縫合糸アンカーデバイス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Suture Anchor Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 135 Pages

- 納期

- 2~3営業日

- 商品コード

- 1797821

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

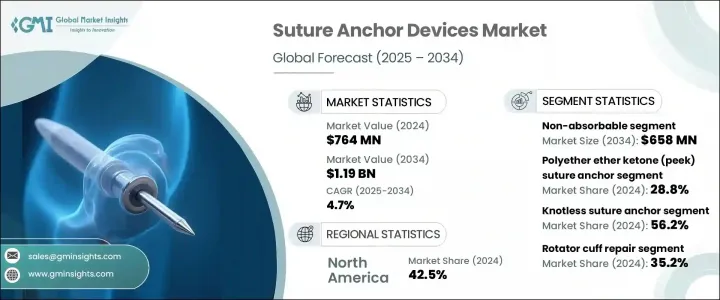

世界の縫合糸アンカーデバイス市場は、2024年に7億6,400万米ドルと評価され、CAGR 4.7%で成長し、2034年には11億9,000万米ドルに達すると推定されています。

この成長は主に、スポーツに関連した怪我の発生率の増加や、腱板修復術、アキレス腱症治療、十字靭帯再建術のような、縫合糸アンカーデバイスを一般的に使用する手術の増加によってもたらされています。これらのインプラントは、腱や靭帯などの軟部組織を骨に取り付けることにより、整形外科手術において重要な役割を果たしています。また、老年人口の拡大も、加齢に関連した疾患により多くの手術や介入が必要となるため、市場の成長に大きく寄与しています。業界の大手企業には、Arthrex社、Zimmer Biomet社、Smith &Nephew社、Stryker社などがあります。手術手技や材料の革新に伴い、縫合糸アンカーデバイスは固定強度、生体適合性、使いやすさを向上させるべく進化を続けています。

縫合糸アンカーは、外科手術の際に軟部組織を骨に固定するためのもので、現代の整形外科やスポーツ医学において不可欠なツールです。材料科学の進歩により、機械的強度と生体適合性が強化されたアンカーが開発され、より良い治療成績と患者満足度の向上が保証されています。これらの器具は、回復を成功させるために精度と組織保存が重要な低侵襲手術に不可欠です。回復時間の短縮と手術精度の向上がますます重視される中、高品質の縫合糸アンカーデバイスに対する需要は増加の一途をたどっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 7億6,400万米ドル |

| 予測金額 | 11億9,000万米ドル |

| CAGR | 4.7% |

2024年の縫合糸アンカーデバイス市場は、非吸収性セグメントが4億2,610万米ドルを占め、市場を独占しました。この分野は2034年には6億5,800万米ドルに達し、CAGR 4.5%で成長すると予測されています。非吸収性アンカーは、その優れた機械的強度と長期固定能力により、腱板や関節唇の修復のような高負荷の整形外科手術で好まれています。チタンやPEEK(ポリエーテルエーテルケトン)のような、高い生体適合性、放射線透過性、安定した性能を持つ素材の継続的使用が、非吸収性アンカーの需要を牽引しています。これらの材料は、アンカーが長期にわたって確実に機能し、修復組織に永続的な支持を与えることを保証します。

PEEK縫合糸アンカー・セグメントは2024年に28.8%を占め、市場で最大のシェアを占めています。PEEKアンカーが広く採用されているのは、その強力な臨床性能、安全性プロファイル、非金属性による外科医の嗜好によるものです。PEEKアンカーは優れた強度と放射線透過性を備えており、肩、膝、股関節の手術に理想的です。長期的な研究により、PEEKノットレスアンカーは生分解性アンカーに匹敵する性能を示すことが示されており、整形外科手術における安全で信頼性の高い選択肢としての地位がさらに確固たるものとなっています。

米国の縫合糸アンカーデバイス2024年の市場規模は2億9,980万米ドル。米国は、ロボット支援手術やPEEKベースの縫合糸アンカーなど、先進的な整形外科技術の導入で最先端を走っています。同国の強力な規制枠組み、国民の高い認知度、研究開発への多額の投資が市場成長の主な要因です。スポーツ外傷や加齢に伴う筋骨格系疾患の増加に伴い、米国市場は公衆衛生への取り組みと民間技術の革新の両方によって持続的な成長が見込まれています。

