太陽電池内蔵建材の市場機会、成長促進要因、産業動向分析、2025~2034年予測

Solar-Integrated Construction Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801868

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

太陽電池内蔵建材の世界市場規模は、2024年に902億米ドルとなり、CAGR 11.2%で成長し、2034年には2,592億米ドルに達すると予測されています。

太陽電池内蔵建材は、太陽光発電(PV)パネルなどの太陽電池技術を組み込んだ建築製品を指します。これらの材料は、ファサード、屋根、窓などの建物の機能部品として機能し、再生可能エネルギーの自家発電を可能にします。このような材料を使用することで、建物は従来型エネルギー源への依存を大幅に減らし、エネルギー効率を向上させることができます。

太陽電池一体型材料に対する需要の高まりは、政府の施策、財政的インセンティブ、サステイナブル開発と気候変動緩和への世界のシフトによってもたらされています。さらに、エネルギー効率の高いサステイナブルインフラに重点を置いたスマートシティ開発の台頭が、市場をさらに後押ししています。世界中の都市が持続可能性目標を達成するためにこうした技術への投資を増やしており、このセグメント全体の成長に寄与しています。技術の進歩と支援施策に重点を置く北米は、最も急成長している市場です。施策、イノベーション、都市の拡大という複合的な力が、太陽電池内蔵建材の世界市場を再構築しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 902億米ドル |

| 予測金額 | 2,592億米ドル |

| CAGR | 11.2% |

2024年、建築物一体型太陽光発電(BIPV)モジュールは211億米ドルを生み出し、市場の主要セグメントを占めました。BIPVモジュールは汎用性が高く、エネルギー生成システムとしてだけでなく、ファサード、屋根、窓などの建物外壁の構造要素としても機能します。この多機能性により、建物の美観を向上させながら持続可能性基準を満たそうとする建築家や開発者に高い人気があります。

住宅・建材は2024年の市場の30.5%を占めます。エネルギー効率の高い住宅に対する消費者の需要の高まりと、二酸化炭素排出量の削減を目的とした政府の奨励策や建築基準法が、住宅建物に太陽電池一体型材料を採用する主要原動力となっています。

2024年、米国の太陽電池内蔵建材市場は232億米ドルと評価され、製造、研究開発(R&D)の進歩、グリーンビルディングの推進に後押しされています。カナダでは、エコフレンドリー建築ソリューションに対する消費者の需要の高まりとともに、サステイナブル開発と同国の気候目標へのコミットメントが市場を牽引しています。

太陽電池内蔵建材世界市場の主要企業には、Trina Solar、JA Solar、Panasonic Corporation、AGC Inc.、Tesla、JinkoSolar、First Solar、Mitrex Solar、SunPower Corporation、Saule Technologies、Onyx Solar、Sisecam Group、Guardian Glass、LONGiなどがあります。太陽電池内蔵建材市場での地位を強化するため、企業は様々な戦略的アプローチを採用しています。これには、製品の性能を向上させ、革新的なソーラー技術を建材に統合するための先進的研究開発への投資が含まれます。また、企業は建設会社や開発業者と戦略的パートナーシップを結び、事業範囲を拡大し、ソーラーソリューションを新しい建築プロジェクトに統合しています。さらに、各社はサステイナブル取り組みに注力し、自社の資材がエネルギー効率が高くエコフレンドリー建築ソリューションに対する需要の高まりに応えられるようにしています。また、政府機関との協力関係を強化し、新興のグリーンビルディング基準に沿った製品提供を行うことも重要な戦略となっています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 産業への影響要因

- 促進要因

- 産業の潜在的リスク・課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- 技術とイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 将来の市場動向

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- サステイナブルプラクティス

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- エコフレンドリー取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡大計画

