データセンターアウトソーシング市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Data Center Outsourcing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 310 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801928

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

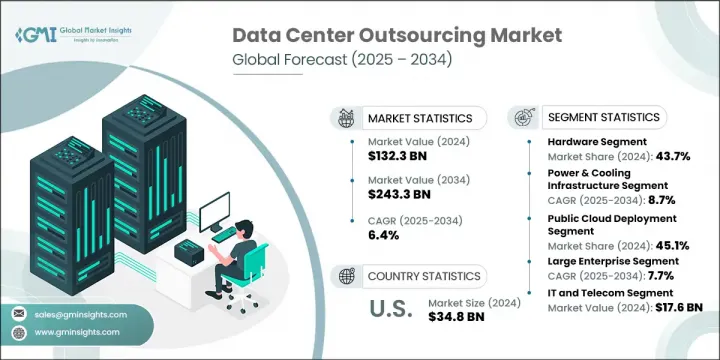

データセンターアウトソーシングの世界市場規模は、2024年に1,323億米ドルとなり、CAGR 6.4%で成長し、2034年には2,433億米ドルに達すると予測されています。

データセンターアウトソーシングに対する需要は、企業が柔軟で安全なインフラストラクチャソリューションをますます追求するようになるにつれて増加の一途をたどっています。企業は、プライベート・クラウドのコントロールとパブリック・クラウド・サービスの俊敏性を組み合わせたハイブリッド・クラウド戦略を採用しています。このアプローチにより、企業は重要なデータの監視を強化しながら、業務を拡大することができます。アウトソーシング・プロバイダーは現在、プライベート環境とパブリック環境の両方にまたがる統合ソリューションを提供し、パフォーマンスとコスト管理を同時に最適化しています。

5G、IoT、リアルタイム・アプリケーションなどの新たなテクノロジーが勢いを増す中、企業はデータ生成源での高速処理を実現するエッジ・コンピューティングに注目しています。このため、小規模で分散化された施設をエンドユーザーの近くに配置する、より分散型のアウトソーシング・モデルへのシフトが進んでいます。米国では、マイクロソフト・アジュール、グーグル・クラウド、AWS、IBMなどのハイパースケール・オペレーターが、巨額の先行投資なしに企業を大規模にサポートする巨大なインフラとキャパシティで、アウトソーシングの動きをリードしています。一方、HIPAA、FINRA、CCPAといったデータ・プライバシーの枠組みがアウトソーシング需要を形成しており、企業は認定施設、強固なコンプライアンス・サポート、地域規制との整合性を提供するプロバイダーとの提携を推進しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 1,323億米ドル |

| 予測金額 | 2,433億米ドル |

| CAGR | 6.4% |

ハードウェア分野は2024年に43.7%のシェアを獲得し、2034年までのCAGRは6.4%と予測されます。データ量の増加とテクノロジーの進化に伴い、企業は資本支出を削減し、運用コストモデルを採用するために、ハードウェア管理のアウトソーシングを選択するようになっています。社内でインフラのアップグレードを管理するのはコストと時間がかかるため、ハードウェア・サービスのアウトソーシングがスケーラビリティと俊敏性の面で好まれるようになっています。

電力・冷却インフラ分野は、2025年から2034年にかけてCAGR 8.7%を記録すると予想されています。アウトソーシング・プロバイダーは、高性能コンピューティング環境をサポートするために高度なエネルギー管理ソリューションを導入しています。AIベースの温度制御、液冷、フリークーリングなどの技術が採用され、高密度のワークロードによって発生する熱を処理すると同時に、エネルギー消費を削減し、システムの信頼性を高めています。

米国データセンターアウトソーシング市場は2024年に76.1%のシェアを占め、348億米ドルを創出。米国は、エクイニクス、アマゾン・ウェブ・サービス(AWS)、ベライゾン・コミュニケーションズ、グーグル・クラウドといった大手プロバイダーの存在により、データセンターの世界のハブであり続けています。規制の枠組みが複雑化するにつれ、企業は、進化するデータプライバシー法に対応できるコンプライアンス資格とインフラを備えたサードパーティパートナーをますます求めるようになっています。カナダの企業市場もまた、スピード、イノベーション、クロスプラットフォーム・オーケストレーションを優先し、クラウド主導のアウトソーシング・モデルへと移行しつつあります。ハイブリッドクラウドやマルチクラウドに強いプロバイダーは、カナダ全土で人気を集めています。

