マイクロLEDの市場機会、成長促進要因、産業動向分析、2025~2034年予測

Micro-LED Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1797785

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

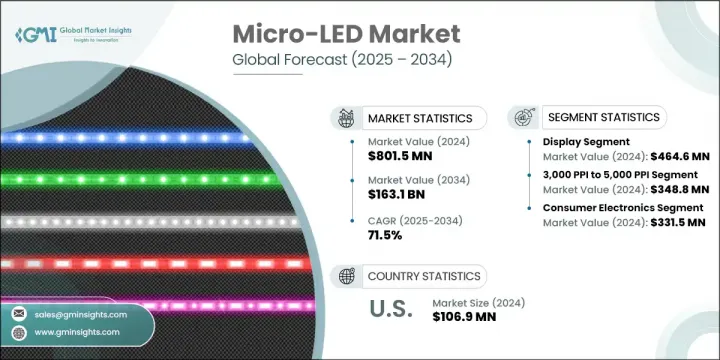

マイクロLEDの世界市場は、2024年には8億150万米ドルとなり、CAGR 71.5%で成長し、2034年には1,631億米ドルに達すると予測されています。

この堅調な拡大は、さまざまな用途でエネルギー効率が高く高性能なディスプレイ技術に対する需要が高まっていることが背景にあります。この成長の背景には、デジタルダッシュボード、ARヘッドアップディスプレイ、高解像度のインフォテインメントパネルが標準となりつつある自動車システムにマイクロLEDが広く採用されていることがあります。さらに、次世代テレビ、高度なデジタルサイネージ、プレミアムなビジュアル体験に対する消費者の嗜好の高まりが、家電および広告分野でのマイクロLED採用を後押ししています。

優れた輝度、エネルギー効率、耐久性を持つマイクロLEDディスプレイは、従来のOLEDやLCD技術に代わる選択肢として注目されています。また、ウェアラブル・エレクトロニクス、スマート・ウィンドウ、小売ベースのサイネージなどの新しいアプリケーションに対応するため、モジュラー・アーキテクチャーと超薄型材料で設計されたフレキシブルで透明なディスプレイへのシフトも進んでいます。製造コストが低下し続ける中、特に品質と長寿命ディスプレイが最重要視されるプレミアム・セグメントにおいて、より広範な商業化が予想されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 8億150万米ドル |

| 予測金額 | 1,631億米ドル |

| CAGR | 71.5% |

2024年、マイクロLED市場のディスプレイ分野の売上高は4億6,460万米ドルでした。個人用電子機器における超高精細で電力効率の高いディスプレイのニーズにより、需要は急増を続けています。マイクロLEDパネルは、高輝度、広色域、高コントラスト、長寿命により、OLEDやLCDを凌駕しています。そのため、AR/VR機器や次世代スマートウォッチに組み込むには特に魅力的です。世界のハイテク企業による研究開発努力の高まりは、普及をさらに加速させ、コンシューマー・エレクトロニクス全体のイノベーションを後押ししています。

3,000 PPIから5,000 PPIのセグメントは、2024年に3億4,880万米ドルを生み出しました。この画素範囲はディスプレイの鮮明さと電力効率のバランスをうまくとっており、プレミアム・エレクトロニクスや没入型リアリティ・アプリケーションにとって非常に魅力的です。主要なディスプレイ研究グループは、この解像度が複合現実環境において実物そっくりの体験を提供する上でますます重要になると指摘しています。マイクロディスプレイの研究開発への継続的な投資-特に防衛グレードの光学部品と高性能ウェアラブルをターゲットとする-は、多様なハイエンド市場で勢いを強めています。

米国マイクロLED市場は2024年に1億690万米ドルを創出しました。この優位性は、マイクロエレクトロニクスやディスプレイイノベーションに特化した大規模な連邦政府資金提供プログラムなど、先端半導体製造を促進する戦略的な国家政策に支えられています。こうした投資は、次世代ディスプレイ技術のサプライチェーンを強化する一方で、国内生産能力の再構築に役立っています。米国は、スマートフォン、ウェアラブル端末、AR/VR端末、その他のスマートシステムにおけるマイクロLEDソリューションの展開に注力する企業によって、世界・イノベーション・リーダーであり続けています。

