デジタルマンモグラフィの市場機会、成長促進要因、産業動向分析、2025~2034年予測

Digital Mammography Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 132 Pages

- 納期

- 2~3営業日

- 商品コード

- 1797724

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

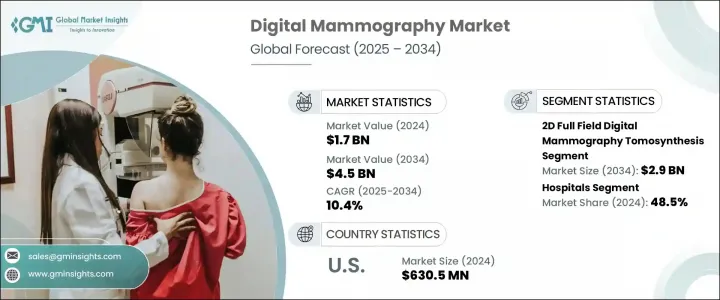

デジタルマンモグラフィの世界市場規模は、2024年に17億米ドルとなり、CAGR 10.4%で成長し、2034年には45億米ドルに達すると予測されています。

この市場は、世界の乳がん罹患率の増加、早期発見に対する意識の高まり、政府の積極的な取り組み、画像技術の進歩などを背景に急成長しています。デジタルマンモグラフィにより、ヘルスケアプロバイダーは乳腺組織の高解像度画像を撮影することができ、乳がんの早期発見と診断に役立ちます。この技術は、病院、診断センター、専門クリニックなどの臨床環境で広く使用されています。この分野の主要企業には、GEヘルスケア、ホロジック、シーメンス・ヘルティニアーズ、富士フイルムホールディングス、Koninklijke Philipsなどがあります。同市場は主に、診断精度の向上、放射線被曝の低減、患者の転帰の改善を実現するフルフィールドデジタルマンモグラフィ(FFDM)や3Dトモシンセシスシステムなどの機器に注力しています。

政府が支援する検診プログラムや画像技術の継続的な進歩に後押しされ、デジタルおよびAIを搭載したマンモグラフィシステムの採用が大幅に増加しています。ヘルスケア業界では患者中心の治療が重視されるようになっており、デジタルマンモグラフィは、より高い画像精度、診断ミスの減少、患者の快適性の向上により、好まれる選択肢になりつつあります。さらに、乳がんの有病率が上昇していることから、臨床転帰を改善するための早期かつ正確な検出の必要性が強調されています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 17億米ドル |

| 予測金額 | 45億米ドル |

| CAGR | 10.4% |

2024年、2Dフルフィールドトモシンセシス(デジタルマンモグラフィトモシンセシス)分野は11億米ドルと評価され、CAGR 10.2%で成長し、2034年には29億米ドルに達すると予測されます。この技術は乳がん診断に不可欠であり、放射線科医が微小石灰化や小さな腫瘤などの微妙な異常を検出するのに役立つ高解像度のデジタル画像を提供します。統合画像ソリューション、AI主導の診断、包括的な乳がん検診プログラムの利用の増加が、このセグメントの成長に寄与しています。画像の鮮明度の向上は早期乳がんの発見に役立ち、介入成功の可能性と患者の転帰を改善します。

病院セグメントは2024年に48.5%のシェアを占めました。病院セグメントが最大のシェアを占めているのは、その高度な画像処理インフラと、乳がんスクリーニングと診断に重要な役割を果たす熟練した放射線科医の存在によるものです。病院は乳がん治療の中心であり、これがマルチモーダル画像システムおよびAI統合デジタルマンモグラフィの需要を促進しています。さらに、新興国市場、特にアジア太平洋、中東・アフリカのような地域におけるヘルスケアインフラの開発は、2Dおよび3Dトモシンセシスシステムの両方を含む、病院内での高度なマンモグラフィ技術の採用を加速しています。

米国のデジタルマンモグラフィ2024年の市場規模は6億3,050万米ドルで、同国における乳がん罹患率の増加が成長を大きく牽引しています。早期かつ正確な乳がん発見の需要が高まるにつれ、デジタルマンモグラフィのような高度な診断ツールの必要性が高まっています。この動向は米国での市場拡大に大きく寄与しています。

デジタルマンモグラフィ市場の主要企業は、Siemens Healthineers, GE Healthcare, Koninklijke Philips, Fujifilm Holdings, and Hologic.などです。市場ポジションを強化するため、デジタルマンモグラフィ業界の企業はいくつかの主要戦略に注力しています。その一つは、診断精度とスピードを向上させるためにマンモグラフィシステムに人工知能(AI)を組み込むなど、画像技術の絶え間ない革新です。もう一つの戦略は、ヘルスケアプロバイダーや組織とパートナーシップを結び、自社の製品やサービスの普及を図ることです。また、多くの企業が、患者の関心が高まっている検診時の不快感を軽減する、より使いやすく患者中心のソリューションの開発に投資しています。さらに、各社は新興国市場、特にヘルスケアインフラが急速に発展している地域をターゲットに市場開発に取り組んでいます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 世界中で乳がんの発生率が増加

