凍結乾燥注射剤市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Lyophilized Injectable Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 155 Pages

- 納期

- 2~3営業日

- 商品コード

- 1797883

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

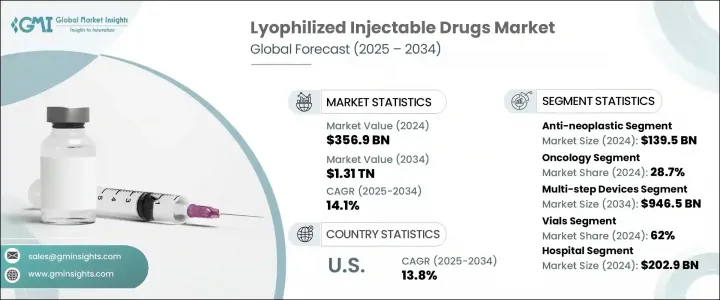

世界の凍結乾燥注射剤市場は、2024年に3,569億米ドルと評価され、CAGR 14.1%で成長し、2034年には1兆3,100億米ドルに達すると推定されます。

がんや感染症を含む慢性的な健康状態の増加により、安定した長時間作用型の治療薬に対する需要が引き続き高まっています。保存期間の延長と薬効改善の必要性から、凍結乾燥注射剤製剤は医薬品パイプラインの重要な一部となっています。さらに、世界の規制承認の増加と凍結乾燥プロセスの技術的進歩により、市場への浸透が著しく高まっています。入院治療と外来治療の両方における生物製剤と注射療法へのシフトに伴い、凍結乾燥注射剤セクターでは製造能力、物流インフラ、臨床応用の急速な発展が見られます。

耐久性があり安定性の高い製剤に対するニーズの高まりは、製薬企業が拡大する注射薬に凍結乾燥を採用することを後押ししています。コールドチェーン流通の強化、単回投与パッケージング、再構成効率の改善などのイノベーションにより、世界のヘルスケアシステム全体で製品の信頼性が強化されています。凍結乾燥製剤は、安定性と無菌性が重要な疾患の治療において勢いを増しています。これらの薬剤は通常、希釈剤と混合した後に投与されるため、ヘルスケアプロバイダーは投与精度を管理し、製品の有用性を拡大することができます。保存期間が長く信頼性の高い製剤が入手できることから、特にインフラが限られ、高度医療へのアクセスが拡大している地域では、凍結乾燥医薬品が好ましい選択肢となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 3,569億米ドル |

| 予測金額 | 1兆3,100億米ドル |

| CAGR | 14.1% |

2024年、抗悪性腫瘍剤セグメントは1,395億米ドルのシェアを獲得したが、これは腫瘍に特化した生物学的製剤や細胞毒性化合物に対する需要の急増を反映しています。凍結乾燥注射剤は、これらの治療に特に適しており、汚染や取り扱いに伴うリスクを最小限に抑えながら、安定性の向上と保存期間の延長を実現しています。これらの特性は、正確な投与量、無菌性、長期保存が不可欠ながん治療において極めて重要です。規制当局ががん領域で凍結乾燥製剤を承認するケースが増えていることから、製薬会社は抗悪性腫瘍性注射剤、特に高価値製剤で効能や純度の逸脱の余地が限られる製剤を中心に開発パイプラインを優先しています。

がん領域は2024年に28.7%のトップシェアを占めました。同分野の優位性は、世界のがん罹患率の増加と、長期間の保管や輸送を通じて治療効果を維持する安定した注射療法の必要性によるものです。世界中のヘルスケアシステムは、より強固なドラッグデリバリーソリューションへの投資を進めており、凍結乾燥注射剤はコスト効率に優れ、長期的な解決策となります。医薬品開発企業は、がん治療に対する需要の高まりに対応するため、デリバリー方法の改良、薬剤の無駄の削減、凍結乾燥による製品寿命の強化に重点的に取り組んでいます。

北米市場は2024年に47%を占め、同地域の先進的な医薬品事情と慢性疾患患者の集中に支えられています。この地域の優位性は、強力な研究開発能力、凍結乾燥注射剤の頻繁なFDA承認、病院や外来での幅広い採用を支える成熟したヘルスケア提供システムにも起因しています。腫瘍学、自己免疫疾患治療薬、生物製剤への継続的な投資と、保存期間が延長された注射薬の受け入れ拡大が、世界の凍結乾燥注射剤市場における同地域の牙城を支え続けています。