世界のマイクロLED市場はダイナミックで非常に細分化されており、既存プレーヤーと新興イノベーターによる競争環境が特徴です。主な参加企業は、BOE Technology、ソニー株式会社、LG Display Co., Ltd.、サムスン電子、Epistar Corporationなどです。主要企業は市場での地位を強化するため、ディスプレイ性能、エネルギー効率、生産拡張性を高める研究開発に多額の投資を行っています。材料サプライヤーや半導体メーカーとの戦略的提携は、多様なアプリケーションにおけるマイクロLED統合の合理化に役立っています。各社はまた、革新的な製造技術や知的財産へのアクセスを得るために買収を進めています。いくつかの企業は、外部サプライヤーへの依存度を下げるため、内部製造能力に注力しており、これによってサプライチェーン・コントロールが向上しています。自動車からウェアラブルまで、さまざまな業界の需要に応えるため、カスタマイズやモジュール製品の開発が進められています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- エコシステム分析

- 業界への影響要因

- 促進要因

- ウェアラブル技術の成長

- 優れた表示性能

- 省エネディスプレイの需要増加

- 自動車アプリケーションへの急速な導入

- 高級テレビやデジタルサイネージの需要

- 落とし穴と課題

- 製造コストの高さと歩留まりの問題

- OLEDとミニLEDとの競合

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 新たなビジネスモデル

- コンプライアンス要件

- 持続可能性対策

- 特許および知的財産分析

- 地政学と貿易のダイナミクス

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 市場集中分析

- 地域別

- 主要プレーヤーの競合ベンチマーキング

- 財務実績の比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオの比較

- 製品ラインナップの広さ

- テクノロジー

- 革新

- 地理的プレゼンスの比較

- 世界フットプリント分析

- サービスネットワークの範囲

- 地域別の市場浸透率

- 競合ポジショニングマトリックス

- リーダーたち

- 課題者たち

- フォロワー

- ニッチプレイヤー

- 戦略的展望マトリックス

- 財務実績の比較

- 主な発展, 2021-2024

- 合併と買収

- パートナーシップとコラボレーション

- 技術的進歩

- 拡大と投資戦略

- 持続可能性への取り組み

- デジタル変革の取り組み

- 新興企業/スタートアップ企業の競合情勢

第5章 市場推計・予測:技術別、2021-2034

- 主要動向

- RGBフルカラー

- モノクロ

第6章 市場推計・予測:ピクセル密度別、2021-2034

- 主要動向

- 3,000ppi未満

- 3,000ppiから5000ppi

- 5000ppi以上

第7章 市場推計・予測:用途別、2021-2034

- 主要動向

- ディスプレイ

- AR/VRヘッドセット

- スマートウォッチ

- スマートフォン

- タブレットとノートパソコン

- テレビとモニター

- デジタルサイネージとビデオウォール

- その他

- 点灯

- 一般照明

- 自動車用照明

- その他

第8章 市場推計・予測:産業別、2021-2034

- 主要動向

- 家電

- 自動車

- 航空宇宙および防衛

- ヘルスケア

- 小売・ホスピタリティ

- その他

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- Global Key Players

- Regional Key Players

- 破壊的イノベーション/ニッチプレーヤー

- 不在

- レイヤード

- TCL CSOT

目次

The Global Micro-LED Market was valued at USD 801.5 million in 2024 and is estimated to grow at a CAGR of 71.5% to reach USD 163.1 billion by 2034. This robust expansion is driven by rising demand for energy-efficient, high-performance display technologies across various applications. A major catalyst behind this growth is the widespread adoption of micro-LEDs in automotive systems, where digital dashboards, AR heads-up displays, and high-resolution infotainment panels are becoming standard. In addition, the increasing consumer preference for next-generation televisions, advanced digital signage, and premium visual experiences is boosting micro-LED adoption in the consumer electronics and advertising sectors.

With superior brightness, energy efficiency, and durability, micro-LED displays emerge as the go-to alternative over traditional OLED and LCD technologies. The market is also witnessing a strong shift toward flexible and transparent displays designed with modular architecture and ultra-thin materials, aligning with new applications such as wearable electronics, smart windows, and retail-based signage. As production costs continue to decline, broader commercialization is anticipated, particularly in premium segments where quality and longevity display are of paramount importance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $801.5 Million |

| Forecast Value | $163.1 Billion |

| CAGR | 71.5% |

In 2024, the display segment in the micro-LED market generated USD 464.6 million. Demand continues to surge due to the need for ultra-high-definition and power-efficient displays in personal electronic devices. Micro-LED panels outperform OLED and LCD alternatives by offering enhanced brightness, broader color range, higher contrast, and significantly longer lifespan. This makes them especially appealing for integration in AR/VR devices and next-gen smartwatches. Growing research and development efforts by global tech giants are further accelerating adoption and pushing innovation across consumer electronics.

