ヘンプクリート市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Hempcrete Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 235 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801921

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

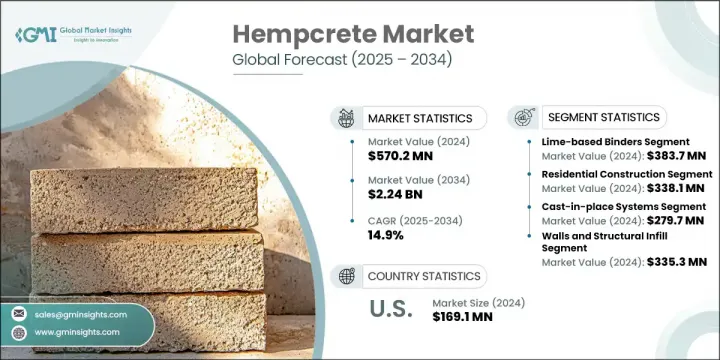

ヘンプクリートの世界市場規模は、2024年に5億7,020万米ドルとなり、CAGR 14.9%で成長し、2034年には22億4,000万米ドルに達すると予測されています。

環境への影響に対する意識が高まるにつれ、開発業者や建設業者は低排出ガスで持続可能な建設代替案への関心を高めています。ヘンプクリートは、生分解性で炭素を隔離することができるため、建築環境における二酸化炭素排出量を削減するという世界の目標に密接に合致しています。その自然な特性は、エネルギー効率の高い建物や環境に配慮した住宅設計において理想的な素材となり、環境に優しいソリューションに対する規制上の要求と消費者の期待の両方を満たすのに役立ちます。

排出量の削減とエネルギー効率の向上を推進する政府の指令は、ヘンプクリートのような天然素材への関心をさらに高めています。いくつかの国では、温室効果ガスの排出を削減するためにより厳しい規制を実施しており、熱効率の高い天然断熱材を使用する方向へのシフトを促しています。さらに、LEEDやBREEAMといった持続可能性の枠組みは、建設会社が環境に優しい素材を優先するよう影響を及ぼしており、長期的には住宅、商業施設、さらには産業部門に至るまで、ヘンプクリートの安定した需要を確保しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 5億7,020万米ドル |

| 予測金額 | 22億4,000万米ドル |

| CAGR | 14.9% |

石灰系バインダー分野は2024年に3億8,370万米ドルを生み出し、2025年から2034年にかけてCAGR 14.5%で成長すると予想されています。これらのバインダーはヘンプハードとの相性が良く、高い通気性と強力な炭素吸収性を提供します。石灰バインダーはヘンプクリートの環境に優しいイメージを支持し、認定グリーン住宅で一般的に使用されています。石灰バインダーは硬化に時間がかかり、構造強度も低いが、継続的な研究開発により、持続可能性はそのままに、より性能を重視した代替品が生まれています。

住宅建設セグメントは2024年に3億3,810万米ドルを生み出し、59.2%のシェアを獲得しました。2034年までのCAGRは14.4%と予想され、この分野はエネルギー効率の高いセルフビルド住宅、低排出構造、気候に配慮した建築動向への関心の高まりから利益を得ています。ヘンプクリートの断熱性、低毒性、CO2吸収特性は、特に北米や欧州の一部のような環境的に先進的な市場において、持続可能な住宅に適した材料となっています。

米国のヘンプクリート市場は2024年に1億6,910万米ドルとなり、2034年までCAGR 14.1%で成長すると予測されています。国内の成長を支えているのは、麻栽培に関する規制の進展、グリーンビルディング製品への需要、持続可能な建築手法の採用増加です。ヘンプクリートは、特に環境的に先進的な州における改修や新築住宅で支持を集めています。カナダの産業用大麻産業への支援は、モジュール式および住宅用アプリケーションのための強固な国境を越えた協力体制とサプライチェーンにも貢献しています。

世界のヘンプクリート市場を形成する主要企業には、Hempitecture Inc.、Cavac Biomateriaux、Hemp and Block、American Hemp LLC、HempStoneなどがあります。ヘンプクリート業界で事業を展開する企業は、市場シェアを拡大するため、バインダー性能の向上、硬化時間の短縮、構造強度の向上のための研究開発に投資しています。持続可能な建設会社や建築家との戦略的提携は、プロジェクトの認知度向上に役立っています。物流コストを削減し、製品へのアクセス性を向上させるため、多くの企業が生産能力を拡大し、地域密着型のサプライチェーンを確立しています。グリーン建築基準に関する教育キャンペーンや認証も、ヘンプクリートを従来の素材に代わる実行可能な主流として位置づけるために利用されています。このような取り組みにより、ブランドの信頼性、法規制への準拠、消費者の信頼が世界市場で高まっています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- 価格動向

