|

市場調査レポート

商品コード

1801860

表面処理の市場機会、成長促進要因、産業動向分析、2025~2034年予測Surface Treatments Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 表面処理の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年08月06日

発行: Global Market Insights Inc.

ページ情報: 英文 210 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

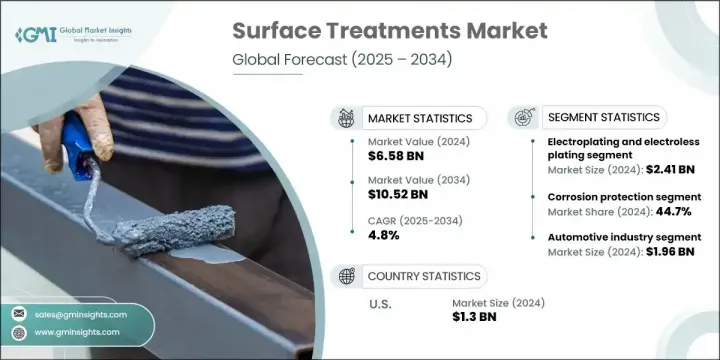

表面処理の世界市場規模は、2024年に65億8,000万米ドルとなり、CAGR 4.8%で成長し、2034年には105億2,000万米ドルに達すると予測されています。

この成長は、自動車、航空宇宙、建設、エレクトロニクスなどのセグメントで表面性能を強化する需要が高まっていることが背景にあります。表面処理は、金属、複合材料、ポリマーを含むさまざまな材料の耐摩耗性、耐食性、接着性、美観などの特性を向上させています。構造材料は湿気、紫外線、化学的劣化などの環境ストレスにさらされるため、表面処理は機能性と長寿命を維持するために不可欠なバリアとして機能します。これらの治療は、シーラント、疎水性コーティング、またはコンクリート、スチール、木材のような基材上のエコフレンドリー保護層などの形で行われます。

また、サステイナブル建築プラクティスへのシフトは、グリーン建築基準に合致する水性と生物由来の治療ソリューションの採用を促しています。より過酷な条件下でより優れた性能を求める産業では、カスタマイズ型処理技術がより重要な役割を果たしています。効率の向上からメンテナンスの必要性の削減まで、表面処理市場は、さまざまな産業で長期的な運用上の利点をもたらす、よりカスタマイズ型エコフレンドリーソリューションへと急速に進化しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 65億8,000万米ドル |

| 予測金額 | 105億2,000万米ドル |

| CAGR | 4.8% |

レーザーテクスチャリング、プラズマ処理、ナノコーティングのような手法への技術投資は、特に電子機器や航空宇宙産業のような精密さに重点を置く産業で人気を集めています。これらの先進的治療では、表面レベルで極めて特殊な性能の修正が可能であり、微視的な不一致でさえ全体的な機能性に影響を与える可能性があります。開発メーカーは、製品の耐久性を促進するカスタマイズ可能な仕上げで、厳しい工業仕様を満たすソリューションを開発し続けています。

電気めっきと無電解めっきセグメントは、2024年に24億1,000万米ドルを生み出しました。これらの広く採用されている方法は、費用対効果の高い腐食保護を実現し、一貫した仕上げと耐摩耗性が不可欠な製造環境では特に有用です。これらと並んで、陽極酸化や化成皮膜などの他の成熟技術も、耐久性と環境適合性を重視する産業で引き続き広く使用されています。これらの方法は保護酸化物層を形成し、表面の弾力性を高めると同時に長期的な性能を記載しています。

腐食保護セグメントは2024年に44.7%のシェアを占めました。この用途は、過酷な環境にさらされる海洋、自動車、インフラセグメントで不可欠であり、長期的な表面保護が必要となっています。コーティングシステム、化成処理、めっき処理は、部品の寿命を延ばし、交換コストを抑え、安全性を高めるのに役立ちます。同様に重要なのが耐摩耗性で、特に航空宇宙機器や高摩擦・高荷重条件下での工具に重点が置かれています。表面強度の向上により、過酷な使用環境においても安定した性能と構造的信頼性を確保することができます。

