|

市場調査レポート

商品コード

1797773

通気レインスクリーンファサード市場:市場機会、成長促進要因、産業動向分析、将来予測(2025~2034年)Ventilated Rainscreen Facade Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 通気レインスクリーンファサード市場:市場機会、成長促進要因、産業動向分析、将来予測(2025~2034年) |

|

出版日: 2025年07月31日

発行: Global Market Insights Inc.

ページ情報: 英文 140 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

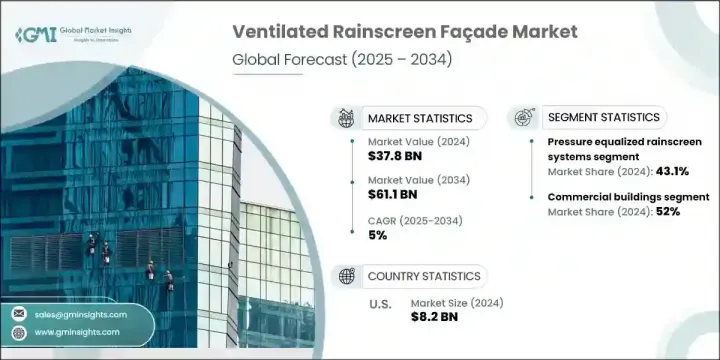

世界の通気レインスクリーンファサード市場は、2024年に378億米ドルと評価され、CAGR 5%で成長し、2034年には611億米ドルに達すると推定されています。

エネルギー効率の高い建設と近代的な建築デザインに対する需要の高まりが、ファサードソリューションの展望を再構築しています。都市化と商業インフラの急成長が、持続可能な建築システムへのニーズに拍車をかけています。換気ファサード設備は、熱調整、湿気管理、建物の耐久性向上などの機能により人気を集めています。教育、ホスピタリティ、商業不動産などの業界では、グリーンビルディング基準や環境規制に合わせて、こうしたシステムを取り入れるケースが増えています。特に建物外壁の効率が優先される場合、性能と組み合わされた美的多様性が消費者の関心を引き続けます。

進化するデザインと性能の要求に応えるため、メーカーはアルミ複合材、ファイバーセメント、高圧ラミネートなどの次世代素材に投資し、構造的完全性と視覚的柔軟性を確保しています。また、これらのファサードはパッシブ冷却戦略にも対応し、HVACへの依存度を下げることで、さまざまな気候帯における運用エネルギーの削減に貢献しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測期間 | 2025~2034年 |

| 当初の市場規模 | 378億米ドル |

| 市場規模予測 | 611億米ドル |

| CAGR | 5% |

2024年には、均圧式レインスクリーンシステムが世界市場をリードし、総売上高の43.1%を占め、2034年までCAGR 5.4%で成長すると予測されます。これらのシステムは、特に高層ビルや風にさらされる環境において、その高度な湿気・空気管理能力が好まれています。内部空洞の設計により空気圧を均一化できるため、水の浸入を効果的に抑えることができます。インフラの性能要件が高まる中、このようなソリューションは現代の設計哲学に不可欠なものとなりつつあります。断熱層を保護し、熱安定性を維持する能力は、長期的なエネルギー節約に貢献します。

2024年の市場シェアは、商業建築物が52%を占めて最大であり、2025~2034年のCAGRは5.4%で成長すると予測されています。高効率で視覚的に特徴的な商業施設の増加が需要を促進する主な要因です。オフィスタワー、ショッピングセンター、複合施設開発では、室内空調を改善し、全体的なエネルギー使用量を削減できる換気ファサードシステムが採用されています。これらのシステムは、外観の魅力を高めると同時に資産性能も向上させるため、高密度に入居している都市部のビルにとって最適な選択肢となっています。都市がビジネスの中心地へと進化するにつれ、美観と性能の両方を実現するファサードは、市場競争力にとってますます不可欠となっています。

米国の通気レインスクリーンファサード市場は2024年に76%のシェアを占め、82億米ドルを創出しました。この地域の優位性は、先進的な建築慣行、厳格な建築基準、エネルギー効率化の強力な推進によって支えられています。高性能ファサード・ソリューションは、改修イニシアチブと企業のグリーンビルディング投資によって、商業施設や施設開発で広く採用されています。この地域の弾力的なインフラニーズは、洗練された製造基盤と相まって、均圧ファサードシステムの広範な統合を支えています。気候への配慮とメンテナンスの最適化が、市場の勢いをさらに加速させています。

