加速度計の市場機会と成長促進要因、産業動向分析、2025~2034年予測

Accelerometer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801853

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

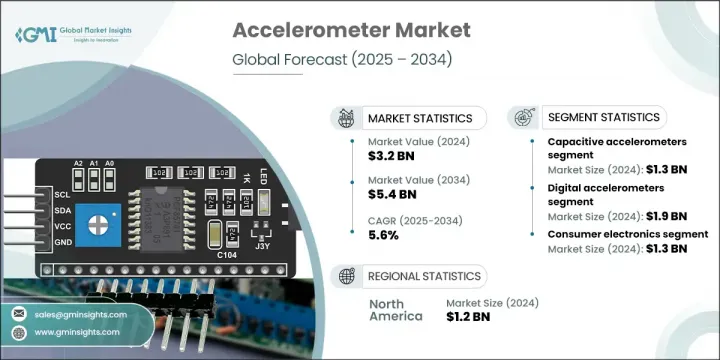

加速度計の世界市場規模は、2024年に32億米ドルとなり、CAGR 5.6%で成長し、2034年には54億米ドルに達すると予測されています。

民生用電子機器、スマートガジェット、産業用システムに加速度計が統合されつつあることが成長を後押ししています。スマートウェアラブル、医療機器、次世代自動車システム(ADAS(先進運転支援技術)に使用されるものを含む)に広く応用されることで、動き、方向、力を感知する方法が変化しています。加速度計は、航空宇宙、ヘルスケア、ロボット工学など、さまざまなセグメントで精度を提供し、リアルタイムのデータ収集にますます頼りにされています。

加速度計は、自動化された産業環境における性能と効率を保証する、予知保全システムにおいても不可欠なものとなっています。IoTの導入が拡大するにつれて、これらのセンサは、家庭、自動車、製造工場にわたって、応答性の高い接続された環境を実現する上で重要な役割を果たしています。加速度計は、その小型化と性能の向上という技術的進歩により、大量生産される民生用アプリケーションから重要なエンタープライズグレードのシステムまで、幅広い関心を集め続けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 32億米ドル |

| 予測金額 | 54億米ドル |

| CAGR | 5.6% |

静電容量型加速度計セグメントは、2024年に13億米ドルを生み出しました。これらのセンサは、コンパクトなフォームファクタ、コスト効率、低エネルギー使用で人気を集めています。エアバッグやモバイルハードウェアのような大衆向け機器での使用が増加しており、需要を牽引しています。さらに、静電容量式MEMSモデルは、正確で再現性の高い動作検出を必要とするインテリジェントプラットフォームに適しています。メーカーは、特に自動車、IoT、ウェアラブルなどの急成長セグメント向けに、信号処理を内蔵した先進的な静電容量式加速度計の製造に研究開発を注いでいます。

デジタル加速度計セグメントは、2024年に19億米ドルを生み出しました。これらのコンポーネントは、プロセッサとの統合が容易で、信号が明瞭で、デジタル通信プロトコルとの互換性があるため、需要が高いです。小型電子機器から産業用システムまで、その汎用性はシームレスな接続性を支えています。デジタル加速度計は、バッテリー寿命の延長とスマート機能を優先する次世代デバイスの要件を満たすために改良されています。各社は、IoT、フィットネス機器、小型消費者向けガジェットなどの需要に対応するため、インテリジェンスを組み込んだより効率的なモデルの開発に注力しています。

北米の加速度計2024年の市場規模は12億米ドルで、2034年までCAGR 5.2%で成長すると予測されます。この地域は、旺盛な防衛資金、先進的インフラ、消費者向け技術の普及拡大から引き続き恩恵を受けています。製造業における自動化の進展とスマート技術の採用拡大により、成長はさらに強化されます。メーカー各社は、その地位を強化するため、現地のOEMと提携し、公共部門の研究開発イニシアティブに参加することが奨励されています。鉱業、航空宇宙、産業オートメーションなどのセクタでイノベーションの取り組みを拡大することは、依然として重要な成長手段です。