世界のデータセンターアウトソーシング市場で事業を展開する主要企業には、コグニザント、タタ・コンサルタンシー・サービシズ(TCS)、富士通、アクセンチュア、アマゾンウェブサービス(AWS)、グーグルクラウド、マイクロソフトアジュール、エクイニクス、ベライゾン・コミュニケーションズ、デジタルリアルティなどがあります。競争の激しいデータセンターアウトソーシング空間での地位を強化するため、各社は世界インフラの拡大、エッジコンピューティングソリューションの統合、ハイブリッドおよびマルチクラウド管理プラットフォームの提供に注力しています。データ管理、エネルギー最適化、リアルタイム監視のためのAIベースの自動化に戦略的投資が行われています。プロバイダーはまた、ハイパースケールクラウドベンダーと提携し、進化する地域規制へのコンプライアンスを確保しつつ、拡張性の高いサービスを共同で提供しようとしています。柔軟なサービスモデル、費用対効果の高いIaaS(Infrastructure-as-a-Service)、ヘルスケアや金融など業界特有のコンプライアンスに対応した専用サポートの提供が重視されています。

目次

第1章 調査手法

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 利益率分析

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- バリューチェーン分析

- データセンターインフラプロバイダー

- マネージドサービスプロバイダー

- クラウドサービスプロバイダー

- システムインテグレーターとコンサルタント

- エンドユーザー組織

- 業界への影響要因

- 促進要因

- クラウド導入の増加

- コスト効率

- コアビジネスに注力

- 高度なセキュリティ要件

- 業界の潜在的リスク&課題

- データプライバシーに関する懸念

- サービスプロバイダーへの依存

- 初期移行コストが高め

- 統合の複雑さ

- 市場機会

- エッジコンピューティングの拡大

- グリーンデータセンターの取り組み

- IoTと5G技術の成長

- 規制遵守のニーズの高まり

- 促進要因

- 成長可能性分析

- 価格モデルとコスト構造分析

- コロケーション料金体系

- マネージドサービスの価格モデル

- クラウドサービスのコスト構造

- 総所有コスト(TCO)分析

- 設備投資と運用コストの意思意思決定の枠組み

- サービスレベル契約(SLA)とパフォーマンス指標

- 稼働時間と可用性の基準

- パフォーマンスベンチマーク

- セキュリティとコンプライアンスの要件

- 災害復旧と事業継続

- サポートおよびメンテナンス基準

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- データセンターの容量分析と需給動向

- 世界容量概要

- 供給側分析

- 需要側分析

- キャパシティプランニングと予測

- 能力投資と資金調達

- 電力使用効率(PUE)分析とベンチマーク

- PUEの基礎と業界標準

- 世界PUEパフォーマンス分析

- PUE最適化戦略とテクノロジー

- 電力分配効率

- IT機器の効率

- AI駆動型PUE最適化

- PUEがビジネス上の意思決定に与える影響

- エネルギー効率技術と最適化戦略

- 高度な冷却技術

- 電力管理と配電効率

- ITインフラストラクチャの効率

- 監視および管理システム

- エネルギー効率のROIとビジネスケース

- 戦略シナリオとベストケース分析

- 包括的なケーススタディと成功事例

- テクノロジーとイノベーションの情勢

- 現在の技術分析

- 新興技術の動向

- 特許分析

- 持続可能性と環境戦略

- 環境影響評価

- グリーンデータセンター技術とソリューション

- 持続可能なインフラ設計

- 環境規制とコンプライアンス

- 企業の持続可能性戦略

- 持続可能性の経済的利益

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ハードウェア

- ソフトウェア

- サービス

第6章 市場推計・予測:物理インフラストラクチャ別、2021年~2034年

- 主要動向

- データセンター施設

- 電力および冷却インフラストラクチャ

- ラックとキャビネット

- ケーブル配線

- その他

第7章 市場推計・予測:展開モデル別、2021年~2034年

- 主要動向

- パブリッククラウドの展開

- プライベートクラウドの展開

- ハイブリッドクラウドの展開

- コミュニティクラウドの展開

- マルチクラウド展開

第8章 市場推計・予測:組織規模別、2021年~2034年

- 主要動向

- 中小企業

- 大企業

- 政府および公共部門

第9章 市場推計・予測:業種別、2021年~2034年

- 主要動向

- BFSI

- ITおよび通信

- ヘルスケアとライフサイエンス

- 政府および公共部門

- 製造業および工業

- 小売業とeコマース

- その他の産業

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ポーランド

- 北欧諸国

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- シンガポール

- インドネシア

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- アルゼンチン

- メキシコ

- チリ

- コロンビア

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- 世界のリーダー

- Accenture

- AWS

- Cognizant

- Digital Realty

- Equinix

- Google Cloud

- Hewlett Packard Enterprise(HPE)

- IBM

- Microsoft Azure

- NTT

- Tata Consultancy Services(TCS)

- 地域企業

- CyrusOne

- Fujitsu

- Interxion

- Iron Mountain

- Kyndryl

- Lumen Technologies

- Rackspace Technology

- Schneider Electric

- 新興企業

- AT&T

- Verizon Communications

目次

The Global Data Center Outsourcing Market was valued at USD 132.3 billion in 2024 and is estimated to grow at a CAGR of 6.4% to reach USD 243.3 billion by 2034. The demand for data center outsourcing continues to rise as businesses increasingly pursue flexible and secure infrastructure solutions. Organizations are embracing hybrid cloud strategies that combine the control of private clouds with the agility of public cloud services. This approach enables companies to scale operations while maintaining tighter oversight of critical data. Outsourcing providers are now offering integrated solutions that span both private and public environments, optimizing performance and cost management simultaneously.

