水中ドローンの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Underwater Drones Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801875

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

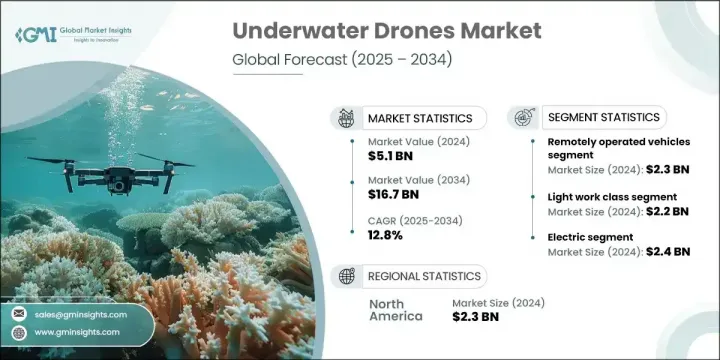

水中ドローンの世界市場規模は、2024年に51億米ドルとなり、CAGR12.8%で成長し、2034年には167億米ドルに達すると推定されています。

この拡大は、海底探査需要の増加、海洋石油・ガスプロジェクトへの投資の増加、海上セキュリティの強化、再生可能エネルギー事業の統合によって大きく支えられています。さらに、自律性、推進システム、画像技術の絶え間ない向上が、商業と防衛の両部門でより広範な市場導入を促進しています。

このセグメントを再形成する重要な動向は、電気推進システムに対する嗜好の高まりです。このようなアップグレードにより、航続距離の向上、音響フットプリントの削減、エネルギー効率の向上が実現し、電動推進システムはさまざまな用途に理想的なものとなっています。リチウムイオンバッテリー、ブラシレスDCモーター、スーパーコンデンサの統合により、最新の電動ドローンは、特定のミッションにおいて72時間以上稼働するようになりました。この変革は、低騒音と高効率の性能が不可欠な中水域や近海での活動において特に価値があります。同時に、自律型水中航行体(AUV)への関心も急増しています。AUVは、搭載されたナビゲーション、センサ、ミッションソフトウェアを使用して独自に動作し、リアルタイムのオペレーター入力なしで精度を高めることができます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 51億米ドル |

| 予測金額 | 167億米ドル |

| CAGR | 12.8% |

2024年の遠隔操作車(ROV)セグメントの市場規模は23億米ドルでした。このセグメントは、石油・ガス、防衛、インフラ検査におけるリアルタイムの水中作業のニーズの高まりにより急成長しています。ROVは多用途のツールシステムを備え、強力な積載能力を持ち、オペレーターに完全な手動制御を提供するため、深海の検査、保守作業、水中回収作業に理想的です。

中規模クラスのドローンセグメントは、2024年に22億米ドルを生み出しました。これらのドローンは、操作の柔軟性、手頃な価格、検査や軽介入ミッションの実行における有効性により、広く採用されています。センサやマニピュレーターによる適応性、展開の複雑性の低さ、表面サポートの必要性の最小化により、限られた過酷な環境に適しています。進化する運用ニーズをサポートするため、メーカーは港湾管理、インフラモニタリング、オフショア請負などの産業に対応するプラグアンドプレイ設計、エッジAI統合、改良型テザー制御システムに注力しています。

カナダの水中ドローン市場は2034年までに7億7,510万米ドルに達します。この成長の原動力は、オフショアエネルギー事業の拡大、海洋領土モニタリングの強化、海洋科学への投資の深化です。氷点下航行、海底遠隔モニタリング、生息地マッピングのためのドローンの使用は増加し続けています。機器開発者は、科学探査と防衛の両方の用途に適したモジュール型センサ構成を持つ、堅牢で冷水対応のドローンシステムを優先することをお勧めします。

世界水中ドローン市場の主要企業には、PowerRay、Gavia AUV、SRV-8 ROV、Neptune ROV、Phantom ROVシリーズ、FIFISH V6、Flying Nodes AUV、Marlin AUV、HUGIN AUV、Seaeye Falcon ROV、HUGIN AUVなどがある、Seaeye Falcon ROV、Sibiu Pro、SeaDrone ROV、SeaCat AUV、Seasam ROV、BW Space Pro、Blueye X3、Bluefin-21 AUV、Oceaneering ROVs、Eelume Subsea Robot、Absolute Ocean AUV。

