|

市場調査レポート

商品コード

1801878

関節鏡検査器具の市場機会と促進要因、業界動向分析、2025年~2034年予測Arthroscopy Instruments Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 関節鏡検査器具の市場機会と促進要因、業界動向分析、2025年~2034年予測 |

|

出版日: 2025年08月01日

発行: Global Market Insights Inc.

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

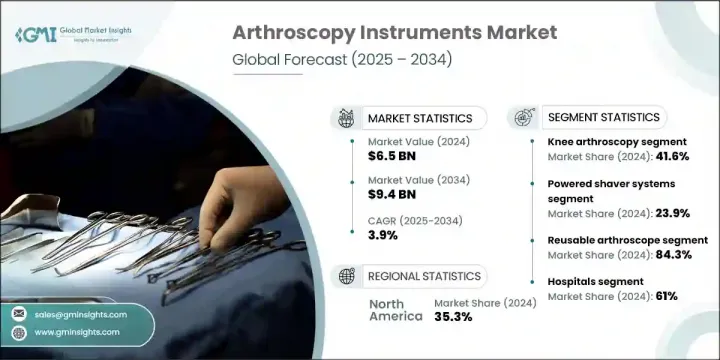

関節鏡検査器具の世界市場規模は、2024年に65億米ドルとなり、CAGR 3.9%で成長し、2034年には94億米ドルに達すると予測されています。

関節関連疾患の割合の増加、高齢者の増加、スポーツ傷害の増加がこの市場を牽引する主要因の一つです。低侵襲手術へのシフトが進んでおり、関節鏡手術は、回復時間の短縮、入院期間の短縮、術後合併症の減少などの利点から、好ましいアプローチとして際立っています。さらに、可視化技術の進歩、ロボット工学の統合、使い捨て器具の重視により、関節鏡手術は大きく変化しています。関節の問題の早期治療と診断に対する患者の意識の高まりも、これらの器具の世界の需要を後押ししています。

特に都市部では外来手術センターが急速に拡大し、外来関節鏡検査の主要拠点となっており、市場の成長にさらに貢献しています。新興経済国でのヘルスケアインフラの拡大は、支出の増加とともに、公的・私的医療セクタの両方で関節鏡技術や器具の幅広い採用を促しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 65億米ドル |

| 予測金額 | 94億米ドル |

| CAGR | 3.9% |

電動シェーバーシステムは、低侵襲関節手術において正確な組織・骨切除を行う上で不可欠な役割を果たすため、2024年には23.9%のシェアを獲得しました。優れた効率性、扱いやすさ、先進的可視化システムとシームレスに統合する能力により、最新の関節鏡手術で好まれるツールとなっています。外来手術センターでの使用が増えていることも、手術時間を短縮すると同時に、精度と手技の成功率を高めるため、普及を後押ししています。

膝関節鏡検査セグメントは2024年に41.6%と最大の市場シェアを占めたが、これは世界的に膝に関連する怪我や変形性関節症の症例が多いことに起因しています。このセグメントは、スポーツ参加者の増加、高齢者の増加、低侵襲的介入への幅広いシフトから利益を得ています。靭帯断裂や軟骨損傷には関節鏡視下手術が日常的に用いられており、最も多く行われている手技です。手技、ツール、回復結果の開発は、先進国、発展途上国の両地域において、関節鏡手術の優位性を支え続けています。

北米の関節鏡検査器具2024年のシェアは35.3%。このリーダーシップは、先進的手術インフラ、最先端医療技術の早期導入、整形外科手術の頻度の高さによってもたらされています。米国とカナダは整形外科専門センターと外来手術施設への投資を続けており、低侵襲手技の広範な統合を可能にしています。平均寿命の伸びと変形性関節症やスポーツ傷害の有病率の増加が相まって、この地域全体の関節鏡ツールの需要がさらに加速しています。