通気レインスクリーンファサード市場を形成する主要企業には、Trespa International、Benson Industries、Zahner、Simpson Strong-Tie、Cladding Corp、Enclos Corp、SFS Group(NV 1 Systems)、Kingspan Group、Powers Fasteners、ITW Construction Products、Central International、Permasteelisa North America、Walters &Wolf、James Hardie Industries、Hilti Corporationなどがあります。通気レインスクリーンファサードの主要企業はそのプレゼンスを拡大するため、いくつかのコア戦略を活用しています。これらには、耐候性、断熱性能、設計適応性を向上させるための材料革新への重点的な投資が含まれます。建築家や建設業者とのコラボレーションは、様々な用途向けにカスタマイズされたソリューションを提供するために重視されています。各社はまた、機関投資家の顧客を引き付けるため、持続可能性認証やグリーン・コンプライアンスにも力を入れています。ファサードシステムの設計と施工プロセスのデジタル化とともに、新興建設市場への地理的拡大が、企業のサービス提供と顧客体験の向上に役立っています。さらに、改修ソリューションとエネルギー効率に優れたアップグレードは、新築と改修の両分野に対応するために優先されています。

目次

第1章 分析手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- エネルギー効率の高い建築ソリューションの需要

- 現代建築美学へのこだわり

- グリーンビルディングを支援する規制

- 業界の潜在的リスクと課題

- 設置コストと材料費の高さ

- 発展途上地域での関心の低さ

- 機会

- 老朽化した建物の改修需要

- 新興国の拡大

- 促進要因

- 成長可能性分析

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- システムの種類別

- 規制の枠組み

- 標準とコンプライアンス要件

- 地域規制枠組み

- 認証基準

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 企業合併・買収 (M&A)

- 事業提携・協力

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:システムの種類別(2021~2034年)

- 主要動向

- 均圧式レインスクリーンシステム

- 排水・逆換気システム

- 換気孔システム

- クロスシステム分析

第6章 市場推計・予測:材料の種類別(2021~2034年)

- 主要動向

- 金属複合材料

- ファイバーセメントパネル

- 天然石パネル

- セラミック・テラコッタパネル

- 高圧ラミネートパネル

第7章 市場推計・予測:用途別(2021~2034年)

- 主要動向

- 商業建築物

- 住宅

- 産業建築物

- 公共施設

第8章 市場推計・予測:地域別(2021~2034年)

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第9章 企業プロファイル

- Benson Industries

- Centria International

- Cladding Corp

- Enclos Corp

- Hilti Corporation

- ITW Construction products

- James Hardie Industries

- Kingspan Group

- Permasteelisa North America

- Power Fasteners

- SFS Group(NV1 Systems)

- Simpson Strong-Tie

- Trespa International

- Walters & Wolf

- Zahner

The Global Ventilated Rainscreen Facade Market was valued at USD 37.8 billion in 2024 and is estimated to grow at a CAGR of 5% to reach USD 61.1 billion by 2034. The growing demand for energy-efficient construction and modern architectural design is reshaping the facade solutions landscape. Urbanization and the rapid growth of commercial infrastructure are fueling the need for sustainable building systems. Ventilated facade installations are gaining popularity due to their ability to offer thermal regulation, moisture management, and extended building durability. Industries such as education, hospitality, and commercial real estate are increasingly incorporating these systems to align with green building standards and environmental regulations. Aesthetic versatility combined with performance continues to drive consumer interest, especially where building envelope efficiency is prioritized.

To meet evolving design and performance demands, manufacturers are investing in next-generation materials, including aluminum composites, fiber cement, and high-pressure laminates, to ensure structural integrity and visual flexibility. These facades also support passive cooling strategies, helping reduce operational energy use in varied climate zones by lowering HVAC dependency.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $37.8 Billion |

| Forecast Value | $61.1 Billion |

| CAGR | 5% |

In 2024, pressure-equalized rainscreen systems led the global market, representing 43.1% of total revenue, and are expected to grow at a 5.4% CAGR through 2034. These systems are preferred for their advanced moisture and air management capabilities, especially in high-rise and wind-exposed environments. Their internal cavity design allows for equalized air pressure, effectively minimizing water ingress. With the rise in infrastructure performance requirements, such solutions are becoming integral to modern design philosophies. Their capacity to protect insulation layers and maintain thermal stability contributes to long-term energy savings.

