複合碍子の市場機会と成長促進要因、産業動向分析、2025~2034年予測

Composite Insulators Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 165 Pages

- 納期

- 2~3営業日

- 商品コード

- 1797837

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

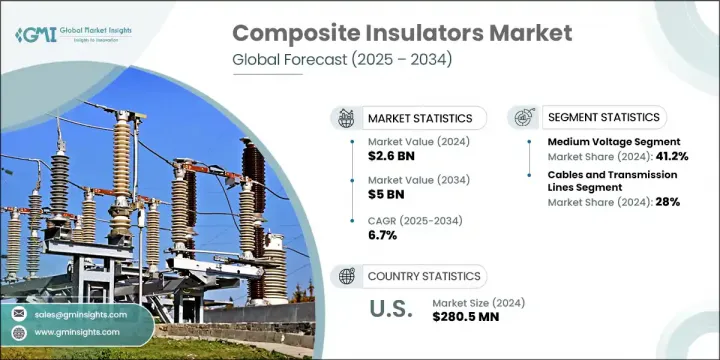

複合碍子の世界市場規模は、2024年に26億米ドルとなり、CAGR 6.7%で成長し、2034年には50億米ドルに達すると予測されています。

高電圧絶縁のニーズの拡大、材料技術革新の進歩、送電網の信頼性とエネルギー効率への注目の高まりが市場成長の原動力となっています。業界各社は、熱安定性の向上、耐用年数の延長、極限環境に対する耐性を備えた絶縁体を開発するため、多額の研究開発投資を行っています。風力や太陽光などの分散型エネルギー技術の統合が加速していることに加え、スマートグリッド基盤の高度化が進んでいることも、新たな市場機会を生み出し続けています。複合碍子は、低メンテナンスと長期にわたる運用信頼性により、汚染レベルが高く、機械的負荷が極端に高い地域でますます好まれるようになっています。

老朽化した送電網を近代化し、電力インフラのギャップを埋めるための政府の支援策も、この業界を前進させています。特に新興経済諸国では、送電網の拡大と長距離送電の開発が市場の潜在力を強化しています。中東やアフリカのような地域では、電力系統のアップグレード、新しいプラントの建設、インフラ投資が高い需要を刺激しています。これらの絶縁体は、厳しい天候下での効率的な運用と、先進的で持続可能なエネルギー・ネットワークをサポートする能力で受け入れられています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 26億米ドル |

| 予測金額 | 50億米ドル |

| CAGR | 6.7% |

中電圧セグメントは2024年に41.2%の最大市場シェアを占め、2034年までのCAGRは6%と予測されます。このセグメントの成長を支えているのは、地域の相互接続における役割の増大と、都市部と遠隔地に信頼性の高いエネルギーを供給するという重要なニーズです。メーカーは、中電圧絶縁体の機械的強度と電気的信頼性を高め、さまざまな設置環境における耐久性と機能性を最適化しています。

ケーブル・送電線セグメントは2024年に28%のシェアを占め、2034年までCAGR 5.5%で成長すると予測されています。安定的かつ効率的なエネルギー伝送システムの開発が、継続的な送電網の拡張と相まって、この分野における複合碍子の需要を強化しています。これらのユニットは、漏電電流の低減、絶縁特性の強化、負荷応力下での動作の改善など、従来の選択肢よりも優れた利点を提供します。また、遠隔地へのアクセスや十分なサービスを受けていない地域をターゲットとした電化イニシアチブも、新しい送電経路での採用を強化しています。

米国複合碍子市場は2024年に72%のシェアを占め、2億8,050万米ドルを生み出します。この地域の成長は、送電網の近代化と再生可能エネルギー統合への大規模投資によって形成されています。官民の利害関係者は、再生可能エネルギー源に対応しながら一貫したエネルギー供給を確保することを目指し、国のインフラを更新するための資本配分を増やしています。

