ダウンホールコンポーネントと機械加工の市場機会、成長促進要因、産業動向分析、2025~2034年予測

Downhole Component and Machining Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 165 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801866

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

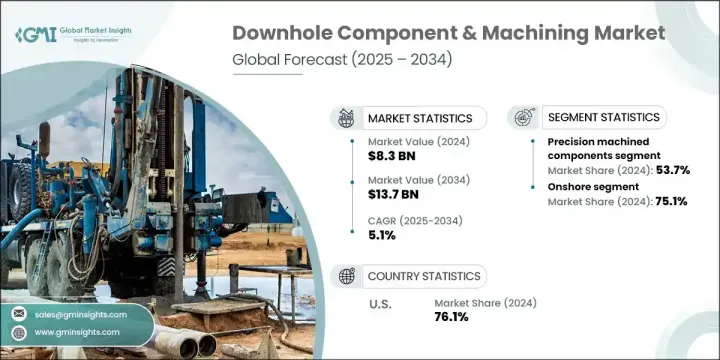

世界のダウンホールコンポーネントと機械加工市場は、2024年に83億米ドルと評価され、CAGR 5.1%で成長し、2034年には137億米ドルに達すると推定されています。

石油・ガス会社がより深く、より過酷な貯留層環境に進出するにつれ、高耐久性材料の需要が急増し続けています。超合金、高性能セラミック、複合材料で作られた部品は、その強度、耐腐食性、極端な温度下での安定性により、ますます不可欠になっています。同時に、石油増進回収と非従来型掘削に重点を置く産業では、先進的流量制御や統合センシングなどの機能を可能にする、極めて精度の高い複雑な機械加工部品へのニーズが高まっています。

ダウンホール機器は、スマート技術の採用により急速に進化しています。精密機械加工技術は、今日の過酷な掘削シナリオで必要とされる、より厳しい公差を持つ複雑な形態の製造を可能にします。現代の油田は、バルブ、モーター、完成システムなどのコンポーネントにインテリジェントセンサを組み込むことで、プロアクティブなオペレーションへとシフトしています。これらのセンサは、圧力、温度、振動、流体構成などの重要な測定基準をリアルタイムで追跡することを可能にし、機器の故障を回避して掘削性能を最適化するのに役立つ予測的洞察を記載しています。このデジタルシフトは、企業が資産を管理し、操業の継続性を維持する方法を再構築しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 83億米ドル |

| 予測金額 | 137億米ドル |

| CAGR | 5.1% |

精密機械加工セグメントの2024年のシェアは53.7%で、2034年のCAGRは4.5%と予想されます。センサとモニタリング機器の使用が増加しているのは、過酷な運転条件下での継続的な性能データに対する産業のニーズが高まっているためです。流量、圧力、リザーバーの挙動などの重要な性能指標は、生産効率、設備の安全性、資源の最適化に関する意思決定の指針となります。オペレーターは、長期の掘削サイクルにわたって安定した性能を発揮する、高精度で耐久性のあるセンサ一体型部品を必要としています。

オンショア部門は2024年に62億米ドルを生み出し、長期サイクルの坑井設計、多段フラクチャリング需要、腐食性流体-これらすべてが堅牢で精密な製造部品を必要とする-に牽引されます。このような環境では、スマートセンサや統合分析プラットフォームによるデジタル化も急速に進んでいます。流量、圧力、温度に関するリアルタイム洞察は、遠隔資産管理、予知保全、プロセスの最適化をサポートし、計画外のダウンタイムを削減しながら運用効率を高めます。

欧州のダウンホールコンポーネントと機械加工市場は、2024年に14億米ドルと評価されました。この地域は、エネルギー転換と自動化に注力しており、石油・ガス機器の進化において極めて重要な役割を果たしています。成熟した海洋油田が最大限の効率を求め、陸上事業が近代化を推し進める中、長寿命でセンサ対応の部品の採用が増え続けています。介入効率、自動モニタリング、デジタル統合における革新が、この地域の展望を形成し、長期的な成長の可能性に拍車をかけています。