加速度計世界市場の各社は、小型化、エネルギー効率、信号精度の向上に注力することで、市場での地位を強化しています。戦略的投資は、デジタルインターフェースと内蔵分析機能を統合したインテリジェントMEMS加速度計を製造するための研究開発に向けられています。ヘルスケア・ウェアラブルや自律走行車などの新興セグメントへの進出により、長期的な収益源が確立されつつあります。いくつかの主要企業は、スマートデバイスや機械へのシームレスな統合を確実にするため、OEMと協力関係を結んでいます。また、サプライチェーンを最適化し、市場アクセスを改善するために、企業は買収や現地での提携を通じて世界の足跡を増やしています。国際安全規格への準拠を重視し、産業別モデルを開発することで、航空宇宙、自動車、産業オートメーションなどのセグメントでの採用が加速しています。主要企業は、STMicroelectronics N.V.、Bosch Sensortec GmbH、ROHM Semiconductor、TE Connectivity、Analog Devices, Inc.、Texas Instruments Incorporated、Microchip Technology Inc、Kearfott Corporation、ASC GmbH、Safran、Hottinger Bruel & Kjaer GmbH、Infineon Technologies AG、Honeywell International Inc.、Rockwell Automation Inc.、Murata Manufacturing、OMEGA Engineering Inc.、TDK InvenSense、LITEF GmbH、Thales Group、NXP Semiconductors、Kistler Groupなどです。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- エコシステム分析

- 産業への影響要因

- 促進要因

- 民生用電子機器製品の普及

- 産業オートメーションと予知保全の台頭

- 航空宇宙と防衛アプリケーションの成長

- IoTとスマートデバイスの利用増加

- ヘルスケアと医療機器の統合の急増

- 落とし穴と課題

- 激しい競合と価格圧力

- マルチセンサシステムによる統合の複雑さ

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- 技術とイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 価格戦略

- 新たなビジネスモデル

- コンプライアンス要件

- 持続可能性対策

- 特許と知的財産分析

- 地政学と貿易の力学

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- 市場集中分析

- 地域別

- 主要参入企業の競合ベンチマーキング

- 財務実績の比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオの比較

- 製品ラインナップの広さ

- 技術

- 革新

- 地理的プレゼンスの比較

- 世界フットプリント分析

- サービスネットワークの範囲

- 地域による市場浸透率

- 競合ポジショニングマトリックス

- リーダー

- 課題者

- フォロワー

- ニッチ参入企業

- 戦略的展望マトリックス

- 財務実績の比較

- 主要開発、2021~2024年

- 合併と買収

- パートナーシップとコラボレーション

- 技術的進歩

- 拡大と投資戦略

- 持続可能性への取り組み

- デジタル変革の取り組み

- 新興企業/スタートアップ企業の競合情勢

第5章 市場推定・予測:タイプ別、2021~2034年

- 主要動向

- 静電容量型加速度計

- 圧電加速度計

- ピエゾ抵抗型加速度計

- サーボ加速度計

- 熱加速度計

- その他

第6章 市場推定・予測:軸構成別、2021~2034年

- 主要動向

- 1軸

- 2軸

- 3軸

- 6軸以上

第7章 市場推定・予測:出力タイプ別、2021~2034年

- 主要動向

- アナログ加速度計

- デジタル加速度計

第8章 市場推定・予測:用途別、2021~2034年

- 主要動向

- 民生用電子機器

- スマートフォンとタブレット

- ウェアラブル

- ゲーム機

- その他

- 自動車

- エアバッグシステム

- 車両安定制御

- ナビゲーションとテレマティクス

- その他

- 工業と製造業

- ロボット工学と自動化

- 状態モニタリング

- 構造健全性モニタリング

- その他

- ヘルスケア

- 患者モニタリング装置

- アクティビティトラッカー

- その他

- 航空宇宙と防衛

- 航空機ナビゲーションシステム

- ミサイル誘導

- 無人航空機とドローン

- その他

- その他

第9章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- 世界の主要企業

- Bosch Sensortec GmbH

- Infineon Technologies AG

- Kearfott Corporation

- NXP Semiconductors

- OMEGA Engineering Inc.

- Rockwell Automation Inc.

- Safran

- STMicroelectronics N.V.

- TE Connectivity

- Texas Instruments Incorporated

- Thales Group

- 地域別主要企業

- 北米

- Analog Devices, Inc.

- Honeywell International Inc.

- Microchip Technology Inc.

- 欧州

- ASC GmbH

- Hottinger Bruel & Kjaer GmbH

- Kistler Group

- Asia-Pacific

- Murata Manufacturing Co., Ltd.

