GaNパワー充電器市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

GaN-powered Chargers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 185 Pages

- 納期

- 2~3営業日

- 商品コード

- 1797729

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

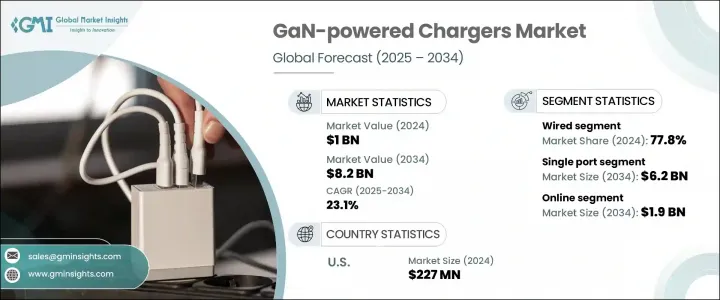

GaNパワー充電器の世界市場規模は、2024年に10億米ドルとなり、CAGR 23.1%で成長し、2034年には82億米ドルに達すると予測されています。

この急成長は、電気自動車や自動産業システムなどの分野からの需要の高まりとともに、家庭や産業界全体でスマートデバイスの統合が進んでいることが背景にあります。世界のデジタル接続の深化に伴い、より多くの消費者や企業が電力を消費する電子機器に依存するようになり、その結果、コンパクトでエネルギー効率に優れた高速充電オプションのニーズが加速しています。

GaNベースの充電器は、そのコンパクトな設計、より高速な電力供給、改善された熱効率で人気を集めています。これらの特徴は、より小型で、より高速に充電し、より少ない電力を浪費するデバイスに対する現在の技術的要求に合致しています。電化への取り組みが世界的に拡大するにつれ、特に輸送や製造の分野では、GaNを電源とするシステムへのシフトがより明白になってきています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 10億米ドル |

| 予測金額 | 82億米ドル |

| CAGR | 23.1% |

効率的なエネルギー変換を実現しながらコンパクトなアーキテクチャを提供できることから、進化するEVインフラやスマート産業環境において、充電器が好ましい選択肢となっています。産業や輸送システムの電動化が進むにつれて、エネルギー損失を最小限に抑え、スペースを取らない高性能充電ソリューションへの需要が急増しています。GaNパワー充電器は、充電サイクルの高速化を可能にし、熱蓄積を低減し、スペースの最適化と省エネルギーを優先する次世代設計にシームレスに統合するため、このシフトに理想的に適しています。

2024年の有線セグメントのシェアは77.8%です。このセグメントは、効率性、様々な急速充電プロトコルとの互換性、高い信頼性、特に仕事中心でハイブリッドな環境で支持されています。ユーザーは、特に業務用や旅行用シナリオにおいて、その速度と一貫性から有線充電に依存し続けています。有線ソリューションの優位性は、USB-C PDのようなユニバーサル充電プロトコルが広く受け入れられていることにも裏付けられています。メーカー各社は、有線GaN充電器の設計革新、特に高性能とコスト意識の高い購入者の両方の要求を満たすためのマルチプロトコルサポートの統合を優先することが推奨されます。

シングルポートGaN充電器セグメントは、シンプルさと携帯性を求める個人からの強い訴求力に支えられ、2034年までに62億米ドルに達すると予想されます。これらの充電器は、学生、通勤者、外出先での迅速な充電を必要とするミニマリストユーザーに特に人気があります。コンパクトなサイズと主要な電子機器との互換性により、日常的なニーズにとって実用的な選択肢となっています。さらに、USB-Cパワーデリバリー規格の普及が拡大しており、サイズを最適化しながら電力伝送を簡素化することで、市場の成長を支え続けています。メーカーは、省スペースで効率的な充電オプションを求めるユーザーをターゲットに、30W~65Wの出力範囲でポケットサイズのGaNモデルを積極的に発売しています。

北米のGaNパワー充電器市場は24.9%のシェアを占め、2025年から2034年にかけてCAGR 24%で成長すると予測されています。この増加傾向は主に、高性能充電器に対する消費者の期待の高まりと、エネルギーを意識した電子ソリューションの採用増加によるものです。この地域では、コンパクトで熱効率が高く、高速の充電デバイスが受け入れられており、GaN技術を後押ししています。消費者の嗜好は、かさばる低速充電製品から、持続可能な慣行と性能ニーズに沿った、よりスマートで高度なソリューションへとシフトしています。

