アポトーシスアッセイの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Apoptosis Assay Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034-

医薬品

医薬品

-

バイオ医薬品

,

遺伝子療法/RNAi

,

ゲノム創薬

バイオ医薬品

,

遺伝子療法/RNAi

,

ゲノム創薬

- 発行日

- ページ情報

- 英文 132 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801863

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

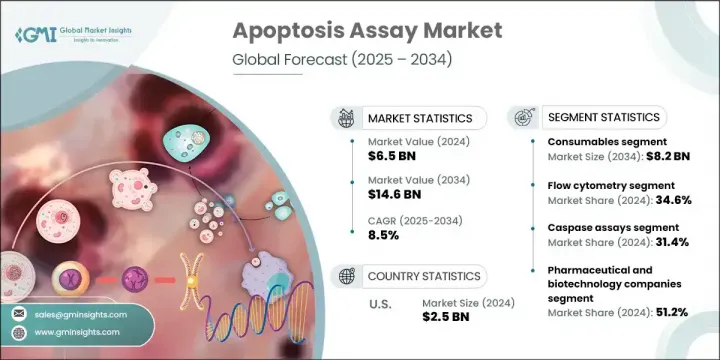

アポトーシスアッセイの世界市場規模は、2024年に65億米ドルとなり、CAGR 8.5%で成長し、2034年には146億米ドルに達すると予測されています。

この市場の着実な拡大は、慢性疾患の有病率の上昇と個別化された治療ソリューションに対する需要の高まりによってもたらされています。先進的イメージングによるアッセイや高性能のフローサイトメトリーなど、細胞分析ツールの革新は、調査方法の精度と効率を大幅に向上させています。さらに、ライフサイエンスへの資金提供の増加や、医薬品開発におけるアポトーシスアッセイの幅広い利用が、先進国、発展途上国を問わず世界の普及を後押ししています。アポトーシスアッセイは、プログラムされた細胞死を同定・測定するために不可欠であり、疾患研究や医薬品イノベーションを推進する上で重要な役割を果たしています。ヘルスケアシステムが標的治療と早期診断を優先する中、アポトーシス測定法の関連性は複数の医療セグメントで拡大し続けています。

個別化医療への注目の高まりは、アポトーシスアッセイ市場の強力な成長エンジンとして作用しています。個人の遺伝的体質や特定の疾患特性に合わせた治療を行うには、正確な細胞レベルの分析が可能な先進的ツールが必要です。アポトーシス・アッセイは、特に神経変性疾患、がん、自己免疫疾患などのセグメントにおいて、細胞が治療にどのように反応するかを評価することを可能にします。この種の細胞反応の追跡は、治療効果の判定、投与戦略の最適化、副作用の最小化に不可欠です。臨床医が治療によって誘導されるアポトーシスをモニターできるようにすることで、これらのアッセイは、より良い結果を得るための治療プロトコルの改良に役立ちます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 65億米ドル |

| 予測金額 | 146億米ドル |

| CAGR | 8.5% |

2024年、フローサイトメトリーセグメントのシェアは34.6%でした。フローサイトメトリーは、そのスピード、正確さ、単一細胞レベルで複数のパラメータ分析を行う能力で支持されています。高性能機能を提供し、様々なアポトーシス指標を同時に同定することに優れています。レーザーベース検出、自動化されたゲーティング機構、ライブデータモニタリングなどの最先端機能により、現代のラボへの統合がサポートされており、大規模な臨床・研究環境に理想的です。

カスパーゼアッセイセグメントは2024年に31.4%のシェアを占めました。これらのアッセイは、アポトーシスで中心的な役割を果たすカスパーゼ酵素の活性を測定することにより、プログラムされた細胞死を追跡するのに役立ちます。免疫学、腫瘍学、薬剤スクリーニングなどのセグメントで、治療が細胞の生存率にどのような影響を与えるかを評価するために広く使用されています。カスパーゼアッセイは、大量スクリーニング環境での使用向けに設計されており、自動化システムとの互換性を特徴とし、柔軟で高感度な性能のために発光と蛍光検出をサポートしています。