凍結乾燥注射剤業界の企業は、市場でのリーダーシップを確保するため、大容量の凍結乾燥装置や、厳しい世界規制基準を満たす最先端の製造ラインへの投資を増やしています。多くの企業は、受託製造サービスを拡大し、コールドチェーン・ロジスティクスを改善し、ダウンタイムと製造コストを削減するために自動化を統合しています。革新的な生物学的化合物へのアクセスを獲得し、製品ポートフォリオを拡大するために、戦略的共同研究やライセンシング契約が一般的に利用されています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 慢性疾患および感染症の蔓延

- ドラッグデリバリーシステムにおける技術的進歩

- 生物製剤と複合分子の需要の高まり

- 業界の潜在的リスク&課題

- 生産コストと設備コストが高め

- 規制と品質コンプライアンスの課題

- 市場機会

- 個別化医療と精密医療

- 契約調査製造サービス(CRAMS)の拡大

- 促進要因

- 成長可能性分析

- テクノロジーの情勢

- 現在の技術動向

- 新興技術

- 価格分析

- パイプラインとR&D投資分析

- 特許情勢分析

- 親市場分析

- 規制情勢

- 将来の市場動向

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 世界

- 北米

- 欧州

- アジア太平洋地域

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

第5章 市場推計・予測:薬剤タイプ別、2021年~2034年

- 主要動向

- 抗感染性

- 抗腫瘍性

- 抗凝固剤

- ホルモン

- 抗不整脈薬

- プロトンポンプ阻害剤

- 麻酔薬

- その他の薬物の種類

第6章 市場推計・予測:適応症別、2021年~2034年

- 主要動向

- 自己免疫疾患

- 呼吸器疾患

- 胃腸障害

- 腫瘍学

- 心血管疾患

- 感染症

- ホルモン障害

- 代謝障害

- 生殖に関する健康

- その他の適応症

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- プレフィルド希釈液シリンジ

- 多段階デバイス

第8章 市場推計・予測:包装別、2021年~2034年

- 主要動向

- バイアル

- カートリッジ

- プレフィルドデバイス

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 専門クリニック

- その他の用途

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Akums Drugs and Pharmaceuticals

- Aurobindo Pharma

- Bora Pharmaceuticals

- Bristol Myers Squibb

- Cipla

- F. Hoffmann-La Roche

- Fareva

- Fresenius

- Gilead Sciences

- Gufic Group

- Johnson &Johnson

- Meiji Group

- Merck

- Novo Nordisk

- Pfizer

- Sanofi

- Takeda Pharmaceuticals

- Vetter Pharma

- Zydus

目次

The Global Lyophilized Injectable Drugs Market was valued at USD 356.9 billion in 2024 and is estimated to grow at a CAGR of 14.1% to reach USD 1.31 trillion by 2034. Rising incidences of chronic health conditions, including cancer and infectious diseases, continue to escalate demand for stable and long-acting therapeutics. The need for extended shelf life and improved drug efficacy has made freeze-dried injectable formulations an essential part of the pharmaceutical pipeline. Additionally, the increase in global regulatory approvals and technological advancements in lyophilization processes is significantly enhancing market penetration. With a shift toward biologics and injectable therapies in both inpatient and outpatient care, the lyophilized injectables sector is seeing rapid development in manufacturing capabilities, logistics infrastructure, and clinical applications.

The rising need for durable and highly stable drug formulations is pushing pharmaceutical companies to adopt lyophilization for an expanding range of injectable drugs. Innovations such as enhanced cold-chain distribution, single-dose packaging, and improvements in reconstitution efficiency are strengthening product reliability across global healthcare systems. Lyophilized formulations are gaining momentum in the treatment of diseases where stability and sterility are critical. These drugs are typically administered after mixing with a diluent, allowing healthcare providers to manage dosing accuracy and extend product usability. The availability of reliable formulations with longer shelf lives makes lyophilized drugs a preferred choice, particularly in regions with limited infrastructure and growing access to advanced medical care.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $356.9 Billion |

| Forecast Value | $1.31 Trillion |

| CAGR | 14.1% |

In 2024, the anti-neoplastic agents segment captured a USD 139.5 billion share, reflecting the surging demand for oncology-focused biologics and cytotoxic compounds. Lyophilized injectable drugs are particularly well-suited for these treatments, offering improved stability and longer shelf life while minimizing the risks associated with contamination and handling. These properties are critical in cancer care, where precise dosage, sterility, and long-term storage are vital. With regulatory bodies increasingly approving freeze-dried formulations in oncology, pharmaceutical firms are prioritizing development pipelines around anti-neoplastic injectables, particularly those with high-value formulations and limited room for deviation in potency or purity.