GaNパワー充電器市場を形成している主な業界企業には、Baseus Technology、RAVPower、Anker Innovations、Belkin International、Aukey Internationalなどがあります。これらの企業は、競合情勢の中での地位を固めるため、研究、革新、製品の多様化に積極的に投資しています。市場での存在感を高めるため、主要企業はさまざまな戦略的取り組みに注力しています。主な戦略には、継続的な技術革新が含まれ、特に、消費者セグメントと産業セグメントの両方の進化するニーズに応える、マルチプロトコル対応のコンパクトで高ワット数のGaN充電器の開発が挙げられます。戦略的パートナーシップとOEM提携は、世界な流通を拡大し、新興市場に浸透するために活用されています。さらに、サプライチェーンの効率向上と生産コスト削減のため、企業は垂直統合に投資しています。一部のブランドは、世界のエネルギー基準や持続可能な技術動向に合わせて、環境にやさしく熱効率の高い設計を優先しています。こうした積極的な戦略は、市場のリーダー企業が長期的な成長と強靭な競争優位性を確保するのに役立っています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- スマートデバイスと家電製品の普及

- 電気自動車や産業用途での採用増加

- USB-CおよびPD充電規格の採用増加

- 5GインフラとIoTエコシステムの拡大

- リモートワークとモバイルデバイスの使用の急増

- 業界の潜在的リスク&課題

- GaN部品と製造に関連する高コスト

- レガシーデバイスとの互換性の制限

- 市場機会

- 小型で高効率な充電器の需要増加

- 電気自動車とポータブルEVアクセサリーの成長

- 産業用および医療用電子機器におけるGaN nの統合

- ユニバーサルマルチポート充電ステーションの開発

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 価格戦略

- 新たなビジネスモデル

- コンプライアンス要件

- 特許および知的財産分析

- 地政学と貿易のダイナミクス

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 地域別

- 主要企業の競合ベンチマーキング

- 財務実績の比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオの比較

- 製品ラインナップの広さ

- テクノロジー

- 革新

- 地理的プレゼンスの比較

- 世界フットプリント分析

- サービスネットワークの範囲

- 地域別の市場浸透率

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 財務実績の比較

- 主な発展, 2021-2024

- 合併と買収

- パートナーシップとコラボレーション

- 技術的進歩

- 拡大と投資戦略

- 持続可能性への取り組み

- デジタル変革の取り組み

- 新興企業/スタートアップ企業の競合情勢

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 有線

- 無線

第6章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 壁掛け充電器

- デスクトップ充電器

- 旅行用アダプター

- その他

第7章 市場推計・予測:ポート数別、2021年~2034年

- 主要動向

- シングルポート

- マルチポート

第8章 市場推計・予測:出力別、2021年~2034年

- 主要動向

- 30W未満

- 31W~65W

- 66W~100W

- 101W~200W

- 200W以上

第9章 市場推計・予測:ポートタイプ別、2021年~2034年

- 主要動向

- USBタイプC

- USBタイプA

- 混合ポート

第10章 市場推計・予測:デバイス互換性別、2021年~2034年

- 主要動向

- スマートフォン

- タブレット

- ノートパソコン

- スマートウォッチとウェアラブル

- 携帯ゲーム機

- カメラとドローン

- その他

第11章 市場推計・予測:販売チャネル別、2021年~2034年

- 主要動向

- オンライン

- オフライン

第12章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 個人消費者

- 企業および法人

- 政府と防衛

- その他

第13章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第14章 企業プロファイル

- 世界の主要企業

- Anker Innovations

- Aukey International

- Baseus Technology

- Belkin International

- RAVPower

- 地域の主要企業

- 北米

- Apple

- Energizer

- Spigen

- Satechi

- 欧州

- Philips

- VOLTME

- Hama GmbH & Co KG

- アジア太平洋地域

- Samsung Electronics

- Xiaomi

- UGREEN Group

- Pisen Electronics

- Momax Technology

- Zonsan Electronics

- 北米

- ニッチ企業/ディスラプター

- DSD Tech

- iWalk Electronics

- OmniCharge

- Zendure

目次

The Global GaN-powered Chargers Market was valued at USD 1 billion in 2024 and is estimated to grow at a CAGR of 23.1% to reach USD 8.2 billion by 2034. This rapid growth is being fueled by the increasing integration of smart devices across households and industries, along with growing demand from sectors such as electric vehicles and automated industrial systems. As global digital connectivity deepens, more consumers and businesses are relying on power-hungry electronics, which in turn accelerates the need for compact, energy-efficient, and high-speed charging options.

