低侵襲脊椎手術装置の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Minimally Invasive Spine Surgery Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1797733

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

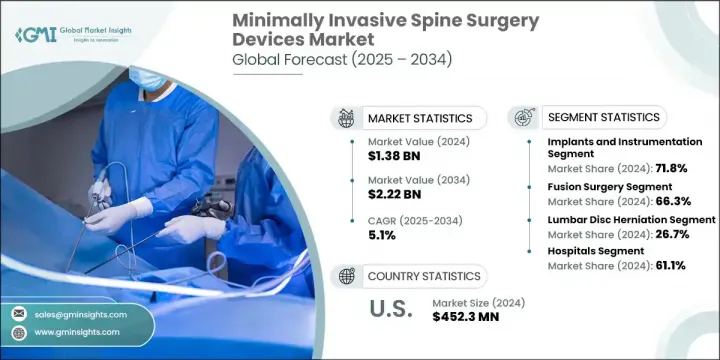

低侵襲脊椎手術装置の世界市場は、2024年には13億8,000万米ドルとなり、CAGR 5.1%で成長し、2034年には22億2,000万米ドルに達すると予測されています。

低侵襲脊椎手術装置への嗜好が高まっている背景には、切開創が小さく、入院期間が短く、回復が早いという利点があります。これらの手術は痛みが少なく、傷跡が残りにくいため、ますます患者から支持されるようになっています。医療画像とナビゲーション技術の進歩は手術の精度を高め、より安全な手術と幅広い普及に貢献しています。

低侵襲脊椎手術の需要が高まるにつれ、高齢化社会と脊椎疾患の増加に支えられ、市場は成長を続けています。世界の高齢化により、椎間板変性症、脊柱管狭窄症、椎間板ヘルニアといった疾患の罹患率が高くなっており、外科的介入を必要とすることが多いです。加えて、座りがちな生活習慣や身体的負担の増加などの生活習慣要因も、あらゆる年齢層における脊椎疾患の蔓延に寄与しています。外傷の減少、出血量の減少、リハビリの迅速化など、低侵襲手技の利点を患者やヘルスケアプロバイダーが認識する中、これらの手技に対する嗜好は着実に高まっています。さらに、手術技術の進歩や、新興地域における質の高いヘルスケア施設へのアクセスの拡大が、患者層を広げています。こうした手術に対する認識が向上し、保険適用が拡大するにつれて、人口動態の変化と医療技術革新の両方が原動力となって、市場はさらに加速すると予想されます。この動向は、より安全で効率的な脊椎手術を促進する機器に対する需要の持続を裏付けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 13億8,000万米ドル |

| 予測金額 | 22億2,000万米ドル |

| CAGR | 5.1% |

2024年には、インプラント・器具分野が71.8%のシェアを占め、外科手術の精度と患者の回復を向上させるために設計された高度な脊椎固定システムとインプラントの使用が増加していることが牽引しています。外科医がこれらの器具を好むのは、安定性を高め、術中合併症を減らし、迅速な治癒をサポートする能力があるからです。ナビゲーション支援器具、胴体間ケージ、ロボット支援技術の統合が進んでいることも、この分野の採用を後押ししています。

脊椎の安定化を必要とする変性椎間板疾患、脊柱管狭窄症、脊椎すべり症などの有病率の上昇に後押しされ、2024年の固定術セグメントのシェアは66.3%でした。低侵襲の固定術は、組織の損傷を最小限に抑え、回復を早めるため、患者や外科医の間で人気を集めています。より優れた骨移植材や強化されたインターボディケージなど、癒合器具の技術革新により、手術の成功率は大幅に向上し、外来や病院での使用範囲も広がっています。

北米の低侵襲脊椎手術装置2024年の市場シェアは35.3%であったが、これは最先端の手術法や器具の迅速な導入を促す強固なヘルスケアインフラがあるためです。低侵襲手術の利点に関する患者や医師の意識の高さが需要を促進しています。さらに、この地域には主要な医療機器メーカーが集中しているため、継続的な技術革新が促進され、幅広い製品の入手が可能になっています。

