EVプラットフォーム市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

EV Platform Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 310 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801916

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

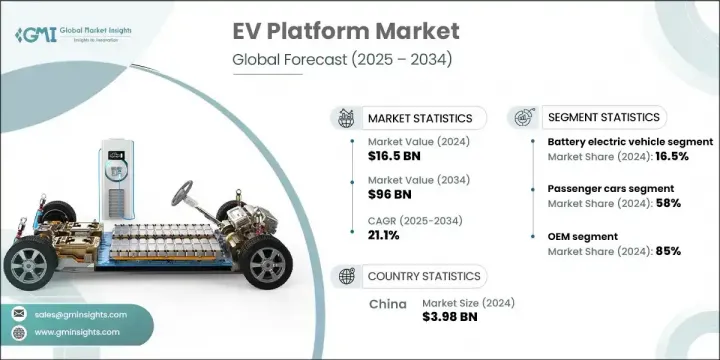

世界のEVプラットフォーム市場は、2024年には165億米ドルとなり、CAGR 21.1%で成長し、2034年には960億米ドルに達すると推定されています。

持続可能でゼロ・エミッションのモビリティ・ソリューションへのシフトの高まりは、EVプラットフォームの急速な技術革新に火をつけた。これらのプラットフォームは現在、自律走行、バッテリー統合、拡張可能なパワートレインなどの高度な機能をサポートする、モジュール式のソフトウェア定義システムへと進化しています。自動車メーカーは、コスト効率に優れた生産とエネルギー効率の向上を実現しながら、車両クラスを超えた柔軟なアーキテクチャを可能にするプラットフォームを設計しています。

AI主導の機能と無線アップデートは、航続距離と性能を最適化する上で極めて重要な役割を果たします。パンデミックは、デジタル・ファーストの車両体験に対する需要を加速させ、各社が非接触機能およびリアルタイム・コネクティビティ・ツールをプラットフォーム設計に統合するよう後押ししました。遠隔診断、音声アシスト制御、インテリジェント・ルート管理などの進歩により、EVプラットフォームは基本的な構造部品から、次世代モビリティのためのインテリジェントで適応性の高いバックボーンへと昇華しました。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 165億米ドル |

| 予測金額 | 960億米ドル |

| CAGR | 21.1% |

バッテリー電気自動車分野のシェアは16.5%で、2034年までのCAGRは21%と予測されます。BEVは、クリーンなアーキテクチャと、車内スペース、バッテリー配置、設計の柔軟性を最大化するスケートボードスタイルのプラットフォームとの互換性により、支持されています。純粋な電気自動車であるため燃焼システムが不要であり、メーカーは合理的な構造を設計し、生産コストを削減し、性能効率を高めることができます。

乗用車セグメントは2024年に58%と最も高いシェアを占め、2025年から2034年までのCAGRは20%で力強い成長を維持すると予測されます。電気乗用車の普及は、消費者の需要の高まりとOEMによるプラットフォーム開発への多額の投資によって後押しされています。各社は、セダン、ハッチバック、コンパクトSUVに最適化したEV専用アーキテクチャを構築し、柔軟な設計、強化されたバッテリー寿命、コネクテッド機能のサポートを提供しています。このような幅広い適応性により、自動車メーカーは、航続距離、安全性、デジタル統合を向上させ、大衆市場をターゲットにすることができます。

中国のEVプラットフォーム市場は69%のシェアを占め、2024年には39億8,000万米ドルを生み出します。同国は主要なEVメーカーであると同時に消費者でもあり、市場で極めて重要な役割を果たしています。補助金、生産義務、充電インフラ投資を通じた戦略的な政府支援により、プラットフォーム革新に強い勢いが生まれています。国内企業は、拡大する電気自動車ユーザーのニーズに応えながら、性能と航続距離のバランスをとった、拡張性のある手頃な価格のEVプラットフォームを開発し続けています。

世界のEVプラットフォーム市場を形成している主要企業には、フォード、テスラ、トヨタ、フォルクスワーゲン、BMW、ゼネラルモーターズ、ボルボなどがあります。市場での地位を強化するため、EVプラットフォーム分野の企業は戦略的投資と提携を優先しています。OEMは、新たなソフトウェア駆動技術との互換性を確保しつつ、幅広い車両サイズと機能をサポートするモジュール式プラットフォームを開発するため、研究開発に多額の投資を行っています。また、自動車メーカーは、コネクティビティ、充電、自律性のための統合エコシステムを構築するために、バッテリーメーカーやハイテク企業と協力しています。さらに、モーター、コントローラー、バッテリーパックなどの主要コンポーネントを制御するために、多くのメーカーが垂直統合モデルを採用し、性能とコスト管理を強化しています。これらの戦略は、進化するEV情勢において、拡張性、適応性、長期的競争力を確保するのに役立ちます。

