航空機整備予測の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Predictive Airplane Maintenance Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1797776

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

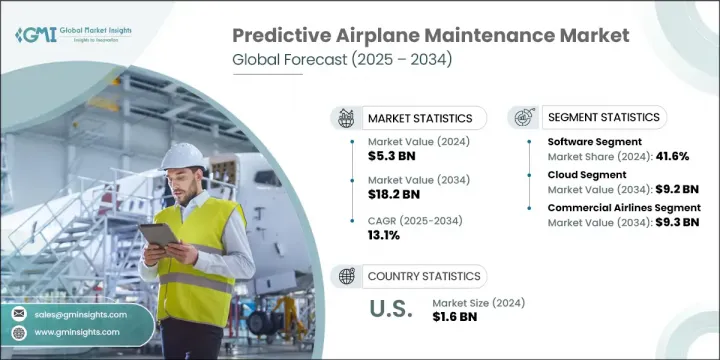

航空機整備予測の世界市場規模は、2024年には53億米ドルとなり、CAGR 13.1%で成長し、2034年には182億米ドルに達すると予測されています。

この成長の主な要因は、世界の航空交通量の増加と継続的な航空機の拡大です。航空分野では、高度なモノのインターネット(IoT)ソリューションと高度な分析を導入して保守作業を強化する動きが加速しています。航空需要が拡大する中、航空機の安全性を確保し、信頼性を高め、運航効率を最大化するためには、予知保全が不可欠になっています。航空会社と整備・修理・オーバーホール(MRO)プロバイダーは、人工知能と機械学習を活用して故障検出を強化し、故障を予測することで、事前予防的な整備スケジュールを可能にし、予期せぬダウンタイムを最小限に抑えています。この進化により、航空機の稼働時間が向上し、リソースの配置が世界に最適化されます。しかし、これらのプラットフォームは相互接続されたデータシステムに依存しているため、新たな脅威から機密情報を保護するためのサイバーセキュリティ対策が不可欠となっています。

2024年には、ソフトウェア・セグメントが41.6%の最大市場シェアを占める。航空機整備予測ソフトウェアは、リアルタイムのデータ処理、故障特定、故障予測に不可欠です。同市場では、拡張性とカスタマイズ性を考慮して調整されたAI主導の自動化ソリューションへの投資が増加しており、既存の航空会社の業務とのシームレスな統合と需要の変化への適応が可能になっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 53億米ドル |

| 予測金額 | 182億米ドル |

| CAGR | 13.1% |

一方、クラウド分野は2034年までに92億米ドルに達すると予測されています。クラウドプラットフォームは、リモートアクセス、柔軟性、リアルタイムのデータストリーミングを容易にし、コラボレーションと意思決定を強化します。データ・セキュリティや遅延に関する懸念は根強いもの、初期コストの削減やシステム・アップグレードの合理化により、導入が進んでいます。プロバイダーは、堅牢なサイバーセキュリティとハイブリッド・クラウド・アーキテクチャを提供することで対応しています。

北米航空機整備予測2024年のシェアは36.5%で、2034年までのCAGRは12.1%と予想されます。同地域は、広範な航空インフラ、予測技術の積極的な採用、航空整備におけるデジタル革新を支援する強力な規制枠組みなどのメリットを享受しています。この市場を牽引する主要企業には、IBM、ルフトハンザテクニーク、ボーイング社、エアバスSE、ゼネラル・エレクトリック社などがあります。

市場での地位を強化するため、航空機整備予測市場の企業はいくつかの戦略的アプローチに注力しています。これには、AIと機械学習機能を強化し、より正確で自動化された診断を可能にするための研究開発への多額の投資が含まれます。また、航空会社やMROプロバイダーとの戦略的パートナーシップやコラボレーションを追求し、市場への浸透を深め、顧客のニーズに合わせたソリューションを提供しています。シームレスな統合機能を備えたモジュール式でスケーラブルなソフトウェア・プラットフォームを提供することは、多様な運用環境に対応するための鍵となります。さらに、プロバイダーはサイバーセキュリティとハイブリッドクラウドソリューションの強化を重視し、信頼を築き、厳しい規制要件を満たすことで、安全で信頼性の高いサービス提供と持続的な競争優位性を確保しています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 航空交通量の増加と航空機の拡張

- 航空業界におけるIoTと高度な分析の導入拡大

- リアルタイムの航空機健康監視を求める規制当局の圧力

- 次世代航空機の需要増加

- インフラ開発と建設セクターの成長

- 業界の潜在的リスク&課題

- 初期導入および統合コストが高め

- データセキュリティとプライバシーに関する懸念

- 市場機会

- クラウドベースの予知保全プラットフォームの需要増加

- 航空会社とMROによるデジタル変革への投資増加

- 新興市場が商用車の増加を牽引

- 軍事および防衛航空における予知保全の応用

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 新たなビジネスモデル

- コンプライアンス要件

- 国防予算分析

- 世界の防衛費の動向

- 地域防衛予算配分

- 北米

- 欧州

- アジア太平洋地域

- 中東・アフリカ

- ラテンアメリカ

- 主要な防衛近代化プログラム

- 予算予測(2025-2034)

