ATPアッセイ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

ATP Assay Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 138 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801833

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

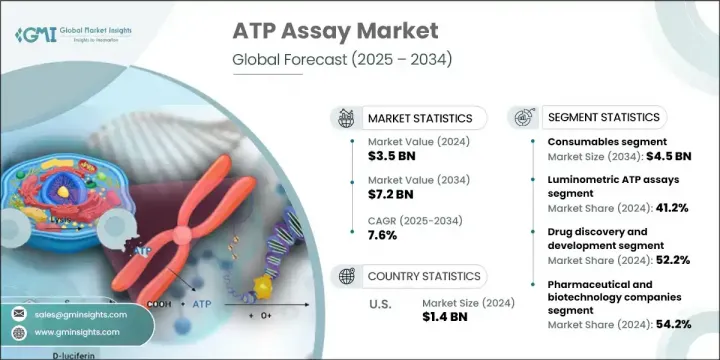

ATPアッセイの世界市場規模は2024年に35億米ドルとなり、CAGR 7.6%で成長し、2034年には72億米ドルに達すると推定されます。

市場の成長は、慢性疾患の負担の増加、個別化治療への需要の高まり、アッセイ技術の継続的な革新によって加速しています。ルモメトリックおよび酵素検出プラットフォームの進化により、スループット、精度、感度が大幅に向上し、研究、診断、医薬品開発での利用が拡大しています。分光光度計や高スループットルミノメーターなどの強化されたラボ機器は、アッセイ効率を高めながら、ワークフローの合理化に役立っています。

ATPアッセイは、アデノシン三リン酸レベルの検出に不可欠であり、細胞生存能、エネルギー代謝、細胞毒性反応の指標として機能します。精密医療や生物学的関連検査へのシフトに伴い、リアルタイムの細胞ベースアッセイへの需要が高まっています。このような検査により、研究者は初期の薬剤開発、環境モニタリング、毒性スクリーニングにおいて、細胞の挙動、生存能力、ストレス応答を評価することができます。バイオテクノロジーや製薬の研究室では、標的創薬やハイスループットスクリーニングを重視する傾向が強まっており、次世代治療薬に不可欠な信頼性が高くスケーラブルな生物学的データを提供するATPアッセイの役割はますます高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 35億米ドル |

| 予測金額 | 72億米ドル |

| CAGR | 7.6% |

2024年、消耗品セグメントは21億米ドルを生み出し、CAGR 7.7%で2034年までに45億米ドルに達します。このセグメントは、アッセイキット、試薬、日常的な処置に不可欠な特殊な実験材料が繰り返し必要とされるため、依然として支配的です。これらの品目はほとんどのATP検査ワークフローのバックボーンを形成し、特に薬物スクリーニングや汚染検出など、複数のプラットフォームに不可欠です。ラボの規模が拡大するにつれて、研究・診断用途でこれらの材料が継続的に使用されることが、セグメントの着実な成長を支えています。

ルミノメトリックアッセイセグメントは2024年に41.2%のシェアを占めました。ルミノメトリーアッセイの普及は、高精度、迅速な結果、自動化への適合性に起因しています。ルミノメトリックアッセイは、高感度でバックグラウンドノイズの少ない定量データを提供できるため、大規模なスクリーニングやラボのワークフローに適しています。自動化システムとの統合が容易であること、リアルタイムモニタリングが可能であること、マルチプレキシングが可能であることなどから、大量生産型の研究環境において広く使用されています。大規模なデータセットを最小限の手動処理で効率的に処理できるため、データの一貫性を維持しながらスループットを大幅に向上させることができます。

北米ATPアッセイ市場は2024年に42.5%のシェアを占める。同地域は、研究のための高度なインフラ、製薬企業やバイオテクノロジー企業の強い存在感、新規診断技術の急速な普及が引き続き需要を牽引しています。米国とカナダの研究所では、細胞ベースの検査、医薬品開発、汚染検出のニーズが高まっており、同地域のリーダーシップが強化されています。慢性疾患患者の急増や臨床試験への投資拡大も、学術・産業分野でのATPアッセイ使用の増加に寄与しています。

