ひび割れ補修用化学品市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Crack Repair Chemicals Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801843

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

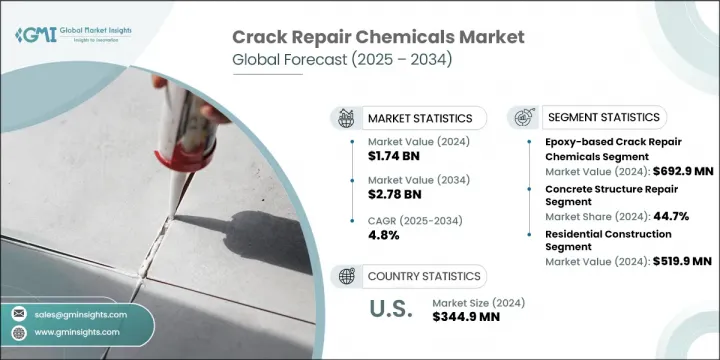

ひび割れ補修用化学品の世界市場規模は、2024年に17億4,000万米ドルとなり、CAGR 4.8%で成長し、2034年には27億8,000万米ドルに達すると予測されています。

この成長は、住宅、商業、インフラ、工業プロジェクトなど、さまざまな分野で耐久性があり、迅速かつ効率的な補修ソリューションに対する需要が高まっていることが背景にあります。これらの化学薬品は、新築だけでなく老朽化した構造物の修復にも不可欠であり、特に道路や橋、公共建築物が摩耗や劣化に直面する先進地域では重要です。また、重要な資産の長寿命化、安全性、性能の向上に重点を置くことも需要を支えています。

材料科学の革新により、ひび割れ補修ソリューションは、より優れた柔軟性、耐薬品性、接着性を提供し、地震、湿気、極端な温度などの過酷な環境条件に耐えられるように設計されています。進行中のインフラ近代化プロジェクトと持続可能な建設慣行の優先順位付けにより、ひび割れ補修用化学品の使用は世界的に拡大し続けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 17億4,000万米ドル |

| 予測金額 | 27億8,000万米ドル |

| CAGR | 4.8% |

2024年、エポキシ系ひび割れ補修材は6億9,290万米ドルを生み出し、その高い強度と耐久性が牽引しました。ポリウレタンを主成分とする化学薬品は、その弾力性と動きや温度変動への適応能力により急速に勢いを増しており、トンネル、橋、交通量の多いゾーンなどの動的環境に理想的です。また、硬化時間が短いため、構造物の補修時のダウンタイムを最小限に抑えることができます。アクリルベースのオプションは、特に予算が優先される非重要用途において、性能と手頃な価格の実用的なバランスを提供します。各タイプは、それぞれ異なる性能要件と環境要求に対応しています。

コンクリート補修分野は、2024年に44.7%のシェアを獲得しました。これは主に、高速道路、建物、産業ユニットなどの主要インフラでコンクリートが広く使用されていることに起因しています。これらの構造物が老朽化するにつれて、完全性を維持することが重要になり、ひび割れ補修用化学品への依存度が高まっています。これらの製品は、強力な接着性、環境ストレスに対する長期的な耐性、さまざまな条件下での耐久性を提供し、構造の安定性と耐用年数の延長を保証します。

米国のひび割れ補修用化学品市場は、2024年に3億4,490万米ドルを創出しました。同国が主導権を握っているのは、インフラ復旧への多額の投資と成熟した建設産業によるものです。同国は、大規模なインフラ・プロジェクトを支援するために、高性能補修材料、特にエポキシ系とポリウレタン系のシステムに重点を置いています。大手企業の存在、強力な研究開発活動、予防保全に関する意識の高まりが、同国の高度な化学補修ソリューションの需要をさらに押し上げています。

ひび割れ補修用化学品市場を牽引する主要企業には、Sika AG、MAPEI S.p.A.、Fosroc International Limited、Dow Inc.、RPM International Inc.、BASF SE、Arkema S.A.、Master Builders Solutions(MBCC Group)、Henkel AG &Co.KGaA、3M Companyです。市場開拓を強化するため、ひび割れ補修用化学品分野の企業は、より高い弾性、耐薬品性、速硬化性を持つ配合物を開発するための研究開発に注力しています。インフラ開発業者や政府との長期供給契約のための主な発展も重要な戦略です。企業は、現地生産と流通を通じて新興市場に進出し、環境規制を満たすために環境に優しい低VOC配合を重視しています。地域の気候課題や建設基準に基づいてソリューションをカスタマイズすることも、競争力を維持し、世界のブランド・ロイヤルティを高めるために行われている戦術です。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 素材タイプ別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- エポキシ系ひび割れ補修用化学品