- ROHM Semiconductor

- TDK InvenSense

- 北米

- 破壊的イノベーション/ニッチ参入企業

- LITEF GmbH

目次

The Global Accelerometer Market was valued at USD 3.2 billion in 2024 and is estimated to grow at a CAGR of 5.6% to reach USD 5.4 billion by 2034. The rising integration of accelerometers across consumer electronics, smart gadgets, and industrial systems is fueling growth. Their widespread application in smart wearables, medical devices, and next-gen automotive systems-including those used in advanced driver assistance technologies-is transforming how motion, direction, and force are sensed. Accelerometers are increasingly relied on for real-time data collection, offering precision across multiple fields such as aerospace, healthcare, and robotics.

Accelerometers are also becoming essential in predictive maintenance systems, ensuring performance and efficiency in automated industrial settings. As IoT adoption scales up, these sensors are playing a key role in enabling responsive, connected environments across homes, vehicles, and manufacturing plants. With technological advancements enhancing their compactness and performance, accelerometers continue to attract widespread interest across both high-volume consumer applications and critical enterprise-grade systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.2 Billion |

| Forecast Value | $5.4 Billion |

| CAGR | 5.6% |

The capacitive accelerometers segment generated USD 1.3 billion in 2024. These sensors are gaining traction for their compact form factor, cost-effectiveness, and low energy usage. Their growing use in mass-market devices such as airbags and mobile hardware is driving demand. Additionally, capacitive MEMS models are well-suited for intelligent platforms requiring accurate, repeatable motion detection. Manufacturers are channeling R&D into producing advanced capacitive accelerometers that integrate built-in signal processing, especially for fast-growing sectors like automotive, IoT, and wearables.

The digital accelerometers segment generated USD 1.9 billion in 2024. These components are in high demand due to their ease of integration with processors, strong signal clarity, and compatibility with digital communication protocols. From compact electronics to industrial systems, their versatility supports seamless connectivity. Digital accelerometers are being refined to meet next-gen requirements in devices that prioritize extended battery life and smart functionality. Companies are focusing on developing more efficient models with embedded intelligence to align with demand across IoT, fitness tech, and compact consumer gadgets.

North America Accelerometer Market was valued at USD 1.2 billion in 2024 and is projected to grow at a CAGR of 5.2% through 2034. The region continues to benefit from strong defense funding, advanced infrastructure, and increasing penetration of consumer tech. Growth is further reinforced by heightened automation in manufacturing and the growing adoption of smart technologies. To strengthen their position, manufacturers are encouraged to partner with local OEMs and participate in public sector R&D initiatives. Expanding innovation efforts in sectors like mining, aerospace, and industrial automation remains a key growth avenue.

Companies in the Global Accelerometer Market are strengthening their market position by focusing on miniaturization, energy efficiency, and enhanced signal accuracy. Strategic investments are directed toward R&D to produce intelligent MEMS accelerometers integrated with digital interfaces and built-in analytics. Expansion into emerging sectors like healthcare wearables and autonomous vehicles is enabling long-term revenue streams. Several key players are forming collaborations with OEMs to ensure seamless integration into smart devices and machinery. Companies are also increasing their global footprint through acquisitions and local partnerships to optimize supply chains and improve market access. Emphasis on compliance with international safety standards and development of industry-specific models helps accelerate adoption across verticals such as aerospace, automotive, and industrial automation. STMicroelectronics N.V., Bosch Sensortec GmbH, ROHM Semiconductor, TE Connectivity, Analog Devices, Inc., Texas Instruments Incorporated, Microchip Technology Inc., Kearfott Corporation, ASC GmbH, Safran, Hottinger Bruel & Kjaer GmbH, Infineon Technologies AG, Honeywell International Inc., Rockwell Automation Inc., Murata Manufacturing Co., Ltd., OMEGA Engineering Inc., TDK InvenSense, LITEF GmbH, Thales Group, NXP Semiconductors, and Kistler Group.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Type trend

- 2.2.2 Axis configuration trends

- 2.2.3 Output type trends

- 2.2.4 End use application trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2025-2034 (USD Billion)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry ecosystem analysis

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Proliferation of Consumer Electronics

