宝飾品製造・貴金属加工機器の市場機会と成長促進要因、産業動向分析、予測、2025年~2034年

Jewelry Making and Precious Metals Processing Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 250 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801855

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

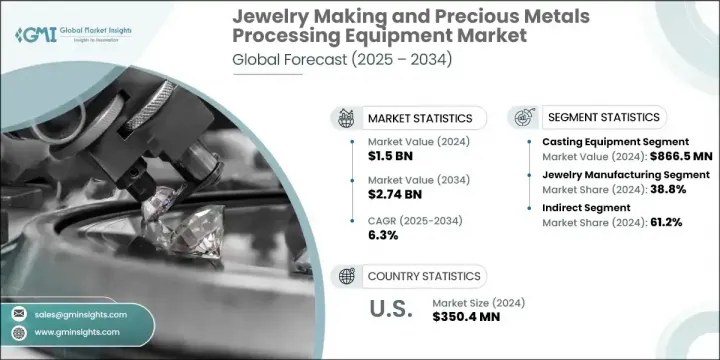

宝飾品製造・貴金属加工機器の世界市場規模は、2024年に15億米ドルとなり、CAGR6.3%で成長し、2034年には27億4,000万米ドルに達すると予測されています。

この市場は、主に高品質でカスタムデザインのジュエリーに対する消費者の関心の高まりによって、力強く持続的な成長を目の当たりにしています。特に、ライフスタイルや個性を表現するジュエリーを求める若い層や、先進国・新興国を問わず富裕層の需要が高まっています。精密製造の必要性が高まるにつれ、業界各社は精度と拡張性を確保する高度な製造技術を導入しています。

コンピューター支援設計ソフトウェア、3Dプリンティングツール、自動化システムは、材料の無駄と生産時間を最小限に抑えながら、詳細で一貫性があり、拡張性のあるデザインを提供するメーカーを支援しています。これらの進歩は、人件費の大幅な削減にも貢献しています。アジア太平洋地域は、確立されたインフラ、熟練した労働力、国内および世界の需要の拡大により、この産業の主要なハブであり続けています。同地域の国々は、低コストの労働力、有利な規制の枠組み、宝飾品の購入を促進する文化的嗜好などの恩恵を受けており、これらが世界市場の展望におけるAPACの影響力を強化しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 15億米ドル |

| 予測金額 | 27億4,000万米ドル |

| CAGR | 6.3% |

鋳造機器セグメントは2024年に8億6,650万米ドルを生み出し、2025年から2034年にかけてCAGR 6.7%で成長すると予測されています。この機器は、大量生産に適していること、カスタマイズの柔軟性があること、コスト効率が高いことなどから、宝飾品や貴金属の用途で高く支持されています。彫刻や溶接ツールのようなレーザーベースのシステムが精密仕上げにますます使用されるようになっている一方で、鋳造技術は、特に新興市場や中小規模の製造業者の間で、スケーラブルな生産に使用され続けています。その適応性と経済的価値は、引き続きこの分野での普及を後押ししています。

宝飾品製造セグメントは2024年に38.8%のシェアを占め、2034年まで6.8%のCAGRを記録すると予想されます。貴金属加工および宝飾機器産業内の主要アプリケーションとして、このセグメントは、消費者需要の高まり、デジタル製造プロセスの進歩、宝飾品生産ネットワークの国際化により拡大しています。工業精錬やリサイクルのような他の用途に比べ、宝飾品製造はより多様なツールと機器を必要とするため、業界の継続的な発展と革新において中心的な役割を担っています。

米国の宝飾品製造・貴金属加工機器市場は76.5%のシェアを占め、2024年には3億5,040万米ドルを創出しました。この強い地位は、同国の高度な製造能力と高級宝飾品ブランドの確立されたプレゼンスに起因しています。米国の製造業者は、CADソフトウェア、3Dプリンティングシステム、レーザーベースのツールなどのデジタル技術を広く活用し、ワークフローを合理化し、製品の生産性を高めています。このような技術的優位性は、高級宝飾品製造分野におけるアメリカの継続的な優位性を支えており、市場全体における重要なプレーヤーとなっています。