GaN-based chargers are gaining popularity for their compact designs, faster power delivery, and improved thermal efficiency. These features align with current technological demands for devices that are smaller, charge faster, and waste less power. As electrification efforts expand globally, especially in transportation and manufacturing, the shift toward GaN-powered systems is becoming more apparent.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1 Billion |

| Forecast Value | $8.2 Billion |

| CAGR | 23.1% |

Their ability to offer compact architecture while delivering efficient energy conversion is making them a preferred choice in evolving EV infrastructure and smart industrial settings. As industries and transportation systems increasingly transition toward electrification, the demand for high-performance charging solutions that minimize energy loss and occupy less space is surging. GaN-powered chargers are ideally suited for this shift, as they enable faster charging cycles, reduce thermal buildup, and integrate seamlessly into next-generation designs that prioritize space optimization and energy savings.

The wired segment held a 77.8% share in 2024. This segment is favored for its efficiency, compatibility with various fast-charging protocols, and high reliability, particularly in work-centric and hybrid environments. Users continue to rely on wired charging for its speed and consistency, especially in professional and travel scenarios. The dominance of wired solutions is also supported by the broad acceptance of universal charging protocols like USB-C PD. Manufacturers are advised to prioritize innovations in wired GaN charger design, especially by integrating multi-protocol support to meet the demands of both high-performance and cost-conscious buyers.

The single-port GaN charger segment is expected to reach USD 6.2 billion by 2034, supported by its strong appeal among individuals seeking simplicity and portability. These chargers are especially popular with students, commuters, and minimalist users who require quick, on-the-go charging. Their compact size and compatibility with flagship electronic devices make them a practical choice for everyday needs. Moreover, the growing uptake of the USB-C Power Delivery standard continues to support market growth by simplifying power transfer while optimizing size. Manufacturers are actively launching pocket-sized GaN models in the 30W to 65W power range, targeting users looking for space-saving and efficient charging options.

North America GaN-powered Chargers Market held 24.9% share and is forecast to grow at a CAGR of 24% from 2025 to 2034. This upward trend is primarily driven by growing consumer expectations for high-performance chargers and the increasing adoption of energy-conscious electronic solutions. The region's embrace of compact, thermally efficient, and high-speed charging devices is pushing GaN technology forward. Consumer preferences are shifting away from bulky, slow-charging products to sleeker, more advanced solutions that align with sustainable practices and performance needs.

Major industry players shaping the GaN-powered charger market include Baseus Technology, RAVPower, Anker Innovations, Belkin International, and Aukey International. These companies are actively investing in research, innovation, and product diversification to solidify their positions within the competitive landscape. To strengthen their market presence, leading companies are focusing on a range of strategic initiatives. A key tactic involves continuous innovation, especially in developing compact, high-wattage GaN chargers with multi-protocol support that cater to the evolving needs of both consumer and industrial segments. Strategic partnerships and OEM collaborations are being leveraged to expand global distribution and penetrate emerging markets. Additionally, firms are investing in vertical integration to improve supply chain efficiency and reduce production costs. Some brands are prioritizing the creation of environmentally friendly and thermally efficient designs, aligning with global energy standards and sustainable technology trends. These proactive strategies are helping market leaders secure long-term growth and a resilient competitive advantage.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Type trends

- 2.2.2 Product type trends

- 2.2.3 Number of ports trends

- 2.2.4 Power output trends

- 2.2.5 Port type trends

- 2.2.6 Device compatibility trends

- 2.2.7 Sales channel trends

- 2.2.8 End use trends

- 2.2.9 Regional trends

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Proliferation of smart devices and consumer electronics

- 3.2.1.2 Increased adoption in electric vehicles and industrial applications

- 3.2.1.3 Rising adoption of USB-C and PD charging standards

- 3.2.1 Growth drivers

3.2.1.4. Expansion of 5G infrastructure and IoT ecosystems

- 3.2.1.5 Surge in remote work and mobile device usage

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High costs associated with GaN components and manufacturing