世界の複合碍子市場を牽引する主要企業には、シーメンス・エナジー、PFISTERER、ハッベル、日立エナジー、TEコネクティビティなどがあります。大手メーカーは、市場での地位を高めるために多方面からのアプローチを実施しています。優れた耐候性と長寿命を提供する先進的な軽量複合材料を開発するため、研究開発に力を入れています。多くの開発企業は、電力会社と戦略的提携を結び、特定のグリッド課題向けにカスタマイズされた絶縁体ソリューションを共同開発しています。さらに、アフリカや東南アジアのような急速に開発が進んでいる地域への世界展開も、顧客基盤の拡大に役立っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 原材料の入手可能性の情勢

- バリューチェーンに影響を与える要因

- ディスラプション

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

- 複合碍子のコスト構造分析

- 新たな機会と動向

- デジタル化とIoTの統合

- 新興市場への浸透

- 投資分析と将来展望

第4章 競合情勢

- イントロダクション

- 地域別企業市場シェア

- 北米

- 欧州

- アジア太平洋地域

- 中東・アフリカ

- ラテンアメリカ

- 戦略的取り組み

- 競合ベンチマーキングの描写

- 戦略ダッシュボード

- イノベーションとテクノロジーの情勢

第5章 市場規模・予測:電圧別、2021-2034

- 主要動向

- 高電圧

- 中電圧

- 低電圧

第6章 市場規模・予測:用途別、2021-2034

- 主要動向

- ケーブルと送電線

- スイッチギア

- トランス

- バスバー

- その他

第7章 市場規模・予測:製品別、2021-2034

- 主要動向

- ピン絶縁体

- 懸垂碍子

- シャックル絶縁体

- その他の絶縁体

第8章 市場規模・予測:最終用途別、2021-2034

- 主要動向

- 住宅用

- 商業および工業

- ユーティリティ

第9章 市場規模・予測:評価順, 2021-2034

- 主要動向

- 11 kV未満

- 11 kV以上22 kV以下

- 22 kV以上33 kV以下

- 33 kV以上72.5 kV以下

- 72.5 kV以上145 kV以下

- 145 kV以上220 kV以下

- 220 kV以上400 kV以下

- 400 kV以上800 kV以下

- 800 kV以上1,200 kV以下

- 1,200 kV以上

第10章 市場規模・予測:設備別、2021-2034

- 主要動向

- 分布

- トランスミッション

- 変電所

- 鉄道

- その他

第11章 市場規模・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第12章 企業プロファイル

- Bonomi

- CYG Insulator

- CTC Insulator

- Deccan Enterprises

- ENSTO

- Gipro

- Hitachi Energy

- Hubbell

- Izoelektro

- Kuvag

- Nanjing Electric Technology

- Navitas Insulators

- Newell Porcelain

- Olectra Greentech

- Peak Demand

- Pfisterer

- Rayphen

- Siemens Energy

- Taporel

- TE Connectivity

目次

The Global Composite Insulators Market was valued at USD 2.6 billion in 2024 and is estimated to grow at a CAGR of 6.7% to reach USD 5 billion by 2034. The expanding need for high-voltage insulation, advances in material innovation, and rising attention to grid reliability and energy efficiency are fueling market growth. Industry players are making significant R&D investments to develop insulators that provide improved thermal stability, longer service life, and resistance to environmental extremes. The accelerating integration of distributed energy technologies, such as wind and solar, alongside the advancement of smart grid infrastructures, continues to generate new market opportunities. Composite insulators are increasingly favored in areas with high pollution levels and extreme mechanical loads due to their low maintenance and operational reliability over long periods.

Government-backed initiatives to modernize aging grids and bridge power infrastructure gaps are also pushing the industry forward. Grid expansion and long-distance transmission development, especially in emerging economies, are reinforcing market potential. In regions like the Middle East and Africa, power system upgrades, new plant constructions, and infrastructure investments are stimulating high demand. These insulators are being embraced for their efficient operation in harsh weather and their ability to support advanced, sustainable energy networks.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.6 Billion |

| Forecast Value | $5 Billion |

| CAGR | 6.7% |

The medium voltage segment held the largest market share of 41.2% in 2024 and is forecast to grow at a CAGR of 6% through 2034. The segment's growth is supported by its increasing role in regional interconnectivity and the critical need to deliver dependable energy across urban and remote regions. Manufacturers are enhancing the mechanical strength and electrical reliability of medium voltage insulators to optimize their durability and functionality across various installation environments.