The 3,000 PPI to 5,000 PPI segment generated USD 348.8 million in 2024. This pixel range strikes a strong balance between display clarity and power efficiency, making it highly attractive for premium electronics and immersive reality applications. Leading display research groups have identified this resolution as increasingly critical in delivering lifelike experiences in mixed reality environments. Continued investment in micro-display R&D-especially targeting defense-grade optics and high-performance wearables-is reinforcing momentum across diverse high-end markets.

United States Micro-LED Market generated USD 106.9 million in 2024. This dominance is supported by strategic national policies promoting advanced semiconductor manufacturing, such as large-scale federal funding programs dedicated to microelectronics and display innovation. These investments are helping reshape domestic production capabilities while reinforcing the supply chain for next-generation display technologies. The US continues to be a global innovation leader, with a strong corporate focus on deploying micro-LED solutions across smartphones, wearables, AR/VR devices, and other smart systems.

The Global Micro-LED Market is dynamic and highly fragmented, featuring a competitive landscape of established players and emerging innovators. Key participants include BOE Technology, Sony Corporation, LG Display Co., Ltd., Samsung Electronics, and Epistar Corporation. To strengthen their market position, leading micro-LED companies are heavily investing in research and development to enhance display performance, energy efficiency, and production scalability. Strategic collaborations with material suppliers and semiconductor manufacturers are helping streamline micro-LED integration across diverse applications. Companies are also pursuing acquisitions to gain access to innovative manufacturing techniques and intellectual property. Several players are focusing on internal fabrication capabilities to reduce reliance on external suppliers, which improves supply chain control. Customization and modular product offerings are being developed to cater to varying industry demands, from automotive to wearables.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Technology trends

- 2.2.2 Pixel density trends

- 2.2.3 Application trends

- 2.2.4 End use industry trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2025-2034 (USD Billion)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry ecosystem analysis

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Growth in wearable technology

- 3.3.1.2 Superior display performance

- 3.3.1.3 Increasing demand for energy-efficient displays

- 3.3.1.4 Rapid adoption in automotive applications

- 3.3.1.5 Demand for high-end televisions and digital signage

- 3.3.2 Pitfalls and challenges

- 3.3.2.1 High manufacturing costs and yield issues

- 3.3.2.2 Competition from OLED and mini LED

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.5.4 Latin America

- 3.5.5 Middle East & Africa

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Technology and Innovation landscape

- 3.8.1 Current technological trends

- 3.8.2 Emerging technologies

- 3.9 Emerging business models

- 3.10 Compliance requirements

- 3.11 Sustainability measures

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Technology, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 RGB full-color

- 5.3 Monochrome

Chapter 6 Market Estimates and Forecast, By Pixel Density, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Less than 3,000ppi

- 6.3 3,000ppi to 5000ppi

- 6.4 Greater than 5000ppi

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 Displays

- 7.2.1 AR/VR headsets

- 7.2.2 Smartwatches

- 7.2.3 Smartphones

- 7.2.4 Tablets & laptops

- 7.2.5 Televisions & monitors

- 7.2.6 Digital signage & video walls

- 7.2.7 Others

- 7.3 Lighting

- 7.3.1 General lighting

- 7.3.2 Automotive lighting

- 7.3.3 Others

Chapter 8 Market Estimates and Forecast, By Industry, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 Consumer electronics

- 8.3 Automotive

- 8.4 Aerospace & defense

- 8.5 Healthcare

- 8.6 Retail & hospitality

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Samsung Electronics

- 10.1.2 Sony Corporation

- 10.1.3 LG Display Co., Ltd.

- 10.1.4 BOE Technology

- 10.1.5 AU Optronics (AUO)

- 10.2 Regional Key Players

- 10.2.1 North America

- 10.2.1.1 X-Celeprint

- 10.2.1.2 Nanosys

- 10.2.1.3 Kopin Corp

- 10.2.1.4 eLux Inc

- 10.2.1.5 VueReal

- 10.2.2 Europe

- 10.2.2.1 Aledia SA

- 10.2.2.2 Plessey Semiconductors

- 10.2.2.3 MICLEDI Microdisplays

- 10.2.3 Asia-Pacific

- 10.2.3.1 Epistar Corporation

- 10.2.3.2 PlayNitride

- 10.2.3.3 Jade Bird Display (JBD)

- 10.2.3.4 Konka Global

- 10.2.1 North America

- 10.3 Disruptors / Niche Players

- 10.3.1 Absen

- 10.3.2 Leyard

- 10.3.3 TCL CSOT

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日