地下高圧ケーブルの市場機会と成長促進要因、産業動向分析、予測、2025年~2034年

Underground High Voltage Cable Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 151 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801948

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

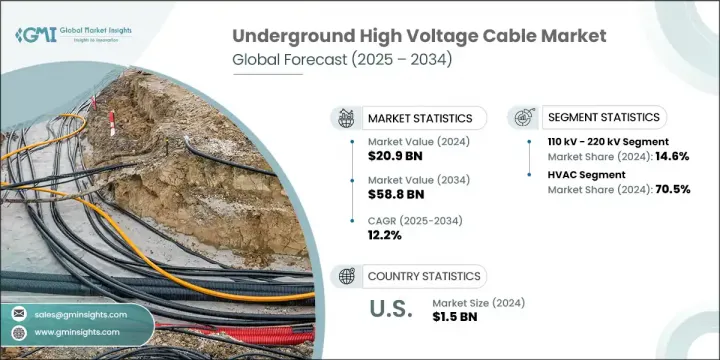

地下高圧ケーブルの世界市場規模は、2024年に209億米ドルとなり、CAGR 12.2%で成長し、2034年には588億米ドルに達すると推定されます。

この力強い成長は、世界の都市化の加速によるところが大きく、特に先進国や急速に開発が進んでいる地域では、信頼性の高い送電に対する需要が高まっています。都市密度が高まるにつれて、スペース効率が高く、視覚的影響が少ない地下ケーブルシステムが好まれるようになっています。美観と安全性が重要視される大都市圏では、電力会社が架空送電線をやめて地下送電線を採用するケースが増えています。

これらのシステムは信頼性が高く、異常気象時の事故や停電のリスクが大幅に低くなります。政府や公益事業会社は、スマートシティ開発計画に地下配線を組み込んでおり、長期的な魅力をさらに高めています。山火事やハリケーンなど、気候に関連した災害の増加に伴い、業界は地下高圧ケーブルを送電網の回復力の要と見ています。グリッド近代化のための規制枠組みや政府主導のインセンティブも、いくつかの地域で市場の勢いを強める上で極めて重要な役割を果たしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 209億米ドル |

| 予測金額 | 588億米ドル |

| CAGR | 12.2% |

110kV~220kVの地下ケーブルセグメントは、2024年に14.6%のシェアを占め、2034年までのCAGRは25%と予想されています。この電圧範囲は、送電や大容量の配電ネットワークに幅広く適用できるため好まれています。特に、大規模な再生可能エネルギープロジェクトを送電網に統合する際、変電所間の接続や中距離の送電に不可欠な役割を果たします。ユーティリティプロバイダーは、地域の配電需要に効率的に対応するため、このケーブルへの依存度を高めています。

高圧交流(HVAC)ケーブルセグメントは2024年に70.5%の最大シェアを占め、2034年までのCAGRは21%と予測されています。HVACシステムは、現在のインフラとの互換性が容易であるため、都市部や中距離送電における地下ケーブル敷設の有力な選択肢であり続けています。絶縁技術とコンパクトなケーブル設計の進歩により、HVACの設置効率はさらに向上し、密集した複雑な環境に理想的なものとなっています。複雑なコンバーターステーションを必要とせず、従来の資産とシームレスに統合できるため、送電網近代化プロジェクトに最適なソリューションとなっています。

米国の地下高圧ケーブル市場は、50.2%のシェアを占め、2024年には15億米ドルを生成しています。米国では、送電網強化の取り組み、エネルギー転換政策、気候変動に関連した災害の頻度増加などが成長の原動力となっています。ユーティリティは、特に災害の多い都市部において、インフラの回復力と継続的な電力供給を確保するため、地下ケーブル配線に投資しています。特に国のインフラ構想による開発プログラムと資金援助が、こうした開発を加速させています。さらに、データセンター、電気自動車ネットワーク、再生可能エネルギーなどの分野からの急速な需要増加が、地下高圧ソリューションのさらなる展開を促しています。

