|

市場調査レポート

商品コード

1801811

バイオスティミュラント製剤材料市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Biostimulants Formulation Material Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| バイオスティミュラント製剤材料市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年08月12日

発行: Global Market Insights Inc.

ページ情報: 英文 192 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

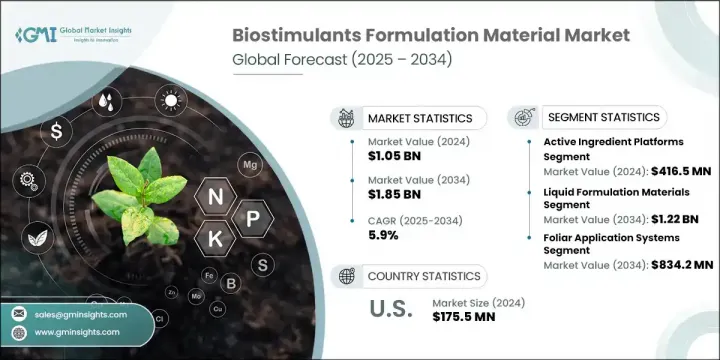

バイオスティミュラント製剤材料の世界市場規模は、2024年に10億5,000万米ドルとなり、CAGR 5.9%で成長し、2034年には18億5,000万米ドルに達すると予測されています。

同市場は、持続可能な農業の実践が世界的に重視され、生産性を高めながらも環境に配慮した投入物への需要が高まっていることから、大きな牽引力となっています。自然ベースや生物学的作物強化ソリューションへの幅広いシフトが、良好な政策環境と相まって、市場拡大を後押ししています。葉面散布は依然として主要な使用方法であり、全使用量の半分近くを占めています。しかし、種子処理や土壌施用製剤への関心の高まりは、特に標的を絞った送達方法の技術革新が進み、広く利用できるようになるにつれて、業界の力学を再構築しつつあります。

微生物溶液、海藻抽出物、天然多糖類など、天然製剤材料への移行が加速しています。化学物質の投入を削減するという規制上の圧力と、残留物のない食品を求める消費者の嗜好とが相まって、持続可能なバイオ刺激剤への移行が加速しています。生産者は、現代農業を支える生分解性で効果的かつ持続可能なソリューションに焦点を当てた研究開発に資源を投入しています。特定の作物の種類、土壌条件、地域の気候に合わせて設計された、高度に調整された製剤を求める傾向が強まっています。企業は、高度なデータ分析と農学的洞察を活用して、収量を高め、プレミアム価格を要求し、正確で高価値の作物ソリューションを求める生産者との長期的関係を促進する、カスタマイズされたバイオスティミュラントを提供しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 10億5,000万米ドル |

| 予測金額 | 18億5,000万米ドル |

| CAGR | 5.9% |

安定剤およびアジュバント分野は、有効成分を保存し、貯蔵寿命を改善し、幅広い用途で生物刺激剤の機能的送達を強化する能力によって支えられ、2034年までCAGR 7.4%で成長します。乳化剤や界面活性剤を含むこれらの成分は、製剤の均一性を維持し、吸収性を確保し、他の農産物との適合性をサポートする上で重要な役割を果たしています。これらの使用量の増加は、今日の作物投入製剤に要求される複雑さと精度の高まりを浮き彫りにしています。

乾燥製剤材料セグメントは、2034年までCAGR 4.6%で成長します。使いやすさと技術革新により液体製剤が目立つようになってきているが、長い保存期間と安定性を必要とする場面では乾燥製剤が依然として重要です。市場の発展に伴い、ドライ製剤のシェアは若干低下することが予想されるが、特定の使用事例では需要は堅調に推移すると思われます。

米国のバイオスティミュラント製剤材料市場は80.1%のシェアを占め、2024年には1億7,550万米ドルを創出します。この地域は、規制状況が整備されていること、農業研究開発への投資が続いていること、環境に配慮した農法が強く推進されていることなどの恩恵を受けています。多糖類はその環境適合性と有効性から米国で広く支持されています。この高度に工業化され、技術重視の市場では、製品の安定性を維持し、他の農薬システムとの整合性を確保するために、安定剤とアジュバントが不可欠です。微生物接種剤、アミノ酸、海藻ベースの資材などの有効成分の使用が圧倒的に多いことは、現代農業における生物学的および精密な投入物への嗜好の高まりを裏付けています。

世界のバイオスティミュラント製剤材料市場を形成している主要企業には、Novozymes A/S、BASF SE、Valagro S.p.A.、UPL Limited、Syngenta AGなどがあります。バイオスティミュラント製剤材料市場で確固たる足場を築くため、各社は環境基準に適合しながら収量を向上させる持続可能な作物専用製品を開発する研究に多額の投資を行っています。特に、さまざまな気候や土壌の条件に適した、生分解性のオーダーメード製剤の開発に重点を置いています。農業技術企業、研究機関、生産者との戦略的協力関係は、企業が地域に特化したソリューションを共同開発するのに役立っています。企業はまた、新たな成長分野を開拓するために、世界な流通網を拡大し、新興市場に参入しています。デジタル・プラットフォームと精密農業ツールの重視は、製品提供のリアルタイム・カスタマイズをサポートします。

