|

|

市場調査レポート

商品コード

1577003

動物ヘルスケア市場、市場動向と促進要因、産業動向分析と予測、2024年~2032年Animal Healthcare Market, Opportunity, Growth Drivers, Industry Trend Analysis and Forecast, 2024-2032 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 動物ヘルスケア市場、市場動向と促進要因、産業動向分析と予測、2024年~2032年 |

|

出版日: 2024年08月02日

発行: Global Market Insights Inc.

ページ情報: 英文 235 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

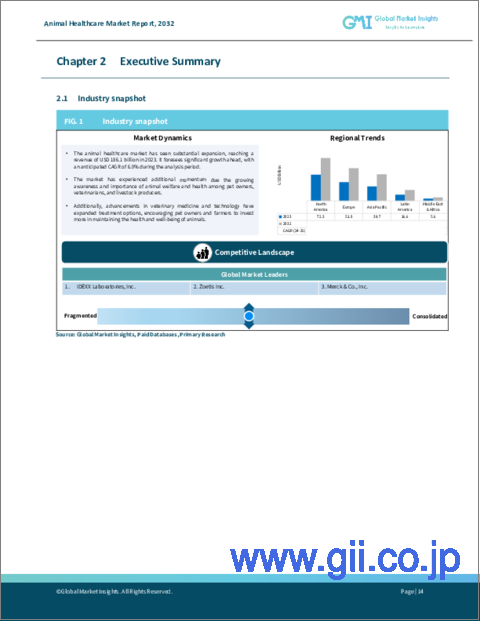

世界の動物ヘルスケア市場は、2023年に1,861億米ドルと評価され、2024年から2032年にかけてCAGR 6%で成長すると予測されています。

ペットの飼育率の増加が、ペットヘルスケアへの支出増につながっています。世界動物基金(World Animal Foundation)によると、世界には3億7,300万匹の猫と4億7,100万匹の犬がいます。人獣共通感染症の増加と動物の健康の重要性に対する意識の高まりが、予防ヘルスケア製品とサービスの需要を押し上げています。

肥満、糖尿病、がんなど、動物の慢性疾患の流行は、高度な獣医学的診断と治療法の必要性を高めています。米国獣医師会(AVMA)の報告によると、犬の約4頭に1頭が腫瘍を発症し、10歳以上の犬の半数近くががんを発症するといいます。

市場は製品別に医薬品、医療機器、動物医療サービスに区分されます。2023年には、動物医療サービスが75.9%と最も高い市場シェアを占めています。動物医療サービスには、予防ケア、診断、治療、手術、歯科治療、緊急サービスが含まれます。また、グルーミングやデイケアサービスも含まれます。人獣共通感染症の流行の高まりと、食の安全を確保するための家畜の予防ヘルスケアの必要性が、この分野の成長を促進しています。

動物ヘルスケア市場は、動物の種類によってコンパニオンアニマルと畜産動物に分類されます。コンパニオンアニマル・セグメントは、2023年に1,132億米ドルの最も高い収益を生み出し、2024~2032年の間に大きく成長すると予想されています。このセグメントには、犬、猫、馬、その他のコンパニオンアニマルが含まれます。ペットを家族の一員として扱うヒューマニゼーション(人間化)の動向が、ペットのヘルスケアニーズへの支出増を促しています。ペット飼育の増加、可処分所得の増加、動物医療サービスの進歩がさらにこのセグメントの成長に寄与しています。

北米の動物ヘルスケア産業は、2023年には38.9%で最大のシェアを占め、予測期間にはCAGR 5.5%で成長すると予測されています。市場シェアが高いのは、獣医医療のインフラが整備されていること、ペットの飼育率が高いこと、畜産人口が多いこと、動物の健康とウェルネスへの関心が高まっていることによります。可処分所得水準の向上は、ペット用ヘルスケア製品やサービスへの支出増につながり、市場成長をさらに後押ししています。主要市場プレイヤーの存在と、動物用診断薬と治療薬における継続的な技術進歩も、動物ヘルスケア業界における優位性に寄与しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- ペット動物の数増加

