|

市場調査レポート

商品コード

1801874

液体膜の市場機会、成長促進要因、産業動向分析、2025~2034年予測Liquid Membrane Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 液体膜の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年08月04日

発行: Global Market Insights Inc.

ページ情報: 英文 192 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

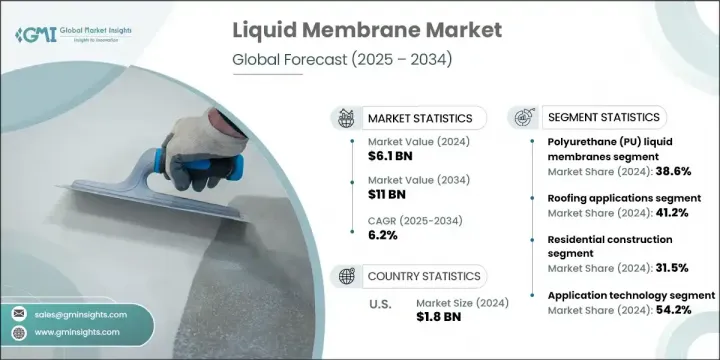

液体膜の世界市場規模は、2024年に61億米ドルとなり、CAGR 6.2%で成長し、2034年には110億米ドルに達すると予測されています。

市場の成長は、インフラ投資の増加、建築要件の進化、官民連携プロジェクトの増加が主要因です。改築や新築プロジェクトでは、商業、住宅、工業構造物全般にわたるエネルギー効率義務や防湿規定への適合を理由に、液状膜が採用されています。新興市場では、シート状のメンブレンに比べ硬化が早く、施工が簡単で寿命が長いため、採用が増加しています。急速な都市化、垂直建築の動向、サステイナブル建築物認証の推進も、このセグメントにおけるポリウレタン、アクリル、セメント系配合の需要を加速しています。

長期的な防水性能と強力な耐薬品性を提供する先進的な液状膜は、気候が不安定な地域の屋上デッキ、地下室、露出した屋根などの課題用途での使用が増加しています。変性ポリウレタンの配合は、強固な接着特性を維持しながら、優れた伸長性、耐紫外線性、透湿性で注目を集めています。VOC含有量の少ないエコフレンドリーアクリルベース膜は、その手頃な価格と環境適合性から、低勾配の屋根、バルコニー、金属構造物に広く採用されています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 61億米ドル |

| 予測金額 | 110億米ドル |

| CAGR | 6.2% |

ポリウレタン(PU)液体膜セグメントは2024年に最大のシェアを占め、総売上高の38.6%を占め、2034年のCAGRは6.8%以上の成長が見込まれます。弾力性、紫外線暴露下での耐久性、複雑な建築デザインへの適合性により、商用ルーフィングとインフラプロジェクトの両方に非常に適しています。その人気は、密集した都市建設地帯で長寿命化のために高性能防水が必要とされる改修工事で拡大しています。

ルーフィング用途セグメントは2024年に41.2%のシェアを占め、2034年のCAGRは5.6%と予測されます。このセグメントの成長は、特に欧州のと北米の都市部における商業ビルや住宅の改修投資が後押ししています。液状膜は、その施工の容易さ、紫外線に対する耐性、優れたクラック橋渡し能力により、屋根用として引き続き支持されています。また、省エネ屋根や太陽電池対応屋根の設置が増加していることも、屋根材セグメント全体の需要を支えています。

米国の液体膜2024年の市場シェアは82%で18億米ドルに達します。同国の優位性は、その確立された建設環境と、防水とエネルギー効率の高い建物外壁への投資の増加によるものです。連邦政府による環境・水インフラへの支出は1,220億米ドルを超え、公共インフラ開発における液状膜の役割と国全体の建物復旧努力がさらに強調されています。

