医薬ロボット市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Pharmaceutical Robots Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801844

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

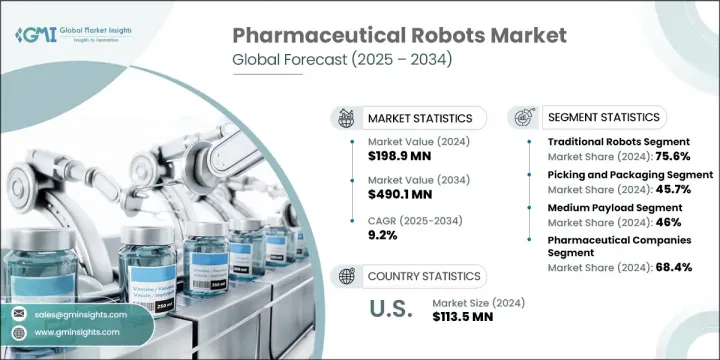

医薬ロボットの世界市場規模は、2024年に1億9,890万米ドルとなり、CAGR 9.2%で成長し、2034年には4億9,010万米ドルに達すると予測されています。

この堅調な成長の背景には、医薬品製造プロセスにおける自動化の進展、研究開発投資の増加、医薬品製造施設における協働ロボットの利用拡大があります。医薬ロボットは、医薬品検査、クリーンルームアプリケーション、生産ワークフローなど、幅広い機能で活用されています。

協働ロボットシステムの採用が増加している背景には、職場の安全性向上、労働力不足への対応、無菌調合やその他の複雑な医薬品製造工程の効率化といったニーズがあります。同時に、次世代治療薬の大幅な進歩や研究開発投資の増加により、製薬会社は業務の自動化を加速させています。このため、拡張性、安全性、一貫した精度を備えたロボットシステムへの需要が高まっています。業界の技術革新と政府の支援が相まって、医薬ロボットが広く採用される基盤が整いつつあり、この分野における自動化の動向はさらに進んでいます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 1億9,890万米ドル |

| 予測金額 | 4億9,010万米ドル |

| CAGR | 9.2% |

2024年には、従来型ロボットが75.6%のシェアを占め、その比類なき精度、スピード、ハイエンド製造環境での有効性が牽引しています。中でも多関節ロボットシステムは、マテリアルハンドリングやパッケージングなどの作業において汎用性が高いため、広く導入されています。柔軟な可搬質量と効率性により、多様な医薬品用途に適しています。業界をリードするプレイヤーは、医薬品製造のニーズに対応するため、これらのロボットのアプリケーション範囲の拡大に積極的に取り組んでいます。

ピッキングとパッケージングアプリケーションセグメントは、2024年に45.7%のシェアを占めました。製薬メーカーが業務を合理化できるコンパクトで省スペースなソリューションを求めているため、包装機能におけるロボットシステムの需要は伸び続けています。これらのシステムはまた、作業スペースの利用を最適化することで効率を向上させる。開発企業は、オートメーション・ソリューション・プロバイダーと提携し、進化する医薬品製造の需要に合わせてカスタマイズされたシステムを開発しています。引き続き、包装ワークフローのスピードアップと、生産施設全体の業務生産性の向上に焦点が当てられています。

米国の医薬ロボット市場規模は2024年に1億1,350万米ドルとなりました。ファイザー、アッヴィ、ジョンソン・エンド・ジョンソン、ブリストル・マイヤーズ・スクイブといった大手製薬企業の存在が、この成長を後押しする上で重要な役割を果たしています。米国を拠点とする企業もまた、コストを最小限に抑えながら透明性と業務効率を向上させるため、ロボット工学やデジタル変革を通じてサプライチェーンの近代化に投資しています。このような効率重視の姿勢が、全国の医薬品製造ラインにおけるロボットシステムの需要を押し上げています。

