オートバイ用カーボンセラミックブレーキローターの市場機会と促進要因、産業動向分析、予測、2025年~2034年

Motorcycle Carbon Ceramic Brake Rotors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801842

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

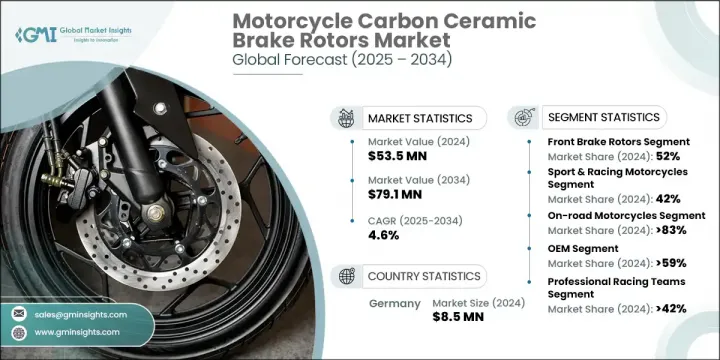

オートバイ用カーボンセラミックブレーキローターの世界市場は、2024年には5,350万米ドルとなり、CAGR 4.6%で成長し、2034年には7,910万米ドルに達すると予測されています。

この市場の成長を牽引しているのは、特にスポーツおよびレースカテゴリーにおける高性能および高級オートバイの人気の高まりです。これらのブレーキ・ローターは、軽量構造、優れた耐熱性、ブレーキ精度の向上により、アグレッシブなライディングや高速コントロールに最適であるとして支持されています。これらのシステムの魅力は、安全性、耐久性、メンテナンスの軽減を優先するライダーの間で特に強いです。複合材料の革新は、過酷なライディング条件下でも、これらのローターの寿命と熱管理を強化しています。

欧州や北米のようなモータースポーツが盛んな地域で需要が拡大しているため、大手メーカーは先進的な冷却技術とモジュール式ローター構造を活用して、公道走行可能なオートバイにサーキットレベルの性能をもたらそうとしています。サプライヤーは、安全性、効率性、性能に関するOEM仕様と消費者の期待に合わせて設計を調整しています。プレミアムセグメントの成長により、EBC Brakes、Sunstar、Braketechなどのメーカーは、アフターマーケットとファクトリーフィットの両方のチャネルで製品を拡大しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 5,350万米ドル |

| 予測金額 | 7,910万米ドル |

| CAGR | 4.6% |

2024年、フロントブレーキローターセグメントのシェアは52%で、2034年までのCAGRは5%と予測されます。制動力の大半はフロントローターが担っているため、性能のアップグレードや技術革新はこれらの部品を中心に行われています。ベンチレーテッドローターやスリットローターのような技術は、スポーツツーリングやスーパーバイクの販売台数が増加し続ける中、人気を集めています。Galfer BrakesやBremboなどのメーカーは、この需要に応えるため、高効率ローターシステムを積極的にリリースしています。

スポーツおよびレース用オートバイセグメントは、2024年に50%のシェアを占める。これらのオートバイでは、高速走行時の比類ないブレーキ制御と熱バランスが要求されます。このセグメントでは、長時間の高性能使用に対応するため、熱歪みを低減し、通気性を高めたローターの製品開発が進んでいます。ライダーは、アグレッシブな条件下でも安定した制動力を発揮するカーボンセラミックを好み、サーキット走行にインスパイアされたモデルでの採用が増加しています。

ドイツのオートバイ用カーボンセラミックブレーキローターの市場シェアは50%で、2024年には850万米ドルを生み出します。同国のリーダーシップは、強固なモータースポーツ文化と強力なOEMサプライヤーネットワークに支えられています。セラミック複合材料の技術革新は、特に電動オートバイ向けの、より軽量で耐熱性の高い材料の需要によって加速しています。先進的な研究開発センターが台頭し、効率性と安全性に重点を置いてローター技術の限界に課題しており、ドイツは世界の製品進化に大きく貢献しています。

オートバイ用カーボンセラミックブレーキローター市場を形成する主要プレーヤーには、AP Racing、Braketech、SICOM Brakes、Galfer Brakes、Sunstar、Brembo S.p.A.、EBC Brakesなどがあります。この市場のメーカーは、熱安定性、軽量構造、エアフローの改善に焦点を当てた高度なローター技術で製品ポートフォリオを拡大しています。OEMとの戦略的提携により、ブランドは進化するオートバイの設計に合わせながら、長期的な供給契約を確保しています。いくつかの企業は、ライフサイクルを延ばし、高温での性能を向上させたローター素材を開発するために研究開発に投資しています。各社はまた、特にモータースポーツが盛んな地域で、アフターマーケットへのアクセスを改善するため、世界な販売網を強化しています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 高性能バイクの需要の高まり