水中ドローンセグメントの企業は、多面的な戦略によって競合を強化しています。自律性、センサの統合、バッテリーの長寿命化、推進技術の進歩のための研究開発が重視されています。メーカー各社は、探査、防衛、検査、科学研究など、特定のミッションに向けた迅速なカスタマイズを可能にするモジュール設計を優先しています。政府機関、エネルギー企業、海洋ラボとの戦略的パートナーシップは、企業が長期契約を確保するのに役立っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- エコシステム分析

- 産業への影響要因

- 促進要因

- 海洋探査の需要の高まり

- オフショア石油・ガス事業の拡大

- 海上安全保障とモニタリングのニーズ

- 再生可能エネルギープロジェクトへの投資増加

- 自律性とイメージングにおける技術の進歩

- 落とし穴と課題

- バッテリー寿命の制限と電源管理

- 先進的水中ドローンの高コスト

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- 技術とイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 価格戦略

- 新たなビジネスモデル

- コンプライアンス要件

- 国防予算分析

- 世界の防衛費の動向

- 地域防衛予算配分

- 北米

- 欧州

- アジア太平洋

- 中東・アフリカ

- ラテンアメリカ

- 主要な防衛近代化プログラム

- 予算予測(2025~2034年)

- 産業の成長への影響

- 国別防衛予算

- サプライチェーンのレジリエンス

- 地政学的分析

- 人材分析

- デジタル変革

- 合併、買収、戦略的提携の情勢

- リスク評価と管理

- 主要契約の締結(2021~2024年)

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- 市場集中分析

- 地域別

- 主要参入企業の競合ベンチマーキング

- 財務実績の比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオの比較

- 製品ラインナップの広さ

- 技術

- 革新

- 地理的プレゼンスの比較

- 世界フットプリント分析

- サービスネットワークの範囲

- 地域による市場浸透率

- 競合ポジショニングマトリックス

- リーダー

- 課題者

- フォロワー

- ニッチ参入企業

- 戦略的展望マトリックス

- 財務実績の比較

- 主要開発、2021~2024年

- 合併と買収

- パートナーシップとコラボレーション

- 技術的進歩

- 拡大と投資戦略

- 持続可能性への取り組み

- デジタル変革の取り組み

- 新興企業/スタートアップ企業の競合情勢

第5章 市場推定・予測:タイプ別、2021~2034年

- 主要動向

- 遠隔操作車両

- 自律型水中車両

- ハイブリッド水中車両

第6章 市場推定・予測:製品クラス別、2021~2034年

- 主要動向

- 超小規模クラス

- 小規模・中規模クラス

- 軽規模クラス

- 重規模クラス

第7章 市場推定・予測:推進システム別、2021~2034年

- 主要動向

- 電気

- 機械

- ハイブリッド

第8章 市場推定・予測:用途別、2021~2034年

- 主要動向

- 防衛と安全保障

- 海軍のモニタリング

- 地雷対策

- 対潜水艦戦

- 水中情報収集と偵察

- 捜索救助任務

- その他

- 科学研究と探査

- 海洋学的研究

- 海洋生物多様性モニタリング

- 海底マッピング

- 気候と環境研究

- インフラの点検と保守

- パイプラインとリグの検査

- 水中ケーブルモニタリング

- ダムと橋の点検

- 港湾整備

- 原子力施設の検査

- その他

- その他

第9章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- 世界の主要企業

- General Dynamics Mission Systems

- Deep Ocean Engineering, Inc.

- Nido Robotics

- Oceanbotics

- Neptune Robotics

- Terradepth

- SeaDrone Inc.

- Edgerov(Notilo Plus)

- Autonomous Robotics Ltd.

- 地域別主要企業

- 北米

- Oceaneering International, Inc.

- Lockheed Martin Corporation

- Teledyne Marine

- 欧州

- Kongsberg Maritime

- Saab Group

- Atlas Elektronik

- Asia-Pacific

- QYSEA Technology

- PowerVision Inc.

- Youcan Robotics(Shanghai)Co., Ltd.