目次

第1章 調査手法

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 持続可能で有機的な農業資材の需要の高まり

- 環境に優しい農薬製品に対する規制支援

- 作物の収穫量と品質向上への重点化

- 製剤および送達システムにおける技術的進歩

- 業界の潜在的リスク&課題

- 農家の意識と技術知識の不足

- 環境要因による製品効果の変動

- 市場機会

- 作物特化型およびカスタマイズされた配合の開発

- デジタル農業と精密農業との統合

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 素材タイプ別

- コスト内訳分析

- 特許分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:材料タイプ別、2021年~2034年

- 主要動向

- 天然多糖類

- 安定剤および補助剤

- 有効成分プラットフォーム

- 海藻エキス製剤原料

- フミン酸およびフルボ酸誘導体

- アミノ酸およびタンパク質加水分解塩基

- 微生物カプセル化材料

第6章 市場推計・予測:形態別、2021年~2034年

- 主要動向

- 液体製剤材料

- 乳化剤および可溶化剤

- 懸濁剤および増粘剤

- 防腐剤および抗菌剤

- 凍結融解安定剤

- 乾燥製剤材料

- 造粒およびペレット化補助剤

- 固結防止剤および流動性向上剤

- 粉塵抑制およびハンドリング性向上剤

- 防湿コーティング

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 種子処理製剤材料

- コーティング材およびバインダー

- 接着促進剤およびフィルム形成剤

- 着色料と識別システム

- 保護封止材

- 葉面散布システム

- スプレー補助剤および浸透促進剤

- ドリフト防止および堆積補助

- UV保護剤および安定性増強剤

- タンク混合用相溶性剤

- 土壌施用材料

- 造粒助剤および結合剤

- 徐放性コーティングシステム

- 土壌浸透促進剤

- 湿気管理材料

- その他

第8章 市場推計・予測:作物別、2021年~2034年

- 主要動向

- 穀物

- 果物と野菜

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- イタリア

- スペイン

- ドイツ

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- エジプト

- その他中東・アフリカ地域

第10章 企業プロファイル

- Ashland Global Holdings Inc.

- BASF SE

- Biotechnica(UK)

- Citymax Group(China)

- Croda International Plc

- Elemental Enzymes

- Evonik Industries AG

- Fertinagro Biotech

- Genvor

- Natural Growth Biostimulants LLC

- Novozymes A/S

- SIPCAM Inagra(欧州)

- Syngenta AG

- UPL Limited

- Valagro S.p.A

The Global Biostimulants Formulation Material Market was valued at USD 1.05 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 1.85 billion by 2034. The market is gaining significant traction due to the worldwide emphasis on sustainable agricultural practices and the increasing demand for productivity-boosting yet environmentally conscious inputs. The broader shift toward nature-based and biological crop enhancement solutions, combined with favorable policy environments, is propelling market expansion. Foliar application remains the dominant method of usage, accounting for nearly half of all applications. However, growing interest in seed treatments and soil-applied formulations is reshaping industry dynamics, especially as innovation in targeted delivery methods becomes more advanced and widely available.

The transition to natural formulation materials-such as microbial solutions, seaweed extracts, and natural polysaccharides-is intensifying. Regulatory pressure to reduce chemical inputs, coupled with consumer preference for residue-free food, is accelerating this move toward sustainable biostimulants. Producers are dedicating resources to research and development focused on biodegradable, effective, and sustainable solutions that support modern agriculture. There's a growing trend toward highly tailored formulations designed for specific crop types, soil conditions, and local climates. Companies are leveraging advanced data analytics and agronomic insights to offer customized biostimulants that boost yields, command premium pricing, and foster long-term relationships with growers seeking precise, high-value crop solutions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.05 Billion |

| Forecast Value | $1.85 Billion |

| CAGR | 5.9% |

The stabilizers and adjuvants segment will grow at a CAGR of 7.4% through 2034, supported by their ability to preserve active ingredients, improve shelf-life, and enhance the functional delivery of biostimulants across a wide range of applications. These ingredients, including emulsifiers and surfactants, play a key role in maintaining formulation uniformity, ensuring absorption, and supporting compatibility with other agricultural products. Their rising use highlights the growing complexity and precision required in today's crop input formulations.

The dry formulation materials segment will grow at a CAGR of 4.6% through 2034. While liquid formulations are becoming more prominent due to ease of use and innovation, dry forms remain critical in scenarios requiring long shelf-life and stability. As the market evolves, a slight decline in dry formulation share is anticipated, although demand will remain steady in certain use cases.