目次

第1章 調査手法

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 部品サプライヤー

- プラットフォーム開発者

- 製造業者

- 流通チャネル

- エンドユーザー

- 業界への影響要因

- 促進要因

- 世界の電気自動車普及の急増

- バッテリー技術の進歩

- OEMのモジュラーEVアーキテクチャへの移行

- EV充電インフラの拡張

- 業界の潜在的リスク&課題

- EVプラットフォームへの初期投資額が大きい

- 新興地域におけるインフラの未整備

- 市場機会

- EV-as-a-Service(EVaaS)モデルの成長

- 自律型およびコネクテッドテクノロジーとの統合

- 商用車の電動化

- 都市におけるマイクロモビリティソリューションの需要の高まり

- 促進要因

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許分析

- 価格動向

- 地域別

- 車両別

- 利益率分析

- コスト内訳分析

- 原材料費の構成要素

- 製造および機械コスト

- 物流・配送コスト

- 人件費と組み立て費

- 研究開発費および試験費

- EVプラットフォーム市場進化と成熟の分析

- ICEへの適応から専用プラットフォームへの歴史的開発

- プラットフォームアーキテクチャの進化のタイムライン

- テクノロジー導入ライフサイクル分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:推進別、2021年~2034年

- 主要動向

- バッテリー電気自動車(BEV)

- ハイブリッド電気自動車(HEV)

- プラグインハイブリッド電気自動車(PHEV)

第6章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- セダン

- SUV/クロスオーバー

- ハッチバック

- 商用車

- 小型商用車

- 大型商用車

第7章 市場推計・予測:プラットフォーム別、2021年~2034年

- 主要動向

- P0

- P1

- P2

- P3

- P4

第8章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- バッテリー

- サスペンションシステム

- モーターシステム

- シャーシ

- 電子制御ユニット(ECU)

- その他

第9章 市場推計・予測:販売チャネル別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- フィリピン

- インドネシア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- 世界企業

- BMW

- Ford

- General Motors

- Hyundai Motor

- Nissan Motor

- Renault

- Stellantis

- Tesla

- Toyota Motor

- Volkswagen

- 地域企業

- Avatar Technology

- BYD Auto

- Leapmotor

- Mahindra Electric

- Seres

- Tata Motors

- Zeekr

- 新興企業

- Bollinger Motors

- Canoo

- Cenntro

- Foxconn

- Geely

- Gaussin

- Lucid Motors

- NIO

- OSVehicle

- REE Automotive

- Rivian Automotive

- XPeng Motors

- Zero Labs Automotive

目次

The Global EV Platform Market was valued at USD 16.5 billion in 2024 and is estimated to grow at a CAGR of 21.1% to reach USD 96 billion by 2034. The increasing shift toward sustainable and zero-emission mobility solutions has sparked rapid innovation in EV platforms. These platforms are now evolving into modular, software-defined systems that support advanced features like autonomous driving, battery integration, and scalable powertrains. Automakers are designing platforms that allow flexible architecture across vehicle classes while enabling cost-efficient production and improved energy efficiency.

AI-driven features and over-the-air updates play a crucial role in optimizing range and performance. The pandemic accelerated demand for digital-first vehicle experiences, pushing companies to integrate contactless functionalities and real-time connectivity tools into platform design. Advancements in remote diagnostics, voice-assisted controls, and intelligent route management have elevated EV platforms from basic structural components to intelligent, adaptable backbones for next-gen mobility.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $16.5 Billion |

| Forecast Value | $96 Billion |

| CAGR | 21.1% |

The battery electric vehicles segment held 16.5% share and is forecasted to grow at a CAGR of 21% through 2034. BEVs are favored due to their clean architecture and compatibility with skateboard-style platforms that maximize interior space, battery placement, and design flexibility. Their pure electric nature eliminates combustion systems, allowing manufacturers to engineer streamlined structures, reduce production costs, and boost performance efficiency.

The passenger car segment held the highest share at 58% in 2024 and is projected to maintain strong growth with a CAGR of 20% from 2025 to 2034. Widespread adoption of electric passenger vehicles has been fueled by growing consumer demand, paired with substantial OEM investment in platform development. Companies are creating dedicated EV architectures optimized for sedans, hatchbacks, and compact SUVs, offering flexible designs, enhanced battery life, and support for connected features. This broad adaptability enables automakers to target a mass-market audience with improved range, safety, and digital integration.