関節鏡検査器具世界市場の主要参入企業には、Olympus、Medacta、Smith & Nephew、Medtronic、Hemodia、Stryker、Richard Wolf、CONMED、Karl Storz、Arthrex、Invamed、Zimmer Biomet、B. Braun、DePuy Synthes (J&J)などがあります。関節鏡検査器具市場の主要企業は、次世代外科技術への一貫した投資を通じて、その地位を高めています。ロボット工学、AIによる視覚化、使い捨てツールなどの革新は、これらの企業がより高い精度、短い回復期間、強化された臨床結果を提供するのに役立っています。いくつかの企業は、外来手術センターからの需要の高まりに対応するため、外来患者に特化した製品ラインを拡大しています。ヘルスケア機関やスポーツ医療の専門家との戦略的提携により、各社は進化する手術手技に合わせた手技に特化した器具を開発しています。さらに、多くの企業は、地域の流通網を強化し、費用対効果の高い器具ラインを発売することで、高成長の新興市場を対象としています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- 産業への影響要因

- 促進要因

- スポーツ関連の傷害と整形外科的疾患の有病率の上昇

- 低侵襲手術の需要増加

- 関節疾患にかかりやすい高齢者の増加

- 関節鏡による可視化と画像化技術の進歩

- 産業の潜在的リスク・課題

- 関節鏡検査機器とインプラントの高コスト

- 低所得地域や農村地域ではアクセスが限られている

- 市場機会

- AIとロボット支援関節鏡検査との技術統合

- 新興市場における成長の可能性

- 促進要因

- 成長可能性分析

- 規制情勢

- 技術とイノベーションの情勢

- 現在の技術動向

- 新興技術

- サプライチェーン分析

- 消費者行動の傾向

- 市場参入戦略分析

- ポーターの分析

- PESTEL分析

- 将来の市場動向

- ギャップ分析

- 価格分析、2024年

- 特許情勢

- 償還シナリオ

- 償還施策が市場成長に与える影響

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 世界

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡大計画

第5章 市場推定・予測:製品タイプ別、2021~2034年

- 主要動向

- 電動シェーバーシステム

- 可視化システム

- 関節鏡

- 流体管理システム

- 関節鏡インプラント

- 高周波(RF)アブレーションシステム

- その他

第6章 市場推定・予測:用途別、2021~2034年

- 主要動向

- 膝関節鏡検査

- 肩関節鏡検査

- 股関節鏡検査

- その他

第7章 市場推定・予測:使用性別、2021~2034年

- 主要動向

- 再利用型関節鏡

- 使い捨て関節鏡

第8章 市場推定・予測:最終用途別、2021~2034年

- 主要動向

- 病院

- 外来手術センター

- その他

第9章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Arthrex

- B. Braun

- CONMED

- DePuy Synthes(J& J)

- Hemodia

- Invamed

- Karl Storz

- Medacta

- Medtronic

- Olympus

- Richard Wolf

- Smith & Nephew

- Stryker

- Zimmer Biomet

The Global Arthroscopy Instruments Market was valued at USD 6.5 billion in 2024 and is estimated to grow at a CAGR of 3.9% to reach USD 9.4 billion by 2034. Rising rates of joint-related conditions, a growing elderly population, and increasing sports injuries are among the major forces driving this market. There is a growing shift toward minimally invasive procedures, and arthroscopy stands out as a preferred approach due to its benefits, such as shorter recovery times, reduced hospital stays, and lower post-operative complications. Additionally, advancements in visualization technologies, robotics integration, and a greater emphasis on disposable devices are transforming arthroscopy procedures. Increasing patient awareness about early treatment and diagnosis of joint issues is also helping to fuel demand for these instruments globally.

Ambulatory surgical centers, especially in urban settings, are rapidly expanding and becoming major hubs for outpatient arthroscopy, contributing further to market growth. Expanding healthcare infrastructure in emerging economies, alongside rising expenditure, is encouraging broader adoption of arthroscopic techniques and devices across both public and private health sectors.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.5 Billion |

| Forecast Value | $9.4 Billion |

| CAGR | 3.9% |

The powered shaver systems captured a 23.9% share in 2024, owing to their essential role in delivering precise tissue and bone resection during minimally invasive joint procedures. Their superior efficiency, ease of handling, and ability to integrate seamlessly with advanced visualization systems make them a preferred tool in modern arthroscopic surgeries. Their growing use in outpatient surgical centers is helping fuel adoption, as they reduce operation time while enhancing precision and procedural success.