世界のダウンホールコンポーネントと機械加工市場の競争環境を形成している主要企業には、Weatherford、SLB、Halliburton、Saipem、Baker Hughesなどがあります。ダウンホールコンポーネントと機械加工市場の主要企業は、競合を強化するために、技術革新、自動化、材料の進歩に注力しています。大手企業は研究開発に多額の投資を行い、過酷な環境に耐える耐熱性と耐腐食性を向上させた次世代材料を開発しています。

さらに、企業はCNCや多軸システムなどの精密機械加工技術を採用し、超精密公差の部品を製造しています。油田サービスプロバイダやデジタルソリューションプロバイダとの戦略的提携により、IoTやセンサ技術のダウンホールツールへの幅広い統合が可能になっています。また、多くの企業は、迅速な納品とカスタマイズをサポートするために、地域の製造拠点とサービスネットワークを拡大しています。これらの戦略は、高性能で耐久性のあるインテリジェントコンポーネントを提供すると同時に、掘削作業全体の運用リスクを低減し、顧客価値を高めることを目的としています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- ディスラプション

- 規制情勢

- 産業への影響要因

- 促進要因

- 産業の潜在的リスク・課題

- 成長可能性分析

- ポーターの分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- PESTEL分析

- 新たな機会と動向

- デジタル化とIoTの統合

- 新興市場への浸透

- 投資分析と将来展望

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析:地域別

- 北米

- 欧州

- アジア太平洋

- 中東・アフリカ

- ラテンアメリカ

- 戦略的取り組み

- 主要なパートナーシップとコラボレーション

- 主要なM&A活動

- 主要イノベーションと新製品

- 市場拡大戦略

- 競合ベンチマーキングの描写

- 戦略ダッシュボード

- イノベーションと技術の情勢

第5章 市場推定・予測:タイプ別、2021~2034年

- 主要動向

- ダウンホールセンサと測定ツール

- ダウンホールモーターとタービン

- ダウンホール制御システム

- 精密機械加工

第6章 市場推定・予測:場所別、2021~2034年

- 主要動向

- オンショア

- オフショア

第7章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ノルウェー

- ドイツ

- イタリア

- 英国

- ロシア

- オランダ

- アジア太平洋

- 中国

- インド

- オーストラリア

- インドネシア

- ベトナム

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- オマーン

- クウェート

- エジプト

- ラテンアメリカ

- ブラジル

- アルゼンチン

- メキシコ

第8章 企業プロファイル

- AMETEK

- Baker Hughes

- BICO Drilling Tools, Inc.

- China Oilfield Services Limited

- Halliburton

- Helmerich & Payne

- Nabors Industries Ltd

- National Oilwell Varco

- NOV

- Oberg Industries

- Penguin Petroleum Services

- Saipem

- Sanmina Corporation

- SLB

- TechnipFMC plc

- Tenaris

- Transocean

- Weatherford

- Wenze

目次

The Global Downhole Component & Machining Market was valued at USD 8.3 billion in 2024 and is estimated to grow at a CAGR of 5.1% to reach USD 13.7 billion by 2034. As oil & gas companies expand into deeper and harsher reservoir environments, the demand for highly durable materials continues to surge. Components made from superalloys, high-performance ceramics, and composite materials are increasingly essential due to their strength, resistance to corrosion, and stability under extreme temperatures. At the same time, the industry's focus on enhanced oil recovery and unconventional drilling is driving the need for intricately machined parts with extreme precision-enabling functions such as advanced flow control and integrated sensing.

Downhole equipment is evolving rapidly with the adoption of smart technologies. Precision machining techniques now enable the production of complex geometries with tighter tolerances needed in today's extreme drilling scenarios. Modern oilfields are shifting toward proactive operations by embedding intelligent sensors in components like valves, motors, and completion systems. These sensors enable real-time tracking of vital metrics, including pressure, temperature, vibration, and fluid makeup, providing predictive insights that help avoid equipment failures and optimize drilling performance. This digital shift is reshaping how companies manage assets and maintain operational continuity.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.3 Billion |

| Forecast Value | $13.7 Billion |

| CAGR | 5.1% |

The precision-machined segment held a 53.7% share in 2024 and is expected to grow at a CAGR of 4.5% through 2034. The rising use of sensors and monitoring instruments is tied to the industry's increasing need for continuous performance data under extreme operational conditions. Key performance indicators such as flow rates, pressure, and reservoir behavior guide decisions around production efficiency, equipment safety, and resource optimization. Operators require highly accurate and durable sensor-integrated parts that deliver consistent performance over long drilling cycles.