- 業界の成長への影響

- 国別防衛予算

- サプライチェーンのレジリエンス

- 地政学的分析

- 人材分析

- デジタル変革

- 合併、買収、戦略的提携の情勢

- リスク評価と管理

- 主要契約の締結(2021-2024)

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 地域別

- 主要プレーヤーの競合ベンチマーキング

- 財務実績の比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオの比較

- 製品ラインナップの広さ

- テクノロジー

- 革新

- 地理的プレゼンスの比較

- 世界フットプリント分析

- サービスネットワークの範囲

- 地域別の市場浸透率

- 競合ポジショニングマトリックス

- リーダーたち

- 課題者たち

- フォロワー

- ニッチプレイヤー

- 戦略的展望マトリックス

- 財務実績の比較

- 主な発展, 2021-2024

- 合併と買収

- パートナーシップとコラボレーション

- 技術的進歩

- 拡大と投資戦略

- 持続可能性への取り組み

- デジタル変革の取り組み

- 新興企業/スタートアップ企業の競合情勢

第5章 市場推計・予測:コンポーネント別、2021-2034

- 主要動向

- ハードウェア

- エッジデバイス

- データ収集ユニット(DAU)

- フライトデータレコーダー/ヘルスモニタリングユニット

- 通信モジュール

- その他

- ソフトウェア

- 予測分析ソフトウェア

- 状態基準監視プラットフォーム

- 機械学習とAIエンジン

- その他

- サービス

- システム統合サービス

- データ処理およびモデルトレーニングサービス

- メンテナンスと技術サポート

- その他

第6章 市場推計・予測:機種別、2021-2034

- 主要動向

- 民間航空機

- 軍用機

- プライベート航空機

- その他

第7章 市場推計・予測:メンテナンス種別、2021-2034

- 主要動向

- 機体整備

- エンジンのメンテナンス

- コンポーネントのメンテナンス

- 地上設備のメンテナンス

第8章 市場推計・予測:展開モード別、2021-2034

- 主要動向

- オンプレミス

- クラウド

- ハイブリッド

第9章 市場推計・予測:技術別、2021-2034

- 主要動向

- 状態基準保全(CBM)

- 予測メンテナンスツール

- 機械学習アルゴリズム

- モノのインターネット(IoT)

- ビッグデータ分析

第10章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 民間航空会社

- 軍事および防衛組織

- 航空機OEM

- その他

第11章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第12章 企業プロファイル

- Global Key Players

- Regional Key Players

- ニッチプレーヤー/ディスラプター

- エアロソフトシステムズ

- 航空インターテック

- CAMPシステム

- スイス航空ソフトウェア

目次

The Global Predictive Airplane Maintenance Market was valued at USD 5.3 billion in 2024 and is estimated to grow at a CAGR of 13.1% to reach USD 18.2 billion by 2034. This growth is driven primarily by the rising volume of air traffic and continuous fleet expansion worldwide. The aviation sector is increasingly adopting advanced Internet of Things (IoT) solutions and sophisticated analytics to enhance maintenance operations. Predictive maintenance is becoming critical for ensuring aircraft safety, boosting reliability, and maximizing operational efficiency amid growing demand for air travel. Airlines and maintenance, repair, and overhaul (MRO) providers are leveraging artificial intelligence and machine learning to enhance fault detection and predict failures, enabling proactive maintenance schedules and minimizing unexpected downtime. This evolution improves fleet uptime and optimizes resource deployment globally. However, as these platforms depend on interconnected data systems, cybersecurity measures have become vital to protect sensitive information from emerging threats.

In 2024, the software segment commanded the largest market share of 41.6%. Predictive airplane maintenance software is integral for real-time data processing, fault identification, and failure forecasting. The market is witnessing increased investment in AI-driven, automated solutions tailored for scalability and customization, allowing seamless integration with existing airline operations and adaptability to shifting demands.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.3 Billion |

| Forecast Value | $18.2 Billion |

| CAGR | 13.1% |

Meanwhile, the cloud segment is projected to reach USD 9.2 billion by 2034. Cloud platforms facilitate remote access, flexibility, and real-time data streaming, enhancing collaboration and decision-making. Adoption is rising due to lower upfront costs and streamlined system upgrades, though concerns around data security and latency persist. Providers are responding by offering robust cybersecurity and hybrid cloud architectures.

North America Predictive Airplane Maintenance Market held a 36.5% share in 2024 and is expected to grow at a CAGR of 12.1% through 2034. The region benefits from extensive aviation infrastructure, proactive adoption of predictive technologies, and strong regulatory frameworks that support digital innovation in aviation maintenance. Major players driving this market include IBM, Lufthansa Technik, The Boeing Company, Airbus SE, and General Electric Company.

