|

市場調査レポート

商品コード

1797780

電動フォークリフトの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Electric Forklift Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 電動フォークリフトの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年07月24日

発行: Global Market Insights Inc.

ページ情報: 英文 140 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

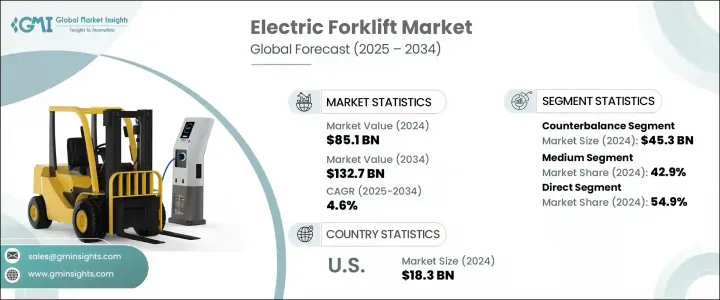

世界の電動フォークリフト市場は、2024年には851億米ドルとなり、CAGR 4.6%で成長し、2034年には1,327億米ドルに達すると推定されています。

この着実な成長の原動力となっているのは、内燃機関からより持続可能なバッテリー駆動への移行が進んでいることです。産業界がよりクリーンでコスト効率の高いマテリアルハンドリングソリューションを求める中、電動フォークリフトは物流、倉庫管理、製造、小売の各分野で大きな支持を集めています。環境に優しいオペレーションと総所有コストの低減に対する需要の高まりは、排出ガスの低減、騒音の低減、効率の改善を提供する電動フォークリフトモデルの採用を企業に促しています。政府や規制機関がより厳しい排出基準を推進し続ける中、電動フォークリフトは多くの先進国や新興経済諸国において好ましい選択肢となりつつあります。

成長を促進する主な要因は、バッテリー技術の急速な進化です。鉛バッテリーは歴史的にほとんどの電動フォークリフトに電力を供給してきたが、充電サイクルの長さと継続的なメンテナンスに悩まされてきました。対照的に、リチウムイオン・バッテリーは、より速い充電、より高いエネルギー密度、最小限のメンテナンス要件を提供することにより、市場を再形成しています。また、リチウムイオンバッテリーは「機会充電」にも対応しており、オペレーターは短時間の作業中断中にバッテリーの寿命を縮めることなく、バッテリーの電力を補充することができます。この機能により、作業時間中、機械をより長く稼働させることができ、生産性の向上に貢献します。水素燃料電池技術の出現も、特に要求の厳しい産業用アプリケーションで注目を集めています。これらのシステムは、しばしば3分未満という超高速の燃料補給と、一貫した中断のないワークフローを可能にする長時間の稼働を提供します。燃料電池は、ダウンタイムを最小限に抑える必要があり、長時間のシフトが一般的な場合に実用的な選択肢となりつつあります。いくつかのメーカーは、水素ベースのシステムを活用することで、バッテリー駆動のユニットと比較してダウンタイムを2桁削減することに成功しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 851億米ドル |

| 予測金額 | 1,327億米ドル |

| CAGR | 4.6% |

製品タイプのうち、カウンターバランス電動フォークリフトセグメントは2024年に453億米ドルを生み出し、2025年から2034年にかけてCAGR 3.5%で成長すると予測されています。これらのモデルは、世界で販売されたフォークリフトユニットの60%近くを占めており、その多用途性と簡単な操作性により、市場の主力製品であり続けています。これらのフォークリフトの構造には、重い前端荷を持ち上げる際に安定性を提供する後部カウンターウェイトが含まれており、大容量・高頻度の持ち上げ環境に理想的です。

中容量電動フォークリフトセグメントは2024年に42.9%のシェアを占め、2025年から2034年までCAGR 5.1%で成長すると予測されています。これらのモデルは、自動車、製造業、港湾、物流拠点など、持ち上げ能力と操縦性のバランスが求められる作業で好まれています。リチウムイオンバッテリーの進歩により、エネルギー密度が200Wh/kgと、ほんの数年前の2倍以上に高まったため、これらのフォークリフトは現在、長時間のシフトでも運転でき、わずか1~2時間で再充電できるようになり、実用性がさらに高まっています。

米国電動フォークリフト2024年の市場規模は183億米ドルで、2034年までCAGR 5.3%で成長すると予測されています。同国のリーダーシップは、確立された製造インフラ、自動化主導のオペレーション、持続可能性を求める強力な規制の推進に起因しています。活況を呈しているeコマースと倉庫管理分野がフォークリフト需要の急増に寄与しており、電動モデルは運転コストと排出ガスの低減を実現しています。米国はまた、製造業者と販売業者の強力な基盤、広範なサービスネットワーク、熟練労働力からも恩恵を受けており、電動フォークリフトの革新と展開における世界的リーダーとして位置づけられています。