米国表面処理2024年の市場規模は13億米ドル。そのリーダーシップは、強固な製造エコシステムと先端材料の普及に支えられています。イノベーションは依然として米国の成長の柱であり、防衛、航空宇宙、エレクトロニクスなどの重要産業における強力な研究プログラムに支えられています。この市場では持続可能性も重視されるようになり、エコフレンドリー治療技術や、性能が重視される用途への表面処理の統合への関心が高まっています。

表面処理市場を牽引する主要企業には、Jotun A/S、BASF SE(Surface Technologies部門)、Kansai Paint Co., Ltd.、RPM International Inc.、Axalta Coating Systems Ltd.、Nippon Paint Holdings Co., Ltd.、The Sherwin-Williams Company、Henkel AG & Co.KGaA、PPG Industries Inc.、AkzoNobel N.V.です。表面処理市場で事業を展開する企業は、規制を遵守しながら製品の機能性を高めるため、先進的でエコフレンドリー技術の開発に注力しています。戦略的な研究開発投資により、ナノコーティング、バイオベース表面改質剤、低VOC(揮発性有機化合物)配合などのセグメントで技術革新が進んでいます。航空宇宙、エレクトロニクス、自動車メーカーとのコラボレーションにより、カスタマイズ型性能重視のソリューションを生み出すことができます。市場をリードする企業も、新興市場への参入と製品ポートフォリオの拡充を図るため、合併、買収、合弁事業を通じて世界的プレゼンスを拡大しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 産業への影響要因

- 促進要因

- 産業の潜在的リスク・課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- 技術とイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 将来の市場動向

- 特許情勢

- 貿易統計(HSコード)

- (注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- サステイナブルプラクティス

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- エコフレンドリー取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡大計画

第5章 市場推定・予測:技術タイプ別、2021~2034年

- 主要動向

- 電気めっきと無電解めっき

- 陽極酸化処理と化学変換コーティング

- 溶射技術

- 物理蒸着(PVD)

- 化学蒸着(CVD)

- プラズマ表面治療

- レーザー表面工学

- 新興技術

第6章 市場推定・予測:用途別、2021~2034年

- 主要動向

- 腐食保護

- 耐摩耗性の向上

- 装飾用美麗仕上げ

- 電気と電子特性

- 生体適合性と医療用途

- 熱管理

- 光学特性の強化

第7章 市場推定・予測:エンドユーザー別、2021~2034年

- 主要動向

- 自動車産業

- 航空宇宙と防衛

- 電子機器と半導体

- 産業機械と装置

- 医療機器とヘルスケア

- エネルギーと発電

- 建設とアーキテクチャ

- 海洋とオフショア

第8章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- アルゼンチン

- チリ

- コロンビア

- メキシコ

- その他のラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他の中東・アフリカ

第9章 企業プロファイル

- PPG Industries Inc.

- The Sherwin-Williams Company

- AkzoNobel N.V.

- BASF SE(Surface Technologies Division)

- Henkel AG & Co. KGaA

- Axalta Coating Systems Ltd.

- RPM International Inc.

- Jotun A/S

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

The Global Surface Treatments Market was valued at USD 6.58 billion in 2024 and is estimated to grow at a CAGR of 4.8% to reach USD 10.52 billion by 2034. This growth is fueled by rising demand for enhanced surface performance in sectors like automotive, aerospace, construction, and electronics. Surface treatments improve properties like wear resistance, corrosion protection, adhesion, and aesthetics for a variety of materials, including metals, composites, and polymers. As structural materials face exposure to environmental stressors like moisture, UV rays, and chemical degradation, surface treatments act as essential barriers that preserve functionality and longevity. These treatments come in forms such as sealants, hydrophobic coatings, or eco-conscious protective layers on substrates like concrete, steel, and timber.

The shift toward sustainable building practices has also encouraged the adoption of water-based and bio-sourced treatment solutions, aligning with green construction standards. With industries demanding better performance in harsher conditions, customized treatment technologies are playing a more prominent role. From increasing efficiency to reducing maintenance needs, the surface treatment market is quickly evolving toward more tailored and environmentally sound solutions that deliver long-term operational advantages across various industries.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.58 Billion |

| Forecast Value | $10.52 Billion |

| CAGR | 4.8% |

Technological investments in methods like laser texturing, plasma treatment, and nanocoatings are gaining traction, especially in precision-focused industries such as electronics and aerospace. These advanced treatments allow for highly specific performance modifications at the surface level, where even microscopic inconsistencies can impact overall functionality. Manufacturers continue to develop solutions that meet exacting industrial specifications with customizable finishes that promote product durability.