To strengthen their market position, companies in the Predictive Airplane Maintenance Market focus on several strategic approaches. These include investing heavily in research and development to enhance AI and machine learning capabilities, enabling more accurate and automated diagnostics. They also pursue strategic partnerships and collaborations with airlines and MRO providers to deepen market penetration and tailor solutions to client needs. Offering modular, scalable software platforms with seamless integration capabilities is key to addressing diverse operational environments. Additionally, providers emphasize enhancing cybersecurity and hybrid cloud solutions to build trust and meet stringent regulatory requirements, thereby ensuring secure, reliable service delivery and sustained competitive advantage.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Component trends

- 2.2.2 Aircraft type trends

- 2.2.3 Maintenance type trends

- 2.2.4 Deployment mode trends

- 2.2.5 Technology trends

- 2.2.6 End user trends

- 2.2.7 Regional trends

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising air traffic and fleet expansion

- 3.2.1.2 Growing adoption of IoT and advanced analytics in aviation

- 3.2.1.3 Regulatory push for real-time aircraft health monitoring

- 3.2.1.4 Increasing demand for next-generation aircraft

- 3.2.1.5 Infrastructure development and construction sector growth

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial implementation and integration costs

- 3.2.2.2 Data security and privacy concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for cloud-based predictive maintenance platforms

- 3.2.3.2 Rising investments in digital transformation by airlines and mros

- 3.2.3.3 Emerging markets driving commercial fleet growth

- 3.2.3.4 Application of predictive maintenance in military and defense aviation

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging business models

- 3.9 Compliance requirements

- 3.10 Defense budget analysis

- 3.11 Global defense spending trends

- 3.12 Regional defense budget allocation

- 3.12.1 North America

- 3.12.2 Europe

- 3.12.3 Asia Pacific

- 3.12.4 Middle East and Africa

- 3.12.5 Latin America

- 3.13 Key defense modernization programs

- 3.14 Budget forecast (2025-2034)

- 3.14.1 Impact on industry growth

- 3.14.2 Defense budgets by country

- 3.15 Supply chain resilience

- 3.16 Geopolitical analysis

- 3.17 Workforce analysis

- 3.18 Digital transformation

- 3.19 Mergers, acquisitions, and strategic partnerships landscape

- 3.20 Risk assessment and management

- 3.21 Major contract awards (2021-2024)

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Component, 2021 - 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Edge devices

- 5.2.2 Data acquisition units (DAU)

- 5.2.3 Flight data recorders / health monitoring units

- 5.2.4 Communication modules

- 5.2.5 Others

- 5.3 Software

- 5.3.1 Predictive analytics software

- 5.3.2 Condition-based monitoring platforms

- 5.3.3 Machine learning & AI engines

- 5.3.4 Others

- 5.4 Services

- 5.4.1 System integration services

- 5.4.2 Data processing & model training services

- 5.4.3 Maintenance & technical support

- 5.4.4 Others

Chapter 6 Market Estimates and Forecast, By Aircraft Type, 2021 - 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Commercial aircraft

- 6.3 Military aircraft

- 6.4 Private aircraft

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Maintenance Type, 2021 - 2034 (USD Billion)

- 7.1 Key trends

- 7.2 Airframe maintenance

- 7.3 Engine maintenance

- 7.4 Components maintenance

- 7.5 Ground equipment maintenance

Chapter 8 Market Estimates and Forecast, By Deployment Mode, 2021 - 2034 (USD Billion)

- 8.1 Key trends

- 8.2 On premise

- 8.3 Cloud

- 8.4 Hybrid

Chapter 9 Market Estimates and Forecast, By Technology, 2021 - 2034 (USD Billion)

- 9.1 Key trends

- 9.2 Condition-based maintenance (CBM)

- 9.3 Predictive maintenance tools

- 9.4 Machine learning algorithms

- 9.5 Internet of things (IoT)

- 9.6 Big data analytics

Chapter 10 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Billion)

- 10.1 Key trends

- 10.2 Commercial airlines

- 10.3 Military & defense organization

- 10.4 Aircraft OEMs

- 10.5 Others

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Billion)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Key Players

- 12.1.1 IMB

- 12.1.2 Lufthansa Technik

- 12.1.3 Boeing

- 12.1.4 Airbus

- 12.1.5 General Electric

- 12.2 Regional Key Players

- 12.2.1 North America

- 12.2.1.1 Delta TechOps

- 12.2.1.2 Honeywell

- 12.2.1.3 Microsoft

- 12.2.1.4 Pratt & Whitney

- 12.2.2 Europe

- 12.2.2.1 Air France KLM

- 12.2.2.2 Rolls-Royce

- 12.2.2.3 Safran

- 12.2.2.4 SAP

- 12.2.2.5 Thales

- 12.2.3 APAC

- 12.2.3.1 ST Engineering

- 12.2.3.2 GMF AeroAsia

- 12.2.1 North America

- 12.3 Niche Players / Disruptors

- 12.3.1 AeroSoft Systems

- 12.3.2 Aviation Intertec

- 12.3.3 CAMP Systems

- 12.3.4 Swiss Aviation Software

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日