As emerging technologies such as 5G, IoT, and real-time applications gain momentum, enterprises are turning to edge computing for faster processing at the source of data generation. This has led to a shift toward more distributed outsourcing models, where smaller, decentralized facilities are placed closer to end users. In the US, hyperscale operators, including Microsoft Azure, Google Cloud, AWS, and IBM, are leading the outsourcing movement with their massive infrastructure and capacity to support enterprises at scale without hefty upfront investments. Meanwhile, data privacy frameworks such as HIPAA, FINRA, and CCPA are shaping outsourcing demand, driving businesses to work with providers who offer certified facilities, robust compliance support, and regional regulatory alignment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $132.3 Billion |

| Forecast Value | $243.3 Billion |

| CAGR | 6.4% |

The hardware segment captured 43.7% share in 2024 and is projected to grow at a CAGR of 6.4% through 2034. With rising data volumes and evolving technologies, organizations are opting to outsource hardware management to cut capital expenses and adopt an operating cost model. Managing in-house infrastructure upgrades proves cost-intensive and time-consuming, which is why outsourcing hardware services has become a preferred path for scalability and agility.

The power and cooling infrastructure segment is expected to register a CAGR of 8.7% from 2025 to 2034. Outsourcing providers are introducing advanced energy management solutions to support high-performance computing environments. Technologies such as AI-based temperature control, liquid cooling, and free cooling are being adopted to handle heat generated by dense workloads while also reducing energy consumption and enhancing system reliability.

United States Data Center Outsourcing Market held a 76.1% share in 2024, generating USD 34.8 billion. The US remains a global hub for data centers, driven by the presence of major providers such as Equinix, Amazon Web Services (AWS), Verizon Communications, and Google Cloud. As regulatory frameworks become more complex, companies increasingly seek third-party partners with the compliance credentials and infrastructure to navigate evolving data privacy laws. Canada's enterprise market is also transitioning toward cloud-driven outsourcing models, prioritizing speed, innovation, and cross-platform orchestration. Providers with strong hybrid and multi-cloud capabilities are seeing increased traction across the region.

Key companies operating in the Global Data Center Outsourcing Market include Cognizant, Tata Consultancy Services (TCS), Fujitsu, Accenture, Amazon Web Services (AWS), Google Cloud, Microsoft Azure, Equinix, Verizon Communications, and Digital Realty. To strengthen their position in the competitive data center outsourcing space, companies are focusing on expanding global infrastructure, integrating edge computing solutions, and offering hybrid and multi-cloud management platforms. Strategic investments are being made in AI-based automation for data management, energy optimization, and real-time monitoring. Providers are also forming alliances with hyperscale cloud vendors to co-deliver scalable services while ensuring compliance with evolving regional regulations. Emphasis is being placed on offering flexible service models, cost-effective infrastructure-as-a-service (IaaS), and dedicated support for industry-specific compliance, like healthcare or finance.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Physical infrastructure

- 2.2.4 Deployment model

- 2.2.5 Organization Size

- 2.2.6 Industry vertical

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Profit margin analysis

- 3.1.2 Cost structure

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Value chain analysis

- 3.2.1 Data center infrastructure providers

- 3.2.2 Managed service providers

- 3.2.3 Cloud service providers

- 3.2.4 System integrators and consultants

- 3.2.5 End use organizations

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Growing cloud adoption

- 3.3.1.2 Cost efficiency

- 3.3.1.3 Focus on core business

- 3.3.1.4 Advanced security requirements

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 Data privacy concerns

- 3.3.2.2 Dependence on service providers

- 3.3.2.3 High initial transition costs

- 3.3.2.4 Complexity of integration

- 3.3.3 Market opportunities

- 3.3.3.1 Expansion of edge computing

- 3.3.3.2 Green data center initiatives

- 3.3.3.3 Growth in IoT and 5G technologies

- 3.3.3.4 Increasing regulatory compliance needs

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Pricing models and cost structure analysis