The oncology segment held the leading share of 28.7% in 2024. Its dominance is driven by the growing global incidence of cancer and the necessity for stable injectable therapies that maintain therapeutic effectiveness through extended storage and transport. Healthcare systems worldwide are investing in more robust drug delivery solutions, and lyophilized injectables provide a cost-effective, long-term answer. Pharmaceutical developers are focusing heavily on refining delivery methods, reducing drug wastage, and enhancing product lifespan through lyophilization to meet the growing demand for cancer treatments.

North America Lyophilized Injectable Drugs Market held 47% in 2024, underpinned by the region's advanced pharmaceutical landscape and high concentration of chronic disease cases. The region's dominance also stems from strong R&D capabilities, frequent FDA approvals for freeze-dried injectables, and a mature healthcare delivery system that supports wide adoption across hospital and ambulatory settings. Continued investment in oncology, autoimmune disease therapies, and biologics, combined with growing acceptance of injectable drugs with extended shelf lives, continues to support the region's stronghold in the global lyophilized injectable drugs market.

Prominent market participants contributing to industry growth include Cipla, Novo Nordisk, Akums Drugs and Pharmaceuticals, Merck, Aurobindo Pharma, Pfizer, Gilead Sciences, Sanofi, Johnson & Johnson, Takeda Pharmaceuticals, Vetter Pharma, Zydus, Meiji Group, Gufic Group, Fareva, Bristol Myers Squibb, Fresenius, F. Hoffmann-La Roche, and Bora Pharmaceuticals. To secure their market leadership, companies in the lyophilized injectable drugs industry are increasingly investing in high-capacity freeze-drying equipment and state-of-the-art manufacturing lines that meet stringent global regulatory standards. Many firms are expanding their contract manufacturing services, improving cold chain logistics, and integrating automation to reduce downtime and production costs. Strategic collaborations and licensing agreements are commonly used to gain access to innovative biologic compounds and expand product portfolios.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Drug type

- 2.2.3 Indication

- 2.2.4 Application

- 2.2.5 Age group

- 2.2.6 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of chronic and infectious diseases

- 3.2.1.2 Technological advancements in drug delivery systems

- 3.2.1.3 Rising demand for biologics and complex molecules

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production and equipment costs

- 3.2.2.2 Regulatory and quality compliance challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Personalized and precision medicine

- 3.2.3.2 Expansion of contract research and manufacturing services (CRAMS)

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Pricing analysis

- 3.6 Pipeline and R&D investment analysis

- 3.7 Patent landscape analysis

- 3.8 Parent market analysis

- 3.9 Regulatory landscape

- 3.9.1 North America

- 3.9.2 Europe

- 3.9.3 Asia Pacific

- 3.9.4 Latin America

- 3.9.5 Middle East and Africa

- 3.10 Future market trends

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

Chapter 5 Market Estimates and Forecast, By Drug Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Anti-infective

- 5.3 Anti-neoplastic

- 5.4 Anticoagulant

- 5.5 Hormones

- 5.6 Antiarrhythmic

- 5.7 Proton pump inhibitors

- 5.8 Anesthetics

- 5.9 Other drug types

Chapter 6 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Autoimmune diseases

- 6.3 Respiratory diseases

- 6.4 Gastrointestinal disorders

- 6.5 Oncology

- 6.6 Cardiovascular diseases

- 6.7 Infectious diseases

- 6.8 Hormonal disorders

- 6.9 Metabolic disorders

- 6.10 Reproductive health

- 6.11 Other indications

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Prefilled diluent syringes

- 7.3 Multi-step devices

Chapter 8 Market Estimates and Forecast, By Packaging, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Vials

- 8.3 Cartridges

- 8.4 Prefilled devices

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Specialty clinics

- 9.4 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 Japan

- 10.4.2 China

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Akums Drugs and Pharmaceuticals

- 11.2 Aurobindo Pharma

- 11.3 Bora Pharmaceuticals

- 11.4 Bristol Myers Squibb

- 11.5 Cipla

- 11.6 F. Hoffmann-La Roche

- 11.7 Fareva

- 11.8 Fresenius

- 11.9 Gilead Sciences

- 11.10 Gufic Group

- 11.11 Johnson & Johnson

- 11.12 Meiji Group

- 11.13 Merck

- 11.14 Novo Nordisk

- 11.15 Pfizer

- 11.16 Sanofi

- 11.17 Takeda Pharmaceuticals

- 11.18 Vetter Pharma

- 11.19 Zydus

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 155 Pages

- 納期

- 2~3営業日