- 北米

- 破壊的イノベーション/ニッチ参入企業

- Blueye Robotics

- Eelume AS

目次

The Global Underwater Drones Market was valued at USD 5.1 billion in 2024 and is estimated to grow at a CAGR of 12.8% to reach USD 16.7 billion by 2034. The expansion is largely supported by increasing demand for subsea exploration, rising investments in offshore oil and gas projects, maritime security enhancements, and the integration of renewable energy ventures. Additionally, constant improvements in autonomy, propulsion systems, and imaging technologies are driving broader market adoption across both commercial and defense sectors.

A key trend reshaping this space is the growing preference for electric propulsion systems. These upgrades enhance mission range, reduce acoustic footprint, and improve energy efficiency, making electric-powered underwater drones ideal for a range of applications. With the integration of lithium-ion batteries, brushless DC motors, and supercapacitors, modern electric drones now operate over 72 hours in certain missions. This transformation is especially valuable in mid-water and nearshore operations where low-noise and high-efficiency performance is essential. At the same time, there's a surge in interest for autonomous underwater vehicles (AUVs), which operate independently using onboard navigation, sensors, and mission software, enabling precision without real-time operator input.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.1 billion |

| Forecast Value | $16.7 billion |

| CAGR | 12.8% |

In 2024, the remotely operated vehicle (ROV) segment was valued at USD 2.3 billion. This segment is growing rapidly due to the rising need for real-time underwater operations in oil and gas, defense, and infrastructure inspections. ROVs are equipped with versatile tool systems, have strong payload capacities, and provide operators with full manual control, making them ideal for deepwater inspections, maintenance work, and underwater recovery tasks.

The light work-class drone segment generated USD 2.2 billion in 2024. These drones are widely adopted due to their operational flexibility, affordability, and effectiveness in performing inspection and light intervention missions. Their adaptability with sensors and manipulators, along with low deployment complexity and minimal surface support needs, makes them suitable for confined and harsh environments. To support evolving operational needs, manufacturers are focusing on plug-and-play designs, edge AI integration, and improved tether control systems to serve industries such as port management, infrastructure surveillance, and offshore contracting.

Canada Underwater Drones Market will reach USD 775.1 million by 2034. This growth is driven by the nation's expanding offshore energy operations, increased maritime territorial monitoring, and deepening investments in marine science. The use of drones for under-ice navigation, remote subsea monitoring, and habitat mapping continues to rise. Equipment developers are advised to prioritize ruggedized, cold-water-capable drone systems with modular sensor configurations suitable for both scientific exploration and defense applications.

Key players in the Global Underwater Drones Market include PowerRay, Gavia AUV, SRV-8 ROV, Neptune ROV, Phantom ROV Series, FIFISH V6, Flying Nodes AUV, Marlin AUV, HUGIN AUV, Seaeye Falcon ROV, Sibiu Pro, SeaDrone ROV, SeaCat AUV, Seasam ROV, BW Space Pro, Blueye X3, Bluefin-21 AUV, Oceaneering ROVs, Eelume Subsea Robot, and Absolute Ocean AUV.

Companies in the underwater drones space are reinforcing their competitive position through multi-faceted strategies. A strong emphasis is placed on R&D to advance autonomy, sensor integration, battery longevity, and propulsion technology. Manufacturers are prioritizing modular designs to enable rapid customization for specific missions, such as exploration, defense, inspection, or scientific research. Strategic partnerships with government bodies, energy firms, and marine institutes are helping companies secure long-term contracts.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Type trends

- 2.2.2 Product class trends

- 2.2.3 Propulsion system trends

- 2.2.4 Application trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2025-2034 (USD Billion)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry ecosystem analysis

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Rising Demand for Ocean Exploration

