硬性内視鏡市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Rigid Endoscopes Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801943

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

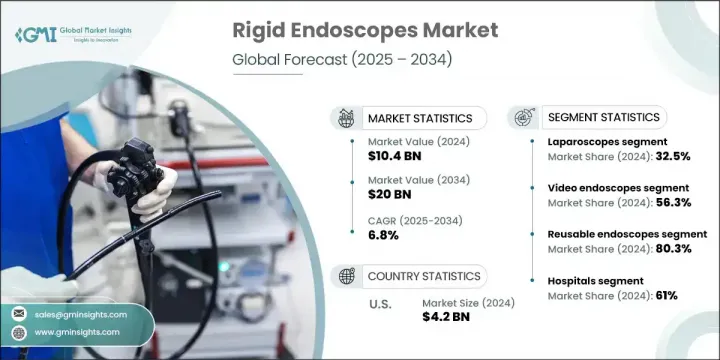

世界の硬性内視鏡市場は、2024年には104億米ドルとなり、CAGR 6.8%で成長し、2034年には200億米ドルに達すると推定されます。

市場拡大の主な要因は、慢性的な健康問題の発生率の上昇と世界人口の高齢化です。硬性内視鏡は、呼吸器合併症、消化器系疾患、耳鼻咽喉科疾患を含む幅広い疾患の診断と治療を支援する低侵襲処置を実施するために不可欠です。これらの装置は鮮明な画像を提供し、腹腔、関節、生殖器系、膀胱を含む手術に広く適用されています。回復が早く、合併症が少なく、入院期間が短いため、低侵襲技術に対する患者の嗜好が高まっていることが、需要を押し上げる上で重要な役割を果たしています。さらに、高精細画像や手術ナビゲーションツールの進歩により、外来および入院治療での採用がさらに進んでいます。

腹腔鏡カテゴリーは2024年に32.5%のシェアを占め、胆嚢摘出、ヘルニア修復、婦人科手術など、術後の痛みを最小限に抑え、入院期間を短縮する手術の人気が拡大していることがその要因となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 104億米ドル |

| 予測金額 | 200億米ドル |

| CAGR | 6.8% |

ビデオ内視鏡の2024年のシェアは56.3%で、リアルタイムで高精細な画像を提供できることが牽引しています。また、これらのツールは、手術中のチームコラボレーションを促進し、外科部門全体で非常に好まれています。

米国の硬性内視鏡市場は堅牢なヘルスケアインフラと低侵襲手術手技の広範な導入に支えられ、2024年には42億米ドルに達しました。強力な償還の枠組み、高齢者人口の増加、早期診断スクリーニングの増加により、地域の需要は引き続き強化されています。手術件数の増加、先進的な画像技術革新、外来患者による手術への注目が、この勢いを持続させています。米国の大手メーカーや医療技術革新企業も、内視鏡の研究開発や自動化に多額の投資を行っています。

市場情勢を形成している主要企業には、Stryker、Olympus Corporation、Richard Wolf、Karl Storz、Smith &Nephew、富士フイルム、Scholly Fiberoptic、Arthrex、PENTAX Medical、ConMed、B. Braun、Henke-Sass、Wolf、Cook Medical、XION GmbH、Boston Scientific、Ambu A/Sなどがあります。硬性内視鏡市場で各社が採用している主な戦略には、AI支援イメージング、人間工学に基づいた器具設計、手術精度を向上させる統合ビデオシステムなどによる製品イノベーションの推進が含まれます。製品ポートフォリオを拡大し、未開拓の地域に参入するために、合併、戦略的提携、買収が一般的です。各社は、低侵襲プラットフォームを強化し、ロボット内視鏡技術を探求するため、研究開発に多額の投資を行っています。また、多くの企業がアフターサービス網を強化し、医師のトレーニングプログラムに取り組んでおり、普及を推進しています。手術センターや医療機関との提携は、早期の臨床導入を支援し、市場への浸透を世界的に高めています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 慢性疾患の増加