第5章 市場推定・予測:製品別、2021~2034年

- 主要動向

- BIPVモジュール

- 結晶シリコンBIPVモジュール

- 薄膜BIPVモジュール

- ペロブスカイトBIPVモジュール

- ソーラーガラス

- 透明ソーラーガラス

- 半透明ソーラーガラス

- カラーソーラーガラス

- ソーラータイルとシングル

- セラミックソーラータイル

- ポリマーソーラータイル

- 一体型ソーラーシングル

- ソーラーファサード

- カーテンウォール太陽光発電システム

- 換気ソーラーファサード

- 二重壁ソーラーファサード

- ソーラー天窓と天窓

- 透明ソーラー天窓

- 半透明ソーラー天窓

- ソーラークラッディングシステム

- その他

- 太陽光断熱材

- 太陽光膜システム

- 軟質ソーラーフィルム

第6章 市場推定・予測:用途別、2021~2034年

- 主要動向

- 住宅用途

- 一戸建て住宅

- 集合住宅

- 住宅改修

- 商業用途

- オフィスビル

- 小売店とショッピングセンター

- ホテルとホスピタリティ

- 教育機関

- ヘルスケア施設

- 産業用途

- 製造施設

- 倉庫と配送センター

- 産業用改修

- 施設用途

- 政府庁舎

- 宗教施設

- 文化・レクリエーション施設

- インフラ用途

- 交通ハブ

- 駐車場構造物

- 橋梁とトンネルの統合

第7章 市場推定・予測:技術別、2021~2034年

- 主要動向

- 結晶シリコン技術

- 単結晶シリコン

- 多結晶シリコン

- 薄膜技術

- アモルファスシリコン(a-Si)

- テルル化カドミウム(CdTe)

- 銅インジウムガリウムセレン(CIGS)

- ペロブスカイト技術

- 鉛系ペロブスカイト

- 鉛フリーペロブスカイト

- ペロブスカイト-シリコンタンデム

- 有機太陽電池(OPV)

- 低分子OPV

- ポリマーOPV

- ハイブリッド技術

- ペロブスカイト有機ハイブリッド

- シリコン-ペロブスカイトタンデム

- 新興技術

- 量子ドット太陽電池

- 色素増感太陽電池

第8章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他のラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他の中東・アフリカ

第9章 企業プロファイル

- AGC Inc

- Canadian Solar

- First Solar

- Guardian Glass

- JA Solar

- JinkoSolar

- LONGi

- Mitrex Solar

- Onyx Solar

- Panasonic Corporation

- Saule Technologies

- Sisecam Group

- SunPower Corporation

- Tesla

- Trina Solar

目次

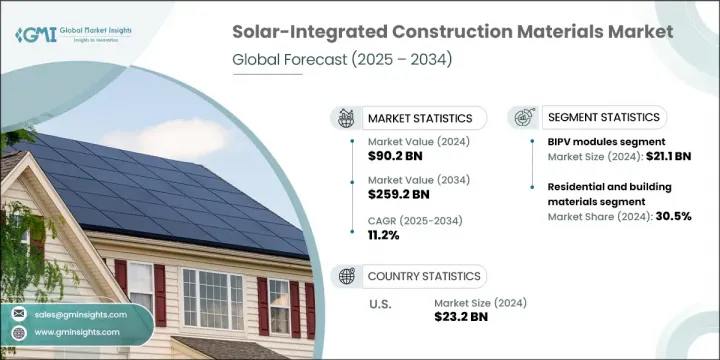

The Global Solar-Integrated Construction Materials Market was valued at USD 90.2 billion in 2024 and is estimated to grow at a CAGR of 11.2% to reach USD 259.2 billion by 2034. Solar-integrated construction materials refer to building products that are embedded with solar technologies, such as photovoltaic (PV) panels. These materials serve as functional components of buildings, including facades, roofing, and windows, enabling the on-site generation of renewable energy. By using such materials, buildings can significantly reduce their reliance on conventional energy sources, improving energy efficiency.

The growing demand for solar-integrated materials is driven by government policies, financial incentives, and a global shift towards sustainable development and climate change mitigation. Additionally, the rise of smart city development, with an emphasis on energy-efficient, sustainable infrastructure, is further supporting the market. Cities worldwide are increasingly investing in such technologies to meet their sustainability targets, contributing to the overall growth of the sector. North America, with its focus on technological advancements and supportive policies, is the fastest-growing market. The combined forces of policy, innovation, and urban expansion are reshaping the global market for solar-integrated construction materials.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $90.2 Billion |

| Forecast Value | $259.2 Billion |

| CAGR | 11.2% |

In 2024, building-integrated photovoltaic (BIPV) modules generated USD 21.1 billion, representing a key segment of the market. BIPV modules are versatile, serving not only as energy-generating systems but also as structural elements for building envelopes, such as facades, roofs, and windows. This multi-functionality makes them highly popular with architects and developers seeking to meet sustainability standards while enhancing building aesthetics.

Residential and building materials made up 30.5% of the market in 2024. Increased consumer demand for energy-efficient homes, along with government incentives and building codes aimed at reducing carbon footprints, are key drivers behind the adoption of solar-integrated materials in residential buildings.