- 乳がんの早期発見に関する意識の高まり

- 政府の取り組みと検査プログラムの増加

- デジタルマンモグラフィにおける技術の進歩

- 業界の潜在的リスク&課題

- 設備とメンテナンスのコストが高め

- 放射線被曝の懸念

- 市場機会

- AIを活用した予測監視ツールとAI統合の採用増加

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- 技術的進歩

- 現在の技術動向

- 新興技術

- サプライチェーン分析

- 将来の市場動向

- 価格分析

- 製品タイプ別

- 特許分析

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021-2034

- 主要動向

- 2Dフルフィールドデジタルマンモグラフィトモシンセシス

- 3Dフルフィールドデジタルマンモグラフィトモシンセシス

第6章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 病院

- 専門クリニック

- 診断センター

第7章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第8章 企業プロファイル

- Allengers

- Canon

- Carestream

- Fujifilm Holdings

- GE Healthcare

- Genoray

- Hologic

- IDETEC Medical Imaging

- IMS Giotto

- Koninklijke Philips

- Planmed

- Siemens Healthineers

- SINO MDT

- SternMed

- Trivitron Healthcare

- Vannin Healthcare

目次

The Global Digital Mammography Market was valued at USD 1.7 billion in 2024 and is estimated to grow at a CAGR of 10.4% to reach USD 4.5 billion by 2034. This market is growing rapidly, driven by the increasing incidence of breast cancer worldwide, heightened awareness about early detection, proactive government initiatives, and advancements in imaging technology. Digital mammography allows healthcare providers to capture high-resolution images of breast tissue, which aids in early detection and diagnosis of breast cancer. This technology is widely used in clinical environments such as hospitals, diagnostic centers, and specialty clinics. Leading companies in the sector include GE Healthcare, Hologic, Siemens Healthineers, Fujifilm Holdings, and Koninklijke Philips. The market primarily focuses on devices such as full-field digital mammography (FFDM) and 3D tomosynthesis systems, which improve diagnostic accuracy, reduce radiation exposure, and enhance patient outcomes.

The adoption of digital and AI-powered mammography systems has seen a significant rise, aided by government-supported screening programs and continuous advancements in imaging technology. With a growing emphasis on patient-centered care in the healthcare industry, digital mammography is becoming the preferred choice due to its higher image accuracy, reduced diagnostic errors, and enhanced patient comfort. Additionally, the rising prevalence of breast cancer underscores the need for early and accurate detection to improve clinical outcomes.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.7 Billion |

| Forecast Value | $4.5 Billion |

| CAGR | 10.4% |

In 2024, 2D full-field digital mammography tomosynthesis segment was valued at USD 1.1 billion and is expected to grow at a CAGR of 10.2%, to reach USD 2.9 billion by 2034. This technology is integral to breast cancer diagnosis, providing high-resolution digital images that help radiologists detect subtle abnormalities such as microcalcifications and small masses. The increased use of integrated imaging solutions, AI-driven diagnostics, and comprehensive breast cancer screening programs is contributing to the growth of this segment. Enhanced clarity of images helps detect early-stage breast cancer, improving the chances of successful intervention and patient outcomes.

The hospitals segment held 48.5% share in 2024. The hospital segment holds the largest share due to its advanced imaging infrastructure and the presence of skilled radiologists who play a vital role in breast cancer screening and diagnosis. Hospitals are central to breast cancer treatment, which drives the demand for multimodal imaging systems and AI-integrated digital mammography. Furthermore, the development of healthcare infrastructure in emerging markets, especially in regions like Asia-Pacific, the Middle East, and Africa, is accelerating the adoption of advanced mammography technologies within hospital settings, including both 2D and 3D tomosynthesis systems.

U.S. Digital Mammography Market was valued at USD 630.5 million in 2024, with growth largely driven by the increasing prevalence of breast cancer in the country. As the demand for early and accurate breast cancer detection rises, the need for advanced diagnostic tools like digital mammography is growing. This trend significantly contributes to the market's expansion in the U.S.

The key players in the Digital Mammography Market include Siemens Healthineers, GE Healthcare, Koninklijke Philips, Fujifilm Holdings, and Hologic. To strengthen their market position, companies in the digital mammography industry are focusing on a few key strategies. One approach is the continuous innovation of imaging technologies, such as the integration of artificial intelligence (AI) into mammography systems to enhance diagnostic accuracy and speed. Another strategy involves forming partnerships with healthcare providers and organizations to expand the reach of their products and services. Many companies are also investing in developing more user-friendly, patient-centric solutions that reduce discomfort during screenings, which is a growing concern for patients. Additionally, companies are working on expanding their market share by targeting emerging markets, particularly in regions where healthcare infrastructure is rapidly developing.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing incidence of breast cancer across the globe

- 3.2.1.2 Growing awareness regarding early breast cancer detection

- 3.2.1.3 Rising government initiatives and screening programs

- 3.2.1.4 Technological advancements in digital mammography

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of equipment and maintenance

- 3.2.2.2 Radiation exposure concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Rising adoption of AI-powered predictive monitoring tools and AI integration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Supply chain analysis

- 3.7 Future market trends

- 3.8 Pricing analysis

- 3.8.1 By product type

- 3.9 Patent analysis

- 3.10 Gap analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 2D full field digital mammography tomosynthesis

- 5.3 3D full field digital mammography tomosynthesis

Chapter 6 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals

- 6.3 Specialty clinics

- 6.4 Diagnostic centers

Chapter 7 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Allengers

- 8.2 Canon

- 8.3 Carestream

- 8.4 Fujifilm Holdings

- 8.5 GE Healthcare

- 8.6 Genoray

- 8.7 Hologic

- 8.8 IDETEC Medical Imaging

- 8.9 IMS Giotto

- 8.10 Koninklijke Philips

- 8.11 Planmed

- 8.12 Siemens Healthineers

- 8.13 SINO MDT

- 8.14 SternMed

- 8.15 Trivitron Healthcare

- 8.16 Vannin Healthcare

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 132 Pages

- 納期

- 2~3営業日