世界の地下高圧ケーブル市場を形成している有力企業には、Sumitomo Electric Industries Ltd.、Nexans、ZTT、TF Kable、Riyadh Cable、NKT A/S、Brugg Kabel AG、Jeddah Cables、Ducab、Prysmian Group、KEI Industries Limited、alfanar Group、ILJIN ELECTRIC、Hellenic Cables、Universal Cable Limited、Taihan Cable &Solution Co.L.L.C.、Tratos、LS Cable &System Ltd.、FURUKAWA ELECTRIC CO., LTD.などがあります。地下高圧ケーブル分野の主要企業は、製品革新に積極的に投資しており、次世代送電要件を満たすため、ケーブルの効率、小型化、熱性能の向上に注力しています。多くの企業は、大規模送電プロジェクトの長期契約を確保するため、公益事業者やインフラ開発業者と戦略的提携や合弁事業を結んでいます。メーカーはまた、リードタイムを短縮し、各地域の需要急増により効果的に対応するため、世界な生産拠点を拡大しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 規制情勢

- 業界への影響要因

- 価格動向分析(USD/km)

- 電圧別

- 地域別

- 成長可能性分析

- ポーターの分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析:地域別

- 北米

- 欧州

- アジア太平洋地域

- 世界のその他の地域

- 戦略的取り組み

- 競合ベンチマーキング

- 戦略的ダッシュボード

- イノベーションとテクノロジーの情勢

第5章 市場規模・予測:電圧別、2021年~2034年

- 主要動向

- 110kV未満

- 110kV~220kV

- 220kV超

第6章 市場規模・予測:電流別、2021年~2034年

- 主要動向

- HVAC

- HVDC

第7章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- アジア太平洋地域

- 中国

- インド

- タイ

- インドネシア

- 世界のその他の地域

第8章 企業プロファイル

- alfanar Group

- Brugg Kabel AG

- Ducab

- FURUKAWA ELECTRIC CO., LTD.

- Hellenic Cables

- ILJIN ELECTRIC

- Jeddah Cables

- KEI Industries Limited

- LS Cable &System Ltd.

- Nexans

- NKT A/S

- Prysmian Group

- Power Plus Cables Co. L.L.C.

- Riyadh Cable

- Southwire Company, LLC

- Sumitomo Electric Industries Ltd.

- Taihan Cable &Solution Co., Ltd.

- TF Kable

- Tratos

- Universal Cable Limited

- ZTT

目次

The Global Underground High Voltage Cable Market was valued at USD 20.9 billion in 2024 and is estimated to grow at a CAGR of 12.2% to reach USD 58.8 billion by 2034. This robust growth is largely attributed to the accelerating rate of urbanization worldwide, which is intensifying the demand for dependable electricity transmission, especially in industrialized and fast-developing regions. As urban density increases, the preference is shifting toward underground cable systems due to their space efficiency and reduced visual impact. In metropolitan areas where aesthetics and safety are vital, utilities are increasingly abandoning overhead lines in favor of underground solutions.

These systems offer greater reliability and significantly lower risks of accidents or outages during extreme weather conditions. Governments and utility companies are incorporating underground cabling into smart city development plans, further enhancing its long-term appeal. With the rise in climate-related disruptions, such as wildfires and hurricanes, the industry is seeing underground high voltage cables as a cornerstone of grid resiliency. Regulatory frameworks and government-led incentives for grid modernization are also playing a pivotal role in strengthening market momentum across several regions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $20.9 Billion |

| Forecast Value | $58.8 Billion |

| CAGR | 12.2% |

The 110 kV to 220 kV underground cable segment accounted for a 14.6% share in 2024 and is expected to register a CAGR of 25% through 2034. This voltage range is favored due to its broad applicability in transmission and high-capacity distribution networks. It serves essential roles in linking substations and routing power over moderate distances, especially when integrating large-scale renewable energy projects into the grid. Utility providers increasingly rely on these cables to meet regional power distribution demands efficiently.