世界の液体膜市場を形成している主要企業には、BASF SE、Sika AG、Soprema Group、Tremco Incorporated、Carlisle Companies Inc.などがあります。液体膜市場におけるプレゼンスを強化するため、主要企業はいくつかの戦略的イニシアチブを展開しています。これには、特定の気候や用途のニーズを満たす製品ラインの拡大、より高い弾性、UV保護、環境適合性を備えた先進的配合の研究開発への多額の投資などが含まれます。インフラ開発業者、請負業者、建築家とのパートナーシップにより、大規模プロジェクト向けにカスタマイズ型ソリューションが可能になっています。また、多くの企業が持続可能性に重点を置き、グリーンビルディング基準に適合する低VOC製品やリサイクル可能な製品を開発しています。特に成長率の高い新興市場での地域拡大や、スマートアプリケーション技術の統合は、より幅広い市場への浸透と長期的な顧客ロイヤリティの促進に役立っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 産業への影響要因

- 促進要因

- 建設産業の需要増加

- インフラ開発と都市化

- 建物の耐久性への重点化

- 産業の潜在的リスク・課題

- 原料価格の変動

- 技術的な応用上の課題

- 市場機会

- サステイナブルバイオベースソリューション

- スマート膜技術

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- 価格動向

- 地域別

- 製品タイプ別

- 将来の市場動向

- 技術とイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- サステイナブルプラクティス

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- エコフレンドリー取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡大計画

第5章 市場推定・予測:製品タイプ別、2021~2034年

- 主要動向

- ポリウレタン(PU)液体膜

- 単一コンポーネントPUシステム

- 2成分PUシステム

- 芳香族PU膜

- 脂肪族PU膜

- バイオベースPU膜

- アクリル液膜

- 水性アクリルシステム

- 溶剤系アクリル系

- 純粋なアクリル膜

- 改質アクリル膜

- セメント質液体膜

- 軟質セメント系

- 硬質セメント系

- ポリマー改質セメント質

- 結晶防水システム

- ハイブリッド膜と特殊膜

- ポリウレアシステム

- シリコーンベース膜

- ビチューメン改質システム

- その他の特殊配合

第6章 市場推定・予測:用途別、2021~2034年

- 主要動向

- 屋根材用途

- 平屋根の防水

- 傾斜屋根の用途

- グリーン屋根システム

- 屋根の改修と修理

- 地下防水

- 地下室の防水

- 基礎防水

- 地下構造物

- トンネル防水

- 地上用途

- バルコニーとテラスの防水

- 浴室と湿潤場所の防水

- ファサードと壁の保護

- プールの防水

- インフラ用途

- 橋梁デッキの防水

- 駐車場デッキ用途

- 水処理施設

- 産業用床コーティング

- 特殊用途

- 海洋と沖合構造物

- 交通インフラ

- 農業用途

- 鉱業と重工業

第7章 市場推定・予測:最終用途産業別、2021~2034年

- 主要動向

- 住宅建設

- 新築住宅建設

- 住宅改修と修理

- 集合住宅

- 一戸建て住宅

- 商業建設

- オフィスビル

- 小売店とショッピングセンター

- ホスピタリティとエンターテイメント

- ヘルスケア施設

- 産業建設

- 製造施設

- 倉庫と配送センター

- 化学とプロセス産業

- 飲食施設

- インフラと公共事業

- 交通インフラ

- 水と廃水処理

- エネルギーと発電

- 政府機関と公共施設

第8章 市場推定・予測:技術別、2021~2034年

- 主要動向

- 応用技術

- 冷間応用システム

- 温間応用システム

- スプレー塗布システム

- ブラシ/ローラー塗布システム

- 硬化技術

- 湿気硬化システム

- 熱硬化システム

- UV硬化システム

- 化学硬化システム

- パフォーマンス技術

- 標準パフォーマンスシステム

- 高性能システム

- 特殊パフォーマンスシステム

- スマート応答性システム

第9章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他のラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他の中東・アフリカ

第10章 企業プロファイル

- Sika AG

- BASF SE

- Tremco Incorporated

- Carlisle Companies Inc.

