サイクロンセパレーター市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Cyclone Separator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801904

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

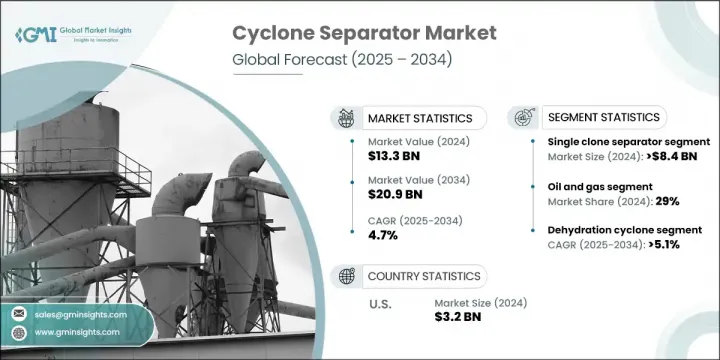

サイクロンセパレーターの世界市場規模は、2024年に133億米ドルとなり、CAGR 4.7%で成長し、2034年には209億米ドルに達すると予測されています。

同市場は、クリーンエネルギー・ソリューションへの高まりと世界の厳しい環境規制により、牽引力を増しています。バイオマス、太陽光、その他の代替エネルギー源の需要が増加するにつれて、排出を減らし機器を保護するための高性能空気ろ過システムへの要求も高まっています。サイクロンセパレーターは、微粒子を処理する効率性から不可欠なソリューションとして登場し、複数の産業における持続可能性の目標をサポートしています。

多段ろ過、CFD最適化設計、ハイブリッドシステムなどの技術の進歩により、性能とエネルギー効率が大幅に向上しています。その役割は、特に化学、エレクトロニクス、製薬のような精密集約的な分野で急速に進化しています。アジア太平洋地域では、工業化が急速に進んでいる国々が、排出規制の強化により需要を牽引しています。サイクロンセパレーターは、インフラと製造活動の拡大に対応して広く採用されています。今日の競合情勢では、特に業界が長期的な信頼性と低メンテナンスを優先しているため、製品のカスタマイズや材料の耐久性などの特徴が、購入者の意思決定にとって重要になってきています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 133億米ドル |

| 予測金額 | 209億米ドル |

| CAGR | 4.7% |

シングルサイクロンセパレーターは2024年に84億米ドルに達し、2034年までCAGR 4.6%で成長すると予測されます。このシステムが広く採用されているのは、初期費用が低く、機械構造がシンプルで、メンテナンスの必要性が最小であるためです。可動部品がないこれらのシステムは、継続的な稼働時間と予算管理が不可欠な環境においてコスト効率の高いソリューションを提供し、運用の信頼性を求める重工業において特に魅力的なものとなっています。

石油・ガスセクターは2024年に29%のシェアを占め、2025年から2034年にかけてCAGR 5.2%で成長すると予測されています。サイクロンセパレーターは、砂落としや液体と気体の分離装置を必要とする上流工程から、ガス処理、精製、パイプライン保守を含む下流工程に至るまで、バリューチェーン全体を通じて重要です。これらのセパレータは、粒子状物質の負荷を低減し、高価値の機械を保護し、高圧・大量環境での運転を中断させないという重要な役割を担っています。

米国サイクロンセパレーター市場は、2024年に32億米ドルを生み出す79%のシェアを占めています。この成長を後押ししているのは、高度な大気品質管理ソリューションを必要とする厳しい環境政策です。規制により、産業界は効率的な微粒子除去技術の導入を余儀なくされています。サイクロンセパレーターは一般的に前ろ過ツールとして使用され、最終ろ過システムの負担を効果的に軽減し、規制遵守を確保し、全体的な運用効率を最適化します。