- 3.3.1.2 Expansion of Offshore Oil & Gas Activities

- 3.3.1.3 Maritime Security and Surveillance Needs

- 3.3.1.4 Growing Investment in Renewable Energy Projects

- 3.3.1.5 Technological Advancements in Autonomy & Imaging

- 3.3.2 Pitfalls and challenges

- 3.3.2.1 Limited Battery Life and Power Management

- 3.3.2.2 High Cost of Advanced Underwater Drones

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.5.4 Latin America

- 3.5.5 Middle East & Africa

- 3.6 Porter’s analysis

- 3.7 PESTEL analysis

- 3.8 Technology and Innovation landscape

- 3.8.1 Current technological trends

- 3.8.2 Emerging technologies

- 3.9 Price trends

- 3.9.1 By region

- 3.9.2 By product

- 3.10 Pricing strategies

- 3.11 Emerging business models

- 3.12 Compliance requirements

- 3.13 Defense budget analysis

- 3.14 Global defense spending trends

- 3.15 Regional defense budget allocation

- 3.15.1 North america

- 3.15.2 Europe

- 3.15.3 Asia Pacific

- 3.15.4 Middle East and Africa

- 3.15.5 Latin america

- 3.16 Key defense modernization programs

- 3.17 Budget forecast (2025-2034)

- 3.17.1 Impact on industry growth

- 3.17.2 Defense budgets by country

- 3.18 Supply chain resilience

- 3.19 Geopolitical analysis

- 3.20 Workforce analysis

- 3.21 Digital transformation

- 3.22 Mergers, acquisitions, and strategic partnerships landscape

- 3.23 Risk assessment and management

- 3.24 Major contract awards (2021-2024)

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market Concentration Analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market estimates and forecast, by Type, 2021 - 2034 (USD Billion & Units)

- 5.1 Key trends

- 5.2 Remotely operated vehicles

- 5.3 Autonomous underwater vehicles

- 5.4 Hybrid underwater vehicles

Chapter 6 Market estimates and forecast, by Product Class, 2021 - 2034 (USD Billion & Units)

- 6.1 Key trends

- 6.2 Micro class

- 6.3 Small and medium class

- 6.4 Light work class

- 6.5 Heavy work class

Chapter 7 Market estimates and forecast, by Propulsion System, 2021 - 2034 (USD Billion & Units)

- 7.1 Key trends

- 7.2 Electric

- 7.3 Mechanical

- 7.4 Hybrid

Chapter 8 Market estimates and forecast, by Application, 2021 - 2034 (USD Billion & Units)

- 8.1 Key trends

- 8.2 Defense and security

- 8.2.1 Naval surveillance

- 8.2.2 Mine countermeasures

- 8.2.3 Anti-submarine warfare

- 8.2.4 Underwater intelligence and reconnaissance

- 8.2.5 Search and rescue missions

- 8.2.6 Others

- 8.3 Scientific research and exploration

- 8.3.1 Oceanographic studies

- 8.3.2 Marine biodiversity monitoring

- 8.3.3 Seabed mapping

- 8.3.4 Climate and environmental studies

- 8.4 Infrastructure inspection and maintenance

- 8.4.1 Pipeline and rig inspection

- 8.4.2 Underwater cable monitoring

- 8.4.3 Dam and bridge inspection

- 8.4.4 Port and harbour maintenance

- 8.4.5 Nuclear facility inspection

- 8.4.6 Others

- 8.5 Others

Chapter 9 Market estimates and forecast, by Region, 2021 - 2034 (USD Billion & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 General Dynamics Mission Systems

- 10.1.2 Deep Ocean Engineering, Inc.

- 10.1.3 Nido Robotics

- 10.1.4 Oceanbotics

- 10.1.5 Neptune Robotics

- 10.1.6 Terradepth

- 10.1.7 SeaDrone Inc.

- 10.1.8 Edgerov (Notilo Plus)

- 10.1.9 Autonomous Robotics Ltd.

- 10.2 Regional Key Players

- 10.2.1 North America

- 10.2.1.1 Oceaneering International, Inc.

- 10.2.1.2 Lockheed Martin Corporation

- 10.2.1.3 Teledyne Marine

- 10.2.2 Europe

- 10.2.2.1 Kongsberg Maritime

- 10.2.2.2 Saab Group

- 10.2.2.3 Atlas Elektronik

- 10.2.3 Asia-Pacific

- 10.2.3.1 QYSEA Technology

- 10.2.3.2 PowerVision Inc.

- 10.2.3.3 Youcan Robotics(Shanghai) Co., Ltd.

- 10.2.1 North America

- 10.3 Disruptors / Niche Players

- 10.3.1 Blueye Robotics

- 10.3.2 Eelume AS

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日