U.S. Biostimulants Formulation Material Market held 80.1% share, generating USD 175.5 million in 2024. The region benefits from a well-developed regulatory landscape, ongoing investment in agricultural R&D, and a strong push for environmentally responsible farming practices. Polysaccharides are widely favored in the U.S. due to their environmental compatibility and effectiveness. In this highly industrialized and tech-focused market, stabilizers and adjuvants are essential to maintaining product stability and ensuring alignment with other agrochemical systems. The dominant use of active ingredients such as microbial inoculants, amino acids, and seaweed-based materials underscores a growing preference for biologicals and precision inputs in modern agriculture.

Key players shaping the Global Biostimulants Formulation Material Market include Novozymes A/S, BASF SE, Valagro S.p.A., UPL Limited, and Syngenta AG. To establish a strong foothold in the Biostimulants Formulation Material Market, companies are investing heavily in research to develop sustainable, crop-specific products that enhance yield while aligning with environmental standards. A major focus lies in innovation-particularly in creating biodegradable, tailored formulations suited for varied climatic and soil conditions. Strategic collaborations with agricultural tech firms, research institutes, and growers are helping companies co-develop region-specific solutions. Firms are also expanding global distribution networks and entering emerging markets to tap into new growth areas. Emphasis on digital platforms and precision agriculture tools supports real-time customization of product offerings.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Material type

- 2.2.2 Form

- 2.2.3 Application method

- 2.2.4 Crop type

- 2.2.5 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for sustainable and organic agricultural inputs

- 3.2.1.2 Regulatory support for eco-friendly crop protection products

- 3.2.1.3 Increasing focus on crop yield and quality enhancement

- 3.2.1.4 Technological advancements in formulation and delivery systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited farmer awareness and technical knowledge

- 3.2.2.2 Variability in product efficacy due to environmental factors

- 3.2.3 Market opportunities

- 3.2.3.1 Development of crop-specific and customized formulations

- 3.2.3.2 Integration with digital agriculture and precision farming

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By material type

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly Initiatives

- 3.12 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, by Material Type, 2021 - 2034 (USD Bn, Tons)

- 5.1 Key trends

- 5.2 Natural polysaccharides

- 5.3 Stabilizers and adjuvants

- 5.4 Active ingredient platforms

- 5.4.1 Seaweed extract formulation materials

- 5.4.2 Humic and fulvic acid derivatives

- 5.4.3 Amino acid and protein hydrolysate bases

- 5.4.4 Microbial encapsulation materials

Chapter 6 Market Estimates & Forecast, by Form, 2021 - 2034 (USD Bn, Tons)

- 6.1 Key trends

- 6.2 Liquid formulation materials

- 6.2.1 Emulsifiers and solubilizers

- 6.2.2 Suspension agents and thickeners

- 6.2.3 Preservatives and antimicrobial agents

- 6.2.4 Freeze-thaw stabilizers

- 6.3 Dry formulation materials

- 6.3.1 Granulation and pelletization aids

- 6.3.2 Anti-caking and flow enhancement agents

- 6.3.3 Dust control and handling improvers

- 6.3.4 Moisture barrier coatings

Chapter 7 Market Estimates & Forecast, by Application Method, 2021 - 2034 (USD Bn, Tons)

- 7.1 Key trends

- 7.2 Seed treatment formulation materials

- 7.2.1 Coating materials and binders

- 7.2.2 Adhesion promoters and film formers

- 7.2.3 Colorants and identification systems

- 7.2.4 Protective encapsulation materials

- 7.3 Foliar application systems

- 7.3.1 Spray adjuvants and penetration enhancers

- 7.3.2 Anti-drift and deposition aids

- 7.3.3 UV protectants and stability enhancers

- 7.3.4 Compatibility agents for tank mixing

- 7.4 Soil application materials

- 7.4.1 Granulation aids and binding agents

- 7.4.2 Slow-release coating systems

- 7.4.3 Soil penetration enhancers

- 7.4.4 Moisture management materials

- 7.5 Others

Chapter 8 Market Estimates & Forecast, by Crop Type, 2021 - 2034 (USD Mn, Tons)

- 8.1 Key trends

- 8.2 Cereals and grains

- 8.3 Fruits and vegetables

- 8.4 Others

Chapter 9 Market Estimates & Forecast, by Region, 2021 - 2034 (USD Mn, Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 France

- 9.3.3 Italy

- 9.3.4 Spain

- 9.3.5 Germany

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Egypt

- 9.6.5 Rest of MEA

Chapter 10 Company Profiles

- 10.1 Ashland Global Holdings Inc.

- 10.2 BASF SE

- 10.3 Biotechnica (UK)

- 10.4 Citymax Group (China)

- 10.5 Croda International Plc

- 10.6 Elemental Enzymes

- 10.7 Evonik Industries AG

- 10.8 Fertinagro Biotech

- 10.9 Genvor

- 10.10 Natural Growth Biostimulants LLC

- 10.11 Novozymes A/S

- 10.12 SIPCAM Inagra (Europe)

- 10.13 Syngenta AG

- 10.14 UPL Limited

- 10.15 Valagro S.p.A