温度制御包装材料市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Temperature-Controlled Packaging Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 192 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801831

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

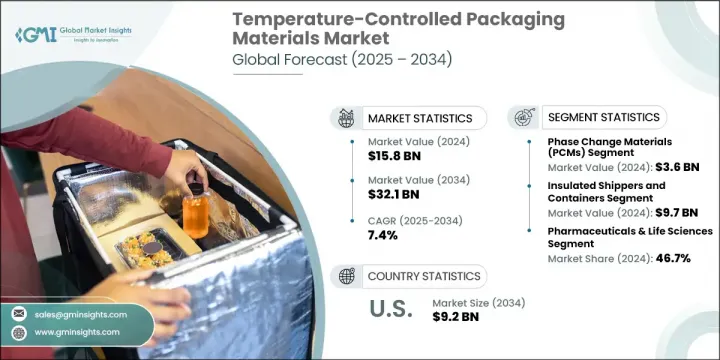

温度制御包装材料の世界市場規模は、2024年に158億米ドルとなり、CAGR 7.4%で成長し、2034年には321億米ドルに達すると予測されています。

成長の原動力は、医薬品、バイオテクノロジー、臨床研究、生鮮食品物流などの重要産業における需要の急増です。温度に敏感な製品を安全に輸送しなければならないというプレッシャーが高まる中、メーカーは輸送中の安定性、無菌性、一貫した温度管理が可能な高性能素材へとシフトしています。製品の取り扱いが複雑化するにつれ、先進パッケージング素材はオプションではなく必需品となっています。このような上昇傾向は、ますます温度に敏感な製品が増える中、より洗練されたサプライチェーン・ソリューションを求める世界の動向を反映しています。

効率的なサーマル・パッケージングの必要性は、わずかな温度差でも製品の完全性が損なわれかねない医薬品・バイオ医薬品分野で特に重要です。生物製剤、遺伝子治療、その他の複雑な治療が主流になるにつれ、包装ソリューションは、より厳しい温度管理とより長い出荷期間をサポートするために適応しなければなりません。企業はこうした要求に対応できる断熱包装フォーマットに投資しており、コールドチェーン全体の透明性とトレーサビリティを確保するために、モノのインターネット(IoT)ベースのモニタリングシステムの統合が一般的になってきています。さらに、持続可能でコスト効率に優れたパッケージングを求める動きが強まっており、再利用可能で国際的な規制に準拠した新しい素材の設計と展開に影響を与えています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 158億米ドル |

| 予測金額 | 321億米ドル |

| CAGR | 7.4% |

材料タイプ別では、相変化材料が主要セグメントとして浮上しており、2024年の評価額は36億米ドルに達します。2034年までCAGR 8.4%で成長すると予想されるこれらの材料は、輸送中に正確な温度範囲を維持する能力で好まれています。水性製剤やゲル製剤は、必要な温度条件を保持する効率が高く、パッシブ・コールド・チェーン・ソリューションで再利用できる可能性があるため、人気を集めています。これらの材料は、技術的な性能だけでなく、従来の冷媒に比べて環境への影響が少ないことでも支持されています。信頼性が高くエネルギー効率の高い選択肢を求める市場の高まりは、相変化技術の技術革新を加速させており、これは現在、医薬品と食品グレードのロジスティクスの双方にとって中心的な存在となっています。

製品別では、断熱シッパーとコンテナが市場を席巻しており、2024年の市場規模は97億米ドル、2034年までのCAGRは7%と予測されています。これらのソリューションは、小包、パレット、バルク貨物など、さまざまな出荷形態に対応するように設計されています。医薬品、生物製剤、温度に敏感な食品などの物流ニーズが需要を牽引しています。包装設計のカスタマイズ化が進むことで、厳格な温度管理が必須となる臨床試験や個別化治療などの新たな用途に対応できるようになっています。断熱カートン、木枠、箱、パウチなどの製品は、ラストワンマイル配送や地域配送網に有効であるため、引き続き幅広く使用されています。