サイクロンセパレーター市場を積極的に形成している主要企業には、Mikropor、Sulzer、FLSmidth、Gulf Coast Air &Hydraulics、Cyclone Engineering Projects、Multotec、The Weir Group、KREBS、Exterran Corporation、Air Dynamics、Cyclotech、Haiwang Hydrocyclone、Mahle Industrial Filtration、Elgin Separation Solutions、サイクロンセパレーターAustraliaなどがあります。サイクロンセパレーター市場の主要メーカーは、競争力を強化するために戦略的な製品革新と地域拡大に注力しています。CFDのような先進的なシミュレーションツールを導入し、セパレーターの設計を最適化することで、より高い効率と低いエネルギー消費を実現する企業が増えています。また、製薬、エレクトロニクス、クリーンエネルギーなどの高精度産業に対応するための製品の多様化も進んでいます。各メーカーは産業界の顧客とパートナーシップを結び、厳しい排出基準や運用基準を満たすオーダーメードのソリューションを提供しています。多くの企業は、特にアジア太平洋の新興市場に対応するため、世界な製造・販売ネットワークを拡大しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 機会

- 成長可能性分析

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- タイプ別

- 規制情勢

- 標準とコンプライアンス要件

- 地域規制枠組み

- 認証基準

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 軸流

- 逆流

第6章 市場推計・予測:クローンタイプ別、2021年~2034年

- 主要動向

- 単一クローンセパレーター

- マルチクローンセパレーター

第7章 市場推計・予測:容量別、2021年~2034年

- 主要動向

- 2000 kg/時 未満

- 2000 kg/時~3000 kg/時

- 3000 kg/時 以上

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 脱水サイクロン

- 脱泥サイクロン

- スラグ除去サイクロン

- その他(集中サイクロン、サイクロン群など)

第9章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 石油・ガス

- 化学薬品

- 鉱業および鉱物処理

- 発電

- 飲食品

- その他(パルプ・紙、繊維、医薬品等)

第10章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 直接販売

- 間接販売

第11章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第12章 企業プロファイル

- Air Dynamics

- Cyclone Engineering Projects

- Cyclone Separator Australia

- Cyclotech

- Elgin Separation Solutions

- Exterran Corporation

- FLSmidth

- Gulf Coast Air &Hydraulics

- Haiwang Hydrocyclone

- KREBS

- Mahle Industrial Filtration

- Mikropor

- Multotec

- Sulzer

- The Weir Group

目次

The Global Cyclone Separator Market was valued at USD 13.3 billion in 2024 and is estimated to grow at a CAGR of 4.7% to reach USD 20.9 billion by 2034. The market is gaining traction due to the increasing push toward clean energy solutions and stringent global environmental regulations. As the demand for biomass, solar, and other alternative energy sources increases, so does the requirement for high-performance air filtration systems to reduce emissions and protect equipment. Cyclone separators have emerged as vital solutions due to their efficiency in handling particulates, supporting sustainability goals across multiple industries.

Technological advancements such as multi-stage filtration, CFD-optimized designs, and hybrid systems have significantly improved performance and energy efficiency. Their role is rapidly evolving, especially in precision-intensive sectors like chemicals, electronics, and pharmaceuticals. In the Asia-Pacific region, countries experiencing fast industrialization are driving demand due to tighter emission regulations. Cyclone separators are being widely adopted in response to growing infrastructure and manufacturing activity. In today's competitive landscape, features such as product customization and material durability are becoming critical for buyer decision-making, especially as industries prioritize long-term reliability and low maintenance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $13.3 Billion |

| Forecast Value | $20.9 Billion |

| CAGR | 4.7% |

Single cyclone separators reached USD 8.4 billion in 2024 and is anticipated to grow at a CAGR of 4.6% through 2034. Their widespread adoption is attributed to low upfront costs, simple mechanical structure, and minimal maintenance requirements. With no moving parts, these systems offer a cost-efficient solution in environments where continuous uptime and budget control are essential, making them especially appealing in heavy industries seeking operational reliability.