- 低粘度エポキシ樹脂

- 高弾性エポキシシステム

- 耐湿性エポキシ溶液

- 速硬化エポキシ配合

- ポリウレタンベースのソリューション

- 疎水性ポリウレタングラウト

- 軟性ポリウレタンシーラント

- エクスパンディングポリウレタンシステム

- アクリル系補修材

- 水性アクリルシステム

- 溶剤系アクリル溶液

- 改質アクリルポリマー

- セメント系補修材

- ポリマー改質セメントシステム

- 速硬化セメントモルタル

- 収縮補償セメント

- シラン/シロキサンベースの製品

- その他(ハイブリッドシステム、バイオベース材料)

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- コンクリート構造物の修理

- 建築・建設

- 橋とインフラ

- 産業施設

- ファンデーションの修理

- 住宅基礎

- 商業財団

- 産業基盤

- 舗装と道路の補修

- 高速道路と幹線道路

- 空港の滑走路と誘導路

- 駐車場構造物

- 海洋および沿岸構造物

- 地下およびトンネル用途

- その他(プール、水処理施設)

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 住宅建設

- 新築

- 改修と修理

- メンテナンスサービス

- 商業建設

- オフィスビル

- 小売店とショッピングセンター

- ホスピタリティとエンターテイメント

- 産業建設

- 製造施設

- 倉庫と配送センター

- 発電施設

- インフラと公共事業

- 交通インフラ

- 水と廃水処理

- 政府機関および市町村の建物

第8章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 従来の修復技術

- 注入ベースのシステム

- 表面塗布方法

- 構造補強システム

- 高度な修復技術

- 自己修復システム

- ナノテクノロジーを活用した製品

- スマートで反応性の高い素材

- 新興技術

- バイオベースの治癒システム

- AI支援アプリケーションシステム

- IoT対応監視ソリューション

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第10章 企業プロファイル

- Sika AG

- MAPEI S.p.A.

- RPM International Inc.

- Master Builders Solutions(MBCC Group)

- BASF SE

- Arkema S.A.

- Dow Inc.

- 3M Company

- Henkel AG &Co. KGaA

- FOSROC International Limited

目次

The Global Crack Repair Chemicals Market was valued at USD 1.74 billion in 2024 and is estimated to grow at a CAGR of 4.8% to reach USD 2.78 billion by 2034. This growth is fueled by rising demand for durable, quick, and efficient repair solutions across various sectors, including residential, commercial, infrastructure, and industrial projects. These chemicals are vital not only for new construction but also for restoring aged structures, especially in developed regions where roads, bridges, and public buildings face wear and deterioration. The demand is also supported by a focus on enhancing the longevity, safety, and performance of critical assets.

With innovation in material science, crack repair solutions are being engineered to offer better flexibility, chemical resistance, and adhesion, enabling them to withstand harsh environmental conditions such as earthquakes, moisture, and extreme temperatures. Ongoing infrastructure modernization projects and the prioritization of sustainable construction practices continue to amplify the use of crack repair chemicals globally.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.74 Billion |

| Forecast Value | $2.78 Billion |

| CAGR | 4.8% |

In 2024, the epoxy-based crack repair materials generated USD 692.9 million, driven by their high strength and durability. Polyurethane-based chemicals are gaining rapid momentum due to their elasticity and ability to adjust to movement and temperature fluctuations, making them ideal for dynamic environments such as tunnels, bridges, and high-traffic zones. Their quick curing time also ensures minimal downtime during structural repairs. Acrylic-based options offer a practical balance between performance and affordability, especially in non-critical applications where budget remains a priority. Each type caters to distinct performance requirements and environmental demands.

The concrete repair segment generated 44.7% share in 2024. This is largely attributed to the wide use of concrete in key infrastructure, including highways, buildings, and industrial units. As these structures age, maintaining integrity becomes critical, increasing reliance on crack repair chemicals. These products offer strong adhesion, long-term resistance to environmental stress, and endurance under varying conditions, ensuring structural stability and extended service life.

U.S. Crack Repair Chemicals Market generated USD 344.9 million in 2024. Its leadership stems from substantial investment in infrastructure rehabilitation and a mature construction industry. The country places emphasis on high-performance repair materials-especially epoxy and polyurethane-based systems-to support large-scale infrastructure projects. The presence of major players, strong research and development activity, and increased awareness around preventive maintenance further boost demand for advanced chemical repair solutions across the country.