世界の宝飾品製造・貴金属加工機器市場を形成する主要企業には、Durston Tools、UIHM、Orotig、Supermelt、Indutherm、LaserStar Technologies、CDOCAST Machinery、Gesswein、Rio Grande、EnvisionTEC、Gravotech、Schultheiss、Contenti、Pepetoolsなどがあります。市場ポジションを強化するため、この分野の企業は製品革新に注力し、デジタル設計能力を拡大し、製造技術をアップグレードしています。設計精度を高め、生産スケジュールを合理化するために、自動化やAI駆動ツールを統合している企業も多いです。ユーザーフレンドリーなインターフェイスとモジュール式の機械に投資することで、企業は小規模な職人工房から大規模な製造業者まで、幅広い顧客ニーズに対応することができます。企業はまた、地域の販売代理店とのパートナーシップを確立し、迅速なアフターサービスを提供することで、世界なプレゼンスを高めています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- カスタムジュエリーや高級ジュエリーの需要増加

- 加工設備の技術的進歩

- 自動化とデジタル設計ツールの利用の増加

- 業界の潜在的リスク&課題

- 高度な機器の高コスト

- 貴金属価格の変動

- 機会

- 宝飾品製造における3Dプリントの出現

- 持続可能で倫理的なジュエリーの需要の増加

- 促進要因

- 成長可能性分析

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 規制環境

- バリューチェーン分析

- 原材料サプライヤーおよび部品メーカー

- 機器メーカーおよびOEM

- 流通チャネルと販売ネットワーク

- 最終用途セグメントとアプリケーション

- アフターサービスプロバイダー

- 価格動向

- 地域別

- 機器の種類別

- 規制情勢

- 標準およびコンプライアンス要件

- 地域規制枠組み

- 認証基準貿易統計

- 主要輸入国

- 主要輸出国

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推定・予測:機器タイプ別、2021年~2034年

- 主要動向

- 鋳造機器

- 溶解・精錬装機器

- スタンピング・成形機器

- レーザー機器

- 研磨・仕上げ機器

- 電気めっき機器

- その他

第6章 市場推定・予測:金属タイプ別、2021年~2034年

- 主要動向

- 金加工機器

- 銀加工機器

- 白金族金属機器

- その他

第7章 市場推定・予測:最終用途産業別、2021年~2034年

- 主要動向

- 宝飾品製造

- 貴金属精錬

- 腕時計製造

- その他

第8章 市場推定・予測:流通チャネル別、2021年~2034年

- 主要動向

- 直接販売

- 間接販売

第9章 市場推定・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- CDOCAST Machinery

- Contenti

- Durston Tools

- EnvisionTEC

- Gesswein

- Gravotech

- Indutherm

- LaserStar Technologies

- Orotig

- Pepetools

- Rio Grande

- Schultheiss

- Superbmelt

- UIHM

目次

The Global Jewelry Making and Precious Metals Processing Equipment Market was valued at USD 1.5 billion in 2024 and is estimated to grow at a CAGR of 6.3% to reach USD 2.74 billion by 2034. This market is witnessing strong and sustained growth, primarily driven by increasing consumer interest in high-quality, custom-designed jewelry. The demand is especially strong among younger demographics and affluent consumers in both established and emerging economies who seek pieces that express their lifestyle and individuality. As the need for precision manufacturing rises, industry players are embracing advanced production technologies that ensure accuracy and scalability.

Computer-aided design software, 3D printing tools, and automated systems are helping manufacturers deliver detailed, consistent, and scalable designs while minimizing material waste and production time. These advancements are also contributing to significant reductions in labor costs. The Asia-Pacific region remains the dominant hub for this industry, thanks to its established infrastructure, skilled labor force, and growing domestic and global demand. Countries across the region benefit from low-cost labor, favorable regulatory frameworks, and cultural preferences that promote jewelry purchases, which collectively strengthen APAC's influence on the global market landscape.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.5 Billion |

| Forecast Value | $2.74 Billion |

| CAGR | 6.3% |

The casting equipment segment generated USD 866.5 million in 2024 and is forecasted to grow at a CAGR of 6.7% between 2025 and 2034. This equipment is highly favored in jewelry and precious metal applications due to its suitability for mass production, flexibility in customization, and cost efficiency. While laser-based systems like engraving and welding tools are increasingly used for precision finishing, casting technology remains the go-to for scalable production, particularly in emerging markets and among small to mid-sized manufacturers. Its adaptability and economic value continue to drive its widespread adoption across the sector.