縫合糸アンカーデバイス市場の企業は、その地位を固め、市場シェアを拡大するために様々な戦略を採用しています。特に、複雑な手術に使用される縫合糸アンカーの性能と耐久性の向上に注力しています。また、多くの企業がPEEKベースや生体吸収性の縫合糸アンカーを導入して製品ポートフォリオを拡大し、これらの素材に対する需要の高まりに対応しています。もう一つの戦略は、病院、整形外科クリニック、研究機関と戦略的パートナーシップを結び、自社製品をより確実に普及させることです。さらに、現地の製造施設や流通網に投資して新興市場での存在感を高めることも、多くの大手企業にとって重要な焦点となっています。これらの企業はまた、ロボット支援手術のような技術的進歩を活用して、縫合糸アンカーデバイスを次世代外科手術に統合し、精度の向上と回復時間の短縮を実現しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- スポーツ事故の増加

- 高齢化人口の増加

- 低侵襲手術の需要

- アンカー設計における技術的進歩

- 業界の潜在的リスク&課題

- 高度なアンカーと手術の高コスト

- 術後合併症のリスク

- 市場機会

- AIとロボット支援手術の統合

- 生体適合性および生体吸収性材料の革新

- 促進要因

- 成長可能性分析

- 規制情勢

- 技術的進歩

- 現在の技術動向

- 新興技術

- サプライチェーン分析

- 価格分析、2024

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- 吸収性

- 非吸収性

第6章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- 金属製縫合糸アンカー

- 生体吸収性縫合糸アンカー

- ポリエーテルエーテルケトン(PEEK)縫合糸アンカー

- バイオコンポジット縫合糸アンカー

- オールソフト縫合糸アンカー

第7章 市場推計・予測:結び方別、2021年~2034年

- 主要動向

- ノットレス縫合糸アンカー

- ノットあり縫合糸アンカー

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 腱板修復

- アーキレス腱炎の修復

- 十字靭帯修復

- 上腕二頭筋腱固定術

- その他の用途

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院と診療所

- 外来手術センター

- その他の用途

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第11章 企業プロファイル

- Anika Therapeutics

- Arthrex

- ConMed

- Enovis Corporation

- Fuse Medical

- Johnson &Johnson

- MJ Surgical

- NeoSys

- Orthomed

- Ossio

- Parcus Medical

- SBM

- Smith &Nephew

- Stryker Corporation

- Teknimed

- Tulpar Medical Solutions

- Zimmer Biomet

目次

The Global Suture Anchor Devices Market was valued at USD 764 million in 2024 and is estimated to grow at a CAGR of 4.7% to reach USD 1.19 billion by 2034. This growth is primarily driven by the increasing incidence of sports-related injuries, as well as the rise in procedures like rotator cuff repair, Achilles tendinosis treatment, and cruciate ligament reconstruction, all of which commonly employ suture anchor devices. These implants play a crucial role in orthopedic surgeries by attaching soft tissues such as tendons and ligaments to bone. The expanding geriatric population is also contributing significantly to market growth, as age-related conditions require more surgeries and interventions. Leading players in the industry include Arthrex, Zimmer Biomet, Smith & Nephew, and Stryker. With innovations in surgical techniques and materials, suture anchor devices continue to evolve to offer improved fixation strength, biocompatibility, and ease of use.

Suture anchors are essential tools in modern orthopedic and sports medicine, designed to fasten soft tissue to bone during surgical procedures. Advancements in materials science have led to the development of anchors with enhanced mechanical strength and biocompatibility, ensuring better outcomes and increased patient satisfaction. These devices are integral to minimally invasive surgeries, where precision and tissue preservation are critical for successful recovery. With a growing emphasis on reducing recovery times and improving surgical precision, the demand for high-quality suture anchor devices continues to rise.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $764 Million |

| Forecast Value | $1.19 Billion |

| CAGR | 4.7% |

The non-absorbable segment dominated the suture anchor devices market in 2024, accounting for USD 426.1 million. This segment is projected to reach USD 658 million by 2034, growing at a CAGR of 4.5%. Non-absorbable anchors are preferred in high-load orthopedic procedures, such as rotator cuff and labral repairs, due to their superior mechanical strength and long-term fixation capabilities. The continued use of materials like titanium and PEEK (polyether ether ketone), which offer high biocompatibility, radiolucency, and consistent performance, is driving the demand for non-absorbable anchors. These materials ensure that the anchors perform reliably over time, providing permanent support to repaired tissues.