米国アポトーシスアッセイ2024年の市場規模は25億米ドル。この成長は、同国の研究開発への旺盛な投資、有利な規制の枠組み、先端診断ツールに関する高い認知度を反映しています。米国市場は、生物医療研究、特に免疫療法や腫瘍学などのセグメントで、拡大性のある自動化ソリューションへの需要が高まっていることから利益を得ています。継続的な公衆衛生への取り組みと民間の技術革新が市場の勢いを強化し続け、アポトーシスアッセイ技術の長期的な普及を確実なものにしています。

アポトーシスアッセイ世界市場の主要企業には、Thermo Fisher Scientific、プロメガ、パーキンエルマー、ベクトン・ディッキンソン・アンド・カンパニー、ジーンコポエイア、タカラバイオ、アジレント技術、ダナハー、ザルトリウス、アブカム、Gバイオサイエンシズ、Merck、ビオチウム、バイオ・ラッド・ラボラトリーズ、バイオテクネなどがあります。これらの企業は積極的に世界市場を形成しています。市場ポジションを強化するため、アポトーシスアッセイ産業の大手企業は、アッセイ感度、スピード、マルチパラメーター機能の革新に重点を置いています。各社は自動化対応プラットフォームで製品ポートフォリオを強化し、より正確な結果を得るためにAI主導の分析を統合しています。製薬会社や学術機関との戦略的提携は、個別化医療や創薬への新たな応用を支援しています。これと並行して、企業は地域提携、現地生産、新興市場向けのカスタマイズ型製品提供を通じて、地理的なリーチを拡大しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- 産業への影響要因

- 促進要因

- 慢性疾患の有病率の増加

- 個別化医療のニーズの高まり

- フローサイトメトリーの技術的進歩

- 毒物学と医薬品の安全性評価における応用の増加

- 産業の潜在的リスク・課題

- 先進的技術の高コスト

- 規制と倫理上の課題

- 市場機会

- がんと神経変性疾患の調査への注目の高まり

- 促進要因

- 成長可能性分析

- 規制情勢

- 技術的進歩

- 現在の技術動向

- 新興技術

- サプライチェーン分析

- 価格分析、2024年

- 将来の市場動向

- ギャップ分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡大計画

第5章 市場推定・予測:製品別、2021~2034年

- 主要動向

- 機器

- 消耗品

- キットと試薬

- マイクロプレート

- その他

第6章 市場推定・予測:技術別、2021~2034年

- 主要動向

- フローサイトメトリー

- 細胞イメージングと分析システム

- 分光光度計

- その他の検出技術

第7章 市場推定・予測:アッセイタイプ別、2021~2034年

- 主要動向

- カスパーゼアッセイ

- DNAセグメント化アッセイ

- ミトコンドリアアッセイ

- アネキシンV

- 細胞透過性アッセイ

第8章 市場推定・予測:最終用途別、2021~2034年

- 主要動向

- 製薬とバイオテクノロジー企業

- 病院と診断ラボ

- 学術研究機関

第9章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- Abcam

- Agilent Technologies

- Becton, Dickinson and Company

- Bio-Rad Laboratories

- Bio-Techne

- BIoTium

- Danaher

- G Biosciences

- GeneCopoeia

- Merck

- PerkinElmer

- Promega

- Sartorius

- Takara Bio

- Thermo Fisher Scientific

目次

The Global Apoptosis Assay Market was valued at USD 6.5 billion in 2024 and is estimated to grow at a CAGR of 8.5% to reach USD 14.6 billion by 2034. The steady expansion of this market is being driven by the rising prevalence of chronic conditions and the growing demand for personalized therapeutic solutions. Innovations in cell analysis tools, including advanced imaging-based assays and high-throughput flow cytometry, are significantly enhancing the accuracy and efficiency of research processes. Additionally, increased funding for life sciences and broader use of apoptosis assays in drug development are fueling global adoption across both developed and developing regions. Apoptosis assays are essential for identifying and measuring programmed cell death and play a key role in advancing disease research and pharmaceutical innovations. As healthcare systems prioritize targeted treatment and early diagnostics, the relevance of apoptosis assays continues to grow across multiple medical fields.

