スマートリングメインユニット市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Smart Ring Main Unit Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 157 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801937

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

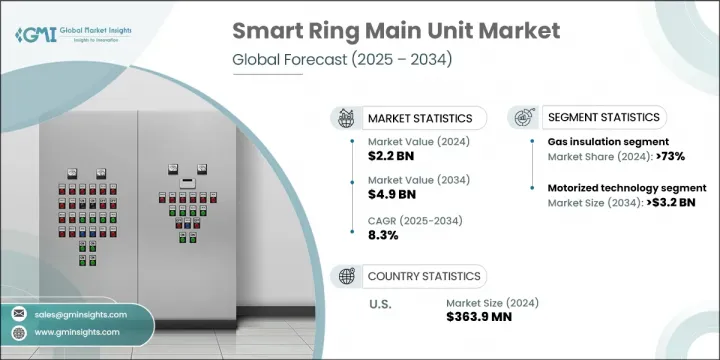

スマートリングメインユニットの世界市場規模は、2024年に22億米ドルとなり、CAGR 8.3%で成長し、2034年には49億米ドルに達すると予測されています。

信頼性が高く自動化された中高圧配電システム、特に都市環境における需要の高まりにより、市場は勢いを増しています。送電網の近代化への投資の増加、再生可能エネルギーの統合の増加、電気網の複雑化などが需要を後押ししています。スマートRMUは、故障検出機能、遠隔スイッチング機能、リアルタイムデータ分析機能を強化し、最新のグリッドインフラにとって不可欠なものとなっています。エネルギー効率を高め、停電時間を最小化する取り組みが、電力事業者にこうしたインテリジェント・システムの大規模導入を促しています。環境規制とスマートシティ構想は、省スペースで自動化された環境に優しいスイッチギヤの必要性を強化し、採用をさらに後押ししています。

2024年には、ガス絶縁セグメントが73%以上のシェアで市場をリードしています。その主な理由は、コンパクトな設計、最小限のメンテナンス、制約のあるスペースでの信頼性です。温室効果ガス排出削減への規制圧力が高まる中、メーカーは環境への影響を抑えながら絶縁品質を維持するフルオロニトリルベースのガスなど、SF6を使用しない代替品の開発を進めています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 22億米ドル |

| 予測金額 | 49億米ドル |

| CAGR | 8.3% |

電動スマートRMUは2024年に61%のシェアを占め、2034年には32億米ドルに達すると予測されています。SCADAシステムやIoTプラットフォームとの統合により、ユーティリティ企業はリアルタイムの診断、遠隔故障切り分け、自動負荷管理を行うことができ、産業ハブ、スマートグリッドシステム、再生可能エネルギーパークに理想的です。これらの先進的なRMUにより、系統運用者は手動介入を回避し、停電時間を大幅に短縮し、動的な系統環境における運用制御を強化することができます。

米国のスマートリングメインユニット市場規模は2024年に3億6,390万米ドル、シェアは68.7%となりました。送電網の近代化を目的とした連邦政府のプログラムが、この成長の主な原動力となっています。スマートRMUは、気候変動への耐性を高め、中電圧システムを自動化し、進化する都市インフラをサポートするために採用されています。遠隔操作性、故障管理、リアルタイム・モニタリングへの投資により、これらのユニットは大都市圏や工業地帯のグリッド変革課題に不可欠なものとなっています。

世界のスマートリングメインユニット市場を形成している主要企業には、イートン、ルーシーエレクトリック、ABB、シーメンス、シュナイダーエレクトリックなどがあります。スマートリングメインユニット市場における地位を強化するため、主要企業は先進的な製品開発と持続可能性に焦点を当てた戦略を追求しています。これには、SF6フリーのガス絶縁技術の革新や、AIを活用した予知保全機能の統合などが含まれます。ユーティリティ・プロバイダーやスマートシティ・プランナーとの協業は、都市送電網全体での展開拡大に役立っています。各社はまた、デジタルツイン技術、サイバーセキュリティの強化、SCADA互換プラットフォームにも投資し、完全に統合されたソリューションを提供しています。現地生産による世界展開、強固なアフターセールス・サポート、地域プレーヤーの買収は、市場浸透を促進するさらなる戦術です。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 規制情勢

- サプライチェーンのレジリエンスとリスク評価

- 原材料調達の課題

- 製造能力分析

- 物流・配送ネットワーク

- 地政学的リスク要因

- 輸入輸出貿易分析

- 主要輸入国

- 主要輸出国

- 価格動向分析(USD/単位)

- 技術別

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーターの分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 戦略的ダッシュボード

