers by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 16: World 16-Year Perspective for Transducers by Geographic Region - Percentage Breakdown of Value Sales for USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World for Years 2014, 2024 & 2030

- TABLE 17: World Recent Past, Current & Future Analysis for Other Devices by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2023 through 2030 and % CAGR

- TABLE 18: World Historic Review for Other Devices by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 19: World 16-Year Perspective for Other Devices by Geographic Region - Percentage Breakdown of Value Sales for USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World for Years 2014, 2024 & 2030

- TABLE 20: World Recent Past, Current & Future Analysis for Aerospace & Defense by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2023 through 2030 and % CAGR

- TABLE 21: World Historic Review for Aerospace & Defense by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 22: World 16-Year Perspective for Aerospace & Defense by Geographic Region - Percentage Breakdown of Value Sales for USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World for Years 2014, 2024 & 2030

- TABLE 23: World Recent Past, Current & Future Analysis for Telecommunication by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2023 through 2030 and % CAGR

- TABLE 24: World Historic Review for Telecommunication by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 25: World 16-Year Perspective for Telecommunication by Geographic Region - Percentage Breakdown of Value Sales for USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World for Years 2014, 2024 & 2030

- TABLE 26: World Recent Past, Current & Future Analysis for Environmental & Industrial by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2023 through 2030 and % CAGR

- TABLE 27: World Historic Review for Environmental & Industrial by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 28: World 16-Year Perspective for Environmental & Industrial by Geographic Region - Percentage Breakdown of Value Sales for USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World for Years 2014, 2024 & 2030

- TABLE 29: World Recent Past, Current & Future Analysis for Automotive by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2023 through 2030 and % CAGR

- TABLE 30: World Historic Review for Automotive by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 31: World 16-Year Perspective for Automotive by Geographic Region - Percentage Breakdown of Value Sales for USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World for Years 2014, 2024 & 2030

- TABLE 32: World Recent Past, Current & Future Analysis for Consumer Electronics by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2023 through 2030 and % CAGR

- TABLE 33: World Historic Review for Consumer Electronics by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 34: World 16-Year Perspective for Consumer Electronics by Geographic Region - Percentage Breakdown of Value Sales for USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World for Years 2014, 2024 & 2030

- TABLE 35: World Recent Past, Current & Future Analysis for Other End-Use Industries by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2023 through 2030 and % CAGR

- TABLE 36: World Historic Review for Other End-Use Industries by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 37: World 16-Year Perspective for Other End-Use Industries by Geographic Region - Percentage Breakdown of Value Sales for USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World for Years 2014, 2024 & 2030

III. MARKET ANALYSIS

- UNITED STATES

- Surface Acoustic Wave (SAW) Devices Market Presence - Strong/Active/Niche/Trivial - Key Competitors in the United States for 2024 (E)

- TABLE 38: USA Recent Past, Current & Future Analysis for Surface Acoustic Wave (SAW) Devices by Device - Filters, Oscillators, Resonators, Transducers and Other Devices - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 39: USA Historic Review for Surface Acoustic Wave (SAW) Devices by Device - Filters, Oscillators, Resonators, Transducers and Other Devices Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 40: USA 16-Year Perspective for Surface Acoustic Wave (SAW) Devices by Device - Percentage Breakdown of Value Sales for Filters, Oscillators, Resonators, Transducers and Other Devices for the Years 2014, 2024 & 2030

- TABLE 41: USA Recent Past, Current & Future Analysis for Surface Acoustic Wave (SAW) Devices by End-Use Industry - Aerospace & Defense, Telecommunication, Environmental & Industrial, Automotive, Consumer Electronics and Other End-Use Industries - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 42: USA Historic Review for Surface Acoustic Wave (SAW) Devices by End-Use Industry - Aerospace & Defense, Telecommunication, Environmental & Industrial, Automotive, Consumer Electronics and Other End-Use Industries Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 43: USA 16-Year Perspective for Surface Acoustic Wave (SAW) Devices by End-Use Industry - Percentage Breakdown of Value Sales for Aerospace & Defense, Telecommunication, Environmental & Industrial, Automotive, Consumer Electronics and Other End-Use Industries for the Years 2014, 2024 & 2030