The knee arthroscopy segment held the largest market share at 41.6% in 2024, attributed to the high volume of knee-related injuries and osteoarthritis cases globally. The segment benefits from growing sports participation, a rise in elderly populations, and a broader shift toward minimally invasive interventions. Ligament tears and cartilage damage are routinely addressed using arthroscopic methods, making it the most performed procedure. Improvements in techniques, tools, and recovery outcomes continue to support its dominance across both developed and developing regions.

North America Arthroscopy Instruments Market held a 35.3% share in 2024. This leadership is driven by advanced surgical infrastructure, early adoption of cutting-edge medical technologies, and a high frequency of orthopedic procedures. The U.S. and Canada continue to invest in specialty orthopedic centers and outpatient surgical facilities, enabling wide-scale integration of minimally invasive techniques. Rising life expectancy, combined with the increasing prevalence of osteoarthritis and sports injuries, further accelerates the demand for arthroscopic tools across the region.

Key participants in the Global Arthroscopy Instruments Market include Olympus, Medacta, Smith & Nephew, Medtronic, Hemodia, Stryker, Richard Wolf, CONMED, Karl Storz, Arthrex, Invamed, Zimmer Biomet, B. Braun, and DePuy Synthes (J&J). Leading companies in the arthroscopy instruments market are advancing their position through consistent investment in next-generation surgical technologies. Innovations in robotics, AI-driven visualization, and disposable tools are helping these firms offer greater precision, shorter recovery periods, and enhanced clinical outcomes. Several players are expanding their outpatient-specific product lines to meet rising demand from ambulatory surgical centers. Strategic collaborations with healthcare institutions and sports medicine specialists are enabling companies to develop procedure-specific instruments tailored to evolving surgical techniques. Additionally, many are targeting high-growth emerging markets by strengthening regional distribution networks and launching cost-effective instrument lines.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Application trends

- 2.2.4 Usability trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of sports-related injuries and orthopedic disorders

- 3.2.1.2 Growing demand for minimally invasive surgical procedures

- 3.2.1.3 Increasing geriatric population prone to joint diseases

- 3.2.1.4 Advancements in arthroscopic visualization and imaging technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of arthroscopy equipment and implants

- 3.2.2.2 Limited accessibility in low-income and rural regions

- 3.2.3 Market opportunities

- 3.2.3.1 Technological integration with AI and robotic-assisted arthroscopy

- 3.2.3.2 Growth potential in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Supply chain analysis

- 3.7 Consumer behaviour trend

- 3.8 Go-to-market strategy analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Future market trends

- 3.12 Gap analysis

- 3.13 Pricing analysis, 2024

- 3.14 Patent Landscape

- 3.15 Reimbursement scenario

- 3.15.1 Impact of reimbursement policies on market growth

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.2.5 Latin America

- 4.2.6 Middle East and Africa

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Powered shaver systems

- 5.3 Visualization systems

- 5.4 Arthroscopes

- 5.5 Fluid management systems

- 5.6 Arthroscopic implants

- 5.7 Radiofrequency (RF) ablation systems

- 5.8 Other product types

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Knee arthroscopy

- 6.3 Shoulder arthroscopy

- 6.4 Hip arthroscopy

- 6.5 Other applications

Chapter 7 Market Estimates and Forecast, By Usability, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Reusable arthroscope

- 7.3 Disposable arthroscopes

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Ambulatory surgical centers

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Arthrex

- 10.2 B. Braun

- 10.3 CONMED

- 10.4 DePuy Synthes (J&J)

- 10.5 Hemodia

- 10.6 Invamed

- 10.7 Karl Storz

- 10.8 Medacta

- 10.9 Medtronic

- 10.10 Olympus

- 10.11 Richard Wolf

- 10.12 Smith & Nephew

- 10.13 Stryker

- 10.14 Zimmer Biomet