グルテンフリー穀粉の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Gluten Free Flour Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801859

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

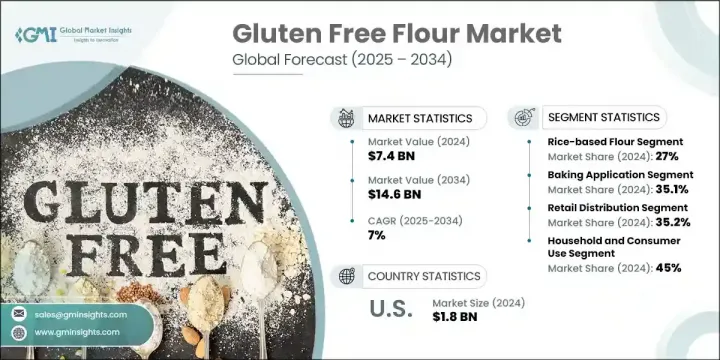

グルテンフリー穀粉の世界市場規模は、2024年に74億米ドルとなり、CAGR 7%で成長し、2034年には146億米ドルに達すると推定されます。

この市場拡大の背景には、グルテン過敏症に対する消費者の意識の高まりに加え、より健康的な食習慣への幅広いシフトや、ウェルネスや体重管理に焦点を当てた食事動向があります。医療的に診断された人であれ、単に健康志向の人であれ、グルテンを含む穀物の代替品を求める人が増えるにつれて、豆類、種子、豆類、穀物、ナッツ類由来の小麦粉の需要は増加の一途をたどっています。この成長を支えているのは、植物性食品やクリーンラベル・ダイエットの人気です。

多くの消費者がグルテンフリー穀粉を選ぶようになったのは、グルテン関連疾患と診断されていなくても、消化器系や健康面でメリットがあると考えられているためです。ホームベーカリーから大規模な業務用食品メーカーまで、グルテンフリー穀粉製品の魅力が市場全体の技術革新と拡大を促進しています。北米は、確立された小売ネットワーク、消費者の意識の高まり、グルテンフリーのライフスタイルの広範な採用により、依然として最前線にあり、これらすべてがこのセグメントでのリーダーシップを強化するのに役立っています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 74億米ドル |

| 予測金額 | 146億米ドル |

| CAGR | 7% |

2024年、米粉部門が最大のシェアを占め、27%を占め、2034年のCAGRは7.3%で成長します。米粉は、そのマイルドな風味、手頃な価格、多様なレシピへの適応性から特に人気が高いです。米粉は、製パンや調理において小麦粉の実用的な代用品として役立ち、グルテンフリー穀粉セグメントの定番となっています。様々な澱粉とグルテンフリーの穀物や豆類を組み合わせたブレンド粉や特殊粉も人気を集めています。これらのブレンド粉は、従来型小麦ベース小麦粉の弾力性と食感を再現するように設計されており、グルテンフリーの焼き菓子の味と品質に対する消費者の期待に応えています。

製パンセグメントは2024年に35.1%のシェアを占めました。クッキー、ケーキ、パン、マフィン、ペストリーなどの焼き菓子は、グルテンフリー穀粉の主要な使用事例であり続けています。この優位性は、セリアック病の診断件数の増加や、健康志向の消費者の関心の高まりに関連しています。小麦粉の配合や結合剤の技術的進歩は、グルテンフリーの焼き菓子の食感、外観、味を大幅に改善し、幅広い消費者を惹きつけ、市場の拡大を支えています。

米国のグルテンフリー穀粉2024年の市場規模は18億米ドルで、2034年までにCAGR 5.9%で成長すると予測されています。米国市場の成長は、栄養に対する一般消費者の関心の高まり、グルテン関連の健康診断の大幅な増加、成分の透明化とアレルゲンフリー食品を求める動きに起因します。小麦粉に代わる健康的な食品を積極的に探す消費者が増えていることから、米国の需要は増加の一途をたどっており、世界のグルテンフリー穀粉市場において最もダイナミックで重要な地域のひとつとなっています。

世界グルテンフリー穀粉市場を形成する著名企業には、Bob's Red Mill Natural Foods、Ancient Harvest(Quinoa Corporation)、Archer Daniels Midland Company(ADM)、Arrowhead Mills(Hain Celestial Group)、General Mills Inc.、Enjoy Life Foods、Cargill Inc.などがあります。グルテンフリー穀粉産業の各社は、市場シェアを維持・拡大するため、技術革新、提携、製品の多様化を組み合わせています。消費者の嗜好の変化に対応するため、古代穀物や高タンパク原料を取り入れることで、グルテンフリーの製品を拡大している企業も多いです。先進的製粉・混合技術への投資は、製品の一貫性と拡大性の向上に役立っています。ブランドはまた、健康志向の購買層にアピールするため、クリーンラベル認証、魅力的な包装、ニーズに合わせたマーケティングにも力を入れています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 産業への影響要因