The onshore segment generated USD 6.2 billion in 2024, driven by long-cycle well designs, multi-stage fracturing demands, and corrosive fluids-all of which require ruggedized, precision-manufactured components. These environments are also rapidly embracing digitalization through smart sensors and integrated analytics platforms. Real-time insights into flow, pressure, and temperature support remote asset management, predictive maintenance, and process optimization, enhancing operational efficiency while reducing unplanned downtime.

Europe Downhole Component & Machining Market was valued at USD 1.4 billion in 2024. The region's focus on energy transition and automation is playing a pivotal role in the evolution of its oil and gas equipment landscape. As mature offshore fields demand maximum efficiency and onshore operations push for modernization, the adoption of long-life, sensor-enabled components continues to rise. Innovations in intervention efficiency, automated monitoring, and digital integration are shaping the regional outlook and fueling long-term growth potential.

The leading companies shaping the competitive landscape in the Global Downhole Component & Machining Market include Weatherford, SLB, Halliburton, Saipem, and Baker Hughes. Major players in the Downhole Component & Machining Market are focusing on innovation, automation, and material advancement to strengthen their competitive position. Leading firms are investing heavily in R&D to develop next-generation materials with improved thermal and corrosion resistance for hostile environments.

In addition, companies are adopting precision machining technologies such as CNC and multi-axis systems to manufacture components with ultra-tight tolerances. Strategic collaborations with oilfield service providers and digital solution providers are enabling broader integration of IoT and sensor technologies into downhole tools. Many firms are also expanding their regional manufacturing bases and service networks to support rapid delivery and customization. These strategies aim to deliver high-performance, durable, and intelligent components while reducing operational risks and increasing client value across drilling operations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factors affecting the value chain

- 3.1.2 Disruptions

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter’s analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Emerging opportunities & trends

- 3.7.1 Digitalization & IoT integration

- 3.7.2 Emerging market penetration

- 3.8 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic initiatives

- 4.3.1 Key partnerships & collaborations

- 4.3.2 Major M&A activities

- 4.3.3 Key innovations & launches

- 4.3.4 Market expansion strategies

- 4.4 Competitive benchmarking depictions

- 4.5 Strategy dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Downhole sensors and measurement tools

- 5.3 Downhole motors and turbines

- 5.4 Downhole control systems

- 5.5 Precision machined components

Chapter 6 Market Estimates & Forecast, By Location, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Onshore

- 6.3 Offshore

Chapter 7 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Norway

- 7.3.2 Germany

- 7.3.3 Italy

- 7.3.4 UK

- 7.3.5 Russia

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Australia

- 7.4.4 Indonesia

- 7.4.5 Vietnam

- 7.5 Middle East and Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Oman

- 7.5.4 Kuwait

- 7.5.5 Egypt

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

- 7.6.3 Mexico

Chapter 8 Company Profiles

- 8.1 AMETEK

- 8.2 Baker Hughes

- 8.3 BICO Drilling Tools, Inc.

- 8.4 China Oilfield Services Limited

- 8.5 Halliburton

- 8.6 Helmerich & Payne

- 8.7 Nabors Industries Ltd

- 8.8 National Oilwell Varco

- 8.9 NOV

- 8.10 Oberg Industries

- 8.11 Penguin Petroleum Services

- 8.12 Saipem

- 8.13 Sanmina Corporation

- 8.14 SLB

- 8.15 TechnipFMC plc

- 8.16 Tenaris

- 8.17 Transocean

- 8.18 Weatherford

- 8.19 Wenze

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 165 Pages

- 納期

- 2~3営業日