- Soprema Group

- GAF Materials Corporation

- Johns Manville Corporation

- Firestone Building Products

- Dow Chemical Company

- Huntsman Corporation

- Pidilite Industries Limited(インド)

- Fosroc International Limited(英国)

- MAPEI S.p.A.(イタリア)

The Global Liquid Membrane Market was valued at USD 6.1 billion in 2024 and is estimated to grow at a CAGR of 6.2% to reach USD 11 billion by 2034. Growth in the market is largely driven by rising infrastructure investments, evolving architectural requirements, and an increase in public-private partnership projects. Renovation and new construction projects are embracing liquid membranes due to their compliance with energy efficiency mandates and moisture protection codes across commercial, residential, and industrial structures. Emerging markets are seeing increased adoption because of the fast-curing nature, easy application, and extended lifespan of these materials compared to sheet membranes. Rapid urbanization, vertical construction trends, and a push for sustainable building certifications are also accelerating demand for polyurethane, acrylic, and cementitious formulations in this space.

Advanced liquid membranes offering long-term waterproofing performance and strong chemical resistance are seeing increased usage in challenging applications like podium decks, basements, and exposed roofs in regions with volatile climates. Modified polyurethane formulations are gaining attention for their superior elongation, UV resistance, and breathability while maintaining solid adhesion properties. Eco-friendly acrylic-based membranes with low VOC content are being widely adopted for use on low-slope roofs, balconies, and metal structures, due to their affordability and environmental compliance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.1 Billion |

| Forecast Value | $11 Billion |

| CAGR | 6.2% |

The polyurethane (PU) liquid membranes segment held the largest share in 2024, contributing 38.6% of total revenue and are expected to grow at over 6.8% CAGR through 2034. Their elasticity, durability under UV exposure, and compatibility with complex architectural designs have made them highly suitable for both commercial roofing and infrastructure projects. Their popularity is expanding across retrofitting works where high-performance waterproofing is required for extended lifespans in dense urban construction zones.

The roofing applications segment held 41.2% share in 2024 and is forecasted to grow at a CAGR of 5.6% through 2034. Growth in this segment is fueled by investments in commercial and residential building upgrades, particularly across urban regions in Europe and North America. Liquid membranes continue to be favored for roofing due to their ease of application, resistance to UV rays, and superior crack-bridging capabilities. Rising installations of energy-saving roofs and solar-compatible designs are also supporting demand across the roofing segment.

United States Liquid Membrane Market held 82% share contributing USD 1.8 billion in 2024. The country's dominance stems from its well-established construction landscape and growing investments in waterproofing and energy-efficient building envelopes. Robust federal spending on environmental and water infrastructure, which topped USD 122 billion, further underscores the role of liquid membranes in public infrastructure development and building recovery efforts across the nation.

Top companies shaping the Global Liquid Membrane Market include BASF SE, Sika AG, Soprema Group, Tremco Incorporated, and Carlisle Companies Inc. To strengthen their presence in the liquid membrane market, leading companies are deploying several strategic initiatives. These include expanding product lines to meet specific climate and application needs, investing heavily in R&D for advanced formulations with higher elasticity, UV protection, and eco-compliance. Partnerships with infrastructure developers, contractors, and architects are enabling customized solutions for large-scale projects. Many players are also focusing on sustainability, developing low-VOC and recyclable products to align with green building standards. Regional expansion, especially in high-growth emerging markets, and the integration of smart application technologies are helping to drive broader market penetration and long-term customer loyalty.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Application

- 2.2.4 End use industry

- 2.2.5 Technology

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing construction industry demand

- 3.2.1.2 Infrastructure development and urbanization

- 3.2.1.3 Increasing focus on building durability

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Raw material price volatility

- 3.2.2.2 Technical application challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Sustainable and bio-based solutions

- 3.2.3.2 Smart membrane technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Polyurethane (PU) liquid membranes