The commercial structures held the largest share of the market in 2024, accounting for 52% share, and are anticipated to grow at a CAGR of 5.4% during 2025-2034. The rise of high-efficiency and visually distinctive commercial properties is a major factor driving demand. Office towers, shopping centers, and mixed-use developments are opting for ventilated facade systems for their ability to improve indoor climate control and reduce overall energy usage. These systems enhance exterior appeal while boosting asset performance, making them a go-to option for densely occupied urban buildings. As cities evolve into business hubs, facades that deliver on both aesthetics and performance are increasingly vital to market competitiveness.

U.S. Ventilated Rainscreen FaASade Market held 76% share in 2024, generating USD 8.2 billion. This regional dominance is supported by advanced construction practices, stringent building codes, and a strong push for energy efficiency. High-performing facade solutions are widely adopted across commercial and institutional developments, driven by retrofitting initiatives and corporate green building investments. The region's resilient infrastructure needs, paired with a sophisticated manufacturing base, support the widespread integration of pressure-equalized facade systems. Climate considerations and maintenance optimization further contribute to market momentum.

Key companies shaping the Ventilated Rainscreen FaASade Market include Trespa International, Benson Industries, Zahner, Simpson Strong-Tie, Cladding Corp, Enclos Corp, SFS Group (NV 1 Systems), Kingspan Group, Powers Fasteners, ITW Construction Products, Central International, Permasteelisa North America, Walters & Wolf, James Hardie Industries, and Hilti Corporation. To expand their presence, leading Ventilated Rainscreen FaASade Market companies are leveraging several core strategies. These include heavy investment in material innovation for improved weather resistance, thermal performance, and design adaptability. Collaboration with architects and contractors is being emphasized to deliver customized solutions for varied applications. Companies are also focusing on sustainability certifications and green compliance to attract institutional clients. Geographic expansion into emerging construction markets, along with digitalization in facade system design and installation processes, is helping firms enhance service delivery and customer experience. Additionally, retrofitting solutions and energy-efficient upgrades are being prioritized to serve both new construction and renovation sectors.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 By system type

- 2.2.2 By material type

- 2.2.3 By application

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Demand for energy-efficient building solutions

- 3.2.1.2 Preference for modern architectural aesthetics

- 3.2.1.3 Supportive green building regulations

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High installation and material costs

- 3.2.2.2 Low awareness in developing regions

- 3.2.3 Opportunities

- 3.2.3.1 Retrofit demand in aging buildings

- 3.2.3.2 Expansion in emerging economies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By system type

- 3.7 Regulatory framework

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger & acquisitions

- 4.6.2 Partnership & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By System Type, 2021 - 2034 ($Bn) (Thousand Units)

- 5.1 Key trends

- 5.2 Pressure equalized rainscreen systems

- 5.3 Drained and back-ventilated systems

- 5.4 Ventilated cavity systems

- 5.5 Cross-system analysis

Chapter 6 Market Estimates & Forecast, By Material Type, 2021 - 2034 ($Bn) (Thousand Units)

- 6.1 Key trends

- 6.2 Metal composite materials

- 6.3 Fiber cement panels

- 6.4 Natural stone panels

- 6.5 Ceramic and terracotta panels

- 6.6 High-pressure laminate panels

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn) (Thousand Units)

- 7.1 Key trends

- 7.2 Commercial buildings

- 7.3 Residential buildings

- 7.4 Industrial buildings

- 7.5 Institutional buildings

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn) (Thousand Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 South Africa

- 8.6.3 Saudi Arabia

Chapter 9 Company Profiles

- 9.1 Benson Industries

- 9.2 Centria International

- 9.3 Cladding Corp

- 9.4 Enclos Corp

- 9.5 Hilti Corporation

- 9.6 ITW Construction products

- 9.7 James Hardie Industries

- 9.8 Kingspan Group

- 9.9 Permasteelisa North America

- 9.10 Power Fasteners

- 9.11 SFS Group (NV1 Systems)

- 9.12 Simpson Strong-Tie

- 9.13 Trespa International

- 9.14 Walters & Wolf

- 9.15 Zahner