- 政府や公的機関による動物ケア支援の増加

- オンライン動物薬局の需要の増加

- 動物ヘルスケア支出の増加

- 業界の潜在的リスク&課題

- 動物用医薬品の高コスト

- 農村部でのアクセス制限

- 促進要因

- 成長の可能性分析

- 規制状況

- 北米

- 米国

- カナダ

- 欧州連合

- アジア太平洋

- 日本

- 中国

- 北米

- 技術展望

- 償還シナリオ

- 動物医療産業におけるベンチャーキャピタルのシナリオ

- 動物医療産業の経済的影響

- ギャップ分析

- 消費者行動動向

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品別、2018年~2032年

- 主要動向

- 医薬品

- 医薬品

- 抗寄生虫薬

- 抗炎症薬

- 抗感染症薬

- その他の医薬品

- ワクチン

- 改良型生ワクチン(MLV)

- キルド不活化ワクチン

- その他のワクチン

- 薬用飼料添加物

- 抗生物質

- ビタミン

- アミノ酸

- 酵素

- 酸化防止剤

- プレバイオティクスとプロバイオティクス

- ミネラル

- その他の薬用飼料添加物

- 医薬品

- 医療機器

- 動物用診断機器

- 動物用麻酔機器

- 動物用患者モニタリング機器

- 動物用手術機器

- 動物用消耗品

- その他の医療機器

- 動物医療サービス

第6章 市場推計・予測:動物の種類別、2018年~2032年

- 主要動向

- コンパニオンアニマル

- 犬

- 猫

- 馬

- その他のコンパニオンアニマル

- 家畜

- 家禽

- 豚

- 牛

- 魚類

- その他の家畜

第7章 市場推計・予測:流通チャネル別、2018年~2032年

- 主要動向

- 動物病院薬局

- eコマース

- 小売薬局

第8章 市場推計・予測:地域別、2018年~2032年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- ポーランド

- オランダ

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- 台湾

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ

- 中東・アフリカ

- 南アフリカ

- GCC諸国

- イスラエル

- その他中東とアフリカ

第9章 企業プロファイル

- B. Braun Vet Care(B Braun Melsungen AG)

- Boehringer Ingelheim International GmbH

- Ceva Sante Animale

- Dechra Pharmaceuticals

- Elanco Animal Health

- Endovac Animal Health

- HIPRA

- IDEXX Laboratories

- Merck and Co

- Medtronic plc

- Neogen Corporation

- Sklar Surgical Instruments

- Symrise

- Vetoquinol SA

- Virbac SA

- Zoetis, Inc.

The Global Animal Healthcare Market was valued at USD 186.1 billion in 2023 and is projected to grow at a CAGR of 6% from 2024 to 2032. Increasing pet ownership rates are driving higher spending on pet healthcare. According to the World Animal Foundation, there are nearly 373 million pet cats and 471 million pet dogs globally. The rise in zoonotic diseases and growing awareness of animal health importance are boosting demand for preventive healthcare products and services.

The prevalence of chronic diseases in animals, such as obesity, diabetes, and cancer, is increasing the need for advanced veterinary diagnostics and therapeutics. The American Veterinary Medical Association (AVMA) reports that approximately 1 in 4 dogs will develop neoplasia, and nearly half of dogs over 10 years old will develop cancer.

The overall industry is divided into product, animal type, distribution channel, and region.

The market is segmented by product into pharmaceuticals, medical devices, and veterinary services. In 2023, veterinary services held the highest market share at 75.9%. Veterinary services encompass preventive care, diagnostics, treatments, surgeries, dental care, and emergency services. They also include grooming and day-care services. The rising prevalence of zoonotic diseases and the need for preventive healthcare in livestock to ensure food safety are driving this segment's growth.

The animal healthcare market is classified by animal type into companion animals and livestock animals. The companion animals segment generated the highest revenue of USD 113.2 billion in 2023 and is expected to grow significantly during 2024-2032. This segment includes dogs, cats, horses, and other companion animals. The trend of pet humanization, where pets are treated as family members, is driving higher spending on their healthcare needs. Increasing pet ownership, rising disposable incomes, and advancements in veterinary healthcare services are further contributing to segment growth.