The PEEK suture anchor segment held the largest share of the market, accounting for 28.8% in 2024. The widespread adoption of PEEK anchors is attributed to their strong clinical performance, safety profile, and preference among surgeons for their non-metallic nature. PEEK anchors offer excellent strength and radiolucency, making them ideal for use in shoulder, knee, and hip surgeries. Long-term studies have shown that PEEK knotless anchors perform comparably to biodegradable anchors, further cementing their position as a safe and reliable choice for orthopedic procedures.

United States Suture Anchor Devices Market was valued at USD 299.8 million in 2024. The U.S. is at the forefront of adopting advanced orthopedic technologies, including robotic-assisted surgeries and PEEK-based suture anchors. The country's strong regulatory framework, high levels of public awareness, and substantial investments in research and development are major contributors to market growth. With the increasing prevalence of sports injuries and age-related musculoskeletal conditions, the U.S. market is expected to experience sustained growth, driven by both public health initiatives and innovations in private sector technologies.

Major players in the Suture Anchor Devices Market include Smith & Nephew, Stryker Corporation, Zimmer Biomet, Arthrex, and ConMed. Companies in the suture anchor devices market employ a range of strategies to solidify their position and increase market share. A key strategy is the continuous innovation in materials and device design, particularly focusing on improving the performance and durability of suture anchors used in complex surgeries. Many companies are also expanding their product portfolios by introducing PEEK-based and bioabsorbable suture anchors, catering to the growing demand for these materials. Another strategy involves forming strategic partnerships with hospitals, orthopedic clinics, and research institutions to ensure better adoption of their products. In addition, enhancing their presence in emerging markets by investing in local manufacturing facilities and distribution networks is a key focus for many leading players. These companies are also leveraging technological advancements such as robotic-assisted surgery to integrate suture anchor devices into next-gen surgical procedures, ensuring improved accuracy and faster recovery times.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Material trends

- 2.2.4 Tying type trends

- 2.2.5 Application trends

- 2.2.6 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising number of sports accidents

- 3.2.1.2 Increasing geriatric population

- 3.2.1.3 Demand for minimally invasive surgeries

- 3.2.1.4 Technological advancements in anchor design

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced anchors and surgery

- 3.2.2.2 Risk of post operative complications

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of AI and robotic assisted surgery

- 3.2.3.2 Innovation in biocompatible and bioabsorbable materials

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Supply chain analysis

- 3.7 Pricing analysis, 2024

- 3.8 Future market trends

- 3.9 Gap analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Absorbable

- 5.3 Non absorbable

Chapter 6 Market Estimates and Forecast, By Material, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Metallic suture anchor

- 6.3 Bio absorbable suture anchor

- 6.4 Polyether ether ketone (PEEK) suture anchor

- 6.5 Bio composite suture anchor

- 6.6 All soft suture anchor

Chapter 7 Market Estimates and Forecast, By Tying Type, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Knotless suture anchor

- 7.3 Knotted suture anchor

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Rotator cuff repair

- 8.3 Archilles tendinosis repair

- 8.4 Cruciate ligament repairs

- 8.5 Biceps tenodesis

- 8.6 Other applications

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospital and clinics

- 9.3 Ambulatory surgical centres

- 9.4 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Anika Therapeutics

- 11.2 Arthrex

- 11.3 ConMed

- 11.4 Enovis Corporation

- 11.5 Fuse Medical

- 11.6 Johnson & Johnson

- 11.7 MJ Surgical

- 11.8 NeoSys

- 11.9 Orthomed

- 11.10 Ossio

- 11.11 Parcus Medical

- 11.12 SBM

- 11.13 Smith & Nephew

- 11.14 Stryker Corporation

- 11.15 Teknimed

- 11.16 Tulpar Medical Solutions

- 11.17 Zimmer Biomet

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 135 Pages

- 納期

- 2~3営業日