- CANADA

- TABLE 44: Canada Recent Past, Current & Future Analysis for Surface Acoustic Wave (SAW) Devices by Device - Filters, Oscillators, Resonators, Transducers and Other Devices - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 45: Canada Historic Review for Surface Acoustic Wave (SAW) Devices by Device - Filters, Oscillators, Resonators, Transducers and Other Devices Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 46: Canada 16-Year Perspective for Surface Acoustic Wave (SAW) Devices by Device - Percentage Breakdown of Value Sales for Filters, Oscillators, Resonators, Transducers and Other Devices for the Years 2014, 2024 & 2030

- TABLE 47: Canada Recent Past, Current & Future Analysis for Surface Acoustic Wave (SAW) Devices by End-Use Industry - Aerospace & Defense, Telecommunication, Environmental & Industrial, Automotive, Consumer Electronics and Other End-Use Industries - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 48: Canada Historic Review for Surface Acoustic Wave (SAW) Devices by End-Use Industry - Aerospace & Defense, Telecommunication, Environmental & Industrial, Automotive, Consumer Electronics and Other End-Use Industries Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 49: Canada 16-Year Perspective for Surface Acoustic Wave (SAW) Devices by End-Use Industry - Percentage Breakdown of Value Sales for Aerospace & Defense, Telecommunication, Environmental & Industrial, Automotive, Consumer Electronics and Other End-Use Industries for the Years 2014, 2024 & 2030

- JAPAN

- Surface Acoustic Wave (SAW) Devices Market Presence - Strong/Active/Niche/Trivial - Key Competitors in Japan for 2024 (E)

- TABLE 50: Japan Recent Past, Current & Future Analysis for Surface Acoustic Wave (SAW) Devices by Device - Filters, Oscillators, Resonators, Transducers and Other Devices - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 51: Japan Historic Review for Surface Acoustic Wave (SAW) Devices by Device - Filters, Oscillators, Resonators, Transducers and Other Devices Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 52: Japan 16-Year Perspective for Surface Acoustic Wave (SAW) Devices by Device - Percentage Breakdown of Value Sales for Filters, Oscillators, Resonators, Transducers and Other Devices for the Years 2014, 2024 & 2030

- TABLE 53: Japan Recent Past, Current & Future Analysis for Surface Acoustic Wave (SAW) Devices by End-Use Industry - Aerospace & Defense, Telecommunication, Environmental & Industrial, Automotive, Consumer Electronics and Other End-Use Industries - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 54: Japan Historic Review for Surface Acoustic Wave (SAW) Devices by End-Use Industry - Aerospace & Defense, Telecommunication, Environmental & Industrial, Automotive, Consumer Electronics and Other End-Use Industries Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 55: Japan 16-Year Perspective for Surface Acoustic Wave (SAW) Devices by End-Use Industry - Percentage Breakdown of Value Sales for Aerospace & Defense, Telecommunication, Environmental & Industrial, Automotive, Consumer Electronics and Other End-Use Industries for the Years 2014, 2024 & 2030

- CHINA

- Surface Acoustic Wave (SAW) Devices Market Presence - Strong/Active/Niche/Trivial - Key Competitors in China for 2024 (E)

- TABLE 56: China Recent Past, Current & Future Analysis for Surface Acoustic Wave (SAW) Devices by Device - Filters, Oscillators, Resonators, Transducers and Other Devices - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 57: China Historic Review for Surface Acoustic Wave (SAW) Devices by Device - Filters, Oscillators, Resonators, Transducers and Other Devices Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 58: China 16-Year Perspective for Surface Acoustic Wave (SAW) Devices by Device - Percentage Breakdown of Value Sales for Filters, Oscillators, Resonators, Transducers and Other Devices for the Years 2014, 2024 & 2030

- TABLE 59: China Recent Past, Current & Future Analysis for Surface Acoustic Wave (SAW) Devices by End-Use Industry - Aerospace & Defense, Telecommunication, Environmental & Industrial, Automotive, Consumer Electronics and Other End-Use Industries - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 60: China Historic Review for Surface Acoustic Wave (SAW) Devices by End-Use Industry - Aerospace & Defense, Telecommunication, Environmental & Industrial, Automotive, Consumer Electronics and Other End-Use Industries Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 61: China 16-Year Perspective for Surface Acoustic Wave (SAW) Devices by End-Use Industry - Percentage Breakdown of Value Sales for Aerospace & Defense, Telecommunication, Environmental & Industrial, Automotive, Consumer Electronics and Other End-Use Industries for the Years 2014, 2024 & 2030