- 地域別

- 製品別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な実践

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測、バインダータイプ別、2021年~2034年

- 主要動向

- 石灰系バインダー

- 水硬性石灰

- 生石

- 改質石灰配合

- セメント系バインダー

- ポートランドセメント

- 混合セメントシステム

- 低炭素セメントの代替品

- 代替バインダー

- アルカリ活性化バインダー

- セノスフィアバインダー

- ジオポリマーバインダー

- 菌糸体ベースのバインダー

- ハイブリッド製剤

- 石灰セメント混合物

- ポリマー改質システム

- 繊維強化配合

第6章 市場推計・予測:工法別、2021年~2034年

- 主要動向

- 現場打ちシステム

- 手鋳造法

- 空気圧配置

- 型枠システム

- プレキャストシステム

- ブロック製造

- パネル生産

- モジュラーコンポーネント

- スプレー塗布

- ウェットスプレーシステム

- ドライミックスアプリケーション

- ロボットスプレーシステム

- 高度な製造業

- 3Dプリント技術

- 自動化生産システム

- デジタル製造方法

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 壁と構造充填材

- 住宅用途

- 商業用途

- 産業用途

- 断熱システム

- 断熱材市場

- 防音用途

- 改修断熱ソリューション

- 屋根材と床材

- 屋根材用途

- 床システム

- 特殊なアプリケーション

- プレキャストブロックとパネル

- プレキャストブロック市場

- パネルシステム

- モジュラー建設アプリケーション

- 現場打ち用途

- 現場鋳造

- スプレー塗布

- カスタム処方

- 新興アプリケーション

- 3Dプリントアプリケーション

- 複合材料

- 特殊建設用途

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 住宅建設

- 一戸建て住宅

- 集合住宅

- 手頃な価格の住宅プロジェクト

- 改修と改築

- 商業建設

- オフィスビル

- 小売スペース

- 教育施設

- ヘルスケア施設

- 産業建設

- 製造施設

- 倉庫と配送センター

- 農業用建物

- 特殊産業用途

- インフラプロジェクト

- 公共の建物

- コミュニティセンター

- 交通インフラ

- ユーティリティビル

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東およびアフリカ

第10章 企業プロファイル

- American Hemp LLC

- Cavac Biomateriaux

- Hemp and Block

- Hemp Building Institute

- Hemp Technology Ltd.

- Hempitecture Inc.

- HempStone

- IsoHemp

- Lower Sioux Indian Community

- Rare Earth Global

- rePlant Hemp Advisors

- Sativa Building Systems

目次

The Global Hempcrete Market was valued at USD 570.2 million in 2024 and is estimated to grow at a CAGR of 14.9% to reach USD 2.24 billion by 2034. As awareness of environmental impact grows, developers and builders are increasingly turning toward low-emission, sustainable construction alternatives. Hempcrete, being biodegradable and capable of sequestering carbon, aligns closely with global goals to reduce the carbon footprint in the built environment. Its natural properties make it an ideal material in energy-efficient buildings and eco-conscious residential design, helping meet both regulatory demands and consumer expectations for greener solutions.

Government mandates pushing for lower emissions and enhanced energy efficiency are further driving interest in natural materials like hempcrete. Several countries are enforcing stricter codes to reduce greenhouse gas emissions, which has prompted a shift toward using thermally efficient and natural insulation options. In addition, sustainability frameworks such as LEED and BREEAM are influencing construction companies to prioritize eco-friendly materials, ensuring steady demand for hempcrete across residential, commercial, and even industrial sectors in the long term.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $570.2 Million |

| Forecast Value | $2.24 Billion |

| CAGR | 14.9% |

Lime-based binders segment generated USD 383.7 million in 2024 and is expected to grow at a CAGR of 14.5% from 2025 to 2034. These binders are well-aligned with hemp hurd, offering high breathability and strong carbon absorption. Lime binders uphold the environmentally friendly image of hempcrete and are commonly used in certified green housing. Though they take longer to cure and offer lower structural strength, continuous R&D has given rise to more performance-driven alternatives while keeping sustainability intact.

The residential construction segment generated USD 338.1 million in 2024 and capturing 59.2% share. With a CAGR of 14.4% anticipated through 2034, the sector benefits from rising interest in energy-efficient self-build homes, low-emission structures, and climate-conscious architectural trends. Hempcrete's thermal insulation, low toxicity, and CO2 absorbing qualities make it a favorable material for sustainable housing, particularly in environmentally progressive markets such as North America and parts of Europe.