低侵襲脊椎手術装置市場で事業を展開している注目すべき企業には、Heraeus、Orthofix Medical、Globus Medical、SI-BONE、Invibio、Wenzel Spine、Xenco Medical、Matexcel、Premia Spine、B. Braun、Medtronic、DePuy Synthes(Johnson &Johnson)、Spinal Elements、Nexus Spine、Stryker、Zimmer Biomet、NuVasive、Evonikなどがあります。低侵襲脊椎手術装置市場の各社は、継続的な技術革新に注力し、先進的なインプラント、ナビゲーションツール、ロボット支援ソリューションなどの製品ポートフォリオを拡充することで、足場を固めています。病院や研究機関との戦略的提携は、機器の有効性や外科医のトレーニングの向上に役立っています。多くの企業が研究開発に多額の投資を行い、手術成績を向上させ合併症を減少させる患者中心のソリューションを開発しています。地理的拡大、特に新興市場への進出も、拡大する需要を取り込むための優先事項です。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 脊椎疾患の有病率の上昇

- 高齢化人口の増加

- 外来脊椎手術の採用増加

- ナビゲーションとロボット工学における技術の進歩

- 業界の潜在的リスク&課題

- 高度なMISS機器の高コスト

- 発展途上地域における熟練外科医の不足

- 市場機会

- AIと拡張現実との統合

- 費用対効果の高いMISSソリューションの開発

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- サプライチェーン分析

- 消費者行動の傾向

- 市場参入戦略分析

- ポーター分析

- PESTEL分析

- 将来の市場動向

- ギャップ分析

- 価格分析、2024

- 特許情勢

- 償還シナリオ

- 償還政策が市場成長に与える影響

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 世界

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021-2034

- 主要動向

- インプラントと器具

- 椎弓根スクリューとロッド

- 椎体間ケージ

- 固定システム

- その他のインプラントおよび器具

- 生体材料

- 骨移植代替品

- 合成骨移植

- その他の生体材料

第6章 市場推計・予測:用途別、2021-2034

- 主要動向

- 融合手術

- 非固定手術

第7章 市場推計・予測:適応症別、2021-2034

- 主要動向

- 腰椎椎間板ヘルニア

- 脊柱管狭窄症

- 変性脊椎疾患

- 頸椎椎間板疾患

- 胸椎椎間板ヘルニア

- その他の適応症

第8章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 病院

- 外来手術センター

- その他の用途

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- B. Braun

- DePuy Synthes(Johnson &Johnson)

- Evonik

- Globus Medical

- Heraeus

- Invibio

- Matexcel

- Medtronic

- Nexus Spine

- NuVasive

- Orthofix Medical

- Premia Spine

- SI-BONE

- Spinal Elements

- Stryker

- Wenzel Spine

- Xenco Medical

- Zimmer Biomet

目次

The Global Minimally Invasive Spine Surgery Devices Market was valued at USD 1.38 billion in 2024 and is estimated to grow at a CAGR of 5.1% to reach USD 2.22 billion by 2034. The growing preference for minimally invasive spine surgery devices is fueled by the advantages of smaller incisions, shorter hospital stays, and quicker recovery periods. These procedures are less painful and reduce scarring, making them increasingly favored by patients. Advances in medical imaging and navigation technology have enhanced surgical accuracy, contributing to safer procedures and wider adoption.

As demand for minimally invasive spinal surgeries increases, the market continues to grow, supported by an aging population and rising spinal disorders. Aging populations worldwide are experiencing higher incidences of conditions like degenerative disc disease, spinal stenosis, and herniated discs, which often require surgical intervention. Additionally, lifestyle factors such as sedentary habits and increased physical strain contribute to the prevalence of spinal issues across all age groups. With patients and healthcare providers recognizing the benefits of minimally invasive techniques-such as reduced trauma, less blood loss, and quicker rehabilitation-the preference for these procedures is steadily climbing. Furthermore, advancements in surgical technology and growing access to high-quality healthcare facilities in emerging regions are broadening the patient base. As awareness improves and insurance coverage expands for these procedures, the market is expected to accelerate further, driven by both demographic shifts and medical innovations. This trend underscores a sustained demand for devices that facilitate safer, more efficient spinal surgeries.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.38 Billion |

| Forecast Value | $2.22 Billion |

| CAGR | 5.1% |

In 2024, implants and instrumentation segment accounted for 71.8% share, driven by the increasing use of advanced spinal fixation systems and implants designed to improve surgical precision and patient recovery. Surgeons prefer these devices due to their ability to enhance stability, reduce intraoperative complications, and support quicker healing. The growing integration of navigation-assisted instruments, interbody cages, and robotic-assisted technologies is also boosting the adoption of this segment.