- 促進要因

- セリアック病の有病率と認知度が上昇

- 高級・職人技の食品市場の成長

- 健康とウェルネスの動向の採用

- クリーンラベルと天然製品の需要

- 産業の潜在的リスク・課題

- 生産コストと原料コストの上昇

- 保存期間が限られており保管に問題がある

- 市場機会

- 古代穀物とスーパーフードの融合

- タンパク質強化小麦粉の開発

- 機能性成分の強化

- 新興市場への浸透

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- 価格動向

- 地域別

- 小麦粉タイプ別

- 将来の市場動向

- 技術とイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- サステイナブルプラクティス

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- エコフレンドリー取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡大計画

第5章 市場推定・予測:小麦粉タイプ別、2021~2034年

- 主要動向

- 米粉

- 白米粉

- 玄米粉

- 甘味米粉

- 特製米粉

- ナッツと種子の粉

- アーモンド粉

- ココナッツ粉

- その他のナッツ粉

- 種子粉

- 根菜と塊茎の粉

- キャッサバ粉

- ジャガイモ粉

- その他の根菜粉

- 古代穀物粉

- キヌア粉

- アマランサス粉

- テフ粉

- キビ粉

- 豆類と豆の粉

- ひよこ豆粉

- レンズ豆粉

- その他の豆粉

- トウモロコシベース小麦粉

- コーンフラワー(マサハリーナ)

- コーンミール

- コーンスターチ

- 特殊小麦粉とブレンド小麦粉

- マルチグレインブレンド

- ベーキングミックスブレンド

- タンパク質強化ブレンド

- 機能性成分ブレンド

第6章 市場推定・予測:用途別、2021~2034年

- 主要動向

- ベーキング用途

- パンとパン製品

- ケーキとペストリー

- クッキーとビスケット

- ピザとフラットブレッド

- 調理と料理の用途

- 増粘とコーティング

- パスタと麺作り

- 朝食用途

- 商業食品製造

- 包装された焼き菓子

- 冷凍食品用途

- スナック食品製造

- 食品サービス用途

- レストランやベーカリーでの使用

- 施設内フードサービス

- ケータリングとイベント

第7章 市場推定・予測:流通チャネル別、2021~2034年

- 主要動向

- 小売流通

- スーパーマーケットとハイパーマーケット

- 健康食品・専門店

- コンビニエンスストア

- オンラインとeコマース

- 主要なeコマースプラットフォーム

- 消費者直接流通チャネル

- モバイルコマース

- 卸売とB2B流通

- 食品卸売業者

- 工業と商業販売

- 代替流通チャネル

- ファーマーズマーケットと地元の販売

- 協同組合と購入グループ

- バルク販売と倉庫販売

- 輸出と国際貿易

第8章 市場推定・予測:最終用途産業別、2021~2034年

- 主要動向

- 家庭用と消費者用

- 家庭でのパン作り愛好家

- 健康志向の家族

- セリアック病とグルテン過敏症の家庭

- 料理愛好家やシェフ

- 商業食品製造

- 焼き菓子メーカー

- スナック食品メーカー

- 冷凍食品会社

- 朝食用シリアルメーカー

- 食品サービス産業

- レストランとカフェ

- パン屋とパティスリー

- ピザやファーストフードチェーン

- ケータリングとイベントサービス

- 施設内フードサービス

- 学校と教育機関

- ヘルスケア施設

- 企業カフェテリア

- 高齢者向けコミュニティ

- 産業用途

- ペットフード製造

- 栄養補助食品の製造

- 医薬品用途

- 化粧品とパーソナルケア

第9章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他のラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他の中東・アフリカ

第10章 企業プロファイル

- Ancient Harvest(Quinoa Corporation)

- Anthony's Goods

- Archer Daniels Midland Company

- Arrowhead Mills(Hain Celestial Group)

- Authentic Foods

- Bob's Red Mill Natural Foods

- Cargill Inc.

- Doves Farm Foods

- Enjoy Life Foods(Mondelez International)

- Firebird Artisan Mills

- General Mills Inc.

- Giusto's Specialty Foods

- Great River Organic Milling

- Hodgson Mill

- Honeyville Food Products

- Ingredion Incorporated

- King Arthur Baking Company

- Maida Place Mills

- Nutiva

- Pamela's Products

- Shipton Mill Ltd.