U.S. Hempcrete Market was valued at USD 169.1 million in 2024 and is forecasted to grow at a CAGR of 14.1% through 2034. Domestic growth is supported by evolving regulations around hemp cultivation, demand for green building products, and increasing adoption of sustainable construction practices. Hempcrete has gained traction particularly in retrofitting and new housing across environmentally progressive states. Canada's support for the industrial hemp industry also contributes to robust cross-border collaborations and supply chains for modular and residential applications.

Key players shaping the Global Hempcrete Market include Hempitecture Inc., Cavac Biomateriaux, Hemp and Block, American Hemp LLC, and HempStone. To expand their market share, companies operating in the hempcrete industry are investing in research and development to enhance binder performance, speed up curing time, and improve structural strength. Strategic collaborations with sustainable construction firms and architects are helping to increase project visibility. Many are scaling their production capabilities and establishing localized supply chains to reduce logistics costs and improve product accessibility. Educational campaigns and certifications around green building standards are also used to position hempcrete as a viable mainstream alternative to traditional materials. These efforts collectively enhance brand credibility, regulatory compliance, and consumer trust across global markets.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Binder Type

- 2.2.3 Construction Method

- 2.2.4 Application

- 2.2.5 End Use

- 2.3 TAM Analysis, 2021-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, Binder Type, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Lime-based binders

- 5.2.1 Hydraulic lime

- 5.2.2 Aerial lime

- 5.2.3 Modified lime formulations

- 5.3 Cement-based binders

- 5.3.1 Portland cement

- 5.3.2 Blended cement systems

- 5.3.3 Low-carbon cement alternatives

- 5.4 Alternative binders

- 5.4.1 Alkali-activated binders

- 5.4.2 Cenosphere binders

- 5.4.3 Geopolymer binders

- 5.4.4 Mycelium-based binders

- 5.5 Hybrid formulations

- 5.5.1 Lime-cement blends

- 5.5.2 Polymer-modified systems

- 5.5.3 Fiber-reinforced formulations

Chapter 6 Market Estimates & Forecast, By Construction Method, 2021-2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Cast-in-place systems

- 6.2.1 Hand-casting methods

- 6.2.2 Pneumatic placement

- 6.2.3 Formwork systems

- 6.3 Precast systems

- 6.3.1 Block manufacturing

- 6.3.2 Panel production

- 6.3.3 Modular components

- 6.4 Spray applications

- 6.4.1 Wet spray systems

- 6.4.2 Dry mix applications

- 6.4.3 Robotic spray systems

- 6.5 Advanced manufacturing

- 6.5.1 3d printing technology

- 6.5.2 Automated production systems

- 6.6 Digital fabrication methods

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Walls and structural infill

- 7.2.1 Residential applications

- 7.2.2 Commercial applications

- 7.2.3 Industrial applications

- 7.3 Insulation systems

- 7.3.1 Thermal insulation market

- 7.3.2 Acoustic insulation applications

- 7.3.3 Retrofit insulation solutions

- 7.4 Roofing and flooring

- 7.4.1 Roofing applications

- 7.4.2 Flooring systems

- 7.4.3 Specialty applications

- 7.5 Precast blocks and panels

- 7.5.1 Precast block market

- 7.5.2 Panel systems

- 7.5.3 Modular construction applications

- 7.6 Cast-in-place applications

- 7.6.1 On-site casting

- 7.6.2 Spray applications

- 7.6.3 Custom formulations

- 7.7 Emerging applications

- 7.7.1 3d printing applications

- 7.7.2 Composite materials

- 7.7.3 Specialty construction uses

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Residential construction

- 8.2.1 Single-family homes

- 8.2.2 Multi-family housing

- 8.2.3 Affordable housing projects

- 8.2.4 Retrofit and renovation

- 8.3 Commercial construction

- 8.3.1 Office buildings

- 8.3.2 Retail spaces

- 8.3.3 Educational facilities

- 8.3.4 Healthcare facilities

- 8.4 Industrial construction

- 8.4.1 Manufacturing facilities

- 8.4.2 Warehouses and distribution centers

- 8.4.3 Agricultural buildings

- 8.4.4 Specialty industrial applications

- 8.5 Infrastructure projects

- 8.5.1 Public buildings

- 8.5.2 Community centers

- 8.5.3 Transportation infrastructure

- 8.5.4 Utility buildings

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East & Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East & Africa

Chapter 10 Company Profiles

- 10.1 American Hemp LLC

- 10.2 Cavac Biomateriaux

- 10.3 Hemp and Block

- 10.4 Hemp Building Institute

- 10.5 Hemp Technology Ltd.

- 10.6 Hempitecture Inc.

- 10.7 HempStone

- 10.8 IsoHemp

- 10.9 Lower Sioux Indian Community

- 10.10 Rare Earth Global

- 10.11 rePlant Hemp Advisors

- 10.12 Sativa Building Systems

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 235 Pages

- 納期

- 2~3営業日