ATPアッセイの世界市場を牽引しているトップ企業には、Danaher、3M Company、Promega Corporation、Merck、Thermo Fisher Scientificなどがあり、世界市場シェアの55%を占めています。ATPアッセイ市場の主要企業は、アッセイ感度、スケーラビリティ、自動化適合性の継続的な研究開発を通じて、イノベーション主導の成長に注力しています。各社は、ハイスループット・アプリケーションをサポートする高度なルモメトリック技術とマイクロプレートベースのシステムを統合することで、製品ラインを強化しています。バイオテクノロジー企業や研究機関との戦略的提携は、ブランド認知度を高めながらエンドユーザー層の拡大に役立っています。M&Aもまた、新しい地理的市場への参入と生産能力の強化に利用されています。デジタルラボソリューションやクラウドベースのアナリティクスに投資し、より優れたアッセイモニタリングやデータトレーサビリティを提供する企業も増えています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 慢性疾患の負担増大

- 細胞ベースのアッセイの需要の高まり

- バイオ医薬品研究開発の成長

- アッセイフォーマットの技術的進歩

- 業界の潜在的リスク&課題

- 高度なキットの高コスト

- 厳格な規制ガイドライン

- 市場機会

- 衛生と環境監視の爆発的な成長

- 促進要因

- 成長可能性分析

- 規制情勢

- 技術的進歩

- 現在の技術動向

- 新興技術

- サプライチェーン分析

- 価格分析、2024

- 将来の市場動向

- ギャップ分析

- 償還シナリオ

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 機器

- ルミノメーター

- 分光光度計

- 消耗品

- 試薬とキット

- マイクロプレート

- その他の消耗品

第6章 市場推計・予測:アッセイタイプ別、2021年~2034年

- 主要動向

- 発光ATPアッセイ

- 酵素ATPアッセイ

- 生物発光共鳴エネルギー移動(BRET)ATPアッセイ

- 細胞ベースのATPアッセイ

- その他のアッセイタイプ

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 医薬品の発見と開発

- 汚染検査

- 疾患の検出

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 製薬およびバイオテクノロジー企業

- 病院および診断ラボ

- 学術研究機関

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- 3M Company

- AAT Bioquest

- Abcam

- Agilent Technologies

- Berthold Technologies

- Biotium

- BioVision

- Cayman Chemical

- Cell Signaling Technology

- Charm Sciences

- Danaher Corporation

- Lonza

- Merck

- PCE Instruments

- Promega

- Reddot Biotech

- Revvity

- Thermo Fisher Scientific

目次

The Global ATP Assay Market was valued at USD 3.5 billion in 2024 and is estimated to grow at a CAGR of 7.6% to reach USD 7.2 billion by 2034. Market growth is being accelerated by the rising burden of chronic diseases, the growing demand for personalized therapies, and continuous innovation in assay technology. The evolution of luminometric and enzymatic detection platforms is significantly improving throughput, precision, and sensitivity, resulting in expanded use across research, diagnostics, and pharmaceutical development. Enhanced lab instrumentation, like spectrophotometers and high-throughput luminometers, is helping streamline workflows while increasing assay efficiency.

ATP assays are essential for detecting adenosine triphosphate levels, which act as indicators of cellular viability, energy metabolism, and cytotoxic response. With the shift toward precision medicine and biologically relevant testing, demand for real-time, cell-based assays is rising. These tests enable researchers to assess cellular behavior, viability, and stress responses during early drug development, environmental monitoring, and toxicity screening. The growing emphasis on targeted drug discovery and high-throughput screening in biotechnology and pharmaceutical labs continues to elevate the role of ATP assays in delivering reliable and scalable biological data essential for next-generation therapeutics.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.5 Billion |

| Forecast Value | $7.2 Billion |

| CAGR | 7.6% |

In 2024, the consumables segment generated USD 2.1 billion and will reach USD 4.5 billion by 2034 at a CAGR of 7.7%. This segment remains dominant due to the recurring need for assay kits, reagents, and specialized lab materials essential for routine procedures. These items form the backbone of most ATP testing workflows and are vital across multiple platforms, particularly in drug screening and contamination detection. As laboratories scale their operations, the continued use of these materials in research and diagnostic applications supports steady segmental growth.