- 技術的進歩

- 低侵襲手術の導入増加

- 健康意識の高まりと早期診断の需要

- 業界の潜在的リスク&課題

- デバイスのコストが高め

- 患者の不快感や手順の制限のリスク

- 市場機会

- 外来および外来手術センター(ASC)の拡張

- ヘルスケアインフラが整備されている新興市場

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- テクノロジーの情勢

- 現在の技術動向

- 新興技術

- 償還シナリオ

- 価格分析、2024

- 将来の市場動向

- 市場参入戦略

- パイプライン分析

- ギャップ分析

- ポーターの分析

- PESTEL分析

- バリューチェーン分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- 世界

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 腹腔鏡

- 関節鏡

- 膀胱鏡

- 耳鼻咽喉科内視鏡

- 気管支鏡

- 尿管鏡

- 子宮鏡

- その他の製品タイプ

第6章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 従来の内視鏡

- ビデオ内視鏡

- 光ファイバー内視鏡

第7章 市場推計・予測:ユーザビリティ別、2021年~2034年

- 主要動向

- 再利用可能な内視鏡

- 使い捨て内視鏡

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 外来手術センター

- その他の用途

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Ambu

- Arthrex

- B. Braun

- Boston Scientific

- ConMed

- Cook

- Fujifilm

- Henke-Sass Wolf

- Olympus

- PENTAX Medical

- Richard Wolf

- Scholly Fiberoptic

- Smith &Nephew

- Storz

- Stryker

- XION medical

目次

The Global Rigid Endoscopes Market was valued at USD 10.4 billion in 2024 and is estimated to grow at a CAGR of 6.8% to reach USD 20 billion by 2034. Market expansion is largely driven by the rising incidence of chronic health issues and an aging global population. Rigid endoscopes are essential for performing minimally invasive procedures that aid in diagnosing and treating a wide range of conditions, including respiratory complications, digestive system ailments, and ENT disorders. These devices deliver crystal-clear imaging and are widely applied in surgeries involving the abdominal cavity, joints, reproductive system, and urinary bladder. Increasing patient preference for minimally invasive techniques-because of faster recovery, fewer complications, and lower hospitalization times-is playing a vital role in boosting demand. Additionally, ongoing advancements in high-definition imaging and surgical navigation tools further reinforce their adoption in both outpatient and inpatient care.

The laparoscopes category held 32.5% share in 2024, fueled by the expanding popularity of procedures like gallbladder removal, hernia repair, and gynecological surgeries that minimize post-operative pain and shorten hospital stays.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.4 Billion |

| Forecast Value | $20 Billion |

| CAGR | 6.8% |

The video endoscopes segment held 56.3% share in 2024, driven by their ability to deliver real-time, high-definition visualization, which enhances surgical precision and clinical documentation. These tools also facilitate team collaboration during operations, making them highly preferred across surgical departments.

U.S. Rigid Endoscopes Market generated USD 4.2 billion in 2024, supported by robust healthcare infrastructure and wide-scale adoption of minimally invasive surgical techniques. Strong reimbursement frameworks, a growing elderly population, and an uptick in early diagnostic screenings continue to bolster regional demand. Rising surgical volumes, advanced imaging innovations, and a focus on outpatient procedures across the country are sustaining this momentum. Leading manufacturers and medtech innovators in the U.S. are also channeling substantial investments into endoscopic R&D and automation.

Top players shaping the Rigid Endoscopes Market landscape include Stryker, Olympus Corporation, Richard Wolf, Karl Storz, Smith & Nephew, Fujifilm, Scholly Fiberoptic, Arthrex, PENTAX Medical, ConMed, B. Braun, Henke-Sass, Wolf, Cook Medical, XION GmbH, Boston Scientific, and Ambu A/S. Key strategies adopted by companies in the rigid endoscopes market include advancing product innovation through AI-assisted imaging, ergonomic instrument design, and integrated video systems to improve surgical precision. Mergers, strategic partnerships, and acquisitions are common to expand product portfolios and enter untapped geographic areas. Players are heavily investing in R&D to enhance minimally invasive platforms and explore robotic endoscopic technologies. Many are also strengthening after-sales service networks and engaging in physician training programs to drive adoption. Collaborations with surgical centers and institutions support early clinical adoption and increase market penetration globally.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Technology trends

- 2.2.3 Usability trends

- 2.2.4 End use trends

- 2.2.5 Region trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of chronic conditions

- 3.2.1.2 Technological advancements

- 3.2.1.3 Rising adoption of minimally invasive surgeries

- 3.2.1.4 Increasing health awareness and demand for early-stage diagnosis

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High device cost

- 3.2.2.2 Risk of patient discomfort and procedural limitations

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of outpatient and ambulatory surgical centers (ASCs)

- 3.2.3.2 Emerging markets with improving healthcare infrastructure

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Reimbursement scenario

- 3.7 Pricing analysis, 2024

- 3.7.1 North America

- 3.7.2 Europe

- 3.7.3 Asia Pacific

- 3.7.4 Latin America

- 3.7.5 Middle East and Africa

- 3.8 Future market trends

- 3.9 Go-to-market strategy

- 3.10 Pipeline analysis

- 3.11 Gap analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

- 3.14 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 Latin America

- 4.3.6 MEA

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn and Units)

- 5.1 Key trends

- 5.2 Laparoscopes

- 5.3 Arthroscopes

- 5.4 Cystoscopes

- 5.5 ENT endoscopes

- 5.6 Bronchoscopes

- 5.7 Ureteroscopes

- 5.8 Hysteroscopes

- 5.9 Other product types

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Conventional endoscopes

- 6.3 Video endoscopes

- 6.4 Fiber-optic endoscopes

Chapter 7 Market Estimates and Forecast, By Usability, 2021 - 2034 ($ Mn and Units)

- 7.1 Key trends

- 7.2 Reusable endoscopes

- 7.3 Disposable endoscopes

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Ambulatory surgical centers

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn and Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Ambu

- 10.2 Arthrex

- 10.3 B. Braun

- 10.4 Boston Scientific

- 10.5 ConMed

- 10.6 Cook

- 10.7 Fujifilm

- 10.8 Henke-Sass Wolf

- 10.9 Olympus

- 10.10 PENTAX Medical

- 10.11 Richard Wolf

- 10.12 Scholly Fiberoptic

- 10.13 Smith & Nephew

- 10.14 Storz

- 10.15 Stryker

- 10.16 XION medical

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日