In 2024, the U.S. market for solar-integrated construction materials was valued at USD 23.2 billion, fueled by advancements in manufacturing, research and development (R&D), and a growing push towards green building practices. In Canada, the market is driven by a commitment to sustainable development and the country's climate goals, alongside rising consumer demand for eco-friendly building solutions.

Leading players in the Global Solar-Integrated Construction Materials Market include Trina Solar, JA Solar, Panasonic Corporation, AGC Inc., Tesla, JinkoSolar, First Solar, Mitrex Solar, SunPower Corporation, Saule Technologies, Onyx Solar, Sisecam Group, Guardian Glass, and LONGi. To strengthen their position in the solar-integrated construction materials market, companies are adopting various strategic approaches. These include investing in advanced research and development to enhance product performance and integrate innovative solar technologies into construction materials. Companies are also forming strategic partnerships with construction firms and developers to expand their reach and integrate solar solutions into new building projects. Additionally, firms are focusing on sustainable practices, ensuring their materials meet growing demand for energy-efficient and environmentally friendly building solutions. Increasing collaborations with government bodies and aligning product offerings with emerging green building standards have also been essential strategies.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Product trends

- 2.2.2 Application trends

- 2.2.3 Technology trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Future market trends

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 BIPV modules

- 5.2.1 Crystalline silicon BIPV modules

- 5.2.2 Thin-film BIPV modules

- 5.2.3 Perovskite BIPV modules

- 5.3 Solar glass

- 5.3.1 Transparent solar glass

- 5.3.2 Semi-transparent solar glass

- 5.3.3 Colored solar glass

- 5.4 Solar tiles and shingles

- 5.4.1 Ceramic solar tiles

- 5.4.2 Polymer solar tiles

- 5.4.3 Integrated solar shingles

- 5.5 Solar facades

- 5.5.1 Curtain wall solar systems

- 5.5.2 Ventilated solar facades

- 5.5.3 Double-skin solar facades

- 5.6 Solar skylights and canopies

- 5.6.1 Transparent solar skylights

- 5.6.2 Semi-transparent solar canopies

- 5.7 Solar cladding systems

- 5.8 Others

- 5.8.1 Solar insulation materials

- 5.8.2 Solar membrane systems

- 5.8.3 Flexible solar films

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Residential applications

- 6.2.1 Single-family homes

- 6.2.2 Multi-family residential buildings

- 6.2.3 Residential retrofits

- 6.3 Commercial applications

- 6.3.1 Office buildings

- 6.3.2 Retail and shopping centers

- 6.3.3 Hotels and hospitality

- 6.3.4 Educational institutions

- 6.4 Healthcare facilities

- 6.5 Industrial applications

- 6.5.1 Manufacturing facilities

- 6.5.2 Warehouses and distribution centers

- 6.5.3 Industrial retrofits

- 6.6 Institutional applications

- 6.6.1 Government buildings

- 6.6.2 Religious buildings

- 6.6.3 Cultural and recreational facilities

- 6.7 Infrastructure applications

- 6.7.1 Transportation hubs

- 6.7.2 Parking structures

- 6.7.3 Bridge and tunnel integration

Chapter 7 Market Estimates and Forecast, By Technology, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Crystalline silicon technology

- 7.2.1 Monocrystalline silicon

- 7.2.2 Polycrystalline silicon

- 7.3 Thin-film technology

- 7.3.1 Amorphous silicon (a-Si)

- 7.3.2 Cadmium telluride (CdTe)

- 7.3.3 Copper indium gallium selenide (CIGS)

- 7.4 Perovskite technology

- 7.4.1 Lead-based perovskites

- 7.4.2 Lead-free perovskites

- 7.4.3 Perovskite-silicon tandems

- 7.5 Organic photovoltaics (OPV)

- 7.5.1 Small molecule OPV

- 7.5.2 Polymer OPV

- 7.6 Hybrid technologies

- 7.6.1 Perovskite-organic hybrids

- 7.6.2 Silicon-perovskite tandems

- 7.7 Emerging technologies

- 7.7.1 Quantum dot solar cells

- 7.7.2 Dye-sensitized solar cells

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 AGC Inc

- 9.2 Canadian Solar

- 9.3 First Solar

- 9.4 Guardian Glass

- 9.5 JA Solar

- 9.6 JinkoSolar

- 9.7 LONGi

- 9.8 Mitrex Solar

- 9.9 Onyx Solar

- 9.10 Panasonic Corporation

- 9.11 Saule Technologies

- 9.12 Sisecam Group

- 9.13 SunPower Corporation

- 9.14 Tesla

- 9.15 Trina Solar

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日