The luminometric assays segment held 41.2% share in 2024. Their widespread adoption stems from high accuracy, fast results, and automation compatibility. The ability of these assays to deliver quantitative data with high sensitivity and low background noise makes them the preferred choice for large-scale screening and laboratory workflows. They are widely used in high-volume research settings for their easy integration with automated systems, real-time monitoring, and multiplexing capabilities. Their efficiency in handling large datasets with minimal manual processing significantly improves throughput while maintaining data consistency.

North America ATP Assay Market held 42.5% share in 2024. The region's advanced infrastructure for research, strong presence of pharmaceutical and biotech firms, and rapid uptake of novel diagnostic technologies continue to drive demand. A growing need for cell-based testing, drug development, and contamination detection across labs in the U.S. and Canada has strengthened the region's leadership. The surge in chronic illness cases and expanding investments in clinical trials also contribute to the rising use of ATP assays across academic and industrial sectors.

Top companies driving the Global ATP Assay Market include Danaher, 3M Company, Promega Corporation, Merck, and Thermo Fisher Scientific-together accounting for 55% of global market share. Key players in the ATP assay market are focusing on innovation-driven growth through continuous R&D in assay sensitivity, scalability, and automation compatibility. Companies are enhancing their product lines by integrating advanced luminometric technologies and microplate-based systems that support high-throughput applications. Strategic collaborations with biotech firms and research institutes help expand their End user base while strengthening brand recognition. Mergers and acquisitions are also being used to enter new geographic markets and enhance production capacity. Firms are increasingly investing in digital lab solutions and cloud-based analytics to offer better assay monitoring and data traceability.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Assay type trends

- 2.2.4 Application trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising burden of chronic diseases

- 3.2.1.2 Growing demand for cell-based assays

- 3.2.1.3 Growth in biopharmaceutical R&D

- 3.2.1.4 Technological advancements in assay formats

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced kits

- 3.2.2.2 Stringent regulatory guidelines

- 3.2.3 Market opportunities

- 3.2.3.1 Explosive growth in hygiene and environmental monitoring

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Supply chain analysis

- 3.7 Pricing analysis, 2024

- 3.8 Future market trends

- 3.9 Gap analysis

- 3.10 Reimbursement scenario

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Instruments

- 5.2.1 Luminometers

- 5.2.2 Spectrophotometers

- 5.3 Consumables

- 5.3.1 Reagents and kits

- 5.3.2 Microplates

- 5.3.3 Other consumables

Chapter 6 Market Estimates and Forecast, By Assay Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Luminometric ATP assays

- 6.3 Enzymatic ATP assays

- 6.4 Bioluminescence resonance energy transfer (BRET) ATP assays

- 6.5 Cell-based ATP assays

- 6.6 Other assay types

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Drug discovery and development

- 7.3 Contamination testing

- 7.4 Disease detection

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Pharmaceutical and biotechnology companies

- 8.3 Hospital and diagnostic laboratories

- 8.4 Academic and research institutes

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 3M Company

- 10.2 AAT Bioquest

- 10.3 Abcam

- 10.4 Agilent Technologies

- 10.5 Berthold Technologies

- 10.6 Biotium

- 10.7 BioVision

- 10.8 Cayman Chemical

- 10.9 Cell Signaling Technology

- 10.10 Charm Sciences

- 10.11 Danaher Corporation

- 10.12 Lonza

- 10.13 Merck

- 10.14 PCE Instruments

- 10.15 Promega

- 10.16 Reddot Biotech

- 10.17 Revvity

- 10.18 Thermo Fisher Scientific

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 138 Pages

- 納期

- 2~3営業日