- 戦略的取り組み

- 競合ベンチマーキング

- イノベーションとテクノロジーの情勢

第5章 市場規模・予測:断熱材別、2021年~2034年

- 主要動向

- ガス

- 空気

- 油

- 固体誘電体

- その他

第6章 市場規模・予測:ポジション別、2021年~2034年

- 主要動向

- 2-3-4ポジション

- 5-6ポジション

- 7-10ポジション

- その他

第7章 市場規模・予測:技術別、2021年~2034年

- 主要動向

- 電動RMU

- 非電動RMU

第8章 市場規模・予測:設備別、2021年~2034年

- 主要動向

- 屋内

- 屋外

第9章 市場規模・予測:コンポーネント別、2021年~2034年

- 主要動向

- スイッチとヒューズ

- 自己駆動型電子リレー

- 伝達可能性

- 従来のCT/VTセンサー

- 低電力CT/VTセンサー

- 非伝達可能性

- 伝達可能性

- オートメーションRTU

- UPS

- 故障箇所表示/短絡表示

- 伝達可能性

- 従来のCT/VTセンサー

- 従来のCT/VTセンサー

- 非伝達可能性

- 伝達可能性

- VDIS

第10章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 配電設備

- 電動RMU

- 非電動RMU

- 産業

- インフラストラクチャー

- 電動RMU

- 非電動RMU

- 輸送機関

- その他

第11章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- イタリア

- スペイン

- フランス

- スウェーデン

- ギリシャ

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- クウェート

- 南アフリカ

- カタール

- ラテンアメリカ

- ブラジル

- アルゼンチン

第12章 企業プロファイル

- ABB

- alfanar

- Bonomi Eugenio

- CG Power

- CHINT

- C-Sec

- Eaton

- Electric &Electronic

- Eswari Electricals

- HD HYUNDAI ELECTRIC

- Holley Technology

- LS ELECTRIC

- Lucy Group

- Orecco

- Rockwill

- Schneider Electric

- Siemens

- TIEPCO

- Toshiba Energy

- Zhejiang Volcano

目次

The Global Smart Ring Main Unit Market was valued at USD 2.2 billion in 2024 and is estimated to grow at a CAGR of 8.3% to reach USD 4.9 billion by 2034. The market is gaining momentum due to rising demand for reliable and automated medium-voltage distribution systems, especially in urban environments. Growing investments in grid modernization, increased integration of renewables, and the rising complexity of electrical networks are all fueling demand. Smart RMUs offer enhanced fault detection, remote switching, and real-time data analysis, which makes them critical for modern grid infrastructure. Initiatives to enhance energy efficiency and minimize outage durations are prompting utility providers to adopt these intelligent systems at scale. Environmental regulations and smart city initiatives further boost adoption by reinforcing the need for space-saving, automated, and environmentally friendly switchgear.

The gas-insulated segment led the market in 2024 with over 73% share, largely due to its compact design, minimal maintenance, and reliability in constrained spaces. With increasing regulatory pressure to reduce greenhouse gas emissions, manufacturers are developing SF6-free alternatives like fluoronitrile-based gases that preserve insulation quality while reducing environmental impact.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.2 Billion |

| Forecast Value | $4.9 Billion |

| CAGR | 8.3% |

The Motorized smart RMUs held a 61% share in 2024 and is projected to reach USD 3.2 billion by 2034. Their integration with SCADA systems and IoT platforms enables utilities to perform real-time diagnostics, remote fault isolation, and automated load management, making them ideal for industrial hubs, smart grid systems, and renewable parks. These advanced RMUs allow grid operators to avoid manual intervention, significantly reducing outage durations and enhancing operational control in dynamic grid environments.

United States Smart Ring Main Unit Market generated USD 363.9 million in 2024, with a 68.7% share. Federal programs aimed at modernizing the electrical grid are the primary drivers of this growth. Smart RMUs are adopted to improve climate resilience, automate medium-voltage systems, and support evolving urban infrastructures. Investments in remote operability, fault management, and real-time monitoring have made these units an essential part of the grid transformation agenda across major metropolitan and industrial regions.