The oil & gas sector held a 29% share in 2024 and is set to grow at a CAGR of 5.2% between 2025 and 2034. Cyclone separators are critical throughout the entire value chain-from upstream operations requiring devices for desanding and liquid-gas separation to downstream applications involving gas processing, refining, and pipeline maintenance. These separators play a crucial role in reducing particulate load, safeguarding high-value machinery, and ensuring uninterrupted operations in high-pressure, high-volume environments.

United States Cyclone Separator Market held a 79% share generating USD 3.2 billion in 2024. This growth is fueled by strict environmental policies requiring advanced air quality management solutions. Regulations compel industries to deploy efficient particulate removal technologies. Cyclone separators are commonly used as pre-filtration tools, effectively decreasing the burden on final filtration systems, ensuring regulatory compliance, and optimizing overall operational efficiency.

Key players actively shaping the Cyclone Separator Market include Mikropor, Sulzer, FLSmidth, Gulf Coast Air & Hydraulics, Cyclone Engineering Projects, Multotec, The Weir Group, KREBS, Exterran Corporation, Air Dynamics, Cyclotech, Haiwang Hydrocyclone, Mahle Industrial Filtration, Elgin Separation Solutions, and Cyclone Separator Australia. Leading manufacturers in the cyclone separator market are focusing on strategic product innovation and regional expansion to strengthen their competitive positions. Companies are increasingly integrating advanced simulation tools like CFD to optimize separator designs for greater efficiency and lower energy consumption. Product diversification to serve high-precision industries such as pharmaceuticals, electronics, and clean energy is also on the rise. Players are forming partnerships with industrial clients to deliver tailored solutions that meet strict emission and operational standards. Many firms are expanding their global manufacturing and distribution networks to serve emerging markets, especially in Asia-Pacific.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 By type

- 2.2.3 By clone type

- 2.2.4 By capacity

- 2.2.5 By application

- 2.2.6 By end use industry

- 2.2.7 By distribution channel

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 ($Billion, Thousand Units)

- 5.1 Key trends

- 5.2 Axial flow

- 5.3 Reverse flow

Chapter 6 Market Estimates & Forecast, By Clone type, 2021 - 2034 ($Billion, Thousand Units)

- 6.1 Key trends

- 6.2 Single clone separator

- 6.3 Multi-clone separator

Chapter 7 Market Estimates & Forecast, By Capacity, 2021 - 2034 ($Billion, Thousand Units)

- 7.1 Key trends

- 7.2 Up to 2000 kg/hr

- 7.3 2000 kg/hr. - 3000 kg/hr

- 7.4 Above 3000 kg/hr

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Billion, Thousand Units)

- 8.1 Key trends

- 8.2 Dehydration cyclone

- 8.3 Desliming cyclone

- 8.4 Slag removal cyclones

- 8.5 Others (concentration cyclone, cyclone group etc.)

Chapter 9 Market Estimates & Forecast, By End Use Industry, 2021 - 2034 ($Billion, Thousand Units)

- 9.1 Key trends

- 9.2 Oil and gas

- 9.3 Chemical

- 9.4 Mining and mineral processing

- 9.5 Power generation

- 9.6 Food and beverages

- 9.7 Others (pulp & paper, textiles, pharmaceutical etc.)

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Billion, Thousand Units)

- 10.1 Key trends

- 10.2 Direct sales

- 10.3 Indirect sales

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Billion, Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Air Dynamics

- 12.2 Cyclone Engineering Projects

- 12.3 Cyclone Separator Australia

- 12.4 Cyclotech

- 12.5 Elgin Separation Solutions

- 12.6 Exterran Corporation

- 12.7 FLSmidth

- 12.8 Gulf Coast Air & Hydraulics

- 12.9 Haiwang Hydrocyclone

- 12.10 KREBS

- 12.11 Mahle Industrial Filtration

- 12.12 Mikropor

- 12.13 Multotec

- 12.14 Sulzer

- 12.15 The Weir Group

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日