- 優れた耐熱性とブレーキフェードの低減

- モータースポーツとトラックレースの人気の高まり

- ローター製造における技術の進歩

- 軽量で操作性も向上

- 業界の潜在的リスク&課題

- カーボンセラミックローターの高コスト

- 標準的なオートバイとの互換性が限られている

- 市場機会

- 中級バイクへの進出

- 電動バイク(EV)の成長

- 材料科学における技術の進歩

- 新興市場の成長

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 統計概要

- 世界の高級バイク生産統計

- セグメント別のカーボンセラミック採用率

- 従来のローターとのパフォーマンス比較

- コスト分析と価格プレミアム評価

- 世界の高級バイク生産統計

- 技術と材料分析

- 材料構成と構造

- 炭素繊維強化システム

- セラミックマトリックス組成

- 結合剤および添加剤

- 微細構造と性能の関係

- 製造プロセス

- プリフォームの準備とレイアップ

- 化学蒸気浸透(CVI)

- 液体シリコン浸透(LSI)

- 機械加工および仕上げ作業

- パフォーマンス特性

- 熱特性と熱放散

- 機械的強度と耐久性

- 摩擦係数と耐摩耗性

- 軽量化と密度分析

- 材料構成と構造

- 価格動向

- 地域別

- 製品別

- コスト内訳分析

- 特許分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 主要市場企業の競合分析

- ブランド分析と市場認識

- ブランドの強さと認知度

- 顧客の忠誠心と満足度

- レーシングの伝統とパフォーマンスの信頼性

- テクノロジーリーダーシップの認識

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推定・予測:製品別、2021年~2034年

- 主要動向

- フロントブレーキローター

- リアブレーキローター

- フルセット(フロント・リア)

第6章 市場推定・予測:オートバイ別、2021年~2034年

- 主要動向

- スポーツ・レーシング用

- クルーザー・ツーリング用

- ダート・オフロード用

- その他

第7章 市場推定・予測:アプリケーション別、2021年~2034年

- 主要動向

- オンロード

- オフロード

第8章 市場推定・予測:販売チャネル別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第9章 市場推定・予測:最終用途別、2021年~2034年

- 主要動向

- プロのレーシングチーム

- 個人のオートバイオーナー

- オートバイメーカー

第10章 市場推定・予測:地域別、2021年~2034年

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第11章 企業プロファイル

- Alth Brakes

- AP Racing

- Braketech

- BRAKING

- Brembo

- Carbon Lorraine

- EBC Brakes

- Ferodo

- Galfer Brakes

- Galfer USA

- Moto-Master

- NG Brakes

- Nissin Kogyo

- SBS Friction

- SICOM Brakes

- Sunstar Engineering

- TRW Automotive

- Yutaka Giken

目次

The Global Motorcycle Carbon Ceramic Brake Rotors Market was valued at USD 53.5 million in 2024 and is estimated to grow at a CAGR of 4.6% to reach USD 79.1 million by 2034. Growth in this market is driven by the rising popularity of high-performance and luxury motorcycles, particularly in the sport and racing categories. These brake rotors are favored for their lightweight structure, superior heat resistance, and increased braking precision, making them ideal for aggressive riding and high-speed control. The appeal of these systems is especially strong among riders who prioritize safety, durability, and reduced maintenance. Innovations in composite materials are enhancing the lifespan and thermal management of these rotors, even under extreme riding conditions.

With expanding demand across motorsports-heavy regions like Europe and North America, leading manufacturers are leveraging advanced cooling technologies and modular rotor architecture to bring track-level performance to road-legal motorcycles. Suppliers are tailoring designs to match OEM specifications and consumer expectations around safety, efficiency, and performance. Premium segment growth has encouraged manufacturers like EBC Brakes, Sunstar, and Braketech to expand their offerings across both aftermarket and factory-fit channels.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $53.5 Million |

| Forecast Value | $79.1 Million |

| CAGR | 4.6% |

In 2024, the front brake rotor segment held a 52% share and is projected to grow at a CAGR of 5% through 2034. Since most braking power is handled by front rotors, performance upgrades and innovations are centered around these components. Technologies like ventilated and slotted rotor designs are gaining traction as sport touring and superbike sales continue to rise. Manufacturers such as Galfer Brakes and Brembo are actively releasing high-efficiency rotor systems to meet this demand.

The sport and racing motorcycles segment held a 50% share in 2024. These motorcycles require unmatched braking control and thermal balance at high speeds. The segment is seeing ongoing product development with rotors offering reduced thermal distortion and enhanced ventilation to manage prolonged high-performance use. Riders prefer carbon ceramic for its consistent stopping power, even under aggressive conditions, contributing to its rising adoption across track-inspired models.

Germany Motorcycle Carbon Ceramic Brake Rotors Market held a 50% share and generated USD 8.5 million in 2024. The country's leadership is anchored in its robust motorsports culture and strong OEM-supplier networks. Innovation in ceramic composites is being accelerated by the demand for lighter and more heat-tolerant materials, especially for electric motorcycles. Advanced R&D centers are emerging, pushing the limits of rotor technology, with an emphasis on efficiency and safety, making Germany a major contributor to global product evolution.