用途別では、医薬品とライフサイエンスが最大のセグメントを占め、2024年の世界市場シェアの46.7%を占める。この分野は、生物製剤、ワクチン、個別化医療のパイプラインの拡大に後押しされ、2034年までCAGR 7.9%で成長すると予測されています。製薬会社は、無菌性、精密性、規制枠組みへの準拠を確保しつつ、大量展開のための拡張性を備えた包装システムを求めています。シングルユースパッケージング形式と先進冷却ソリューションの重要性の高まりは、デジタルモニター付き容器の採用とともに、この分野におけるロジスティクス業務の形を変えつつあります。世界の健康情勢の変化に伴い、包装技術は、高価値の製品が無傷のまま目的地に到着することを保証する上で不可欠な役割を果たしています。

米国の温度制御包装材料市場は、2024年には48億米ドルとなり、CAGR6.7%を反映して2034年には92億米ドルにまで上昇すると予想されています。米国のバイオテクノロジーと製薬産業の継続的な拡大がこの成長を牽引しています。同市場では、真空断熱パネルや次世代相変化材料などの先進断熱パッケージングシステムの採用が増加しています。さらに、患者直送モデルの拡大により、さまざまな輸送条件下で一貫した温度維持を保証する包装に対する新たな需要が生まれています。米国の利害関係者もまた、インテリジェントな追跡ソリューションと、特殊な治療で必要とされる狭い温度公差を満たす包装のイノベーションを推進しています。

市場の主導権は少数の主要企業に集中しており、2024年の世界市場シェアは上位5社合計で約40%を占める。これらの企業は、適正流通基準(GDP)やその他の世界標準に準拠した再利用可能なソリューションと使い捨てソリューションを組み合わせて提供することで、牙城を築いてきました。規制が厳しくなり、顧客が優れた信頼性、コスト効率、持続可能性を求めるようになるにつれ、競合の激しさは増しています。企業は、スマートな追跡技術の統合、世界・インフラの拡大、環境への影響を低減する素材への投資によって対応しています。競争力を維持するために、M&Aやロジスティクス・プロバイダーやテクノロジー・プロバイダーとの提携を含む戦略的提携が優先されています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- 価格動向

- 地域別

- タイプ別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な実践

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:材料タイプ別、2021年~2034年

- 主要動向

- 断熱材

- 相変化材料(PCM)

- 冷媒および冷却剤

- スマートセンサーと監視デバイス

第6章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 断熱輸送容器およびコンテナ

- カスタムおよび特殊ソリューション

- 冷蔵・冷凍包装

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 医薬品およびライフサイエンス

- 食品・飲料

- 化学品および工業製品

- その他の用途

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第9章 企業プロファイル

- AmerisourceBergen

- Avery Dennison

- Cold Chain Technologies

- Cryopak

- Envirotainer

- Intelsius

- Nordic Cold Chain Solutions

- Pelican BioThermal

- Sealed Air

- Sofrigam

- Softbox Systems

- Sonoco Products Company

- TemperPack

- Tower Cold Chain

- Va-Q-Tec

目次

The Global Temperature-Controlled Packaging Materials Market was valued at USD 15.8 billion in 2024 and is estimated to grow at a CAGR of 7.4% to reach USD 32.1 billion by 2034. The growth is driven by demand surges across critical industries such as pharmaceuticals, biotechnology, clinical research, and perishable food logistics. With increasing pressure to ensure the safe transportation of temperature-sensitive products, manufacturers are shifting toward high-performance materials that can provide stability, sterility, and consistent thermal control throughout transit. This growing complexity in product handling has made advanced packaging materials a necessity rather than an option. This upward trend reflects the global push for more sophisticated supply chain solutions amid an increasingly temperature-sensitive product landscape.

The need for efficient thermal packaging is especially critical in the pharmaceutical and biopharma sectors, where even slight temperature deviations can compromise product integrity. As biologics, gene therapies, and other complex treatments become more mainstream, packaging solutions must adapt to support stricter temperature controls and longer shipping durations. Companies are investing in insulated packaging formats that can meet these demands, and the integration of Internet of Things (IoT)-based monitoring systems has become more common to ensure transparency and traceability across the cold chain. Moreover, the growing push for sustainable and cost-efficient packaging options is influencing the design and deployment of newer materials that are both reusable and compliant with international regulations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $15.8 Billion |

| Forecast Value | $32.1 Billion |

| CAGR | 7.4% |

In terms of material type, phase change materials are emerging as a major segment, reaching a valuation of USD 3.6 billion in 2024. Expected to grow at a CAGR of 8.4% through 2034, these materials are preferred for their ability to maintain precise temperature ranges during shipping. Water-based and gel formulations are gaining traction due to their efficiency in preserving required thermal conditions and their potential for reuse in passive cold chain solutions. These materials are being favored not only for their technical performance but also for their lower environmental impact compared to traditional refrigerants. The market's growing inclination toward reliable and energy-efficient options is accelerating innovation in phase change technologies, which are now central to both pharmaceutical and food-grade logistics.

