HVDCケーブルの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

HVDC Cables Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 151 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801920

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

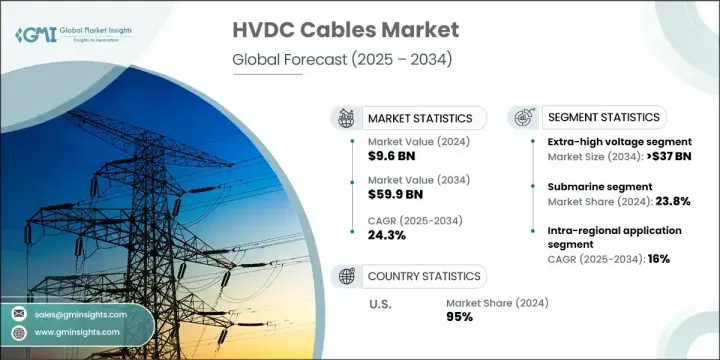

世界のHVDCケーブル市場は、2024年には96億米ドルとなり、CAGR24.3%で成長し、2034年までには599億米ドルに達すると推定されています。

この例外的な成長は、持続可能なエネルギーインフラを求める世界の動きによって後押しされています。政府やエネルギー供給会社が再生可能エネルギー源の送電網への統合に注力する中、HVDCケーブルシステムは効率的な長距離送電のための重要なツールとして台頭しています。エネルギー損失を最小限に抑え、広大な地域で安定した送電を行うことができるHVDCケーブルは、最新の低炭素電力ネットワークでますます採用されるようになっています。脱炭素エネルギーへの移行は送電戦略を再構築し、高度なHVDC技術への投資を後押ししています。

この需要を加速している主な要因は、洋上風力発電所の開発が続いていることです。風力発電プロジェクトがより沖合に進み、タービン容量が増加するにつれて、耐久性が高く高性能な送電システムへのニーズが高まっています。HVDCケーブルは、これらの洋上施設から陸上の送電網に電気を送るための主要なソリューションになりつつあります。さらに、各国が国境を越えたリンクを通じて電力を共有することでエネルギー安全保障を強化しようとしているため、相互接続や国境を越えた送電網の取り組みが活発化しています。エネルギーの流れを正確に管理できるHVDC技術は、こうした送電網プロジェクトに欠かせないものとなっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 96億米ドル |

| 予測金額 | 599億米ドル |

| CAGR | 24.3% |

35 kWから475 kWのセグメントは、エネルギー接続と大容量インフラへの世界の注目が高まるにつれて、2034年までCAGR23%で成長すると予測されます。電圧範囲が35 kWから475 kWの市場は、一括送電における重要な役割のため、より広く採用されるようになってきています。これらのケーブルは、水力発電所や洋上風力プラットフォームなど、遠隔地にある大規模な再生可能エネルギー源からの送電に最適です。

地下セグメントは、複雑な地形や都市の拡張地帯に適合するため、2034年までにCAGR16%で成長すると予想されています。地下のHVDCケーブルは、都市部や工業地帯が省スペースで低負荷の送電システムを優先するため、需要が増加すると見ています。これらのシステムは、混雑した場所や環境に敏感な場所において、架空送電線に代わる実用的な選択肢を提供します。

アジア太平洋のHVDCケーブル市場は2034年までに80億米ドルに達します。都市開発の進展、エネルギー需要の増加、再生可能エネルギーの統合が、この地域市場を形成する主な促進要因のひとつです。中国は、超高圧HVDCインフラへの戦略的投資によって国の送電網の効率を高め、再生可能エネルギー発電の豊富な地域と電力消費の多い地域との間でバランスの取れたエネルギー配分を確保することで主導権を握っています。

世界のHVDCケーブル市場を形成している主な企業には、Gupta Power Infrastructure Limited、Prysmian Group、TELE-FONIKA Kable S.A.、Brugg Kabel AG、Nexans、ILJIN ELECTRIC、ZMS CABLE、Riyadh Cables、ZTT、Elcowire GROUP AB、Furukawa Electric、NKT A/S、Tratos、Mitsubishi Electric Corporation、Sumitomo Electric Industries, Ltd.、LS Cable &System Ltd.、Hitachi Energy Ltd.、Qingdao Hanhe Cable Co., Ltd.、Alfanar Group、Taihan Cable &Solution Co., Ltd.などです。