Key players shaping the Motorcycle Carbon Ceramic Brake Rotors Market include AP Racing, Braketech, SICOM Brakes, Galfer Brakes, Sunstar, Brembo S.p.A., and EBC Brakes. Manufacturers in this market are expanding their product portfolios with advanced rotor technologies that focus on thermal stability, lightweight construction, and improved airflow. Strategic collaborations with OEMs have helped brands secure long-term supply deals while aligning with evolving motorcycle designs. Several players are investing in R&D to develop rotor materials with extended life cycles and enhanced performance at high operating temperatures. Companies are also enhancing their global distribution networks, particularly in motorsport-dominant regions, to improve aftermarket accessibility.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Motorcycle

- 2.2.4 Application

- 2.2.5 Sales Channel

- 2.2.6 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for high-performance motorcycles

- 3.2.1.2 Superior heat resistance & reduced brake fade

- 3.2.1.3 Rising popularity of motorsport & track racing

- 3.2.1.4 Technological advancements in rotor manufacturing

- 3.2.1.5 Lightweight and improved handling

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of carbon ceramic rotors

- 3.2.2.2 Limited compatibility with standard motorcycles

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into mid-range motorcycles

- 3.2.3.2 Growth in electric motorcycles (EVs)

- 3.2.3.3 Technological advancements in material science

- 3.2.3.4 Growth in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.8 Statistical overview

- 3.8.1 Global premium motorcycle production statistics

- 3.8.1.1 Carbon ceramic adoption rates by segment

- 3.8.1.2 Performance comparison vs traditional rotors

- 3.8.1.3 Cost analysis and price premium assessment

- 3.8.1 Global premium motorcycle production statistics

- 3.9 Technology and material analysis

- 3.9.1 Material composition and structure

- 3.9.1.1 Carbon fiber reinforcement systems

- 3.9.1.2 Ceramic matrix compositions

- 3.9.1.3 Binding agents and additives

- 3.9.1.4 Microstructure and performance relationship

- 3.9.2 Manufacturing processes

- 3.9.2.1 Preform preparation and layup

- 3.9.2.2 Chemical vapor infiltration (CVI)

- 3.9.2.3 Liquid silicon infiltration (LSI)

- 3.9.2.4 Machining and finishing operations

- 3.9.3 Performance characteristics

- 3.9.3.1 Thermal properties and heat dissipation

- 3.9.3.2 Mechanical strength and durability

- 3.9.3.3 Friction coefficient and wear resistance

- 3.9.3.4 Weight reduction and density analysis

- 3.9.1 Material composition and structure

- 3.10 Price trends

- 3.10.1 By region

- 3.10.2 By product

- 3.11 Cost breakdown analysis

- 3.12 Patent analysis

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.13.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Brand analysis and market perception

- 4.4.1 Brand strength and recognition

- 4.4.2 Customer loyalty and satisfaction

- 4.4.3 Racing heritage and performance credibility

- 4.4.4 Technology leadership perception

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Front brake rotors

- 5.3 Rear brake rotors

- 5.4 Full set (Front & Rear)

Chapter 6 Market Estimates & Forecast, By Motorcycle, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Sport & racing motorcycles

- 6.3 Cruisers & touring motorcycles

- 6.4 Dirt & off-road motorcycles

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 On-road

- 7.3 Off-road

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 Professional racing teams

- 9.3 Individual motorcycle owners

- 9.4 Motorcycle manufacturers

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 10.1 North America

- 10.1.1 U.S.

- 10.1.2 Canada

- 10.2 Europe

- 10.2.1 UK

- 10.2.2 Germany

- 10.2.3 France

- 10.2.4 Italy

- 10.2.5 Spain

- 10.2.6 Russia

- 10.2.7 Nordics

- 10.3 Asia Pacific

- 10.3.1 China

- 10.3.2 India

- 10.3.3 Japan

- 10.3.4 South Korea

- 10.3.5 ANZ

- 10.3.6 Southeast Asia

- 10.4 Latin America

- 10.4.1 Brazil

- 10.4.2 Mexico

- 10.4.3 Argentina

- 10.5 MEA

- 10.5.1 UAE

- 10.5.2 Saudi Arabia

- 10.5.3 South Africa

Chapter 11 Company Profiles

- 11.1 Alth Brakes

- 11.2 AP Racing

- 11.3 Braketech

- 11.4 BRAKING

- 11.5 Brembo

- 11.6 Carbon Lorraine

- 11.7 EBC Brakes

- 11.8 Ferodo

- 11.9 Galfer Brakes

- 11.10 Galfer USA

- 11.11 Moto-Master

- 11.12 NG Brakes

- 11.13 Nissin Kogyo

- 11.14 SBS Friction

- 11.15 SICOM Brakes

- 11.16 Sunstar Engineering

- 11.17 TRW Automotive

- 11.18 Yutaka Giken

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日