From a product perspective, insulated shippers and containers dominate the landscape, with a market value of USD 9.7 billion in 2024 and a forecasted CAGR of 7% through 2034. These solutions are designed to accommodate various shipping formats such as small parcels, pallets, and bulk shipments. Demand is being driven by the logistics needs of pharmaceuticals, biologics, and temperature-sensitive food products. Increasing customization in packaging design is helping cater to emerging applications like clinical trials and personalized therapies, where strict temperature control is mandatory. Products such as insulated cartons, crates, boxes, and pouches continue to see wide usage due to their effectiveness in last-mile delivery and regional distribution networks.

On the basis of application, pharmaceuticals and life sciences represent the largest segment, accounting for 46.7% of the global market share in 2024. This sector is anticipated to grow at a CAGR of 7.9% through 2034, fueled by the expanding pipeline of biologics, vaccines, and personalized medicine. Pharmaceutical companies are demanding packaging systems that ensure sterility, precision, and compliance with regulatory frameworks while also offering scalability for mass deployment. The increasing importance of single-use packaging formats and advanced cooling solutions, along with the adoption of digitally monitored containers, is reshaping logistics operations in this sector. As the global health landscape evolves, packaging technologies are playing an essential role in ensuring that these high-value products reach their destinations intact.

In the United States, the temperature-controlled packaging materials market was worth USD 4.8 billion in 2024 and is expected to climb to USD 9.2 billion by 2034, reflecting a CAGR of 6.7%. The continued expansion of the U.S. biotechnology and pharmaceutical industries is driving this growth. The market is experiencing increased adoption of advanced thermal packaging systems, such as vacuum insulation panels and next-generation phase change materials. Furthermore, the growth of direct-to-patient delivery models is creating new demands for packaging that ensures consistent temperature maintenance across varied transport conditions. U.S. stakeholders are also pushing for intelligent tracking solutions and packaging innovations that meet the narrow thermal tolerances required by specialized therapies.

Market leadership is concentrated among a few major players, with the top five companies collectively holding approximately 40% of the global market share in 2024. These companies have established a stronghold by offering a mix of reusable and single-use solutions that comply with Good Distribution Practices (GDP) and other global standards. Competitive intensity is growing as regulations become more stringent and customers demand superior reliability, cost-efficiency, and sustainability. Companies are responding by integrating smart tracking technologies, expanding global infrastructure, and investing in materials that lower environmental impact. Strategic collaborations, including M&A and partnerships with logistics and tech providers, are being prioritized to stay competitive.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.7 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Material Type, 2021 - 2034 (USD Billion) (Tons)

- 5.1 Key trends

- 5.2 Insulation Materials

- 5.3 Phase Change Materials (PCMs)

- 5.4 Refrigerants and Cooling Agents

- 5.5 Smart Sensors and Monitoring Devices

Chapter 6 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Tons)

- 6.1 Key trends

- 6.2 Insulated Shippers and Containers

- 6.3 Custom and Specialty Solutions

- 6.4 Refrigerated and Frozen Packaging

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Tons)

- 7.1 Key trends

- 7.2 Pharmaceuticals and Life Sciences

- 7.3 Food and Beverage

- 7.4 Chemicals and Industrial Goods

- 7.5 Other Applications

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 AmerisourceBergen

- 9.2 Avery Dennison

- 9.3 Cold Chain Technologies

- 9.4 Cryopak

- 9.5 Envirotainer

- 9.6 Intelsius

- 9.7 Nordic Cold Chain Solutions

- 9.8 Pelican BioThermal

- 9.9 Sealed Air

- 9.10 Sofrigam

- 9.11 Softbox Systems

- 9.12 Sonoco Products Company

- 9.13 TemperPack

- 9.14 Tower Cold Chain

- 9.15 Va-Q-Tec

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 192 Pages

- 納期

- 2~3営業日