Key players driving Crack Repair Chemicals Market include Sika AG, MAPEI S.p.A, Fosroc International Limited, Dow Inc., RPM International Inc., BASF SE, Arkema S.A., Master Builders Solutions (MBCC Group), Henkel AG & Co. KGaA, and 3M Company. To strengthen their market footprint, companies in the crack repair chemicals sector are focusing on R&D to develop formulations with higher elasticity, chemical resistance, and quick-setting properties. Partnerships with infrastructure developers and governments for long-term supply contracts are also key strategies. Firms are expanding into emerging markets through localized production and distribution and emphasizing eco-friendly and low-VOC formulations to meet environmental regulations. Customization of solutions based on regional climatic challenges and construction standards is another tactic being used to stay competitive and boost brand loyalty globally.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Application trends

- 2.2.3 End user trends

- 2.2.4 Technology trends

- 2.2.5 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By material type

- 3.9 Future market trends

- 3.10 Technology and Innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent Landscape

- 3.12 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021-2034 (USD Million) (Kilo tons)

- 5.1 Key trends

- 5.2 Epoxy-based crack repair chemicals

- 5.2.1 Low-viscosity epoxy resins

- 5.2.2 High-modulus epoxy systems

- 5.2.3 Moisture-tolerant epoxy solutions

- 5.2.4 Rapid-curing epoxy formulations

- 5.3 Polyurethane-based solutions

- 5.3.1 Hydrophobic polyurethane grouts

- 5.3.2 Flexible polyurethane sealants

- 5.3.3 Expanding polyurethane systems

- 5.4 Acrylic-based repair materials

- 5.4.1 Water-based acrylic systems

- 5.4.2 Solvent-based acrylic solutions

- 5.4.3 Modified acrylic polymers

- 5.5 Cement-based repair compounds

- 5.5.1 Polymer-modified cement systems

- 5.5.2 Rapid-setting cement mortars

- 5.5.3 Shrinkage-compensating cement

- 5.6 Silane/siloxane-based products

- 5.7 Others (hybrid systems, bio-based materials)

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Million) (Kilo tons)

- 6.1 Key trends

- 6.2 Concrete structure repair

- 6.2.1 Building and construction

- 6.2.2 Bridge and infrastructure

- 6.2.3 Industrial facilities

- 6.3 Foundation repair

- 6.3.1 Residential foundations

- 6.3.2 Commercial foundations

- 6.3.3 Industrial foundations

- 6.4 Pavement and road repair

- 6.4.1 Highway and arterial roads

- 6.4.2 Airport runways and taxiways

- 6.4.3 Parking structures

- 6.5 Marine and coastal structures

- 6.6 Underground and tunnel applications

- 6.7 Others (swimming pools, water treatment facilities)

Chapter 7 Market Estimates and Forecast, By End Use, 2021-2034 (USD Million) (Kilo tons)

- 7.1 Key trends

- 7.2 Residential construction

- 7.2.1 New construction

- 7.2.2 Renovation and repair

- 7.2.3 Maintenance services

- 7.3 Commercial construction

- 7.3.1 Office buildings

- 7.3.2 Retail and shopping centers

- 7.3.3 Hospitality and entertainment

- 7.4 Industrial construction

- 7.4.1 Manufacturing facilities

- 7.4.2 Warehouses and distribution centers

- 7.4.3 Power generation facilities

- 7.5 Infrastructure and public works

- 7.5.1 Transportation infrastructure

- 7.5.2 Water and wastewater treatment

- 7.5.3 Government and municipal buildings

Chapter 8 Market Estimates and Forecast, By Technology, 2021-2034 (USD Million) (Kilo tons)

- 8.1 Key trends

- 8.2 Conventional repair technologies

- 8.2.1 Injection-based systems

- 8.2.2 Surface application methods

- 8.2.3 Structural strengthening systems

- 8.3 Advanced repair technologies

- 8.3.1 Self-healing systems

- 8.3.2 Nanotechnology-enhanced products

- 8.3.3 Smart and responsive materials

- 8.4 Emerging technologies

- 8.4.1 Bio-based healing systems

- 8.4.2 Ai-assisted application systems

- 8.4.3 IoT-enabled monitoring solutions

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Million) (Kilo tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Sika AG

- 10.2 MAPEI S.p.A.

- 10.3 RPM International Inc.

- 10.4 Master Builders Solutions (MBCC Group)

- 10.5 BASF SE

- 10.6 Arkema S.A.

- 10.7 Dow Inc.

- 10.8 3M Company

- 10.9 Henkel AG & Co. KGaA

- 10.10 FOSROC International Limited

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日