China EV Platform Market held 69% share, generating USD 3.98 billion in 2024. The country plays a pivotal role in the market as both a major EV manufacturer and consumer. Strategic government support through subsidies, production mandates, and charging infrastructure investments has created strong momentum in platform innovation. Domestic firms continue to engineer scalable, affordable EV platforms that balance performance and range while catering to the needs of their expanding electric vehicle user base.

Leading companies shaping the Global EV Platform Market include Ford, Tesla, Toyota, Volkswagen, BMW, General Motors, and Volvo. To reinforce their market position, companies in the EV platform sector are prioritizing a mix of strategic investments and partnerships. OEMs are heavily investing in R&D to develop modular platforms that support a wide range of vehicle sizes and functions, while ensuring compatibility with emerging software-driven technologies. Automakers are also collaborating with battery producers and tech firms to create integrated ecosystems for connectivity, charging, and autonomy. Furthermore, many are adopting vertical integration models to control key components such as motors, controllers, and battery packs, which enhances performance and cost control. These strategies help ensure scalability, adaptability, and long-term competitiveness in the evolving EV landscape.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Propulsion

- 2.2.3 Vehicle

- 2.2.4 Platform

- 2.2.5 Component

- 2.2.6 Sales Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Component suppliers

- 3.1.3 Platform developers

- 3.1.4 Manufacturers

- 3.1.5 Distribution channel

- 3.1.6 End users

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surge in global electric vehicle adoption

- 3.2.1.2 Advancements in battery technology

- 3.2.1.3 OEM shift to modular EV architectures

- 3.2.1.4 Expansion of EV charging infrastructure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial investment in EV platforms

- 3.2.2.2 Underdeveloped infrastructure in emerging regions

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in EV-as-a-service (EVaaS) models

- 3.2.3.2 Integration with autonomous & connected tech

- 3.2.3.3 Electrification of commercial fleets

- 3.2.3.4 Rising demand for urban micro-mobility solutions

- 3.2.1 Growth drivers

- 3.3 Regulatory landscape

- 3.3.1 North America

- 3.3.2 Europe

- 3.3.3 Asia Pacific

- 3.3.4 Latin America

- 3.3.5 Middle East & Africa

- 3.4 Porter’s analysis

- 3.5 PESTEL analysis

- 3.6 Technology and Innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Patent analysis

- 3.8 Price Trend

- 3.8.1 By region

- 3.8.2 By Vehicle

- 3.9 Profit margin analysis

- 3.10 Cost breakdown analysis

- 3.10.1 Raw material cost components

- 3.10.2 Manufacturing and machinery costs

- 3.10.3 Logistics and distribution costs

- 3.10.4 Labor and assembly costs

- 3.10.5 R&D and testing costs

- 3.11 EV platform market evolution and maturity analysis

- 3.11.1 Historical development from ICE adaptations to dedicated platforms

- 3.11.2 Platform architecture evolution timeline

- 3.11.3 Technology adoption lifecycle analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Battery electric vehicles (BEV)

- 5.3 Hybrid electric vehicles (HEV)

- 5.4 Plug-in hybrid electric vehicles (PHEV)

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Sedans

- 6.2.2 SUVs/crossovers

- 6.2.3 Hatchbacks

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles

- 6.3.2 Heavy commercial vehicles

Chapter 7 Market Estimates & Forecast, By Platform, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 P0

- 7.3 P1

- 7.4 P2

- 7.5 P3

- 7.6 P4

Chapter 8 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Battery

- 8.3 Suspension system

- 8.4 Motor system

- 8.5 Chassis

- 8.6 Electronic Control Units (ECUs)

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Netherlands

- 10.3.7 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Philippines

- 10.4.7 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 BMW

- 11.1.2 Ford

- 11.1.3 General Motors

- 11.1.4 Hyundai Motor

- 11.1.5 Nissan Motor

- 11.1.6 Renault

- 11.1.7 Stellantis

- 11.1.8 Tesla

- 11.1.9 Toyota Motor

- 11.1.10 Volkswagen

- 11.2 Regional Players

- 11.2.1 Avatar Technology

- 11.2.2 BYD Auto

- 11.2.3 Leapmotor

- 11.2.4 Mahindra Electric

- 11.2.5 Seres

- 11.2.6 Tata Motors

- 11.2.7 Zeekr

- 11.3 Emerging Players

- 11.3.1 Bollinger Motors

- 11.3.2 Canoo

- 11.3.3 Cenntro

- 11.3.4 Foxconn

- 11.3.5 Geely

- 11.3.6 Gaussin

- 11.3.7 Lucid Motors

- 11.3.8 NIO

- 11.3.9 OSVehicle

- 11.3.10 REE Automotive

- 11.3.11 Rivian Automotive

- 11.3.12 XPeng Motors

- 11.3.13 Zero Labs Automotive

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 310 Pages

- 納期

- 2~3営業日