医薬ロボット市場の主要市場参入企業には、FANUC、OMRON AUTOMATION、EPSON、UNIVERSAL ROBOTS、STAUBLI、ABB、三菱電機、デンソーウェーブ、YASKAWA、KAWASAKI Robotics、KUKAなどがあります。医薬ロボット市場のトップ企業は、市場の足場を固めるために自動化の進展とスマート製造の統合を優先しています。各社は研究開発に投資し、医薬品特有の要件に合わせて安全性と精度を高めた協働ロボットを開発しています。各社は、クリーンルーム基準や無菌環境をサポートする製品ポートフォリオを拡充しています。製薬メーカーとの戦略的パートナーシップにより、包装、マテリアルハンドリング、製剤用にカスタマイズされたソリューションの共同開発が可能になっています。ベンダーはまた、AIと機械学習を活用して、複雑なプロセスに適応できるインテリジェントなロボットシステムを開発しています。さらに、顧客サポートと長期的な信頼性を確保するため、世界展開とアフターサービス網の強化が進められています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 医薬品製造における自動化の需要の高まり

- 医薬品研究開発投資と生産量の増加

- ロボットシステムにおける技術的進歩

- 医薬品製造施設における協働ロボットの導入が急増

- 業界の潜在的リスク&課題

- 初期投資とメンテナンス費用が高め

- 自動化ユニットで働く熟練人員の不足

- 市場機会

- ロボット工学におけるAIと機械学習の統合

- 新興市場への拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- 技術的進歩

- 現在の技術動向

- 新興技術

- バリューチェーン分析

- 世界

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 価格分析、2024

- 市場の進化と歴史的背景

- ポーターの分析

- PESTEL分析

- 将来の市場動向

- ギャップ分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 世界

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 従来のロボット

- 多関節ロボット

- スカラロボット

- デルタ/パラレルロボット

- 直交ロボット

- 双腕ロボット

- 協働ロボット

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- ピッキングと梱包

- 医薬品検査

- ラボ用途

- その他の用途

第7章 市場推計・予測:ペイロード別、2021年~2034年

- 主要動向

- 低(5kg未満)

- 中(6~15kg)

- 高(15kg以上)

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 製薬会社

- 研究ラボ

- その他の用途

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- ABB

- DENSO WAVE

- EPSON

- FANUC

- KAWASAKI Robotics

- KUKA

- MITSUBISHI ELECTRIC

- OMRON AUTOMATION

- STAUBLI

- UNIVERSAL ROBOTS

- YASKAWA

目次

The Global Pharmaceutical Robots Market was valued at USD 198.9 million in 2024 and is estimated to grow at a CAGR of 9.2% to reach USD 490.1 million by 2034. This robust growth is being fueled by increasing automation across pharmaceutical manufacturing processes, heightened investments in R&D, and the expanding use of collaborative robotics within drug production facilities. Pharmaceutical robots are being utilized across a broad range of functions, including drug testing, cleanroom applications, and production workflows.

The rising adoption of collaborative robotic systems is primarily driven by the need for enhanced workplace safety, solutions to address labor shortages, and efficiency in sterile compounding and other complex pharmaceutical processes. At the same time, significant advancements in next-generation therapies and increasing R&D investments are prompting pharmaceutical companies to accelerate the automation of their operations. This is fostering demand for robotics systems that offer scalability, safety, and consistent precision. Industry innovation combined with government support is laying the foundation for widespread adoption of pharmaceutical robots, further advancing the automation trend within the sector.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $198.9 Million |

| Forecast Value | $490.1 Million |

| CAGR | 9.2% |

In 2024, the traditional robots segment held a 75.6% share, driven by their unmatched accuracy, speed, and effectiveness in high-end manufacturing environments. Among these, articulated robotic systems are widely deployed due to their versatility in operations such as material handling and packaging. Their flexible payload capacities and efficiency make them suitable for diverse pharmaceutical applications. Leading industry players are actively working to expand the application scope of these robots to serve pharmaceutical manufacturing needs.