The high voltage alternating current (HVAC) cables segment held the largest share of 70.5% in 2024 and is forecasted to grow at a CAGR of 21% through 2034. HVAC systems remain the dominant choice for underground cable installations in urban and mid-range transmission due to their easy compatibility with current infrastructure. Advances in insulation technologies and compact cable design have further improved HVAC installation efficiency, making them ideal for dense, complex environments. Their seamless integration with conventional assets-without requiring complex converter stations-makes them a go-to solution for grid modernization projects.

U.S. Underground High Voltage Cable Market held 50.2% share, generating USD 1.5 billion in 2024. Growth in the U.S. is strongly driven by grid reinforcement initiatives, energy transition policies, and the increasing frequency of climate-related disruptions. Utilities are investing in underground cabling to ensure infrastructure resilience and a continuous power supply, particularly in disaster-prone and urban areas. Government programs and funding support, especially from national infrastructure initiatives, are accelerating these developments. In addition, rapid demand growth from sectors like data centers, electric vehicle networks, and renewable energy is encouraging further deployment of underground high voltage solutions.

Prominent players shaping the Global Underground High Voltage Cable Market include Sumitomo Electric Industries Ltd., Nexans, ZTT, TF Kable, Riyadh Cable, NKT A/S, Brugg Kabel AG, Jeddah Cables, Ducab, Prysmian Group, KEI Industries Limited, alfanar Group, ILJIN ELECTRIC, Hellenic Cables, Universal Cable Limited, Taihan Cable & Solution Co., Ltd., Southwire Company, LLC, Power Plus Cables Co. L.L.C., Tratos, LS Cable & System Ltd., and FURUKAWA ELECTRIC CO., LTD. Leading companies in the underground high voltage cable sector are actively investing in product innovation, focusing on improving cable efficiency, compactness, and thermal performance to meet next-generation transmission requirements. Many firms are forming strategic alliances and joint ventures with utility providers and infrastructure developers to secure long-term contracts for large-scale transmission projects. Manufacturers are also scaling up their global production footprints to reduce lead times and respond more effectively to regional demand surges.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

- 2.1.1 Business trends

- 2.1.2 Voltage trends

- 2.1.3 Current trends

- 2.1.4 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.4 Price trend analysis (USD/km)

- 3.4.1 By voltage

- 3.4.2 By region

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

- 3.7.1 Political factors

- 3.7.2 Economic factors

- 3.7.3 Social factors

- 3.7.4 Technological factors

- 3.7.5 Environmental factors

- 3.7.6 Legal factors

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis by region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Rest of World

- 4.3 Strategic initiative

- 4.4 Competitive benchmarking

- 4.5 Strategic dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Voltage, 2021 - 2034 (USD Million, km)

- 5.1 Key trends

- 5.2 < 110 kV

- 5.3 110 kV - 220 kV

- 5.4 > 220 kV

Chapter 6 Market Size and Forecast, By Current, 2021 - 2034 (USD Million, km)

- 6.1 Key trends

- 6.2 HVAC

- 6.3 HVDC

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Million, km)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Thailand

- 7.4.4 Indonesia

- 7.5 Rest of World

Chapter 8 Company Profiles

- 8.1 alfanar Group

- 8.2 Brugg Kabel AG

- 8.3 Ducab

- 8.4 FURUKAWA ELECTRIC CO., LTD.

- 8.5 Hellenic Cables

- 8.6 ILJIN ELECTRIC

- 8.7 Jeddah Cables

- 8.8 KEI Industries Limited

- 8.9 LS Cable & System Ltd.

- 8.10 Nexans

- 8.11 NKT A/S

- 8.12 Prysmian Group

- 8.13 Power Plus Cables Co. L.L.C.

- 8.14 Riyadh Cable

- 8.15 Southwire Company, LLC

- 8.16 Sumitomo Electric Industries Ltd.

- 8.17 Taihan Cable & Solution Co., Ltd.

- 8.18 TF Kable

- 8.19 Tratos

- 8.20 Universal Cable Limited

- 8.21 ZTT

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 151 Pages

- 納期

- 2~3営業日