Key players shaping this Global Smart Ring Main Unit Market include Eaton, Lucy Electric, ABB, Siemens, and Schneider Electric. To strengthen their position in the smart ring main unit market, leading companies are pursuing strategies focused on advanced product development and sustainability. These include innovating SF6-free gas insulation technologies and integrating AI-powered predictive maintenance features. Collaborations with utility providers and smart city planners help expand deployment across urban grids. Companies are also investing in digital twin technologies, cybersecurity enhancements, and SCADA-compatible platforms to offer fully integrated solutions. Global expansion through localized manufacturing, robust after-sales support, and acquisitions of regional players are additional tactics driving market penetration.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data Collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculations

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

- 2.1.1 Business trends

- 2.1.2 Insulation trends

- 2.1.3 Position trends

- 2.1.4 Technology trends

- 2.1.5 Installation trends

- 2.1.6 Component trends

- 2.1.7 Application trends

- 2.1.8 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Supply chain resilience and risk assessment

- 3.3.1 Raw material sourcing challenges

- 3.3.2 Manufacturing capacity analysis

- 3.3.3 Logistics and distribution networks

- 3.3.4 Geopolitical risk factors

- 3.4 Import export trade analysis

- 3.4.1 Key importing countries

- 3.4.2 Key exporting countries

- 3.5 Price trend analysis, (USD/Unit)

- 3.5.1 By technology

- 3.6 Industry impact forces

- 3.6.1 Growth drivers

- 3.6.2 Industry pitfalls & challenges

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.8.1 Bargaining power of suppliers

- 3.8.2 Bargaining power of buyers

- 3.8.3 Threat of new entrants

- 3.8.4 Threat of substitutes

- 3.9 PESTEL analysis

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Competitive benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Insulation, 2021 - 2034 (‘000 Units & USD Million)

- 5.1 Key trends

- 5.2 Gas

- 5.3 Air

- 5.4 Oil

- 5.5 Solid-Di-Electric

- 5.6 Others

Chapter 6 Market Size and Forecast, By Position, 2021 - 2034 (‘000 Units & USD Million)

- 6.1 Key trends

- 6.2 2-3-4 Position

- 6.3 5-6 Position

- 6.4 7-10 Position

- 6.5 Others

Chapter 7 Market Size and Forecast, By Technology, 2021 - 2034 (‘000 Units & USD Million)

- 7.1 Key trends

- 7.2 Motorized RMU

- 7.3 Non - motorized RMU

Chapter 8 Market Size and Forecast, By Installation, 2021 - 2034 (‘000 Units & USD Million)

- 8.1 Key trends

- 8.2 Indoor

- 8.3 Outdoor

Chapter 9 Market Size and Forecast, By Component, 2021 - 2034 (USD Million)

- 9.1 Key trends

- 9.2 Switch & Fuses

- 9.3 Self-Powered Electronic Relay

- 9.3.1 Communicable

- 9.3.1.1 Conventional CT/VT Sensors

- 9.3.1.2 Low Power CT/VT Sensors

- 9.3.2 Non-Communicable

- 9.3.1 Communicable

- 9.4 Automations RTU’s

- 9.5 UPS

- 9.6 Fault Passage Indicators/Short Circuit Indicators

- 9.6.1 Communicable

- 9.6.1.1 Conventional CT/VT Sensors

- 9.6.1.2 Conventional CT/VT Sensors

- 9.6.2 Non-Communicable

- 9.6.1 Communicable

- 9.7 VDIS

Chapter 10 Market Size and Forecast, By Application, 2021 - 2034 (‘000 Units & USD Million)

- 10.1 Key trends

- 10.2 Distribution Utilities

- 10.2.1 Motorized RMU

- 10.2.2 Non - Motorized RMU

- 10.3 Industries

- 10.4 Infrastructure

- 10.4.1 Motorized RMU

- 10.4.2 Non - Motorized RMU

- 10.5 Transportation

- 10.6 Others

Chapter 11 Market Size and Forecast, By Region, 2021 - 2032 (‘000 Units & USD Million)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.2.3 Mexico

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 Italy

- 11.3.3 Spain

- 11.3.4 France

- 11.3.5 Sweden

- 11.3.6 Greece

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Middle East & Africa

- 11.5.1 Saudi Arabia

- 11.5.2 UAE

- 11.5.3 Kuwait

- 11.5.4 South Africa

- 11.5.5 Qatar

- 11.6 Latin America

- 11.6.1 Brazil

- 11.6.2 Argentina

Chapter 12 Company Profiles

- 12.1 ABB

- 12.2 alfanar

- 12.3 Bonomi Eugenio

- 12.4 CG Power

- 12.5 CHINT

- 12.6 C-Sec

- 12.7 Eaton

- 12.8 Electric & Electronic

- 12.9 Eswari Electricals

- 12.10 HD HYUNDAI ELECTRIC

- 12.11 Holley Technology

- 12.12 LS ELECTRIC

- 12.13 Lucy Group

- 12.14 Orecco

- 12.15 Rockwill

- 12.16 Schneider Electric

- 12.17 Siemens

- 12.18 TIEPCO

- 12.19 Toshiba Energy

- 12.20 Zhejiang Volcano

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 157 Pages

- 納期

- 2~3営業日