- 3.3.1.2 Rise in Industrial Automation and Predictive Maintenance

- 3.3.1.3 Growth in Aerospace and Defense Applications

- 3.3.1.4 Increased Usage in IoT and Smart Devices

- 3.3.1.5 Surge in Healthcare and Medical Device Integration

- 3.3.2 Pitfalls and challenges

- 3.3.2.1 High Competition and Price Pressure

- 3.3.2.2 Integration Complexity with Multi-Sensor Systems

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.5.4 Latin America

- 3.5.5 Middle East & Africa

- 3.6 Porter’s analysis

- 3.7 PESTEL analysis

- 3.8 Technology and Innovation landscape

- 3.8.1 Current technological trends

- 3.8.2 Emerging technologies

- 3.9 Price trends

- 3.9.1 By region

- 3.9.2 By product

- 3.10 Pricing strategies

- 3.11 Emerging business models

- 3.12 Compliance requirements

- 3.13 Sustainability measures

- 3.14 Patent and IP analysis

- 3.15 Geopolitical and trade dynamics

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market Concentration Analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market estimates and forecast, by Type, 2021 - 2034 (USD Million & Thousand Units)

- 5.1 Key trends

- 5.2 Capacitive accelerometers

- 5.3 Piezoelectric accelerometers

- 5.4 Piezoresistive accelerometers

- 5.5 Servo accelerometers

- 5.6 Thermal accelerometers

- 5.7 Others

Chapter 6 Market estimates and forecast, by Axis Configuration, 2021 - 2034 (USD Million & Thousand Units)

- 6.1 Key trends

- 6.2 1-axis accelerometers

- 6.3 2-axis accelerometers

- 6.4 3-axis accelerometers

- 6.5 6-axis and above

Chapter 7 Market estimates and forecast, by Output Type, 2021 - 2034 (USD Million & Thousand Units)

- 7.1 Key trends

- 7.2 Analog Accelerometers

- 7.3 Digital Accelerometers

Chapter 8 Market estimates and forecast, by End Use Application, 2021 - 2034 (USD Million & Thousand Units)

- 8.1 Key trends

- 8.2 Consumer electronics

- 8.2.1 Smartphones and tablets

- 8.2.2 Wearables

- 8.2.3 Gaming devices

- 8.2.4 Others

- 8.3 Automotive

- 8.3.1 Airbag systems

- 8.3.2 Vehicle stability control

- 8.3.3 Navigation and telematics

- 8.3.4 Others

- 8.4 Industrial & manufacturing

- 8.4.1 Robotics and automation

- 8.4.2 Condition monitoring

- 8.4.3 Structural health monitoring

- 8.4.4 Others

- 8.5 Healthcare

- 8.5.1 Patient monitoring devices

- 8.5.2 Activity trackers

- 8.5.3 Others

- 8.6 Aerospace and defense

- 8.6.1 Aircraft navigation systems

- 8.6.2 Missile guidance

- 8.6.3 UAVs and drones

- 8.6.4 Others

- 8.7 Others

Chapter 9 Market estimates and forecast, by Region, 2021 - 2034 (USD Million & Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company profiles

- 10.1 Global Key Players

- 10.1.1 Bosch Sensortec GmbH

- 10.1.2 Infineon Technologies AG

- 10.1.3 Kearfott Corporation

- 10.1.4 NXP Semiconductors

- 10.1.5 OMEGA Engineering Inc.

- 10.1.6 Rockwell Automation Inc.

- 10.1.7 Safran

- 10.1.8 STMicroelectronics N.V.

- 10.1.9 TE Connectivity

- 10.1.10 Texas Instruments Incorporated

- 10.1.11 Thales Group

- 10.2 Regional Key Players

- 10.2.1 North America

- 10.2.1.1 Analog Devices, Inc.

- 10.2.1.2 Honeywell International Inc.

- 10.2.1.3 Microchip Technology Inc.

- 10.2.2 Europe

- 10.2.2.1 ASC GmbH

- 10.2.2.2 Hottinger Bruel & Kjaer GmbH

- 10.2.2.3 Kistler Group

- 10.2.3 Asia-Pacific

- 10.2.3.1 Murata Manufacturing Co., Ltd.

- 10.2.3.2 ROHM Semiconductor

- 10.2.3.3 TDK InvenSense

- 10.2.1 North America

- 10.3 Disruptors / Niche Players

- 10.3.1 LITEF GmbH

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日