- 3.2.2.2 Compatibility limitations with legacy devices

- 3.2.3 Market opportunities

- 3.2.3.1 Rising demand for compact, high-efficiency chargers

- 3.2.3.2 Growth in electric mobility and portable EV accessories

- 3.2.3.3 Integration of GaN n in industrial and medical electronics

- 3.2.3.4 Development of universal multi-port charging stations

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Million & Thousand Units)

- 5.1 Key trends

- 5.2 Wired

- 5.3 Wireless

Chapter 6 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Million & Thousand Units)

- 6.1 Key trends

- 6.2 Wall chargers

- 6.3 Desktop chargers

- 6.4 Travel adapters

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Number of Ports, 2021 - 2034 (USD Million & Thousand Units)

- 7.1 Key trends

- 7.2 Single port

- 7.3 Multi port

Chapter 8 Market Estimates and Forecast, By Power Output, 2021 - 2034 (USD Million & Thousand Units)

- 8.1 Key trends

- 8.2 Up to 30w

- 8.3 31w to 65w

- 8.4 66w to 100w

- 8.5 101w to 200w

- 8.6 Above 200w

Chapter 9 Market Estimates and Forecast, By Port Type, 2021 - 2034 (USD Million & Thousand Units)

- 9.1 Key trends

- 9.2 USB type-C

- 9.3 USB type-A

- 9.4 Mixed port

Chapter 10 Market Estimates and Forecast, By Device Compatibility, 2021 - 2034 (USD Million & Thousand Units)

- 10.1 Key trends

- 10.2 Smartphones

- 10.3 Tablets

- 10.4 Laptops

- 10.5 Smartwatches & wearables

- 10.6 Portable game consoles

- 10.7 Cameras & drones

- 10.8 Others

Chapter 11 Market Estimates and Forecast, By Sales Channel, 2021 - 2034 (USD Million & Thousand Units)

- 11.1 Key trends

- 11.2 Online

- 11.3 Offline

Chapter 12 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Million & Thousand Units)

- 12.1 Key trends

- 12.2 Individual consumers

- 12.3 Enterprises & corporates

- 12.4 Government & defense

- 12.5 Others

Chapter 13 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million & Thousand Units)

- 13.1 Key trends

- 13.2 North America

- 13.2.1 U.S.

- 13.2.2 Canada

- 13.3 Europe

- 13.3.1 Germany

- 13.3.2 UK

- 13.3.3 France

- 13.3.4 Italy

- 13.3.5 Spain

- 13.3.6 Netherlands

- 13.4 Asia Pacific

- 13.4.1 China

- 13.4.2 India

- 13.4.3 Japan

- 13.4.4 Australia

- 13.4.5 South Korea

- 13.5 Latin America

- 13.5.1 Brazil

- 13.5.2 Mexico

- 13.5.3 Argentina

- 13.6 MEA

- 13.6.1 South Africa

- 13.6.2 Saudi Arabia

- 13.6.3 UAE

Chapter 14 Company Profiles

- 14.1 Global Key Players

- 14.1.1 Anker Innovations

- 14.1.2 Aukey International

- 14.1.3 Baseus Technology

- 14.1.4 Belkin International

- 14.1.5 RAVPower

- 14.2 Regional Key Players

- 14.2.1 North America

- 14.2.1.1 Apple

- 14.2.1.2 Energizer

- 14.2.1.3 Spigen

- 14.2.1.4 Satechi

- 14.2.2 Europe

- 14.2.2.1 Philips

- 14.2.2.2 VOLTME

- 14.2.2.3 Hama GmbH & Co KG

- 14.2.3 APAC

- 14.2.3.1 Samsung Electronics

- 14.2.3.2 Xiaomi

- 14.2.3.3 UGREEN Group

- 14.2.3.4 Pisen Electronics

- 14.2.3.5 Momax Technology

- 14.2.3.6 Zonsan Electronics

- 14.2.1 North America

- 14.3 Niche Players / Disruptors

- 14.3.1 DSD Tech

- 14.3.2 iWalk Electronics

- 14.3.3 OmniCharge

- 14.3.4 Zendure

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 185 Pages

- 納期

- 2~3営業日