- EUROPE

- Surface Acoustic Wave (SAW) Devices Market Presence - Strong/Active/Niche/Trivial - Key Competitors in Europe for 2024 (E)

- TABLE 62: Europe Recent Past, Current & Future Analysis for Surface Acoustic Wave (SAW) Devices by Geographic Region - France, Germany, Italy, UK and Rest of Europe Markets - Independent Analysis of Annual Sales in US$ Million for Years 2023 through 2030 and % CAGR

- TABLE 63: Europe Historic Review for Surface Acoustic Wave (SAW) Devices by Geographic Region - France, Germany, Italy, UK and Rest of Europe Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 64: Europe 16-Year Perspective for Surface Acoustic Wave (SAW) Devices by Geographic Region - Percentage Breakdown of Value Sales for France, Germany, Italy, UK and Rest of Europe Markets for Years 2014, 2024 & 2030

- TABLE 65: Europe Recent Past, Current & Future Analysis for Surface Acoustic Wave (SAW) Devices by Device - Filters, Oscillators, Resonators, Transducers and Other Devices - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 66: Europe Historic Review for Surface Acoustic Wave (SAW) Devices by Device - Filters, Oscillators, Resonators, Transducers and Other Devices Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 67: Europe 16-Year Perspective for Surface Acoustic Wave (SAW) Devices by Device - Percentage Breakdown of Value Sales for Filters, Oscillators, Resonators, Transducers and Other Devices for the Years 2014, 2024 & 2030

- TABLE 68: Europe Recent Past, Current & Future Analysis for Surface Acoustic Wave (SAW) Devices by End-Use Industry - Aerospace & Defense, Telecommunication, Environmental & Industrial, Automotive, Consumer Electronics and Other End-Use Industries - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 69: Europe Historic Review for Surface Acoustic Wave (SAW) Devices by End-Use Industry - Aerospace & Defense, Telecommunication, Environmental & Industrial, Automotive, Consumer Electronics and Other End-Use Industries Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 70: Europe 16-Year Perspective for Surface Acoustic Wave (SAW) Devices by End-Use Industry - Percentage Breakdown of Value Sales for Aerospace & Defense, Telecommunication, Environmental & Industrial, Automotive, Consumer Electronics and Other End-Use Industries for the Years 2014, 2024 & 2030

- FRANCE

- Surface Acoustic Wave (SAW) Devices Market Presence - Strong/Active/Niche/Trivial - Key Competitors in France for 2024 (E)

- TABLE 71: France Recent Past, Current & Future Analysis for Surface Acoustic Wave (SAW) Devices by Device - Filters, Oscillators, Resonators, Transducers and Other Devices - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 72: France Historic Review for Surface Acoustic Wave (SAW) Devices by Device - Filters, Oscillators, Resonators, Transducers and Other Devices Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 73: France 16-Year Perspective for Surface Acoustic Wave (SAW) Devices by Device - Percentage Breakdown of Value Sales for Filters, Oscillators, Resonators, Transducers and Other Devices for the Years 2014, 2024 & 2030

- TABLE 74: France Recent Past, Current & Future Analysis for Surface Acoustic Wave (SAW) Devices by End-Use Industry - Aerospace & Defense, Telecommunication, Environmental & Industrial, Automotive, Consumer Electronics and Other End-Use Industries - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 75: France Historic Review for Surface Acoustic Wave (SAW) Devices by End-Use Industry - Aerospace & Defense, Telecommunication, Environmental & Industrial, Automotive, Consumer Electronics and Other End-Use Industries Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 76: France 16-Year Perspective for Surface Acoustic Wave (SAW) Devices by End-Use Industry - Percentage Breakdown of Value Sales for Aerospace & Defense, Telecommunication, Environmental & Industrial, Automotive, Consumer Electronics and Other End-Use Industries for the Years 2014, 2024 & 2030

- GERMANY

- Surface Acoustic Wave (SAW) Devices Market Presence - Strong/Active/Niche/Trivial - Key Competitors in Germany for 2024 (E)

- TABLE 77: Germany Recent Past, Current & Future Analysis for Surface Acoustic Wave (SAW) Devices by Device - Filters, Oscillators, Resonators, Transducers and Other Devices - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 78: Germany Historic Review for Surface Acoustic Wave (SAW) Devices by Device - Filters, Oscillators, Resonators, Transducers and Other Devices Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 79: Germany 16-Year Perspective for Surface Acoustic Wave (SAW) Devices by Device - Percentage Breakdown of Value Sales for Filters, Oscillators, Resonators, Transducers and Other Devices for the Years 2014, 2024 & 2030