The picking and packaging application segment held a 45.7% share in 2024. The demand for robotic systems in packaging functions continues to grow as pharma manufacturers seek compact, space-saving solutions that can streamline operations. These systems also improve efficiency by optimizing workspace utilization. Companies are partnering with automation solution providers to develop customized systems that align with evolving pharmaceutical production demands. The focus remains on speeding up packaging workflows and enhancing operational output across production facilities.

United States Pharmaceutical Robots Market was valued at USD 113.5 million in 2024. The presence of major pharmaceutical players such as Pfizer, AbbVie, Johnson & Johnson, and Bristol Myers Squibb plays a crucial role in fueling this growth. U.S.-based firms are also investing in modernizing their supply chains through robotics and digital transformation to improve transparency and operational efficiency while minimizing costs. This focus on efficiency is boosting the demand for robotic systems across pharmaceutical production lines nationwide.

Key market participants in the Pharmaceutical Robots Market include FANUC, OMRON AUTOMATION, EPSON, UNIVERSAL ROBOTS, STAUBLI, ABB, MITSUBISHI ELECTRIC, DENSO WAVE, YASKAWA, KAWASAKI Robotics, and KUKA. Top companies in the pharmaceutical robots market are prioritizing automation advancements and smart manufacturing integration to solidify their market foothold. They are investing in R&D to develop collaborative robots with enhanced safety features and precision, tailored to pharmaceutical-specific requirements. Companies are expanding their product portfolios to support cleanroom standards and sterile environments. Strategic partnerships with pharma manufacturers enable co-development of customized solutions for packaging, material handling, and drug formulation. Vendors are also leveraging AI and machine learning to create intelligent robotic systems capable of adapting to complex processes. In addition, global expansion and after-sales service networks are being strengthened to ensure customer support and long-term reliability.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Application trends

- 2.2.4 Payload trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for automation in pharmaceutical manufacturing

- 3.2.1.2 Increasing pharmaceutical research and development investments and production volumes

- 3.2.1.3 Technological advancements in robotic systems

- 3.2.1.4 Surging adoption of collaborative robots in pharma manufacturing facilities

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial investment and maintenance

- 3.2.2.2 Lack of skilled personnel to work in automated units

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of AI and machine learning in robotics

- 3.2.3.2 Expansion in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Value chain analysis

- 3.7 Pharmaceutical robots market in terms of Volume (Units), 2021 -2034

- 3.7.1 Global

- 3.7.2 North America

- 3.7.3 Europe

- 3.7.4 Asia Pacific

- 3.7.5 Latin America

- 3.7.6 MEA

- 3.8 Pricing analysis, 2024

- 3.9 Market evolution and historical context

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Future market trends

- 3.13 Gap analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.2.5 Latin America

- 4.2.6 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Traditional robots

- 5.2.1 Articulated robots

- 5.2.2 SCARA robots

- 5.2.3 Delta/Parallel robots

- 5.2.4 Cartesian robots

- 5.2.5 Dual-arm robots

- 5.3 Collaborative robots

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Picking and packaging

- 6.3 Pharmaceutical drugs inspection

- 6.4 Laboratory applications

- 6.5 Other applications

Chapter 7 Market Estimates and Forecast, By Payload, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Low (Upto 5 kg)

- 7.3 Medium (6-15 kg)

- 7.4 High (more than 15 kg)

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Pharmaceutical companies

- 8.3 Research laboratories

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 ABB

- 10.2 DENSO WAVE

- 10.3 EPSON

- 10.4 FANUC

- 10.5 KAWASAKI Robotics

- 10.6 KUKA

- 10.7 MITSUBISHI ELECTRIC

- 10.8 OMRON AUTOMATION

- 10.9 STAUBLI

- 10.10 UNIVERSAL ROBOTS

- 10.11 YASKAWA

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日