- Terrasoul Superfoods

目次

The Global Gluten Free Flour Market was valued at USD 7.4 billion in 2024 and is estimated to grow at a CAGR of 7% to reach USD 14.6 billion by 2034. This expansion is fueled by increasing consumer awareness about gluten sensitivity, as well as a broader shift toward healthier eating habits and dietary trends focused on wellness and weight control. As more individuals-whether medically diagnosed or simply health-conscious-seek alternatives to gluten-containing grains, demand for flour derived from legumes, seeds, beans, grains, and nuts continues to rise. The growth is supported by the popularity of plant-based and clean-label diets.

Many consumers are opting for gluten-free flour options due to perceived digestive and wellness benefits, even in the absence of diagnosed gluten-related disorders. From home bakers to large-scale commercial food producers, the appeal of gluten-free flour products is driving innovation and expansion across the market. North America remains at the forefront due to its well-established retail networks, heightened consumer awareness, and widespread adoption of gluten-free lifestyles, all of which help reinforce its leadership in this space.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.4 Billion |

| Forecast Value | $14.6 Billion |

| CAGR | 7% |

In 2024, the rice-based flour segment held the largest share, holding 27% and will grow at a CAGR of 7.3% through 2034. Rice flour is especially popular due to its mild flavor, affordability, and adaptability in a wide variety of recipes. It serves as a practical substitute for wheat flour in baking and cooking, making it a staple in the gluten-free flour sector. Blended and specialty flours, which combine various starches and gluten-free grains or legumes, are also gaining traction. These blends are engineered to replicate the elasticity and texture of traditional wheat-based flours, meeting consumer expectations for taste and quality in gluten-free baked goods.

The baking segment held a 35.1% share in 2024. Baked goods such as cookies, cakes, breads, muffins, and pastries continue to be the leading use case for gluten-free flour. This dominance is linked to the increasing diagnosis of celiac disease and growing interest among health-focused consumers. Technological advancements in flour formulations and binding agents have significantly improved the texture, appearance, and taste of gluten-free baked items, attracting a broader audience and supporting ongoing market expansion.

United States Gluten Free Flour Market generated USD 1.8 billion in 2024 and is projected to grow at a CAGR of 5.9% by 2034. The growth of the U.S. market stems from heightened public interest in nutrition, a significant rise in gluten-related health diagnoses, and a movement toward ingredient transparency and allergen-free foods. With more consumers actively searching for healthier substitutes to wheat flour, demand in the U.S. continues to climb, making it one of the most dynamic and vital regions in the global gluten-free flour space.

Prominent companies shaping the Global Gluten Free Flour Market include Bob's Red Mill Natural Foods, Ancient Harvest (Quinoa Corporation), Archer Daniels Midland Company (ADM), Arrowhead Mills (Hain Celestial Group), General Mills Inc., Enjoy Life Foods, and Cargill Inc. To maintain and grow their market share, companies within the gluten-free flour industry are employing a mix of innovation, partnerships, and product diversification. Many are expanding their gluten-free offerings by incorporating ancient grains and high-protein ingredients to cater to evolving consumer preferences. Investments in advanced milling and blending technologies help improve product consistency and scalability. Brands are also focusing on clean-label certifications, appealing packaging, and tailored marketing to appeal to health-conscious buyers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Flour type

- 2.2.3 Application

- 2.2.4 Distribution channel

- 2.2.5 End use industry

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising celiac disease prevalence and awareness.

- 3.2.1.2 Premium and artisanal food market growth.

- 3.2.1.3 Health and wellness trend adoption.

- 3.2.1.4 Clean label and natural product demand.

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Higher production and raw material costs.

- 3.2.2.2 Limited shelf life and storage issues.

- 3.2.3 Market opportunities

- 3.2.3.1 Ancient grains and superfood integration

- 3.2.3.2 Protein-enriched flour development

- 3.2.3.3 Functional ingredient fortification

- 3.2.3.4 Emerging market penetration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By flour type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Flour Type, 2021-2034 (USD Million & Kilo Tons)