The cables and transmission lines segment accounted for a 28% share in 2024 and is projected to grow at a CAGR of 5.5% through 2034. The drive to develop stable and efficient energy transmission systems, paired with continuous grid expansions, is reinforcing the demand for composite insulators in this segment. These units offer superior benefits over traditional options, including lower current leakage, enhanced insulation properties, and better operational outcomes under load stress. Electrification initiatives targeting remote access and underserved areas are also strengthening adoption across new transmission corridors.

United States Composite Insulators Market held a 72% share in 2024, generating USD 280.5 million. Growth in this region is being shaped by significant investments in grid modernization and renewable integration. Public and private stakeholders are increasingly allocating capital to update the nation's infrastructure, aiming to ensure consistent energy delivery while accommodating renewable energy sources.

Major companies driving the Global Composite Insulators Market include Siemens Energy, PFISTERER, Hubbell, Hitachi Energy, and TE Connectivity, among others. Leading manufacturers are implementing a multi-pronged approach to boost their market position. They are focusing heavily on R&D to develop advanced, lightweight composite materials that offer superior weather resistance and long operational life. Many players are entering strategic collaborations with utility companies to co-develop customized insulator solutions for specific grid challenges. Additionally, global expansion into fast-developing regions like Africa and Southeast Asia helps broaden their customer base.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability landscape

- 3.1.2 Factors affecting the value chain

- 3.1.3 Disruptions

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis for composite insulators

- 3.8 Emerging opportunities & trends

- 3.8.1 Digitalization & IoT integration

- 3.8.2 Emerging market penetration

- 3.9 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share, by region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic initiatives

- 4.4 Competitive benchmarking depictions

- 4.5 Strategy dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Voltage, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 High voltage

- 5.3 Medium voltage

- 5.4 Low voltage

Chapter 6 Market Size and Forecast, By Application, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Cables and transmission lines

- 6.3 Switchgears

- 6.4 Transformer

- 6.5 Bus Bars

- 6.6 Others

Chapter 7 Market Size and Forecast, By Product, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 Pin insulators

- 7.3 Suspension insulators

- 7.4 Shackle insulators

- 7.5 Other insulators

Chapter 8 Market Size and Forecast, By End Use, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial & Industrial

- 8.4 Utilities

Chapter 9 Market Size and Forecast, By Rating, 2021 - 2034 (USD Million)

- 9.1 Key trends

- 9.2 ≤ 11 kV

- 9.3 > 11 kV to ≤ 22 kV

- 9.4 > 22 kV to ≤ 33 kV

- 9.5 > 33 kV to ≤ 72.5 kV

- 9.6 > 72.5 kV to ≤ 145 kV

- 9.7 > 145 kV to ≤ 220 kV

- 9.8 > 220 kV to ≤ 400 kV

- 9.9 > 400 kV to ≤ 800 kV

- 9.10 > 800 kV to ≤ 1,200 kV

- 9.11 > 1,200 kV

Chapter 10 Market Size and Forecast, By Installation, 2021 - 2034 (USD Million)

- 10.1 Key trends

- 10.2 Distribution

- 10.3 Transmission

- 10.4 Substation

- 10.5 Railways

- 10.6 Others

Chapter 11 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.2.3 Mexico

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Middle East & Africa

- 11.5.1 Saudi Arabia

- 11.5.2 UAE

- 11.5.3 South Africa

- 11.6 Latin America

- 11.6.1 Brazil

- 11.6.2 Argentina

Chapter 12 Company Profiles

- 12.1 Bonomi

- 12.2 CYG Insulator

- 12.3 CTC Insulator

- 12.4 Deccan Enterprises

- 12.5 ENSTO

- 12.6 Gipro

- 12.7 Hitachi Energy

- 12.8 Hubbell

- 12.9 Izoelektro

- 12.10 Kuvag

- 12.11 Nanjing Electric Technology

- 12.12 Navitas Insulators

- 12.13 Newell Porcelain

- 12.14 Olectra Greentech

- 12.15 Peak Demand

- 12.16 Pfisterer

- 12.17 Rayphen

- 12.18 Siemens Energy

- 12.19 Taporel

- 12.20 TE Connectivity

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 165 Pages

- 納期

- 2~3営業日