- 3.5.1 Colocation pricing framework

- 3.5.2 Managed services pricing models

- 3.5.3 Cloud services cost structures

- 3.5.4 Total cost of ownership (TCO) analysis

- 3.5.5 CapEx vs OpEx decision framework

- 3.6 Service level agreements (SLA) and performance metrics

- 3.6.1 Uptime and availability standards

- 3.6.2 Performance benchmarking

- 3.6.3 Security and compliance requirements

- 3.6.4 Disaster recovery and business continuity

- 3.6.5 Support and maintenance standards

- 3.7 Regulatory landscape

- 3.7.1 North America

- 3.7.2 Europe

- 3.7.3 Asia Pacific

- 3.7.4 LATAM

- 3.7.5 MEA

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

- 3.10 Data center capacity analysis and supply-demand dynamics

- 3.10.1 Global capacity overview

- 3.10.2 Supply-side analysis

- 3.10.3 Demand-side analysis

- 3.10.4 Capacity planning and forecasting

- 3.10.5 Capacity investment and financing

- 3.11 Power usage effectiveness (PUE) analysis and benchmarking

- 3.11.1 PUE fundamentals and industry standards

- 3.11.2 Global PUE performance analysis

- 3.11.3 PUE optimization strategies and technologies

- 3.11.4 Power distribution efficiency

- 3.11.5 IT equipment efficiency

- 3.11.6 AI-Driven PUE optimization

- 3.11.7 PUE impact on business decisions

- 3.12 Energy efficiency technologies and optimization strategies

- 3.12.1 Advanced cooling technologies

- 3.12.2 Power management and distribution efficiency

- 3.12.3 IT infrastructure efficiency

- 3.12.4 Monitoring and management systems

- 3.12.5 ROI and business case for energy efficiency

- 3.13 Strategic scenarios and best case analysis

- 3.14 Comprehensive case studies and success stories

- 3.15 Technology and innovation landscape

- 3.15.1 Current technology analysis

- 3.15.2 Emerging technology trends

- 3.16 Patent analysis

- 3.17 Sustainability and environmental strategies

- 3.17.1 Environmental impact assessment

- 3.17.2 Green data center technologies and solutions

- 3.17.3 Sustainable infrastructure design

- 3.17.4 Environmental regulations and compliance

- 3.17.5 Corporate sustainability strategies

- 3.17.6 Economic benefits of sustainability

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 (USD Mn)

- 5.1 Key trends

- 5.2 Hardware

- 5.3 Software

- 5.4 Service

Chapter 6 Market Estimates & Forecast, By Physical Infrastructure, 2021 - 2034 (USD Mn)

- 6.1 Key trends

- 6.2 Data center facilities

- 6.3 Power & cooling infrastructure

- 6.4 Racks & cabinets

- 6.5 Cabling & wiring

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Deployment Model, 2021 - 2034 (USD Mn)

- 7.1 Key trends

- 7.2 Public cloud deployment

- 7.3 Private cloud deployment

- 7.4 Hybrid cloud deployment

- 7.5 Community cloud deployment

- 7.6 Multi-cloud deployment

Chapter 8 Market Estimates & Forecast, By Organization Size, 2021 - 2034 (USD Mn)

- 8.1 Key trends

- 8.2 Small/medium enterprises

- 8.3 Large enterprises

- 8.4 Government and public sector

Chapter 9 Market Estimates & Forecast, By Industry Vertical, 2021 - 2034 (USD Mn)

- 9.1 Key trends

- 9.2 BFSI

- 9.3 IT and telecom

- 9.4 Healthcare and life sciences

- 9.5 Government and public sector

- 9.6 Manufacturing and industrial

- 9.7 Retail and e-commerce

- 9.8 Other industries

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Poland

- 10.3.7 Nordics

- 10.3.8 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Singapore

- 10.4.5 Indonesia

- 10.4.6 Australia

- 10.4.7 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Argentina

- 10.5.3 Mexico

- 10.5.4 Chile

- 10.5.5 Colombia

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Global Leaders

- 11.1.1 Accenture

- 11.1.2 AWS

- 11.1.3 Cognizant

- 11.1.4 Digital Realty

- 11.1.5 Equinix

- 11.1.6 Google Cloud

- 11.1.7 Hewlett Packard Enterprise (HPE)

- 11.1.8 IBM

- 11.1.9 Microsoft Azure

- 11.1.10 NTT

- 11.1.11 Tata Consultancy Services (TCS)

- 11.2 Regional Players

- 11.2.1 CyrusOne

- 11.2.2 Fujitsu

- 11.2.3 Interxion

- 11.2.4 Iron Mountain

- 11.2.5 Kyndryl

- 11.2.6 Lumen Technologies

- 11.2.7 Rackspace Technology

- 11.2.8 Schneider Electric

- 11.3 Emerging Players

- 11.3.1 AT&T

- 11.3.2 Verizon Communications

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 310 Pages

- 納期

- 2~3営業日