The electroplating and electroless plating segment generated USD 2.41 billion in 2024. These widely adopted methods deliver cost-effective corrosion protection and are especially useful in manufacturing environments where consistent finish and wear resistance are vital. Alongside these, other mature technologies such as anodizing and chemical conversion coatings continue to see extensive usage in industries that value durability and environmental compatibility. These methods create protective oxide layers that enhance surface resilience while offering long-term performance.

The corrosion protection segment held a 44.7% share in 2024. This application is vital across marine, automotive, and infrastructure sectors where harsh environmental exposure makes long-lasting surface protection a necessity. Coating systems, conversion treatments, and plating processes help extend component life, limit replacement costs, and boost safety. Equally critical is the focus on wear resistance, particularly for aerospace machinery and tools under high-friction, high-load conditions. Enhanced surface strength ensures steady performance and structural reliability in extreme operating environments.

U.S. Surface Treatments Market generated USD 1.3 billion in 2024. Its leadership is backed by a robust manufacturing ecosystem and the widespread use of advanced materials. Innovation remains a central pillar of growth in the U.S., supported by strong research programs across high-stakes industries like defense, aerospace, and electronics. This market also places increasing emphasis on sustainability, driving interest in environmentally responsible treatment technologies and the integration of surface treatments into performance-critical applications.

Key players driving the Surface Treatments Market include Jotun A/S, BASF SE (Surface Technologies Division), Kansai Paint Co., Ltd., RPM International Inc., Axalta Coating Systems Ltd., Nippon Paint Holdings Co., Ltd., The Sherwin-Williams Company, Henkel AG & Co. KGaA, PPG Industries Inc., and AkzoNobel N.V. Companies operating in the surface treatments market are focusing on developing advanced, eco-friendly technologies to enhance product functionality while meeting regulatory compliance. Strategic R&D investments are enabling firms to innovate in areas such as nanocoatings, bio-based surface modifiers, and low-VOC (volatile organic compound) formulations. Collaborations with aerospace, electronics, and automotive manufacturers allow them to create customized, performance-oriented solutions. Market leaders are also expanding their global presence through mergers, acquisitions, and joint ventures to gain access to emerging markets and broaden their product portfolios.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Technology type trends

- 2.2.2 Application trends

- 2.2.3 End user trends

- 2.2.4 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)

(Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Technology Type, 2021-2034 (USD Million) (Kilo tons)

- 5.1 Key trends

- 5.2 Electroplating and electroless plating

- 5.3 Anodizing and chemical conversion coatings

- 5.4 Thermal spraying technologies

- 5.5 Physical vapor deposition (PVD)

- 5.6 Chemical vapor deposition (CVD)

- 5.7 Plasma surface treatment

- 5.8 Laser surface engineering

- 5.9 Emerging technologies

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Million) (Kilo tons)

- 6.1 Key trends

- 6.2 Corrosion protection

- 6.3 Wear resistance enhancement

- 6.4 Decorative and aesthetic finishes

- 6.5 Electrical and electronic properties

- 6.6 Biocompatibility and medical applications

- 6.7 Thermal management

- 6.8 Optical properties enhancement

Chapter 7 Market Estimates and Forecast, By End User, 2021-2034 (USD Million) (Kilo tons)

- 7.1 Key trends

- 7.2 Automotive industry

- 7.3 Aerospace and defense

- 7.4 Electronics and semiconductors

- 7.5 Industrial machinery and equipment

- 7.6 Medical devices and healthcare

- 7.7 Energy and power generation

- 7.8 Construction and architecture

- 7.9 Marine and offshore

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Million) (Kilo tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Argentina

- 8.5.3 Chile

- 8.5.4 Colombia

- 8.5.5 Mexico

- 8.5.6 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 PPG Industries Inc.

- 9.2 The Sherwin-Williams Company

- 9.3 AkzoNobel N.V.

- 9.4 BASF SE (Surface Technologies Division)

- 9.5 Henkel AG & Co. KGaA

- 9.6 Axalta Coating Systems Ltd.

- 9.7 RPM International Inc.

- 9.8 Jotun A/S

- 9.9 Kansai Paint Co., Ltd.

- 9.10 Nippon Paint Holdings Co., Ltd.