The jewelry manufacturing segment accounted for a 38.8% share in 2024 and is expected to register a CAGR of 6.8% through 2034. As the leading application within the precious metals processing and jewelry equipment industry, this segment is expanding due to rising consumer demand, advancements in digital manufacturing processes, and the internationalization of jewelry production networks. Compared to other applications like industrial refining or recycling, jewelry production requires a greater variety of tools and equipment, giving it a central role in the industry's continued development and innovation.

U.S. Jewelry Making and Precious Metals Processing Equipment Market held a 76.5% share and generated USD 350.4 million in 2024. This strong position can be attributed to the country's advanced manufacturing capabilities and well-established presence of luxury jewelry brands. American manufacturers widely utilize digital technologies such as CAD software, 3D printing systems, and laser-based tools to streamline workflows and enhance product output. This technological edge supports the country's continued dominance in the high-end jewelry manufacturing space, making it a critical player in the overall market.

Key companies shaping the Global Jewelry Making and Precious Metals Processing Equipment Market include Durston Tools, UIHM, Orotig, Supermelt, Indutherm, LaserStar Technologies, CDOCAST Machinery, Gesswein, Rio Grande, EnvisionTEC, Gravotech, Schultheiss, Contenti, and Pepetools. To reinforce their market position, companies in this sector are focusing on product innovation, expanding digital design capabilities, and upgrading manufacturing technologies. Many are integrating automation and AI-driven tools to enhance design accuracy and streamline production timelines. Investing in user-friendly interfaces and modular machines allows businesses to serve a wide range of customer needs-from small artisan workshops to large-scale manufacturers. Firms are also increasing their global presence by establishing partnerships with regional distributors and offering responsive after-sales support.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.3 Data collection methods

- 1.4 Data mining sources

- 1.4.1 Global

- 1.4.2 Regional/Country

- 1.5 Base estimates and calculations

- 1.5.1 Base year calculation

- 1.5.2 Key trends for market estimation

- 1.6 Primary research and validation

- 1.6.1 Primary sources

- 1.7 Forecast model

- 1.8 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Equipment type

- 2.2.3 Metal type

- 2.2.4 End use Industry

- 2.2.5 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for custom and luxury jewelry

- 3.2.1.2 Technological advancements in processing equipment

- 3.2.1.3 Growing use of automation and digital design tools

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High cost of advanced equipment

- 3.2.2.2 Volatility in precious metal prices

- 3.2.3 Opportunities

- 3.2.3.1 Emergence of 3d printing in jewelry manufacturing

- 3.2.3.2 Increasing demand for sustainable and ethical jewelry

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.6 Regulatory environment

- 3.7 Value Chain Analysis

- 3.7.1 Raw material suppliers and component manufacturers

- 3.7.2 Equipment manufacturers and OEMs

- 3.7.3 Distribution channels and sales networks

- 3.7.4 End use segments and applications

- 3.7.5 After-sales service providers

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By equipment type

- 3.9 Regulatory landscape

- 3.9.1 standards and compliance requirements

- 3.9.2 Regional regulatory frameworks

- 3.10 Certification standards Trade statistics

- 3.10.1 Major importing countries

- 3.10.2 Major exporting countries

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Equipment Type, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Casting equipment

- 5.2.1 Melting and refining equipment

- 5.2.2 Stamping and forming equipment

- 5.3 Laser equipment

- 5.3.1 Polishing and finishing equipment

- 5.3.2 Electroplating equipment

- 5.3.3 Other equipment

Chapter 6 Market Estimates & Forecast, By Metal Type, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Gold processing equipment

- 6.3 Silver processing equipment

- 6.4 Platinum group metals equipment

- 6.5 Other precious metals equipment

Chapter 7 Market Estimates & Forecast, By End Use Industry, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Jewelry manufacturing

- 7.3 Precious metals refining

- 7.4 Watch manufacturing

- 7.5 Other industries

Chapter 8 Market Estimates & Forecast, By Distribution Channel 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 CDOCAST Machinery

- 10.2 Contenti

- 10.3 Durston Tools

- 10.4 EnvisionTEC

- 10.5 Gesswein

- 10.6 Gravotech

- 10.7 Indutherm

- 10.8 LaserStar Technologies

- 10.9 Orotig

- 10.10 Pepetools

- 10.11 Rio Grande

- 10.12 Schultheiss

- 10.13 Superbmelt

- 10.14 UIHM

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 250 Pages

- 納期

- 2~3営業日