- TABLE 80: Germany Recent Past, Current & Future Analysis for Surface Acoustic Wave (SAW) Devices by End-Use Industry - Aerospace & Defense, Telecommunication, Environmental & Industrial, Automotive, Consumer Electronics and Other End-Use Industries - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 81: Germany Historic Review for Surface Acoustic Wave (SAW) Devices by End-Use Industry - Aerospace & Defense, Telecommunication, Environmental & Industrial, Automotive, Consumer Electronics and Other End-Use Industries Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 82: Germany 16-Year Perspective for Surface Acoustic Wave (SAW) Devices by End-Use Industry - Percentage Breakdown of Value Sales for Aerospace & Defense, Telecommunication, Environmental & Industrial, Automotive, Consumer Electronics and Other End-Use Industries for the Years 2014, 2024 & 2030

- ITALY

- TABLE 83: Italy Recent Past, Current & Future Analysis for Surface Acoustic Wave (SAW) Devices by Device - Filters, Oscillators, Resonators, Transducers and Other Devices - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 84: Italy Historic Review for Surface Acoustic Wave (SAW) Devices by Device - Filters, Oscillators, Resonators, Transducers and Other Devices Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 85: Italy 16-Year Perspective for Surface Acoustic Wave (SAW) Devices by Device - Percentage Breakdown of Value Sales for Filters, Oscillators, Resonators, Transducers and Other Devices for the Years 2014, 2024 & 2030

- TABLE 86: Italy Recent Past, Current & Future Analysis for Surface Acoustic Wave (SAW) Devices by End-Use Industry - Aerospace & Defense, Telecommunication, Environmental & Industrial, Automotive, Consumer Electronics and Other End-Use Industries - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 87: Italy Historic Review for Surface Acoustic Wave (SAW) Devices by End-Use Industry - Aerospace & Defense, Telecommunication, Environmental & Industrial, Automotive, Consumer Electronics and Other End-Use Industries Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 88: Italy 16-Year Perspective for Surface Acoustic Wave (SAW) Devices by End-Use Industry - Percentage Breakdown of Value Sales for Aerospace & Defense, Telecommunication, Environmental & Industrial, Automotive, Consumer Electronics and Other End-Use Industries for the Years 2014, 2024 & 2030

- UNITED KINGDOM

- Surface Acoustic Wave (SAW) Devices Market Presence - Strong/Active/Niche/Trivial - Key Competitors in the United Kingdom for 2024 (E)

- TABLE 89: UK Recent Past, Current & Future Analysis for Surface Acoustic Wave (SAW) Devices by Device - Filters, Oscillators, Resonators, Transducers and Other Devices - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 90: UK Historic Review for Surface Acoustic Wave (SAW) Devices by Device - Filters, Oscillators, Resonators, Transducers and Other Devices Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 91: UK 16-Year Perspective for Surface Acoustic Wave (SAW) Devices by Device - Percentage Breakdown of Value Sales for Filters, Oscillators, Resonators, Transducers and Other Devices for the Years 2014, 2024 & 2030

- TABLE 92: UK Recent Past, Current & Future Analysis for Surface Acoustic Wave (SAW) Devices by End-Use Industry - Aerospace & Defense, Telecommunication, Environmental & Industrial, Automotive, Consumer Electronics and Other End-Use Industries - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 93: UK Historic Review for Surface Acoustic Wave (SAW) Devices by End-Use Industry - Aerospace & Defense, Telecommunication, Environmental & Industrial, Automotive, Consumer Electronics and Other End-Use Industries Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 94: UK 16-Year Perspective for Surface Acoustic Wave (SAW) Devices by End-Use Industry - Percentage Breakdown of Value Sales for Aerospace & Defense, Telecommunication, Environmental & Industrial, Automotive, Consumer Electronics and Other End-Use Industries for the Years 2014, 2024 & 2030