North America animal healthcare industry held the largest share at 38.9% in 2023 and is anticipated to grow at a 5.5% CAGR over the forecast period. The strong market share is due to its well-established veterinary healthcare infrastructure, high pet adoption rates, large livestock population, and a growing focus on animal health and wellness. Increased disposable income levels have led to higher spending on pet healthcare products and services, further driving market growth. The presence of key market players and ongoing technological advancements in veterinary diagnostics and therapeutics may also contribute to dominance in the animal healthcare industry.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing population of pet animals

- 3.2.1.2 Increasing support offered by government and public organizations for animal care

- 3.2.1.3 Growing demand for online veterinary pharmacies

- 3.2.1.4 Increase in animal healthcare expenditure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with animal health drugs

- 3.2.2.2 Limited access in rural areas

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 European Union

- 3.4.3 Asia Pacific

- 3.4.3.1 Japan

- 3.4.3.2 China

- 3.4.1 North America

- 3.5 Technology landscape

- 3.6 Reimbursement scenario

- 3.7 Venture capitalist scenario in animal health industry

- 3.8 Economic impacts of the animal health industry

- 3.9 Gap analysis

- 3.10 Consumer behaviour trends

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2018 - 2032 ($ Mn)

- 5.1 Key trends

- 5.2 Pharmaceuticals

- 5.2.1 Drugs

- 5.2.1.1 Antiparasitic

- 5.2.1.2 Anti-inflammatory

- 5.2.1.3 Anti-infectives

- 5.2.1.4 Other drugs

- 5.2.2 Vaccines

- 5.2.2.1 Modified live vaccines (MLV)

- 5.2.2.2 Killed inactivated vaccines

- 5.2.2.3 Other vaccines

- 5.2.3 Medicated feed additives

- 5.2.3.1 Antibiotics

- 5.2.3.2 Vitamins

- 5.2.3.3 Amino acids

- 5.2.3.4 Enzymes

- 5.2.3.5 Antioxidants

- 5.2.3.6 Prebiotics and probiotics

- 5.2.3.7 Minerals

- 5.2.3.8 Other medicated feed additives

- 5.2.1 Drugs

- 5.3 Medical devices

- 5.3.1 Veterinary diagnostic equipment

- 5.3.2 Veterinary anesthesia equipment

- 5.3.3 Veterinary patient monitoring equipment

- 5.3.4 Veterinary surgical equipment

- 5.3.5 Veterinary consumables

- 5.3.6 Other medical devices

- 5.4 Veterinary services

Chapter 6 Market Estimates and Forecast, By Animal Type, 2018 - 2032 ($ Mn)

- 6.1 Key trends

- 6.2 Companion animals

- 6.2.1 Dogs

- 6.2.2 Cats

- 6.2.3 Horses

- 6.2.4 Other companion animals

- 6.3 Livestock animals

- 6.3.1 Poultry

- 6.3.2 Swine

- 6.3.3 Cattle

- 6.3.4 Fish

- 6.3.5 Other livestock animals

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2018 - 2032 ($ Mn)

- 7.1 Key trends

- 7.2 Veterinary hospital pharmacy

- 7.3 E-commerce

- 7.4 Retail pharmacy

Chapter 8 Market Estimates and Forecast, By Region, 2018 - 2032 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Poland

- 8.3.7 Netherlands

- 8.3.8 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Taiwan

- 8.4.7 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 GCC Countries

- 8.6.3 Israel

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 B. Braun Vet Care (B Braun Melsungen AG)

- 9.2 Boehringer Ingelheim International GmbH

- 9.3 Ceva Sante Animale

- 9.4 Dechra Pharmaceuticals

- 9.5 Elanco Animal Health

- 9.6 Endovac Animal Health

- 9.7 HIPRA

- 9.8 IDEXX Laboratories

- 9.9 Merck and Co

- 9.10 Medtronic plc

- 9.11 Neogen Corporation

- 9.12 Sklar Surgical Instruments

- 9.13 Symrise

- 9.14 Vetoquinol SA

- 9.15 Virbac SA

- 9.16 Zoetis, Inc.