The increasing focus on personalized medicine is acting as a powerful growth engine for the apoptosis assay market. Tailoring medical treatments to an individual's genetic makeup and specific disease characteristics demands advanced tools capable of precise cellular-level analysis. Apoptosis assays enable researchers to evaluate how cells respond to therapies, particularly in fields like neurodegenerative disease, cancer, and autoimmune disorders. This type of cellular response tracking is essential for determining the effectiveness of treatments, optimizing dosing strategies, and minimizing adverse effects. By allowing clinicians to monitor therapy-induced apoptosis, these assays help refine treatment protocols for better outcomes.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.5 Billion |

| Forecast Value | $14.6 Billion |

| CAGR | 8.5% |

In 2024, the flow cytometry segment held a 34.6% share. Flow cytometry is favored for its speed, accuracy, and capacity to perform multi-parameter analysis at the single-cell level. It offers high-throughput functionality and excels in identifying various apoptotic indicators simultaneously. Its integration into modern laboratories is supported by cutting-edge features such as laser-based detection, automated gating mechanisms, and live data monitoring, making it ideal for large-scale clinical and research settings.

The caspase assays segment held a 31.4% share in 2024. These assays are instrumental in tracking programmed cell death by measuring the activity of caspase enzymes, which play a central role in apoptosis. They are extensively used in areas like immunology, oncology, and drug screening to assess how therapeutic agents affect cell viability. Designed for use in high-volume screening environments, caspase assays feature compatibility with automated systems and support luminescent and fluorescent detection for flexible, sensitive performance.

United States Apoptosis Assay Market USD 2.5 billion in 2024. This growth reflects the country's strong investment in R&D, favorable regulatory framework, and high level of awareness around advanced diagnostic tools. The U.S. market benefits from increasing demand for scalable, automated solutions in biomedical research, especially in fields like immunotherapy and oncology. Ongoing public health efforts and private innovation continue to strengthen the market's momentum, ensuring long-term adoption of apoptosis assay technologies.

Key companies in the Global Apoptosis Assay Market include Thermo Fisher Scientific, Promega, PerkinElmer, Becton, Dickinson and Company, GeneCopoeia, Takara Bio, Agilent Technologies, Danaher, Sartorius, Abcam, G Biosciences, Merck, Biotium, Bio-Rad Laboratories, and Bio-Techne. These firms are actively shaping the global market landscape. To reinforce their market position, leading players in the apoptosis assay industry are emphasizing innovation in assay sensitivity, speed, and multi-parameter capabilities. Companies are enhancing product portfolios with automation-ready platforms and integrating AI-driven analytics for more precise results. Strategic collaborations with pharmaceutical firms and academic institutions support new applications in personalized medicine and drug discovery. In parallel, firms are expanding their geographic reach through regional partnerships, localized manufacturing, and tailored product offerings for emerging markets.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Technology trends

- 2.2.4 Assay type trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic diseases

- 3.2.1.2 Growing need for personalized medicine

- 3.2.1.3 Technological advancements in flow cytometry

- 3.2.1.4 Rising application in toxicology and drug safety assessment

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced technologies

- 3.2.2.2 Regulatory and ethical challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Rising focus on cancer and neurodegenerative research

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Supply chain analysis

- 3.7 Pricing analysis, 2024

- 3.8 Future market trends

- 3.9 Gap analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Instruments

- 5.3 Consumables

- 5.3.1 Kits and reagents

- 5.3.2 Microplate

- 5.3.3 Other consumables

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Flow cytometry

- 6.3 Cell imaging and analysis system

- 6.4 Spectrophotometry

- 6.5 Other detection technologies

Chapter 7 Market Estimates and Forecast, By Assay Type, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Caspase assays

- 7.3 DNA fragmentation assays

- 7.4 Mitochondrial assays

- 7.5 Annexin V

- 7.6 Cell permeability assays

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Pharmaceutical and biotechnology companies

- 8.3 Hospital and diagnostic laboratories

- 8.4 Academic and research institutes

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abcam

- 10.2 Agilent Technologies

- 10.3 Becton, Dickinson and Company

- 10.4 Bio-Rad Laboratories

- 10.5 Bio-Techne

- 10.6 Biotium

- 10.7 Danaher

- 10.8 G Biosciences

- 10.9 GeneCopoeia

- 10.10 Merck

- 10.11 PerkinElmer

- 10.12 Promega

- 10.13 Sartorius

- 10.14 Takara Bio

- 10.15 Thermo Fisher Scientific

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 132 Pages

- 納期

- 2~3営業日