- 5.1 Key Trends

- 5.2 Rice-based flours

- 5.2.1 White rice flour

- 5.2.2 Brown rice flour

- 5.2.3 Sweet rice flour

- 5.2.4 Specialty rice flour

- 5.3 Nut and seed flours

- 5.3.1 Almond flour

- 5.3.2 Coconut flour

- 5.3.3 Other nut flours

- 5.3.4 Seed flours

- 5.4 Root vegetable and tuber flours

- 5.4.1 Cassava flour

- 5.4.2 Potato flour

- 5.4.3 Other root vegetable flours

- 5.5 Ancient grain flours

- 5.5.1 Quinoa flour

- 5.5.2 Amaranth flour

- 5.5.3 Teff flour

- 5.5.4 Millet flour

- 5.6 Legume and bean flours

- 5.6.1 Chickpea flour

- 5.6.2 Lentil flour

- 5.6.3 Other bean flours

- 5.7 Corn-based flours

- 5.7.1 Corn flour (masa harina)

- 5.7.2 Cornmeal

- 5.7.3 Corn starch

- 5.8 Specialty and blend flours

- 5.8.1 Multi-grain blends

- 5.8.2 Baking mix blends

- 5.8.3 Protein-enhanced blends

- 5.8.4 Functional ingredient blends

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Million & Kilo Tons)

- 6.1 Key trends

- 6.2 Baking application

- 6.2.1 Bread and loaf products

- 6.2.2 Cakes and pastries

- 6.2.3 Cookies and biscuits

- 6.2.4 Pizza and flatbreads

- 6.3 Cooking and culinary applications

- 6.3.1 Thickening and coating

- 6.3.2 Pasta and noodle making

- 6.4 Breakfast applications

- 6.4.1 Commercial food manufacturing

- 6.4.2 Packaged baked goods

- 6.4.3 Frozen food application

- 6.4.4 Snack food manufacturing

- 6.5 Foodservice applications

- 6.5.1 Restaurant and bakery use

- 6.5.2 Institutional foodservice

- 6.5.3 Catering and events

Chapter 7 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Million & Kilo Tons)

- 7.1 Key Trends

- 7.2 Retail distribution

- 7.2.1 Supermarkets & hypermarkets

- 7.2.2 Health food and specialty stores

- 7.2.3 Convenience stores

- 7.3 Online and e-commerce

- 7.3.1 Major e-commerce platforms

- 7.3.2 Direct-to-consumer channels

- 7.3.3 Mobile commerce

- 7.4 Wholesale and b2b distribution

- 7.4.1 Food distributors

- 7.4.2 Industrial and commercial sales

- 7.5 Alternative distribution channels

- 7.5.1 Farmers markets and local sales

- 7.5.2 Co-op and buying groups

- 7.5.3 Bulk and warehouse sales

- 7.5.4 Export and international trade

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2021-2034 (USD Million & Kilo Tons)

- 8.1 Key Trends

- 8.2 Household and consumer use

- 8.2.1 Home baking enthusiasts

- 8.2.2 Health-conscious families

- 8.2.3 Celiac and gluten-sensitive households

- 8.2.4 Culinary hobbyists and chefs

- 8.3 Commercial food manufacturing

- 8.3.1 Baked goods manufacturers

- 8.3.2 Snack food producers

- 8.3.3 Frozen food companies

- 8.3.4 Breakfast cereal manufacturers

- 8.4 Foodservice industry

- 8.4.1 Restaurants and cafes

- 8.4.2 Bakeries and patisseries

- 8.4.3 Pizza and fast food chains

- 8.4.4 Catering and event services

- 8.5 Institutional foodservice

- 8.5.1 Schools and educational institutions

- 8.5.2 Healthcare facilities

- 8.5.3 Corporate cafeterias

- 8.5.4 Senior living communities

- 8.6 Industrial applications

- 8.6.1 Pet food manufacturing

- 8.6.2 Nutritional supplement production

- 8.6.3 Pharmaceutical applications

- 8.6.4 Cosmetic and personal care

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Million & Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Ancient Harvest (Quinoa Corporation)

- 10.2 Anthony's Goods

- 10.3 Archer Daniels Midland Company

- 10.4 Arrowhead Mills (Hain Celestial Group)

- 10.5 Authentic Foods

- 10.6 Bob's Red Mill Natural Foods

- 10.7 Cargill Inc.

- 10.8 Doves Farm Foods

- 10.9 Enjoy Life Foods (Mondelez International)

- 10.10 Firebird Artisan Mills

- 10.11 General Mills Inc.

- 10.12 Giusto's Specialty Foods

- 10.13 Great River Organic Milling

- 10.14 Hodgson Mill

- 10.15 Honeyville Food Products

- 10.16 Ingredion Incorporated

- 10.17 King Arthur Baking Company

- 10.18 Maida Place Mills

- 10.19 Nutiva

- 10.20 Pamela's Products

- 10.21 Shipton Mill Ltd.

- 10.22 Terrasoul Superfoods

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日