世界の電動フォークリフト市場をリードする主なプレーヤーには、Hyster-Yale Materials Handling, Inc.、Toyota Material Handling、Mitsubishi Logisnext Co.Ltd.、KION Group AG、Jungheinrich AGが含まれる。競合戦略の面では、主要電動フォークリフトメーカーは、バッテリー技術、システム統合、インテリジェント車両管理プラットフォームを強化するための研究開発に積極的に投資しています。その多くは、多様なアプリケーションのニーズに適応するモジュラー・バッテリー・パックとスケーラブルなエネルギー・システムに注力しています。エネルギー企業やインフラ・プロバイダーとのコラボレーションは、バッテリー充電や水素補給ステーションの合理化に役立っています。メーカー各社はまた、テレマティクスや遠隔診断機能の向上にも取り組んでおり、フリートオペレーターが性能を監視し、メンテナンスを計画し、フリート利用率を最適化できるようにしています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- バッテリー技術の進歩

- 環境規制と持続可能性の目標

- eコマースと倉庫業の成長

- 業界の潜在的リスク&課題

- 初期投資コストが高め

- 限られた高耐久性

- 機会

- 新興市場への進出

- スマート倉庫との統合

- 急速充電および交換可能なバッテリーソリューションの開発

- 促進要因

- 成長可能性分析

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 規制の枠組み

- 規格と認証

- 環境規制

- 輸出入規制

- 貿易統計

- 主要輸入国

- 主要輸出国

- ポーター分析

- PESTEL分析

- 消費者行動分析

- 購入パターン

- 嗜好分析

- 消費者行動の地域差

- eコマースが購買決定に与える影響

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:タイプ別、2021-2034

- 主要動向

- カウンターバランス

- 倉庫用フォークリフト

- パレットジャッキとスタッカー

- リーチトラック

- その他

第6章 市場推計・予測:容量別、2021-2034

- 主要動向

- 小型(3トン未満)

- 中型(3~10トン)

- 重量(10トン以上)

第7章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 工場

- 倉庫

- 小売店

- 食品・医薬品

- 建設現場

- その他

第8章 市場推計・予測:流通チャネル別、2021-2034

- 主要動向

- 直接

- 間接的

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- マレーシア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

第10章 企業プロファイル

- Anhui Heli Co., Ltd.

- Clark Material Handling Company

- Crown Equipment Corporation

- Doosan Industrial Vehicle Co., Ltd.

- EP Equipment Co., Ltd.

- Hangcha Group Co., Ltd.

- Hyster-Yale Materials Handling, Inc.

- Hyundai Material Handling

- Jungheinrich AG

- KION Group AG

- Komatsu Ltd.

- Lonking Holdings Limited

- Mitsubishi Logisnext Co., Ltd.

- Noblelift Intelligent Equipment Co., Ltd.

- Toyota Material Handling

The Global Electric Forklift Market was valued at USD 85.1 billion in 2024 and is estimated to grow at a CAGR of 4.6% to reach USD 132.7 billion by 2034. This steady growth is being driven by the ongoing transition from internal combustion engines to more sustainable, battery-powered alternatives. As industries seek cleaner and more cost-efficient material handling solutions, electric forklifts are gaining significant traction across logistics, warehousing, manufacturing, and retail sectors. The growing demand for environmentally friendly operations and lower total cost of ownership is pushing businesses to adopt electric forklift models that offer reduced emissions, less noise, and improved efficiency. With governments and regulatory bodies continuing to push stricter emissions standards, electric forklifts are becoming a preferred choice in many developed and developing economies.

A key factor driving growth is the rapid evolution in battery technologies. While lead-acid batteries have historically powered most electric forklifts, they suffer from lengthy charge cycles and ongoing maintenance. In contrast, lithium-ion batteries are reshaping the market by offering faster charging, higher energy density, and minimal maintenance requirements. They also support "opportunity charging," which allows operators to top up battery power during brief operational breaks without diminishing battery life. This feature helps improve productivity by keeping machines operational longer throughout the workday. The emergence of hydrogen fuel cell technology is also gaining attention, especially for demanding industrial applications. These systems offer ultra-fast refueling-often under three minutes-and extended operation times that allow for consistent, uninterrupted workflow. Fuel cells are becoming a practical alternative where downtime needs to be minimized and long shifts are common. Several manufacturers are leveraging hydrogen-based systems to reduce downtime by double-digit percentages compared to battery-powered units.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $85.1 Billion |

| Forecast Value | $132.7 Billion |

| CAGR | 4.6% |

Among the product types, the counterbalance electric forklifts segment generated USD 45.3 billion in 2024 and is expected to grow at a CAGR of 3.5% between 2025 and 2034. These models represent nearly 60% of the total forklift units sold globally and remain the workhorse of the market due to their versatility and straightforward operation. Their construction includes rear counterweights that provide stability when lifting heavy front-end loads, making them ideal for high-capacity, high-frequency lifting environments.