HVDCケーブル市場で事業を展開する企業は、海上、地下、超長距離用途に合わせた先進的な大容量ケーブルソリューションを開発するため、研究開発に多額の投資を行い、その地位を強化しています。いくつかの企業は、大規模送電プロジェクトを確保するために、エネルギー事業者やEPC企業と戦略的パートナーシップを結んでいます。また、カスタマイズされたケーブルシステムの需要増に対応するため、製造能力を拡大し、製造技術をアップグレードしている企業もあります。競争力を維持するため、主要ベンダーはカーボンフットプリントを削減し、リサイクル可能な材料を使用したケーブルを製造することで、持続可能性に注力しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- 規制情勢

- 業界への影響要因

- 成長促進要因

- 業界の潜在的リスク・課題

- 価格動向分析(USD/km)

- インストール別

- 地域別

- 成長可能性分析

- ポーターの分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析:地域別

- 北米

- 欧州

- アジア太平洋

- 戦略的取り組み

- 競合ベンチマーキング

- 戦略的ダッシュボード

- イノベーションとテクノロジーの情勢

第5章 市場規模・予測:電圧別、2021年~2034年

- 主要動向

- 高(35 kV~475 kV)

- 超高(475 kV~600 kV)

- 超高圧(600 kV以上)

第6章 市場規模・予測:設備別、2021年~2034年

- 主要動向

- 架空

- 海底

- 地下

第7章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 域内

- 越境

- その他

第8章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- イタリア

- デンマーク

- ノルウェー

- アジア太平洋

- 中国

- 日本

- インド

- タイ

- インドネシア

- 世界のその他の地域

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ブラジル

第9章 企業プロファイル

- Alfanar Group

- Brugg Kabel AG

- Elcowire GROUP AB

- Furukawa Electric

- Gupta Power Infrastructure Limited

- Hitachi Energy Ltd.

- ILJIN ELECTRIC

- LS Cable &System Ltd.

- Mitsubishi Electric Corporation

- Nexans

- NKT A/S

- Prysmian Group

- Qingdao Hanhe Cable Co., Ltd.

- Sumitomo Electric Industries, Ltd.

- Riyadh Cables

- Taihan Cable &Solution Co., Ltd.

- TELE-FONIKA Kable S.A.

- Tratos

- ZMS CABLE

- ZTT

目次

The Global HVDC Cables Market was valued at USD 9.6 billion in 2024 and is estimated to grow at a CAGR of 24.3% to reach USD 59.9 billion by 2034. This exceptional growth is being fueled by a worldwide push for sustainable energy infrastructure. As governments and energy providers focus on integrating renewable sources into the grid, HVDC cable systems are emerging as critical tools for efficient, long-distance power transmission. With the ability to minimize energy loss and offer stable transmission across vast areas, these cables are increasingly adopted in modern, low-carbon electricity networks. The transition toward decarbonized energy is reshaping power transmission strategies, boosting investments in advanced HVDC technology.

A major factor accelerating this demand is the continued development of offshore wind farms. As wind projects move farther offshore and turbine capacities increase, the need for durable and high-performance power delivery systems has intensified. HVDC cables are becoming the go-to solution for transmitting electricity from these offshore facilities to onshore grids. Additionally, interconnection and cross-border grid initiatives are gaining traction as countries seek to enhance energy security by sharing electricity via transnational links. HVDC technology's ability to manage energy flow precisely makes it indispensable in these grid projects.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.6 Billion |

| Forecast Value | $59.9 Billion |

| CAGR | 24.3% |

The 35 kW to 475 kW segment is forecast to grow at a CAGR of 23% through 2034, as the global focus on energy connectivity and high-capacity infrastructure grows stronger. The market with voltage ranges from 35 kW to 475 kW are becoming more widely adopted due to their critical role in bulk power transmission. These cables are ideal for transferring electricity from large renewable sources located in remote areas, including hydropower stations and offshore wind platforms.