The fusion surgery segment held 66.3% share in 2024, propelled by the rising prevalence of degenerative disc diseases, spinal stenosis, and spondylolisthesis, which require spinal stabilization. Minimally invasive fusion techniques are gaining popularity among patients and surgeons alike because they minimize tissue damage and accelerate recovery. Innovations in fusion devices, including better bone graft materials and enhanced interbody cages, have significantly improved surgical success rates and broadened their use across outpatient and hospital environments.

North America Minimally Invasive Spine Surgery Devices Market held 35.3% share in 2024, owing to its robust healthcare infrastructure that encourages swift adoption of cutting-edge surgical methods and devices. High patient and physician awareness regarding the benefits of minimally invasive procedures fuels demand. Furthermore, the region's concentration of key medical device manufacturers fosters ongoing innovation and ensures wide product availability.

Notable companies operating in the Minimally Invasive Spine Surgery Devices Market include Heraeus, Orthofix Medical, Globus Medical, SI-BONE, Invibio, Wenzel Spine, Xenco Medical, Matexcel, Premia Spine, B. Braun, Medtronic, DePuy Synthes (Johnson & Johnson), Spinal Elements, Nexus Spine, Stryker, Zimmer Biomet, NuVasive, and Evonik. Companies in the Minimally Invasive Spine Surgery Devices Market strengthen their foothold by focusing on continuous innovation and expanding their product portfolios with advanced implants, navigation tools, and robotic-assisted solutions. Strategic collaborations with hospitals and research institutions help improve device efficacy and surgeon training. Many firms invest heavily in R&D to develop patient-centric solutions that enhance surgical outcomes and reduce complications. Expanding geographic reach, particularly into emerging markets, is also a priority to tap into growing demand.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Application trends

- 2.2.4 Indication trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of spine disorders

- 3.2.1.2 Growing geriatric population

- 3.2.1.3 Increased adoption of outpatient spine surgeries

- 3.2.1.4 Technological advancements in navigation and robotics

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced MISS equipment

- 3.2.2.2 Lack of skilled surgeons in developing regions

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with AI and augmented reality

- 3.2.3.2 Development of cost-effective MISS solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Supply chain analysis

- 3.7 Consumer behaviour trend

- 3.8 Go-to-market strategy analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Future market trends

- 3.12 Gap analysis

- 3.13 Pricing analysis, 2024

- 3.14 Patent Landscape

- 3.15 Reimbursement scenario

- 3.15.1 Impact of reimbursement policies on market growth

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.2.5 Latin America

- 4.2.6 Middle East and Africa

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Implants and instrumentation

- 5.2.1 Pedicle screws and rods

- 5.2.2 Interbody cages

- 5.2.3 Fixation systems

- 5.2.4 Other implants and instrumentations

- 5.3 Biomaterials

- 5.3.1 Bone graft substitutes

- 5.3.2 Synthetic bone grafts

- 5.3.3 Other biomaterials

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Fusion surgery

- 6.3 Non-fusion surgery

Chapter 7 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Lumbar disc herniation

- 7.3 Spinal stenosis

- 7.4 Degenerative spinal disease

- 7.5 Cervical disc disorders

- 7.6 Thoracic disc herniation

- 7.7 Other indications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Ambulatory surgical centers

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 B. Braun

- 10.2 DePuy Synthes (Johnson & Johnson)

- 10.3 Evonik

- 10.4 Globus Medical

- 10.5 Heraeus

- 10.6 Invibio

- 10.7 Matexcel

- 10.8 Medtronic

- 10.9 Nexus Spine

- 10.10 NuVasive

- 10.11 Orthofix Medical

- 10.12 Premia Spine

- 10.13 SI-BONE

- 10.14 Spinal Elements

- 10.15 Stryker

- 10.16 Wenzel Spine

- 10.17 Xenco Medical

- 10.18 Zimmer Biomet

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日