The medium-capacity electric forklifts segment held 42.9% share in 2024 and is forecast to grow at a CAGR of 5.1% from 2025 to 2034. These models are favored in operations that demand a balance between lifting capacity and maneuverability-such as in automotive, manufacturing, ports, and distribution hubs. With lithium-ion battery advancements pushing energy densities as high as 200 Wh/kg-more than double what was available just a few years ago-these forklifts can now operate for extended shifts and recharge in just 1 to 2 hours, further enhancing their practicality.

United States Electric Forklift Market generated USD 18.3 billion in 2024 and is projected to grow at a CAGR of 5.3% through 2034. The country's leadership is attributed to its well-established manufacturing infrastructure, automation-driven operations, and a strong regulatory push for sustainability. The booming e-commerce and warehousing segments are contributing to soaring forklift demand, with electric models offering lower operating costs and emissions. The U.S. also benefits from a strong base of manufacturers and distributors, extensive service networks, and a skilled labor force, positioning it as a global leader in electric forklift innovation and deployment.

Key players leading the Global Electric Forklift Market include Hyster-Yale Materials Handling, Inc., Toyota Material Handling, Mitsubishi Logisnext Co., Ltd., KION Group AG, and Jungheinrich AG. In terms of competitive strategies, major electric forklift manufacturers are aggressively investing in research and development to enhance battery technologies, system integration, and intelligent fleet management platforms. Many are focusing on modular battery packs and scalable energy systems that adapt to diverse application needs. Collaborations with energy companies and infrastructure providers help streamline battery charging and hydrogen refueling stations. Manufacturers are also working to improve telematics and remote diagnostics capabilities, allowing fleet operators to monitor performance, schedule maintenance, and optimize fleet utilization.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021-2034

- 2.2 Key market trends

- 2.2.1 Business trends

- 2.2.2 Regional trends

- 2.2.3 Type trends

- 2.2.4 Capacity trends

- 2.2.5 End use trends

- 2.2.6 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry Impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Advancements in battery technology

- 3.2.1.2 Environmental regulations & sustainability goals

- 3.2.1.3 Growth of e-commerce and warehousing

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial investment costs

- 3.2.2.2 Limited heavy-duty capabilities

- 3.2.3 Opportunities

- 3.2.3.1 Expansion into emerging markets

- 3.2.3.2 Integration with smart warehousing

- 3.2.3.3 Development of fast-charging and swappable battery solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and Innovation Landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory framework

- 3.7.1 Standards and certifications

- 3.7.2 Environmental regulations

- 3.7.3 Import export regulations

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Consumer behavior analysis

- 3.11.1 Purchasing patterns

- 3.11.2 Preference analysis

- 3.11.3 Regional variations in consumer behavior

- 3.11.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Counterbalance

- 5.3 Warehouse Forklifts

- 5.3.1 Pallet jacks and stackers

- 5.3.2 Reach trucks

- 5.3.3 Others

Chapter 6 Market Estimates & Forecast, By Capacity, 2021-2034, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Small (under 3 tons)

- 6.3 Medium (3-10 tons)

- 6.4 Heavy (over 10 tons)

Chapter 7 Market Estimates & Forecast, By End use, 2021-2034, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Factories

- 7.3 Warehouses

- 7.4 Retail stores

- 7.5 Food and pharma

- 7.6 Construction sites

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Distribution channel, 2021-2034, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct

- 8.3 Indirect

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Malaysia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 UAE

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Anhui Heli Co., Ltd.

- 10.2 Clark Material Handling Company

- 10.3 Crown Equipment Corporation

- 10.4 Doosan Industrial Vehicle Co., Ltd.

- 10.5 EP Equipment Co., Ltd.

- 10.6 Hangcha Group Co., Ltd.

- 10.7 Hyster-Yale Materials Handling, Inc.

- 10.8 Hyundai Material Handling

- 10.9 Jungheinrich AG

- 10.10 KION Group AG

- 10.11 Komatsu Ltd.

- 10.12 Lonking Holdings Limited

- 10.13 Mitsubishi Logisnext Co., Ltd.

- 10.14 Noblelift Intelligent Equipment Co., Ltd.

- 10.15 Toyota Material Handling