The underground segment is expected to grow at a CAGR of 16% by 2034, due to its compatibility with complex terrains and urban expansion zones. The underground HVDC cables see increased demand as urban and industrial regions prioritize space-saving, low-impact power transmission systems. These systems offer practical alternatives to overhead lines in congested or environmentally sensitive locations.

Asia Pacific HVDC Cables Market will reach USD 8 billion by 2034. Rising urban development, higher energy demands, and renewable energy integration are among the major drivers shaping this regional market. China leads the charge with strategic investments in ultra-high-voltage HVDC infrastructure to enhance national grid efficiency and ensure balanced energy distribution between areas rich in renewable generation and those with elevated electricity consumption.

Key companies shaping the Global HVDC Cables Market include Gupta Power Infrastructure Limited, Prysmian Group, TELE-FONIKA Kable S.A., Brugg Kabel AG, Nexans, ILJIN ELECTRIC, ZMS CABLE, Riyadh Cables, ZTT, Elcowire GROUP AB, Furukawa Electric, NKT A/S, Tratos, Mitsubishi Electric Corporation, Sumitomo Electric Industries, Ltd., LS Cable & System Ltd., Hitachi Energy Ltd., Qingdao Hanhe Cable Co., Ltd., Alfanar Group, and Taihan Cable & Solution Co., Ltd.

Companies operating in the HVDC Cables Market are strengthening their positions by investing heavily in R&D to develop advanced, high-capacity cable solutions tailored for offshore, underground, and ultra-long-distance applications. Several players are entering strategic partnerships with energy utilities and EPC firms to secure large-scale transmission projects. Some firms are also expanding their manufacturing capacities and upgrading production technologies to support the growing demand for customized cable systems. To stay competitive, key vendors are focusing on sustainability by producing cables with reduced carbon footprints and recyclable materials.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Price trend analysis (USD/km)

- 3.4.1 By installation

- 3.4.2 By region

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

- 3.7.1 Political factors

- 3.7.2 Economic factors

- 3.7.3 Social factors

- 3.7.4 Technology factors

- 3.7.5 environmental factors

- 3.7.6 Legal factors

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Strategic initiative

- 4.4 Competitive benchmarking

- 4.5 Strategic dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Voltage, 2021 - 2034 (km, USD Billion)

- 5.1 Key trends

- 5.2 High (35 kV to 475 kV)

- 5.3 Extra high (> 475 kV to 600 kV)

- 5.4 Ultra-high (> 600 kV)

Chapter 6 Market Size and Forecast, By Installation, 2021 - 2034 (km, USD Billion)

- 6.1 Key trends

- 6.2 Overhead

- 6.3 Submarine

- 6.4 Underground

Chapter 7 Market Size and Forecast, By Application, 2021 - 2034 (km, USD Billion)

- 7.1 Key trends

- 7.2 Intra-regional

- 7.3 Cross border

- 7.4 Others

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (km, USD Billion)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 Italy

- 8.3.4 Denmark

- 8.3.5 Norway

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Thailand

- 8.4.5 Indonesia

- 8.5 Rest of the World

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 South Africa

- 8.5.4 Brazil

Chapter 9 Company Profiles

- 9.1 Alfanar Group

- 9.2 Brugg Kabel AG

- 9.3 Elcowire GROUP AB

- 9.4 Furukawa Electric

- 9.5 Gupta Power Infrastructure Limited

- 9.6 Hitachi Energy Ltd.

- 9.7 ILJIN ELECTRIC

- 9.8 LS Cable & System Ltd.

- 9.9 Mitsubishi Electric Corporation

- 9.10 Nexans

- 9.11 NKT A/S

- 9.12 Prysmian Group

- 9.13 Qingdao Hanhe Cable Co., Ltd.

- 9.14 Sumitomo Electric Industries, Ltd.

- 9.15 Riyadh Cables

- 9.16 Taihan Cable & Solution Co., Ltd.

- 9.17 TELE-FONIKA Kable S.A.

- 9.18 Tratos

- 9.19 ZMS CABLE

- 9.20 ZTT

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 151 Pages

- 納期

- 2~3営業日