- REST OF EUROPE

- TABLE 95: Rest of Europe Recent Past, Current & Future Analysis for Surface Acoustic Wave (SAW) Devices by Device - Filters, Oscillators, Resonators, Transducers and Other Devices - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 96: Rest of Europe Historic Review for Surface Acoustic Wave (SAW) Devices by Device - Filters, Oscillators, Resonators, Transducers and Other Devices Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 97: Rest of Europe 16-Year Perspective for Surface Acoustic Wave (SAW) Devices by Device - Percentage Breakdown of Value Sales for Filters, Oscillators, Resonators, Transducers and Other Devices for the Years 2014, 2024 & 2030

- TABLE 98: Rest of Europe Recent Past, Current & Future Analysis for Surface Acoustic Wave (SAW) Devices by End-Use Industry - Aerospace & Defense, Telecommunication, Environmental & Industrial, Automotive, Consumer Electronics and Other End-Use Industries - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 99: Rest of Europe Historic Review for Surface Acoustic Wave (SAW) Devices by End-Use Industry - Aerospace & Defense, Telecommunication, Environmental & Industrial, Automotive, Consumer Electronics and Other End-Use Industries Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 100: Rest of Europe 16-Year Perspective for Surface Acoustic Wave (SAW) Devices by End-Use Industry - Percentage Breakdown of Value Sales for Aerospace & Defense, Telecommunication, Environmental & Industrial, Automotive, Consumer Electronics and Other End-Use Industries for the Years 2014, 2024 & 2030

- ASIA-PACIFIC

- Surface Acoustic Wave (SAW) Devices Market Presence - Strong/Active/Niche/Trivial - Key Competitors in Asia-Pacific for 2024 (E)

- TABLE 101: Asia-Pacific Recent Past, Current & Future Analysis for Surface Acoustic Wave (SAW) Devices by Device - Filters, Oscillators, Resonators, Transducers and Other Devices - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 102: Asia-Pacific Historic Review for Surface Acoustic Wave (SAW) Devices by Device - Filters, Oscillators, Resonators, Transducers and Other Devices Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 103: Asia-Pacific 16-Year Perspective for Surface Acoustic Wave (SAW) Devices by Device - Percentage Breakdown of Value Sales for Filters, Oscillators, Resonators, Transducers and Other Devices for the Years 2014, 2024 & 2030

- TABLE 104: Asia-Pacific Recent Past, Current & Future Analysis for Surface Acoustic Wave (SAW) Devices by End-Use Industry - Aerospace & Defense, Telecommunication, Environmental & Industrial, Automotive, Consumer Electronics and Other End-Use Industries - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 105: Asia-Pacific Historic Review for Surface Acoustic Wave (SAW) Devices by End-Use Industry - Aerospace & Defense, Telecommunication, Environmental & Industrial, Automotive, Consumer Electronics and Other End-Use Industries Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 106: Asia-Pacific 16-Year Perspective for Surface Acoustic Wave (SAW) Devices by End-Use Industry - Percentage Breakdown of Value Sales for Aerospace & Defense, Telecommunication, Environmental & Industrial, Automotive, Consumer Electronics and Other End-Use Industries for the Years 2014, 2024 & 2030

- REST OF WORLD

- TABLE 107: Rest of World Recent Past, Current & Future Analysis for Surface Acoustic Wave (SAW) Devices by Device - Filters, Oscillators, Resonators, Transducers and Other Devices - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 108: Rest of World Historic Review for Surface Acoustic Wave (SAW) Devices by Device - Filters, Oscillators, Resonators, Transducers and Other Devices Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 109: Rest of World 16-Year Perspective for Surface Acoustic Wave (SAW) Devices by Device - Percentage Breakdown of Value Sales for Filters, Oscillators, Resonators, Transducers and Other Devices for the Years 2014, 2024 & 2030

- TABLE 110: Rest of World Recent Past, Current & Future Analysis for Surface Acoustic Wave (SAW) Devices by End-Use Industry - Aerospace & Defense, Telecommunication, Environmental & Industrial, Automotive, Consumer Electronics and Other End-Use Industries - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 111: Rest of World Historic Review for Surface Acoustic Wave (SAW) Devices by End-Use Industry - Aerospace & Defense, Telecommunication, Environmental & Industrial, Automotive, Consumer Electronics and Other End-Use Industries Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 112: Rest of World 16-Year Perspective for Surface Acoustic Wave (SAW) Devices by End-Use Industry - Percentage Breakdown of Value Sales for Aerospace & Defense, Telecommunication, Environmental & Industrial, Automotive, Consumer Electronics and Other End-Use Industries for the Years 2014, 2024 & 2030