- 5.2.1 Single component PU systems

- 5.2.2 Two-component PU systems

- 5.2.3 Aromatic PU membranes

- 5.2.4 Aliphatic PU membranes

- 5.2.5 Bio-based PU membranes

- 5.3 Acrylic liquid membranes

- 5.3.1 Water-based acrylic systems

- 5.3.2 Solvent-based acrylic systems

- 5.3.3 Pure acrylic membranes

- 5.3.4 Modified acrylic membranes

- 5.4 Cementitious liquid membranes

- 5.4.1 Flexible cementitious systems

- 5.4.2 Rigid cementitious systems

- 5.4.3 Polymer-modified cementitious

- 5.4.4 Crystalline waterproofing systems

- 5.5 Hybrid and specialty membranes

- 5.5.1 Polyurea systems

- 5.5.2 Silicone-based membranes

- 5.5.3 Bitumen-modified systems

- 5.5.4 Other specialty formulations

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Roofing applications

- 6.2.1 Flat roof waterproofing

- 6.2.2 Pitched roof applications

- 6.2.3 Green roof systems

- 6.2.4 Roof renovation and repair

- 6.3 Below-grade waterproofing

- 6.3.1 Basement waterproofing

- 6.3.2 Foundation waterproofing

- 6.3.3 Underground structures

- 6.3.4 Tunnel waterproofing

- 6.4 Above-grade applications

- 6.4.1 Balcony and terrace waterproofing

- 6.4.2 Bathroom and wet area waterproofing

- 6.4.3 Facade and wall protection

- 6.4.4 Swimming pool waterproofing

- 6.5 Infrastructure applications

- 6.5.1 Bridge deck waterproofing

- 6.5.2 Parking deck applications

- 6.5.3 Water treatment facilities

- 6.5.4 Industrial floor coatings

- 6.6 Specialty applications

- 6.6.1 Marine and offshore structures

- 6.6.2 Transportation infrastructure

- 6.6.3 Agricultural applications

- 6.6.4 Mining and heavy industry

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Residential Construction

- 7.2.1 New Residential Construction

- 7.2.2 Residential Renovation and Repair

- 7.2.3 Multi-family Housing

- 7.2.4 Single-family Housing

- 7.3 Commercial Construction

- 7.3.1 Office Buildings

- 7.3.2 Retail and Shopping Centers

- 7.3.3 Hospitality and Entertainment

- 7.3.4 Healthcare Facilities

- 7.4 Industrial Construction

- 7.4.1 Manufacturing Facilities

- 7.4.2 Warehouses and Distribution Centers

- 7.4.3 Chemical and Process Industries

- 7.4.4 Food and Beverage Facilities

- 7.5 Infrastructure and Public Works

- 7.5.1 Transportation Infrastructure

- 7.5.2 Water and Wastewater Treatment

- 7.5.3 Energy and Power Generation

- 7.5.4 Government and Public Buildings

Chapter 8 Market Estimates and Forecast, By Technology, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Application Technology

- 8.2.1 Cold Applied Systems

- 8.2.2 Hot Applied Systems

- 8.2.3 Spray Applied Systems

- 8.2.4 Brush/Roller Applied Systems

- 8.3 Curing Technology

- 8.3.1 Moisture Curing Systems

- 8.3.2 Heat Curing Systems

- 8.3.3 UV Curing Systems

- 8.3.4 Chemical Curing Systems

- 8.4 Performance Technology

- 8.4.1 Standard Performance Systems

- 8.4.2 High-Performance Systems

- 8.4.3 Specialty Performance Systems

- 8.4.4 Smart and Responsive Systems

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Sika AG

- 10.2 BASF SE

- 10.3 Tremco Incorporated

- 10.4 Carlisle Companies Inc.

- 10.5 Soprema Group

- 10.6 GAF Materials Corporation

- 10.7 Johns Manville Corporation

- 10.8 Firestone Building Products

- 10.9 Dow Chemical Company

- 10.10 Huntsman Corporation

- 10.11 Pidilite Industries Limited (India)

- 10.12 Fosroc International Limited (UK)

- 10.13 MAPEI S.p.A. (Italy)